A decision method for noisy freelance outcomes#

You do not need motivation here. You need a decision method you can trust when freelance outcomes are noisy. Results are shaped by factors outside your control, so a good choice can look bad for a while, and a weak choice can look good in the short term.

Use this article as a practical decision method: judge the quality of the choice, not just the short-term result. In practice, that means you:

- write down your key planning answers before you act

- set your commitment period at the start

- define failure criteria in advance

One rule up front. If you are hedging, name it. If you are still signaling that you are just “open to opportunities,” write down your commitment period and your failure criteria at the start. Your first checkpoint is simple: how long you are committing and what would show the experiment is not working.

You also need enough visibility for the market to respond. If close contacts do not know you freelance, potential clients are likely to miss it too. Balance visibility with capacity: update your profile, tell your network, use the freelancer label consistently, and review what happens. If you want a lightweight way to track those calls, see How to use a 'Decision Journal' for your freelance business.

What to prepare before you place any career bet#

Before you act, write your decision inputs in one place. The point is not perfect prediction. The point is a choice you can defend with written inputs instead of mood, hope, or one noisy month.

Write your current picture first.

Start with what is true today, in plain language, then write down your answers to:

- How much money do you want to make?

- How many months will you commit to freelancing before review?

- What factors would tell you this experiment is failing?

If you are hedging, name it directly. People can often sense that lack of commitment.

Write it down, not from memory.

Keep these answers written from the beginning so you can review the same criteria later instead of relying on memory. The format can be simple, but it should be easy to revisit.

Log downside drivers before upside stories.

Define failure factors before you start, not after a rough stretch. External variables like your network, the market, and industry cycles will still affect outcomes, so predefining failure signals helps you evaluate results more clearly.

Precommit the review call.

Before you start, write a short precommitment block with your commitment period, income target, failure factors, and review point.

Keep this brief so you will actually use it. Once you commit, follow through with visible signals, such as updating your LinkedIn profile and emailing your network. If you want a clean record for the review, use a short decision journal.

Translate Thinking in Bets into freelance decisions that matter#

Use this shift for every major move: do not ask whether you can predict the outcome, ask whether your choice is strong given today’s evidence. Your job is to make a defensible decision under uncertainty, then review the process without rewriting what you knew at the time.

Use probability, payoff, and uncertainty together.

Turn the core ideas into working decision lenses you can use on real business choices:

- Probability: your best estimate of how likely an outcome is, for example rate acceptance, renewal, or scope approval

- Payoff: what you gain or lose if it happens, such as margin, time, stress, payment speed, or added admin and compliance load

- Uncertainty: what you cannot verify yet

Use all three together. A modest upside with controlled downside is often a better bet than a high-upside story built on unverified assumptions.

Judge process before outcome.

Judge process before outcome so you do not fall into resulting.

After each meaningful decision, run this check:

- What did you know when you decided?

- What did you assume because evidence was missing?

- Did your choice follow the evidence you had, or pressure in the moment?

If you can point to records, constraints, and a pre-set review trigger, your process is improving even when short-term results are mixed.

Apply the lens to the decisions that move your business.

Apply the same lens to the decisions that actually move your business:

| Decision type | Upside case | Downside case | Evidence to verify before acting |

|---|---|---|---|

| Pricing change | Higher revenue per project and better fit | Lower acceptance rate or short-term cash pressure | Close rate, capacity, payment history, client value feedback |

| Client retention | More recurring revenue, fewer sales cycles | Scope drift, late payment, dependence on one account | Contract terms, invoice aging, revision volume, communication pattern |

| Specialization | Clearer positioning, stronger referrals | Narrower pipeline during transition | Lead sources, win rate by niche, sample quality, documented demand signals |

| Cross-border expansion | Access to new clients | Acting on outdated or unverified guidance | Source authenticity (europa.eu), Explanatory Notes file/date checks, current-rule verification |

If downside depends on compliance, verify first and scale second.

Treat expansion as a verification sequence.

When a move touches a new geography, treat expansion as a verification sequence, not a market narrative.

- Confirm your source is on the europa.eu domain before you rely on it.

- Save the English Explanatory Notes PDF (1.83 MB) in your decision record.

- Use the listed Other languages (22) versions when stakeholders need non-English review.

- Treat the visible date (30 JULY 2021) as a freshness flag.

- Verify any current requirements in up-to-date official sources before acting.

