Quick Answer

Solo founders should meet any director requirements for their entity and jurisdiction, then use a Personal Risk Council for informal, nonbinding decision support. Formal directors handle governance, approvals, and required records. A Personal Risk Council is not a legal substitute for a board, but it can pressure-test assumptions on pricing, hiring, contracts, cash risk, and strategy.

Your Business-of-One Doesn't Need a Board. It Needs a Personal Risk Council.#

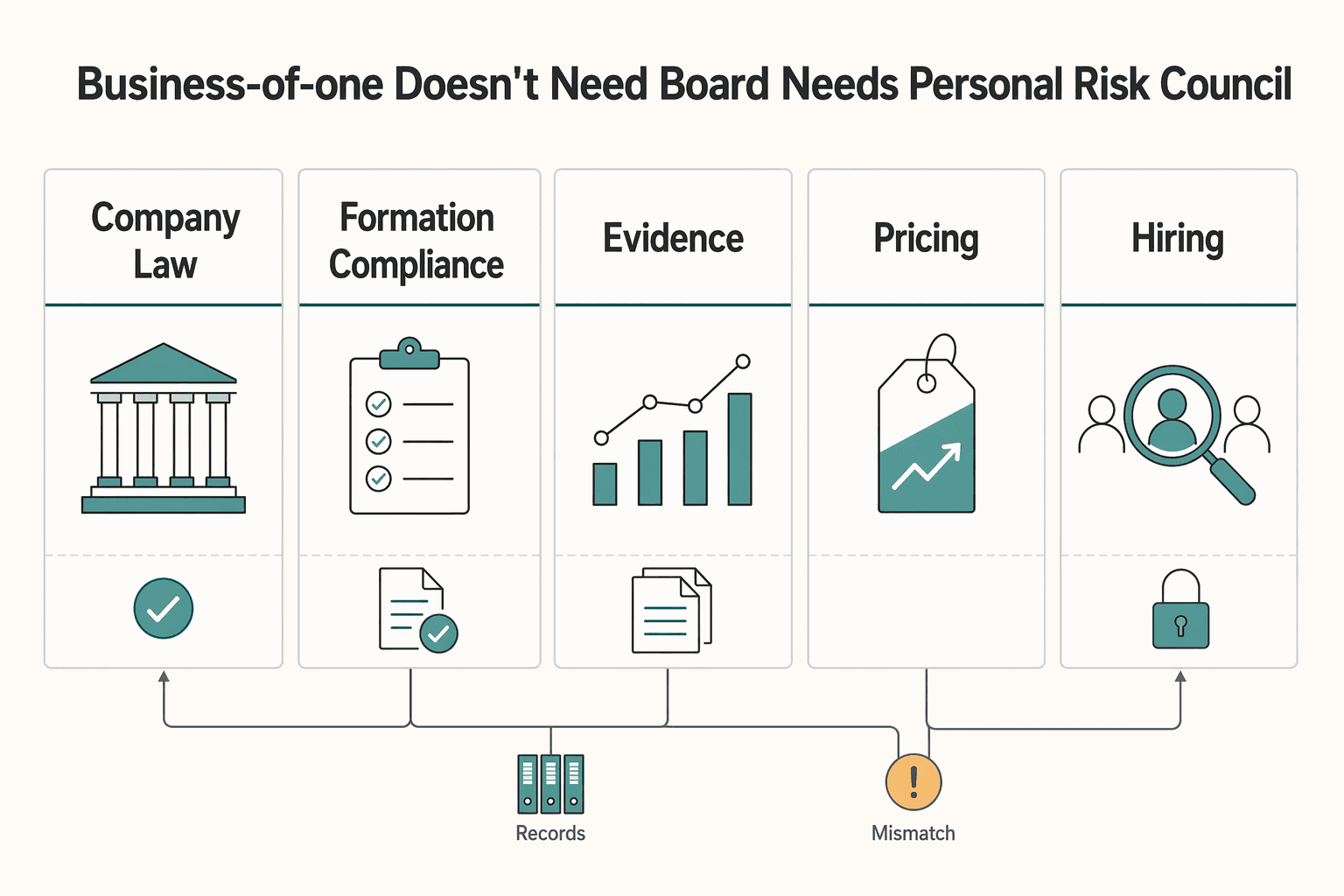

When people tell you to appoint a board of directors, separate the problem first: legal compliance or decision quality. If you need to meet formation and governance formalities, handle the director requirements for your entity and jurisdiction. If you need better judgment under uncertainty, build an informal Personal Risk Council to pressure-test your thinking.

