Quick Answer

Yes. Confirmation bias in freelance can push you to keep low-margin clients, trust outdated payment assumptions, and stop compliance checks too early. Use the article’s sequence: calculate TNPPC, verify rule-sensitive decisions with primary guidance, and run a pre-decision disconfirming check. Then log each call in one page with assumption, evidence, disconfirming evidence, decision, and next review trigger. This keeps instinct useful without letting it make the final call.

Why Your 'Good Instincts' Are a High-Stakes Liability#

Your instincts are not the problem. The risk starts when a familiar answer feels true enough that you stop looking for contradictory evidence. With confirmation bias, you look for facts that support the client, price, payment tool, or compliance answer you already want and screen out the rest. That is an operating risk, not a personality flaw.

Familiar choices feel safe because they remove friction. You do not have to rethink a long-time client, reopen your pricing, or read the full payment terms. The exposure can show up later, when margin shrinks, cash gets delayed, or a client asks for documentation you cannot produce. The practical fix is to stop treating first impressions as decisions. Treat them as claims that need proof.

Step 1. Reclassify gut feel as a claim to verify#

A small shift helps. Treat your first judgment as a draft, not a conclusion. If you catch yourself saying, "I've always done it this way," or "this client has been good to me," ask one disconfirming question before you proceed: What fact, if true, would make me reverse this decision?

That pause matters because bias can hide the information you actually need. If you cannot name the fact that would change your mind, you are probably defending a preference rather than testing a business choice.

Step 2. Check the five battlegrounds where bias can hide#

Most bad calls do not start as obvious mistakes. They start in a few familiar places where convenience feels like evidence. Two areas deserve extra caution.

| Area | Instinct-led decision | Possible consequence | Early signal to notice | Evidence-led decision |

|---|---|---|---|---|

| Client selection | Keep a familiar client because the relationship feels reliable | You may carry low-margin work longer than you should | More chase emails, more revisions, slower payment follow-up | Review actual revenue, time spent, and payment speed before renewing |

| Pricing | Reuse an old rate or anchor to one peer comment | Your rate can lag your current scope and effort | You quote from memory without checking recent projects | Compare current scope, hours, and a fresh benchmark |

| Payments | Stick with the same platform because nothing has gone wrong yet | Cash flow risk can stay invisible until a hold, dispute, or payout issue hits | You cannot point to current terms or a backup payout method | Read current provider terms and confirm how larger invoices, disputes, and withdrawals are handled |

| Compliance research | Stop at the first article that says you are "probably fine" | You build procedures on incomplete or weak support | Your "research" is one bookmarked post and no primary source | Save the official guidance or source document behind the decision |

| Feedback | Write off client process requests as bureaucracy | You may repeat preventable admin errors across accounts | The same invoice or paperwork correction appears twice | Treat repeated client comments as operational evidence and update your checklist |

Start with payments. A dated 2010 anecdote about one freelancer marketplace described lower project quality, scam exposure, and fee friction, but that is not a current market benchmark. Use stories like that only as a prompt to verify today's provider terms for yourself, not as proof that a current platform is unsafe.

Then compliance research. The failure mode is not only getting the rule wrong. It is feeling finished too early because the answer was convenient. If a decision affects tax treatment, invoicing, data handling, or who is allowed to contract with you, your evidence pack should include the primary source you relied on. Do not stop at a summary article.

Step 3. Add one recurring checkpoint before the damage compounds#

The review only works if you will actually do it, so keep it short. Once a week, log four lines for each decision you made in the five areas above. Capture the choice, the evidence that supported it, the strongest contradictory fact, and what still needs verification.

Use this checkpoint to judge the review itself. If your weekly notes show only confirming evidence and no contradictory facts, you are not reviewing. You are repeating your own story. That is often the earliest visible sign that familiar choices are starting to create hidden exposure.

Next, measure where biased judgment is already distorting your revenue. Related: Canada's Digital Nomad Stream: How to Live and Work in Canada.

The Anti-Bias Audit Part 1: Diagnosing Your Revenue Blind Spots#

Treat this as an evidence check: judge each client on net contribution, not gross invoices.

Step 1. Calculate TNPPC for each active client#

Use one review window (for example, your last full quarter), then calculate:

TNPPC = Total Revenue - (Processor Fees + FX Spread Cost + Payout or Withdrawal Costs + Admin Labor Cost)

Checklist:

- Pull: invoice totals, processor statements, payout/transfer records, and admin records from your calendar, inbox, and invoicing logs.

- Calculate: each cost input separately for every client.

- Decide next: only trust outputs you can tie to records, not memory.

Input definitions:

Processor Fees: charges to accept payment.FX Spread Cost: loss when your received conversion rate is worse than the market reference you verified for that day.Payout or Withdrawal Costs: charges to move funds from platform to bank.Admin Labor Cost: non-billable time spent invoicing, fixing paperwork, chasing approvals, reconciling payments, and handling repeat process questions.

| Line item | Client A | Client B |

|---|---|---|

| Gross revenue | Similar top-line revenue | Similar top-line revenue |

| Processor fees | Higher | Lower |

| FX spread cost | Higher | Lower |

| Payout or withdrawal costs | Higher | Lower |

| Admin labor cost | Higher (more rework/chasing) | Lower (cleaner process) |

| TNPPC | Lower net outcome | Higher net outcome |

Step 2. Separate fee erosion before you optimize anything#

Do not use one blended "payment cost" number.

| Cost drag | Meaning | Review focus |

|---|---|---|

| Processor fees | Charges to accept payment | Review invoicing setup and provider choice |

| FX spread cost | Loss when your received conversion rate is worse than the market reference you verified for that day | Review billing currency and conversion timing |

| Payout or withdrawal costs | Charges to move funds from platform to bank | Review transfer/withdrawal patterns |

Checklist:

- Pull: recent payment records by client.