If you use the EU OSS Guides page in your decision record, do not treat the listed Explanatory Notes as fully current for 2026 without a fresh check. For privacy work tied to expansion, review this GDPR checklist. Related: A freelancer's guide to "Thinking".

Build your minimum viable decision memo#

Before you change pricing, accept a client, or enter a new market, fill a one-page memo. Keep it short enough to use and specific enough to revisit later.

Fill the memo before you act#

Capture what you know now, what you still need to verify, and when you will review the decision. If compliance is involved, mark rules that can change as Current requirement pending official or counsel verification. Use a consistent set of prompts so each decision is comparable:

- Decision: What exact choice are you making right now?

- Options: What are your real alternatives, including waiting or running a small test?

- Assumptions: What are you currently treating as true without full proof?

- Base rate: What happened the last few times you made a similar move?

- Expected upside: What improves first if this works?

- Expected downside: What gets riskier, slower, or harder to unwind if you are wrong?

- Evidence needed before go: Which document or confirmation should exist before launch?

- Kill or pause trigger: What signal means stop, renegotiate, or stay in test mode?

- Review date: When will you review outcome versus what you documented?

- Confidence: How confident are you, as a rough estimate?

- What would change my mind: What new fact would make you pick a different option?

Add a verification block with clear ownership#

A memo is easier to review when each check has an owner and a visible go or no-go signal. Treat this as a checklist, not legal advice.

| Area | What to verify | Go/no-go signal | Owner |

|---|---|---|---|

| Contract and scope | Scope, payment terms, timing, termination language, and delivery expectations | Go if written terms match expected work; no-go if key terms are still informal | You |

| Privacy and data handling | Whether personal data is involved and which privacy checks apply. Current privacy check pending counsel verification | Go if responsibilities and current requirements are confirmed in writing; no-go if handling is unclear | You, plus client contact or adviser if needed |

| Invoicing and taxes | Customer type, service type, invoice setup, and which tax checks apply. Current tax check pending tax-advisor verification | Go if invoice setup matches verified treatment; no-go if treatment cannot be explained | You or bookkeeper |

| Tax form status | Which tax form the payer requests and whether that request matches your documented status. Current payer tax-form requirement pending payer or tax-advisor verification | Go if status is resolved in writing; no-go if request conflicts or stays vague | You and payer contact |

| Payment records | Whether proposal, invoice, payment confirmation, and bank record align | Go if records agree or differences are explained; no-go if money flow cannot be traced | You |

Run a records checkpoint before scale-up#

Before you expand anything, run a records checkpoint: records should align, exceptions should be explained, and unresolved conflicts should pause scale-up.

Compare the proposal or contract, invoice, payment confirmation, bank or processor entry, and accounting record if kept. If amounts differ, log why, for example fee, partial payment, refund, withholding, or credit. If you cannot trace payment to invoice and invoice to approved scope, pause.

Review process first, then archive for reuse#

On the review date, judge the decision against what you documented at the start, not against whether the short-term outcome was lucky or unlucky.

Close each memo with a short note on what happened, what you learned, and what you will verify earlier next time. Archive the memo and supporting records together so future decisions can build on prior notes.

For a step-by-step walkthrough, see How Availability Heuristic Distorts Risk Assessment for Freelancers. Before you place the bet, tighten scope, payment terms, and change-request boundaries with this freelance contract generator.

Price upside and downside before you act#

Pricing changes create the kind of upside that makes weak assumptions feel reasonable. Use the same sequence every time: clear downside risk first, model upside second, test on a bounded slice third, then commit. If a pricing change creates unresolved compliance risk, pause.

Gate downside risk before you model upside#

Separate commercial risk from compliance risk, then require document-backed checks before launch.

| Risk type | What to verify now | What pauses launch | Evidence to keep |

|---|---|---|---|

| Commercial | New price fit for buyer, scope, and close process | You cannot explain who pays more, why they still buy, or what volume drop you can absorb | Prior proposals, win or loss notes, baseline close rate, average invoice value |

| Compliance | Payer form status: whether a W-9 request matches your status or a W-8BEN is needed to establish foreign status for withholding purposes | Payer paperwork is vague, contradictory, or informal | Completed form, payer confirmation, contract record |

| Compliance | Cross-border checkpoints: whether FEIE or FBAR review is relevant for your facts | You are relying on unverified residency, exclusion, or reporting assumptions | Guidance used, account list, residency dates, adviser note if used |

| Compliance | Invoice and privacy obligations: whether EU VAT invoice requirements or GDPR accountability checks apply | Required invoice fields or data-handling responsibility is unclear | Invoice template, Article 226 field check, client instructions, data-handling note |

If your work is cross-border, use written checks, not memory. For example, FEIE requires foreign earned income, a foreign tax home, and qualifying status. One path uses 330 full days in 12 consecutive months. FEIE also does not remove the requirement to report excluded income on a U.S. return, and for self-employed taxpayers it does not reduce self-employment tax.