| Need | Channel | Article guidance |

|---|---|---|

| Company law | Formal director work | Handle the director requirements for your entity and jurisdiction |

| Formation compliance | Formal director work | Meet formation and governance formalities |

| Required records | Formal director work | Keep your documentation clean, including resolutions where applicable |

| Pricing | Advisory challenge | Build advisory challenge around your assumptions |

| Hiring | Advisory challenge | Build advisory challenge around your assumptions |

| Contracts | Advisory challenge | Build advisory challenge around your assumptions |

| Cash risk | Advisory challenge | Build advisory challenge around your assumptions |

| Strategy | Advisory challenge | Build advisory challenge around your assumptions |

A formal board is a governance body with oversight and direction responsibilities. It is expected to act in the company's best interests rather than run day-to-day operations. A Personal Risk Council is different. It is an informal advisory mechanism, not a legal substitute for a board, and it cannot satisfy statutory director requirements.

Use this quick lens:

- If the need is company law, formation compliance, or required records, do the formal director work your entity requires and keep your documentation clean, including resolutions where applicable. See A Guide to Board Resolutions for a Delaware C-Corp.

- If the need is stronger calls on pricing, hiring, contracts, cash risk, or strategy, build advisory challenge around your assumptions.

In many cases, both tracks matter, but they solve different problems. Compliance protects the legal structure. Advisory challenge protects you from the echo chamber of one. If you are still confirming your structure, start with Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers and, if relevant, Delaware C-Corp vs. Wyoming LLC: Choosing a US Business Entity.

One caution: copying big-company board habits does not automatically improve decisions. In formal boards, heavy reporting can bury critical issues and crowd out real strategic discussion. For a solo operator, the equivalent is producing tidy updates for yourself while no one challenges the underlying assumptions. Keep the legal formalities clean, then build separate advisory pressure-testing. That distinction sets up the directors-versus-advisors decision in the next section.

If you want a deeper dive, read Do Solo Founders Need Directors and Officers (D&O) Insurance?.

Directors vs. Advisors: Understanding the Difference#

Directors are tied to legal authority and governance formalities. Advisors challenge your assumptions so your decisions improve.

A Board of Directors is the formal governance body. Boards and advisory groups are not interchangeable. The board sits on the authority side of the line: approvals, oversight, control, and the duties tied to that role. In U.S. corporate law framing, control and fiduciary accountability are linked, so board composition is a legal governance issue, not just presentation. Requirements vary by entity type and jurisdiction, so confirm local rules before filing.

A Personal Risk Council sits on the other side of that line. Use it for strategic pressure-testing, not as a legal substitute. Bring questions here about pricing, hiring, contracts, market direction, and risk calls, while keeping binding governance actions in the proper channel.

| Founder question | Board of Directors | Personal Risk Council / Advisory Board |

|---|---|---|

| Who has authority to act at the governance level? | Formal authority under governing law and company documents. | No governance authority in this model; advisory input only. |

| Whose interests are they expected to protect? | The role is tied to fiduciary accountability and acting in the company's interests. | They provide candid advice but are not the formal governance body. |

| What is the liability exposure? | Legal exposure can attach because this role is part of control and oversight. | Do not assume advisor roles carry zero exposure in every context; keep the role clearly advisory. |

| Who keeps final decision control? | The board is the channel for binding governance decisions. | You decide whether to accept or reject the advice. |

| What documentation burden comes with it? | Formal governance records matter for binding actions, including resolutions where applicable. | Set the advisory scope in writing and keep basic records as needed. |

A practical split helps keep you out of trouble:

- If the question is "What must we approve, authorize, file, or record?", treat it as director work.

- If the question is "What am I missing, mispricing, underestimating, or rationalizing?", bring it to advisors.

If you are still choosing your structure, decide that first because governance obligations can follow entity design. Start with Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers and, where relevant, Delaware C-Corp vs. Wyoming LLC: Choosing a US Business Entity. When you need formal governance action, keep the record clean. That includes resolutions where applicable, as covered in A Guide to Board Resolutions for a Delaware C-Corp.

The operating risk to avoid is blending the two tracks. Problems start when advisory arrangements function like hidden governance, or when real governance decisions are handled informally without proper records. Keep legal authority where the law expects it, and keep advisory challenge separate.

We covered the investor-side expectation piece in The FinTech Pitch Deck Anatomy VCs Actually Underwrite.

The 3-Person Framework for Your Personal Risk Council#

If you want an advisory group that improves decisions, build for coverage, not prestige. A simple starting point is one advisor for your numbers, one for market direction, and one for your decision logic. This is not a legal requirement and not a substitute for formal governance. It is a practical way to reduce solo decision risk.

The goal is not impressive names. The goal is to pressure-test major decisions from three different angles before you commit money, time, or reputation.

| Advisor | Decision responsibility | When to involve them | Expected output |

|---|---|---|---|

| Financial Realist | Test pricing, cash flow, concentration risk, margins, and downside assumptions | Before price changes, new fixed costs, hiring, long contracts, or heavier dependence on one client | A clear go/no-go/revise view, assumptions that need proof, and downside scenarios to model |

| Industry Veteran | Test market direction, offer strategy, positioning, and timing | When demand shifts, competitors repackage offers, you explore a new niche, or you add a service/product | A sharper read on what buyers are rewarding, what is noise, and where the offer should or should not move |

| Trusted Outsider | Test bias, weak logic, hidden attachment, and overconfidence | When you feel unusually certain, defensive, rushed, or pulled by a "can't miss" move | Better questions, explicit tradeoffs, and a plain-language stress test of your reasoning |

One useful habit from formal governance can help here, with limits. The OCC Corporate and Risk Governance handbook (Version 2.0, July 2019) is written for bank examiners, not solo operators. Still, two practices are worth adapting: review materials before decisions, and ask for explanations rather than conclusions alone. For your council, that means sending a short pre-read and asking people to show their reasoning.

Financial Realist#

This seat exists to stop optimism from quietly rewriting your math. Good challenge sounds like this: "Show the assumptions behind this price change," or "What happens if your largest client pauses for 60 days?" Weak advice is generic caution without a model. It can also sound supportive while ignoring margin, payment timing, and concentration risk.

Bring this advisor in when you need to know whether a move is resilient, not just attractive. Scenario prompts include: "If I raise prices by 15% and lose two smaller clients, do profit and delivery load still improve?" and "At what point does client concentration move from manageable to dangerous?"

Keep accountability with you. Provide one-page inputs before the call, such as revenue by client, utilization, delivery cost, payment terms, and fixed commitments. Then decide.

Industry Veteran#

Use this seat to separate real market change from reactive noise. Good challenge is specific and comparative. It sounds like: "Your buyers want faster outcomes, not more features," or "This offer may work, but this buyer usually does not buy it this way." Weak advice is nostalgia, broad anecdotes, or claims not tied to buyer behavior.

Bring this advisor in when you rework an offer, reposition, enter a new segment, or react to a competitor. Scenario prompts include: "Top clients keep buying one service. Is productizing it expansion or avoidance?" and "If AI compresses part of my service, what should I stop, keep, or rebundle over the next 12 months?" Use their pattern recognition, but keep final strategy ownership yourself.

Trusted Outsider#

This is the seat that catches the story you are telling yourself. Good challenge sounds like: "Why must growth look like this?" or "Are you solving a client problem or protecting an identity?" Weak advice is empty contrarianism or motivation without a real test of your reasoning.

Bring this advisor in when there is emotional heat around a decision. Scenario prompts include: "Is dropping smaller clients a strategy move or a burnout response?" and "What evidence would prove my 'scalable offer' thesis wrong?"