For FBAR, the trigger is aggregate foreign account value over $10,000 at any time in the year, with an annual due date of April 15 and automatic extension to October 15.

Model upside in a three-line template#

Keep the model short enough to use before acting.

- Conservative: Estimate close rate, average invoice value, and payment timing under normal friction. Add one key assumption and one validation metric.

- Expected: Estimate the same three outcomes using your recent base rate. Add one key assumption and one validation metric.

- Optimistic: Estimate the same three outcomes if adoption is smooth. Add one key assumption and one validation metric.

If your expected case only works with flat close rate, no scope pressure, and no payment delay, it is probably an optimistic case in disguise.

Test against an unchanged baseline#

Do not roll out to every lead at once. Keep one unchanged baseline cohort and one changed cohort, then compare like-for-like conditions.

Compare the outcomes pricing should move:

- proposal-to-close rate

- average invoice value

- days to payment

- scope pushback or revision pressure

Precommit your rule before the first test quote: continue only if invoice-value gain survives any loss in close rate, payment timing, or rework cost. Stop if results become noisy from confusion, renegotiation, or weak records. A no-winner result is still useful because it tells you not to scale yet.

Precommit the tradeoff sentence#

Write this before launch: I am accepting [specific commercial risk] to pursue [specific upside] over [review window], and I will pause immediately if [compliance assumption or document] is not confirmed.

If you cannot complete that sentence without guessing about FEIE, FBAR, W-9 versus W-8BEN, VAT invoice requirements, or GDPR responsibility, the right decision is pause.

Set kill criteria for clients, niches, and offers#

Write your keep, renegotiate, and exit rules down before the next review date. Move lanes only on repeated patterns, not one lucky or bad outcome.

Define lane rules you can execute#

Use this table in every review so you know what to check, what proof you need, and what to do next.

| Trigger category | Keep | Renegotiate | Exit | Required evidence |

|---|---|---|---|---|

| Delivery scope control | Scope stays inside signed terms and approved changes. | Scope drift appears after you tighten approvals, revision limits, or change-order steps. | Scope drift continues across review cycles after reset. | Contract or SOW, change-request log, revision log, meeting notes |

| Payment reliability | Payments stay predictable on agreed terms. | Payment timing slips after deposit, milestone, or due-date tightening. | Slow-pay pattern persists after reset. | Invoice issue, due, and paid dates, DSO trend, promise-to-pay log |

| Margin health after process fixes | Margin holds after normal process cleanup. | Margin weakens but may recover after briefing, revision, or process fixes. | Margin remains structurally weak after fixes across review cycles. | Estimated versus actual effort, rework log, margin notes |

| Pipeline fit quality | Leads in this segment continue to fit your offer. | Fit quality drops, with more friction, objections, or discount pressure. | Poor fit persists after positioning or qualification changes. | CRM segment notes, win or loss notes, call patterns |

| Compliance admin load | Admin remains manageable for delivery. | Admin load rises enough to justify term or process changes. | Admin burden keeps outweighing upside after reset. | Current payer, tax, and privacy documents, invoicing checklist, compliance task log |

If you cannot find this evidence quickly, you are deciding from memory and outcome bias.

Require pattern persistence before lane changes#

Do not change lanes on one bad week. For client decisions, log the problem, apply one reasonable fix, then review the next cycle. A one-off issue is a note. A repeated issue after the fix is a signal.

- Scope drift: Treat uncontrolled scope expansion as a trigger only when it repeats after stronger scope controls.

- Payment behavior: Track payment patterns with invoice dates and collection timing. Move lanes when delays persist after terms are tightened.

- Margin erosion: Compare estimated versus actual effort after process fixes. If margin still degrades, treat it as structural.

At each review, record three items: what you changed, what period you reviewed, and whether the pattern improved, stayed flat, or worsened.