Keep the documentation line clean. Advisory conversations should have dated decision notes that capture the assumptions challenged and what changed. If your business has formal governance, move formal company actions into those formal records (for example, board and committee minutes), as covered in A Guide to Board Resolutions for a Delaware C-Corp.

If you are still confirming entity setup before you worry about governance mechanics, align that first with Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers and Delaware C-Corp vs. Wyoming LLC: Choosing a US Business Entity.

Get role clarity before outreach. Clear seats make better asks and help you avoid building a council that is pleasant, impressive, and strategically weak.

Related: How to Build a Strategy-Led Mood Board for Branding Projects.

How to Recruit Your Personal Risk Council#

Recruit for the decision gap, not for prestige. The point is to get advice you can use on a specific risk, then keep only the people who consistently sharpen your judgment. Treat this as a practical process, not legal advice.

Define the gap#

Do not start with names. Start with a one-page intake tied to one decision. If you cannot state the decision clearly, pause recruitment and define it first.

| Intake item | What to define | Examples in the article |

|---|---|---|

| Business risk | What goes wrong if this decision is wrong | Margin pressure; concentration risk; reputational downside; a bad market move |

| Decision type | What decision is actually on the table | Pricing; a hiring commitment; offer packaging; a niche shift; a partnership |

| Required perspective | Which lens is missing right now | Financial challenge; market pattern recognition; an independent logic test |

| Expected contribution | What output you need | A go/no-go/revise view; assumptions to test; missed alternatives; a downside case |

Use this intake framework:

- Business risk: What goes wrong if this decision is wrong, such as margin pressure, concentration risk, reputational downside, or a bad market move?

- Decision type: What decision is actually on the table, such as pricing, a hiring commitment, offer packaging, a niche shift, or a partnership?

- Required perspective: Which lens is missing right now, such as financial challenge, market pattern recognition, or an independent logic test?

- Expected contribution: What output do you need, such as a go/no-go/revise view, assumptions to test, missed alternatives, or a downside case?

Before outreach, run a quick pre-brief on yourself: confirm the decision, the stakes, your current evidence, and the one or two questions you want challenged. Planning failures usually produce vague, low-value conversations.

Search in circles, then screen hard#

A concentric search is one practical way to source candidates if you apply consistent quality filters in every circle.

| Search circle | Where to look | What to confirm before serious outreach | Main red flag |

|---|---|---|---|

| Inner circle | Former managers, mentors, senior peers, long-term collaborators | Relevance to this decision, communication style, and willingness to challenge assumptions | They support you, but avoid real pushback |

| Middle circle | Trusted introductions from clients, investors, founder peers, professional communities | Similar checks, plus a credible reference on how they work in real conversations | Strong reputation, unclear working behavior |

| Outer circle | Authors, speakers, niche experts you know through their work | Narrow fit to your exact gap and signs they can engage specifics | Brand signal without decision fit |

Keep information-sharing risk in view. Before sending detailed materials, check whether incentives, overlapping relationships, or role conflicts could affect advice quality.

Make the ask small and specific#

Start with one defined conversation, not an open-ended advisory role. A concise outreach note can include:

| Ask element | What to include |

|---|---|

| Reason | A specific reason you chose them |

| Scope | A one- to two-sentence scope tied to your current decision |

| Compensation | Clear compensation intent |

| Next step | A low-commitment next step with flexible format and timing ([call/video/in-person], [time window]) |

Brief them enough to engage the decision well, but avoid unnecessary sensitive detail in the first note or first call.

Confirm fit after the first call#

Treat the first call as a fit test. Continue only if they engaged the real issue, improved your questions, and clarified tradeoffs.

If there is fit, set lightweight operating norms: agenda before each session, a short decision log after each session, clear action ownership on your side, and a review checkpoint after a few interactions.

Keep records clean. Maintain a simple decision log so advice, assumptions, and actions are easy to review. If you need governance context as decisions become formal actions, see A Guide to Board Resolutions for a Delaware C-Corp. If you are still deciding your entity path, align that first with Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers and Delaware C-Corp vs. Wyoming LLC: Choosing a US Business Entity.

For a step-by-step walkthrough, see How to Create a Financial Forecast for a Funding Round.