Separate client, niche, and offer signals#

Before you kill anything broader than one account, diagnose where the weakness actually lives.

| Level | Signal you are seeing | Action |

|---|---|---|

| Client-level | One account drives scope fights, slow pay, or paperwork drag while similar accounts do not. | Renegotiate or exit that client; keep the niche or offer active. |

| Niche-level | The same segment shows weaker fit and heavier admin across multiple accounts. | Reduce prospecting in that niche until economics or admin improve. |

| Offer-level | Different segments buy the offer, but margin stays weak after process fixes. | Repackage or retire the offer. |

This is where the method stays practical. Diagnose the level of the problem before you cut more than necessary.

Verify current filing rules before final lane decisions#

Do not hard-code old thresholds or form assumptions into your kill rules. Use this checklist and fill values only after verifying current official guidance.

- VAT path: Confirm whether your activity, customer location, and registration status put the work in scope. If EU invoicing applies, check invoice fields against Article 226. If OSS may apply, confirm eligibility and record:

Current threshold pending official or tax-advisor verification. - U.S. payer-document path: Confirm whether the payer needs

Form W-9with the correct TIN or foreign-status documentation such asW-8BENorW-8BEN-E, then verify against the latest IRS forms and instructions. - U.S. reporting path: Confirm current information-return and third-party network reporting rules for your tax year, and record:

Current reporting threshold pending official or tax-advisor verification. Keep a separate note that reporting thresholds do not determine whether income is taxable. - GDPR accountability path, if EU client data is involved: Confirm records are current enough to demonstrate compliance. For a deeper workflow, see GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

Use this rule template at the end of each review:

Unless the client, niche, or offer shows the improvement you named by your next review cycle, and unless the required filing or document check is verified, I will [stop renewing / stop prospecting / retire the offer].

Run a small test before committing fully#

A bounded experiment can work when upside is plausible but outcomes are uncertain. Set the review point before you start, and choose a clear commitment period (in months) before you reassess.

Write the test and cap the downside#

Use one short hypothesis before you act. Write down your answers up front:

- What am I assuming?

- How many months will I commit to freelancing?

- What factors would tell me this experiment was a failure?

- What exact records will I review at the checkpoint?

- When is the review point?

Precommit the review point and hold it. If you cannot pull your decision evidence quickly, tighten the experiment before continuing.

Compare your results to your precommitted criteria#

Change as little as possible during the commitment window, then review with the same criteria you defined at the start. Because freelancing is shaped by your network, market conditions, and other factors outside your control, keep your evaluation practical and explicit.

Avoid hedging during the experiment#

Hedging is a common mistake. If you signal partial commitment, others may read that hesitation too.

Once you commit, take visible execution steps so people know you are available, such as updating your profile and emailing your network.

Pause at the review point and decide#

At the checkpoint, decide based on your written criteria: continue, adjust, or stop. If your evidence is incomplete, clean up the decision trail and rerun a bounded test before expanding. Related reading: Important Conversations for Freelancers Who Need Clear Client Boundaries.

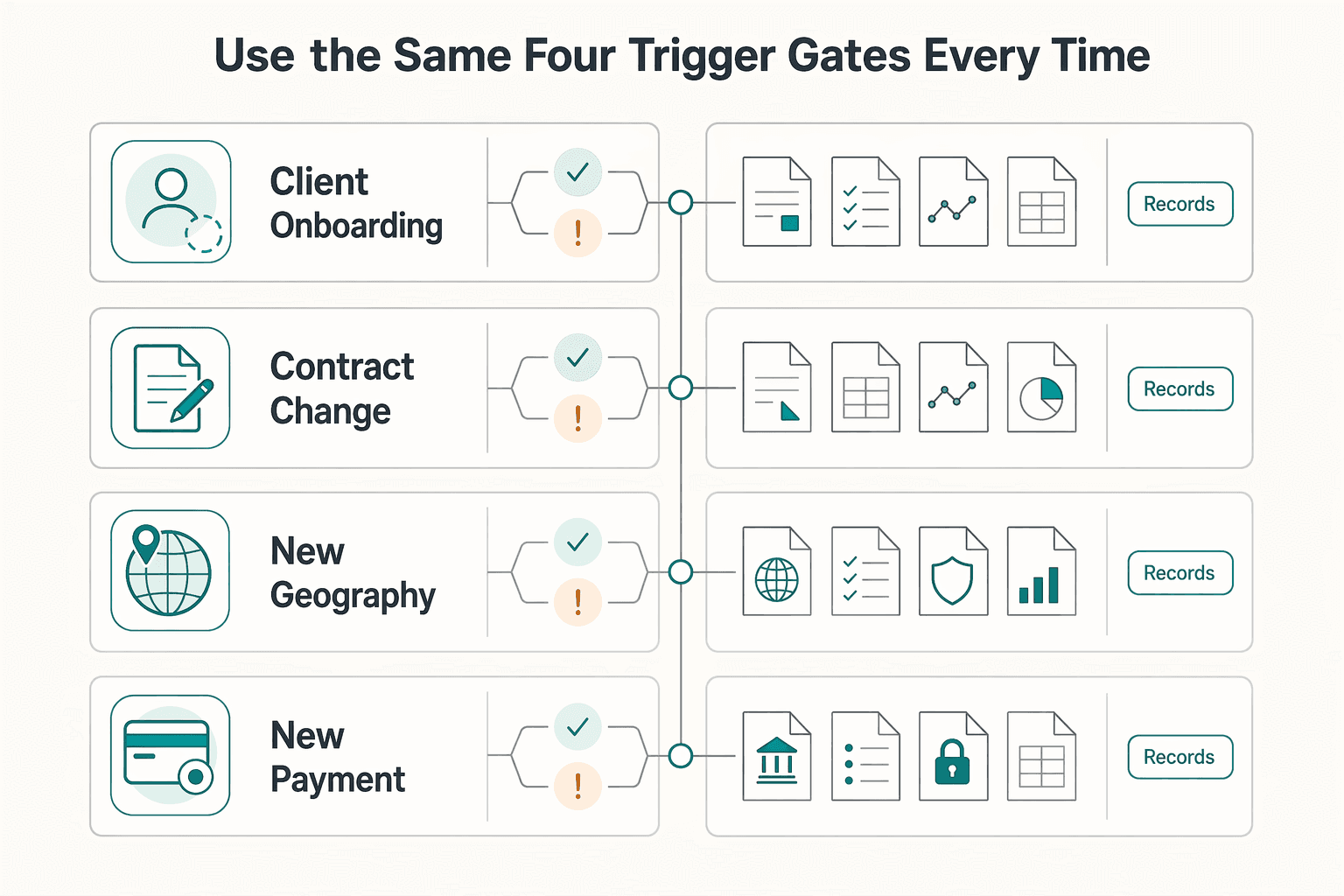

Add compliance gates so growth does not create legal debt#

Growth usually goes wrong at the edges, where a new client type, geography, or payment flow slips past your usual checks. Before any growth move goes live, pass a documented compliance gate or treat it as not ready. If proof is missing, stale, or hard to trace, pause the launch even if the upside looks strong.

Use the same four trigger gates every time#

Run this pre-launch checklist for each trigger: onboarding, contract change, new geography, and new payment flow. For each one, record a go or no-go question, a named owner, and an exact record location.

| Decision type | Go/no-go question | Required proof | Review owner | Record location |

|---|---|---|---|---|

| Client onboarding | Can you show what personal data you collect, why, and whether GDPR territorial scope needs review? | Intake record, data-use note, GDPR scope note if EU exposure may apply, review date | You or privacy or legal reviewer | Compliance/Clients/[Client]/Onboarding |

| Contract change | Does this revision change data use, payment terms, jurisdiction, or contractor status enough to require a fresh check? | Redline, approval note, tax or data impact note | Contract owner | Compliance/Contracts/ClientName/Version-YYYYMMDD |

| New geography | Have you verified whether this market changes data, tax-form, or reporting workflows? | Geography memo, jurisdiction check, Current threshold pending official or tax-advisor verification where cutoffs may apply | You plus accountant or legal reviewer as needed | Compliance/Geographies/[Country-or-Region] |

| New payment flow | Does this rail or provider require different identity, tax, reporting, or account-tracking records? | Provider requirement copy, form-selection note, account inventory update, submission receipt | Finance or ops owner | Compliance/Payments/[Provider-or-Rail] |

Quick test: you should be able to answer each gate quickly from saved records.

Scope identity and AML checks to the actual institution and jurisdiction#

Do not use one universal AML or KYC checklist. Keep checks tied to the specific bank, platform, payment provider, and jurisdiction involved in this launch.