Before your first advisor call, set clear boundaries for confidential information so conversations stay practical and protected: Create a simple NDA draft.

Conclusion: Your Greatest Asset is a System for Better Decisions#

The point of this approach is simple: separate legal governance from decision support, then get deliberate about the second one. Paying for advice, structuring the engagement, and making the ask professionally add up to more than a series of helpful conversations. They change how you operate.

Be clear about the difference. At the board level, governance is about major policy and strategic direction, not day-to-day operations. A Personal Risk Council is not a legal substitute for a board. It is a practical way to build strategic discipline into how you decide.

This is not about adding bureaucracy or giving up autonomy. It is about protecting your autonomy by making sure your biggest calls are pressure-tested before you commit. Done well, that can give you three things:

- Objective Scrutiny: You make yourself explain why you are making a particular choice, so assumptions can be challenged before execution.

- Strategic Filtering: A simple two-by-two lens, decision frequency and familiarity against decision scope and impact, helps separate routine calls from true strategic decisions.

- Better Risk Decisions: By limiting which calls count as strategic, you can create time to prepare for high-impact choices and help reduce avoidable mistakes.

In the end, strong leaders are not the ones who have all the answers. They are the ones who build a reliable way to get better answers. Your Personal Risk Council can be that mechanism. It can turn solo decision pressure into a more disciplined advantage.

You might also find this useful: Best Mood Board Tools for Client Approval and Scope Control.

Once your decision system is in place, tighten execution with payment operations designed for independent professionals working across borders: Explore Gruv for freelancers.

Frequently Asked Questions

What is the real difference between a director and an advisor for a solo founder?

A director is part of the formal governing body and is legally responsible for governance, fiduciary, and strategic oversight. A Personal Risk Council provides informal, nonbinding input and is not a formal governing body. If advice becomes a vote-required action, record it through your formal governance process.

Do I need a board at all?

For nonprofits, yes: the board is the legal governance body, and IRS guidance generally expects at least three board members. Membership structure also matters, and state requirements vary. If you are appointing a board only for optics, confirm the actual governance requirement first.

How do I create a Personal Risk Council without making it heavy?

Keep it narrow and explicitly informal. Use it for nonbinding perspective between formal governance checkpoints. Keep vote-required decisions in the board process, including annual budget approval and other matters requiring votes.

What skills should my advisors have?

Choose people for decision quality and real engagement, not titles. High-status people without action and enthusiasm can be a detriment. If you are assigning formal board seats, keep governance basics documented in bylaws, including service terms.

How do I know an advisor is actually a good fit?

A good advisor improves decision quality without blurring governance roles. Directors handle formal vote-required actions, while informal advisors provide input. If roles start to blur, tighten role definitions in your bylaws and governance process.

How should I ask someone to join my council?

Start with one specific issue and define the role up front. If it is an informal advisory role, set expectations as nonvoting input. If it is a director role, follow your bylaws for nomination or election, term, and meeting cadence.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/sites/default/files/manual/PSC%20Manual%20Ap...trusted

- canr.msu.edu/news/understanding-roles-board-of-directors-...trusted

- corpgov.law.harvard.edu/2016/09/08/principles-of-corporate-governancetrusted

- courts.delaware.gov/Opinions/Download.aspxtrusted

- dot.ca.gov/-/media/dot-media/programs/construction/docu...trusted

- ecfr.gov/current/title-12/chapter-I/part-30/appendix-...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- federalregister.gov/documents/2022/09/30/2022-21020/beneficial-o...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Delaware C-Corp vs Wyoming LLC for Your Next Growth Stage

Choosing between a Delaware C-Corp and a Wyoming LLC is a stage-fit decision, not a state popularity contest. For `delaware c corp vs wyoming llc`, the real question is which structure you can run cleanly over the next 12-24 months while keeping room to scale.

Board Resolutions for a Delaware C-Corp That Stand Up to Review

Your filing is done, but the company still needs the meeting mechanics it will run on. In practice, your **bylaws** and **certificate of incorporation** can set where stockholder meetings happen, and if they do not, the board sets that under § 211(a)(1).