Save three artifacts for each institution request:

- the exact request

- the documents or details you submitted

- the completion result, accepted, rejected, or pending

If two providers ask for different verification, keep separate files. One completed check does not automatically clear another provider.

Build evidence packs by workflow#

Build the evidence pack around the actual workflow, not around a vague label like “tax” or “privacy.”

For GDPR, start with a territorial-scope decision note: does your processing relate to people in the Union because you offer goods or services to them or monitor behavior there? If scope may apply, keep the Article 3 scope note plus your data-purpose record and accountability evidence. For a deeper operational checklist, use GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

For U.S. tax-form selection, treat it as a requester-driven workflow. Store the trigger request, submitted form, and submission date:

Form W-9: when a requester needs your correct TIN for information reportingForm W-8BEN: when a withholding agent or payer requests foreign beneficial-owner documentation

For contractor reporting, document lane selection before filing. Keep proof for payer type, payment rail, totals, and filing decision:

- qualifying nonemployee compensation may require

Form 1099-NEC - card or third-party network payments route to

Form 1099-Kand are excluded from1099-NEC/1099-MISC - record

Current reporting threshold pending official or tax-advisor verificationfor payment-year-sensitive limits - if

1099-NECapplies, include your filing calendar andCurrent filing deadline pending official or tax-advisor verification

For foreign-account reporting, keep FBAR and Form 8938 as separate workflows with separate evidence files:

- FBAR: FinCEN Form 114 via BSA E-Filing

- Form 8938: separate IRS threshold-based workflow

- core artifact for both: current account inventory, institution, account type, holder, country, balance history

Apply one strict readiness rule#

If required compliance proof is missing, stale, or untraceable to an owner and record location, pause rollout and fix records before scaling.

Use payment and record systems as evidence not guesswork#

Once the compliance gate is clear, the next risk is interpretive. Payment issues can become expensive when you rely on memory instead of records. If you cannot prove what was agreed, what was completed, and what your payment system recorded, pause interpretation.

Anchor every payment call to the contract#

Before you label a payment as late, disputed, or risky, open the signed contract and any approved changes. That contract is your enforceable baseline.

Check these in order:

- What exactly did you agree to deliver?

- What counts as completion or acceptance?

- What event triggers payment, and on what timeline?

If payment depends on signoff, approval, or final invoicing, a delay may be a process gap rather than a breach. Keep the signed agreement, SOW, change approvals, invoice, and acceptance message in one file set so you can answer those three questions quickly.

Map each decision to one record source#

Assign one source of truth per decision, then attach the minimum supporting record you would need to defend that decision later.

| Decision question | Single source of truth | Required supporting record |

|---|---|---|

| What work was agreed? | Signed contract or approved change record | Final signed version, scope-change record, invoice terms |

| Was work completed to the agreed standard? | Delivery and acceptance record | Delivered file, timestamp, client acceptance message, revision log if relevant |

| Was payment initiated, settled, or still pending? | Payment provider record | Transaction ID, invoice number, amount, payment proof, date |

| Is this a normal exception or a dispute? | Client exception note | Communication timeline, referenced contract clause, refund or dispute notice if any |

Pause rule: if records conflict, stop the decision and reconcile first. For example, webhook events can confirm payment-system events, but they do not prove contractual completion.

Choose tools for evidence clarity and auditability#

Choose tools for record quality, exportability, and maintenance burden, not just convenience. Your setup can be simple, but it must clearly show income and expenses and preserve supporting details like payee, amount, proof of payment, and date.

Prefer tools that preserve IDs and timestamps. If you use Stripe, create one PaymentIntent per order or customer session so attempt history stays tied to that order or session. If you use webhooks, retain event IDs or synced logs because Stripe event retrieval via API is limited to 30 days. If EU VAT invoice rules apply, use invoicing workflows that capture required Article 226 particulars instead of ad hoc documents.

Run a pre-growth checkpoint, then scale only if records are clean#

Before scaling a new offer, payment rail, or client segment, run this checklist:

- open exceptions with no written resolution

- jobs with unclear completion or acceptance evidence

- payment-state gaps where invoice, provider, and bank or webhook records do not match

Record transactions frequently, ideally daily, not in delayed catch-up batches. If gaps remain, do not scale yet. Fix records first, then scale.

Common mistakes that make smart freelancers misread the bet#

Even with clean records, you can still misread the decision. The common pattern is simple: one outcome, one confident take, or one clever setup starts doing more work in your mind than the evidence can support.

You grade the decision by the outcome#

If one launch, client, or pricing test worked, do not treat that single result as validation. Outcome-bias research and Annie Duke’s “one result is not enough” point to the same correction: separate process quality from short-run results. Corrective action: reopen your original assumptions before scaling, and check whether the result depended on unusual timing or a one-off client situation.

You trust confidence more than payoff shape#

Feeling sure is not the same as having a good bet. What matters is expected value and downside shape, not just conviction; expected value is a decision criterion, not a guarantee of one short-run outcome. Corrective action: replace a single forecast with a low, mid, and high range, then make the low-case trigger explicit before you commit.

You confuse a clever setup with a strong decision#

A smart-looking niche, channel, or offer is not enough on its own. Check base rates, expected value, and downside asymmetry before you scale, then run a premortem to surface how this could fail first. Corrective action: run one premortem and define one stop rule before launch.

| Misread signal | What to check before scaling | Next action |

|---|---|---|

| “It worked once, so it works.” | Original assumptions and whether the result was unusual | Re-test on a small sample |

| “I’m sure this will land.” | Outcome range and expected value, not one-point certainty | Write low, mid, and high cases with a low-case trigger |

| “This setup is clever, so it’s safe.” | Base rates and downside asymmetry | Run a premortem and set one stop rule |

Before your next move, pause and ask: Which assumptions am I treating as facts, what downside am I accepting, and what exact signal tells me to stop rather than rationalize?

Put your next career decision on paper today#

The useful move now is simple: write the decision before you act. The goal is lightweight clarity, not a full system. You want one short note you can use to judge process, not one lucky or unlucky outcome.

Fill the one-page template before you send the proposal#

Fill this one-page template before you send the proposal, change the offer, or chase the niche:

- Decision: What exactly are you choosing?

- Options: What are the real alternatives, including doing nothing?

- Assumptions: What must be true for this to work?

- Likely upside: What should improve if you are right?

- Downside exposure: What is the worst plausible outcome if you are wrong?

- Evidence that would change your mind: What would disconfirm your current view?

Quick check: if someone reads the note tomorrow, they should know what you believed before you acted. If your decision line says only “grow my business,” tighten it.

Separate preparation from commitment#

Classify your next moves so you do not confuse preparation with commitment. Motion can be useful, but it does not produce outcomes by itself.

| Awareness actions | Commitment actions |

|---|---|

| Reading about a niche | Sending a proposal to that niche |

| Rewriting your services page | Offering the new package to real prospects |

| Asking peers for opinions | Testing the price with actual buyers |

| Researching retainer models | Presenting a retainer option in a client call |

If your next moves are all in the left column, you are still preparing. Move one step to the right.

Revise confidence when new evidence shows up#

Revise your confidence when relevant new evidence shows up. Do not anchor to your first estimate, and do not treat one result as proof that your process was good or bad.

Example: if you expected a productized audit to sell, then a few calls where buyers ask for custom work should lower your confidence. If a couple of existing clients accept the audit without discounting and delivery stays clean, raise confidence a little.

Set one review checkpoint, then execute#

Set one review checkpoint, then execute. Useful checkpoints are event-based: after a small batch of proposals, after the first signed scope, or after the first invoice is paid. Keep your note with your proposal, scope, and invoice trail, then compare what you believed with what happened. If a simple structure helps, use a decision journal for your freelance business.

When you’re ready to commit, pressure-test your numbers and assumptions in the tools workspace.

Decision Tables You Can Use This Week#

Tie each career bet to a documented rule set and source-backed compliance trigger. Use IRS references for payment classification and recordkeeping, including About Form W-9, About Form W-8BEN, and the IRS recordkeeping guide for small businesses.

| Bet Type | Upside Metric | Downside Trigger | Kill Criterion |

|---|---|---|---|

| Raise retainers | Gross margin per client improves | Churn above tolerance after notice | Revert pricing if retention falls for two cycles |

| Add a new niche | Qualified lead volume improves | Longer sales cycle reduces cash conversion | Pause if pipeline to close ratio drops below target |

| Take cross-border clients | Higher average contract value | Tax/compliance workload spikes | Stop onboarding if compliance tasks exceed weekly cap |

| Productize a service | Delivery time per unit drops | Quality variance increases | Rollback if rework rate exceeds threshold |

Compliance and Tax Handling Matrix#

| Client Scenario | Form Workflow | Operational Check | Evidence to Retain |

|---|---|---|---|

| US payer, contractor relationship | W-9 collection and 1099 alignment | TIN validation before first payout | Signed tax forms and payout logs |

| Non-US beneficial owner | W-8BEN/W-8BEN-E path | Treaty and withholding review checkpoint | Form archive and decision memo |

| Foreign account exposure | FBAR/8938 screening | Threshold review at month-end close | Account statements and review notes |

| Platform-mediated payouts | Backup withholding watch | Mismatch and exception queue | Exception tickets and remediations |

Experiment Cadence Table#

| Week | Hypothesis | Small Test | Decision Rule |

|---|---|---|---|

| Week 1 | Offer-page rewrite increases qualified calls | A/B intro copy on one service page | Keep variant only if quality-call rate improves |

| Week 2 | Narrowing ICP improves close rate | Run outbound only to one vertical | Expand only if close rate improves over baseline |

| Week 3 | Stricter scope reduces overrun hours | Apply new scope template to 3 proposals | Adopt only if overrun hours decline |

| Week 4 | Payment terms reduce DSO | Test revised invoice schedule | Keep only if DSO trend improves |

Conclusion: Treat Every Freelance Career Move as a Priced Bet#

When you document assumptions, attach measurable upside and downside, and enforce kill criteria, career decisions become testable rather than emotional. Keep the memo short, update it with each cycle, and commit only when the evidence improves.

Budget your next decision memo with explicit thresholds: $2,000 onboarding cost cap, $5,000 downside exposure limit, $1,200 monthly compliance budget, 15 USD per transaction tolerance, and 3,000 USD quarterly tooling ceiling for 2026 planning.

Frequently Asked Questions

What does thinking in bets for freelancers mean in day to day decisions?

It means you set your decision rules before you act, then judge the process against those rules after results arrive. For each client, pricing change, or offer test, write down your commitment length, income goal, and one failure signal that tells you to stop. When results come in, grade your process against that note first.

How do you tell a good decision from a lucky outcome?

Start with what you wrote before acting: commitment length, income goal, and failure factors. Then compare that to what actually happened in your work and payment records, not just whether one invoice got paid. If a win looks hard to repeat, treat it as weak evidence and run another small test.

What should you estimate before you test a price change?

Estimate from your own recent records first, then define the failure factors that would make you stop the test. Because freelancing outcomes are exposed to market and network uncertainty, judge results with your written process and records, not a single short-term outcome.

How do you decide whether to keep, renegotiate, or exit a client?

Use signals you can verify in writing, not your current feeling about the relationship. | Decision path | Signals to look for | What to do next | |---|---|---| | Keep | Results stay inside your written goals and failure factors are not showing up | Continue and keep the same records so you can catch drift early | | Renegotiate | Warning signals start appearing, but a reset in scope or terms could still improve the outcome | Document the issues, restate scope and payment terms, and set a review point | | Exit | Failure factors continue after reset attempts | Close out documented work, send final reconciliation, and stop new work with that client |

When should you stop pushing a niche or service line?

Stop when the failure factors you wrote at the start keep showing up and new tests are not improving the odds. If you keep delaying the decision while staying "open to opportunities," you are hedging instead of learning.

What should your evidence pack include before you scale a decision?

Keep one file or folder with your original decision memo (commitment length, income goal, and failure factors), your work and payment records, and a short review note after each test. You do not need a long write-up, but you do need enough to reconstruct what you believed and what changed. If records conflict, pause scaling until the record is consistent.

How often should you update a decision memo, and when do you verify tax or compliance facts?

Update your memo when material evidence changes, not on a fixed schedule. Recheck it after a pricing pilot, a meaningful change in payment behavior, or when a one-off test starts looking repeatable. For U.S. tax guidance, verify current details through IRS Publication 17 and IRS Future developments updates before relying on a date or rule, because Publication 17 does not replace the law and can differ from court-favorable outcomes.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Thinking, Fast and Slow for Freelancers Who Want Better Clients

Treat thought leadership as risk control for your business, not just a visibility tactic. The real shift is from fast, reactive client chasing to slower, deliberate asset building. You publish to reduce risk before the next dry month, pricing call, or bad-fit project shows up.