- Calculate: three distinct shares of revenue:

processor fees,FX costs, andpayout/withdrawal costs. - Decide next: optimize the largest drag first.

- Current benchmark range pending verification from the chosen source.

Use the split to choose the lever:

- If processor fees dominate, review invoicing setup and provider choice.

- If FX dominates, review billing currency and conversion timing.

- If payout/withdrawal costs dominate, review transfer/withdrawal patterns.

Step 3. Quantify the admin tax and make the next call#

Hidden admin load distorts client profitability unless you track it directly.

Checklist:

- Pull: calendar blocks for client admin, inbox threads for follow-ups/corrections, invoicing events (reissues, rejections, repeated document requests).

- Calculate: convert that time using your existing internal hourly planning/pricing rate, consistently across clients.

- Decide next:

- Renegotiate process when avoidable admin errors repeat. * Reprice when high admin load is structural to the account. * Disengage when the client resists both process fixes and repricing while net contribution keeps eroding.

Once revenue blind spots are quantified, apply the same evidence-first method to your compliance assumptions in Part 2.

For a step-by-step walkthrough, see How to Choose a Niche for Your Freelance Business.

The Anti-Bias Audit Part 2: Stress-Testing Your Compliance Assumptions#

Your compliance setup is only reliable when each assumption is tied to a primary authority and tested against change. Run this sequence in order: challenge the assumption, verify with the authoritative record, then simulate operational change.

Step 1. Challenge the assumption#

Start by trying to break your current view, not confirm it. Use a reusable "Digital Devil's Advocate" search set for each jurisdiction:

| Issue area | Official-guidance search |

|---|---|

| Tax residency | Use the selected jurisdiction's official tax residency guidance and remote worker exception pages; current tax residency threshold pending official verification. |

| Self-employed filing obligations | Use the selected jurisdiction's official self-employed filing guidance for foreign income; current filing threshold pending official verification. |

| Invoice requirements | Use the selected jurisdiction's official freelancer invoicing guidance for foreign clients; current invoice requirement details pending official verification. |

| Payment reporting or withholding | Use the selected jurisdiction's official cross-border payment reporting and withholding guidance for business accounts; current reporting or withholding threshold pending official verification. |

If you want copy-and-paste searches, add the relevant jurisdiction name to each query before using it:

"tax residency remote worker exceptions official guidance current tax residency threshold""self-employed filing obligations foreign income official guidance current filing threshold""freelancer invoice requirements foreign client official guidance current invoice rules""cross-border payment reporting withholding business account official guidance current reporting threshold"

Then add one friction term that could invalidate your assumption: nonresident, temporary stay, foreign payer, place of supply, local establishment, business bank, or change of address. Checkpoint: if your results are only blogs, forums, or summaries, you have not validated the assumption.

Step 2. Verify with primary authority#

Use secondary content to find issues, but validate decisions only with primary regulatory guidance. Treat regulator pages, statutes, agency guidance, or official filing instructions as your source of truth.

Keep a compact evidence log for every live assumption:

| Claim | Jurisdiction | Official source URL | Effective date shown | Open questions to escalate |

|---|---|---|---|---|

| What you currently believe | Country/state/city in scope | Primary authority page | Date shown on that page | Items for qualified legal/tax advisor |

If you cannot name the jurisdiction and attach the official source URL, you are still operating on belief. Keep this log structured so someone else can retrace each claim without guessing.

Step 3. Simulate operational change#

Before changes happen, test how they affect your compliance assumptions.

| Planned state | Changed state | Compliance checks triggered |

|---|---|---|

| Stable work location and travel pattern | More days in another country or longer stays | Recheck residency treatment, filing obligations, and invoicing requirements |

| Mostly familiar client-country mix | More clients in new countries | Recheck invoice rules, cross-border reporting obligations, and any threshold-based obligations. Current threshold or rule window pending official verification. |

| Same entity and banking setup | New entity, new bank, or new payment route | Recheck reporting duties, invoice issuer details, and whether the payment flow changes your compliance position |

If one change creates unresolved questions, pause and resolve them before scaling the same workflow. These evidence logs and scenario checks become inputs for Part 3, where you run a recurring red-team review cycle.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

The Anti-Bias Audit Part 3: Building Your 'Red Team' System#

Turn this into a repeatable cadence: before any high-impact decision, run three checks in order, then log the outcome. Use it for client selection, payment-rail changes, compliance-sensitive moves, and pricing decisions where a wrong call would hurt cash flow or execution.

Step 1. Pre-decision disconfirmation gate#

Start by looking for evidence that your preferred decision is wrong. In opaque, fast-changing systems, it is easy to form a confident hypothesis and hard to verify it unless you force a disconfirming pass.

| Risk type | Disconfirming check |

|---|---|

| Client | What evidence suggests this client could be slow to approve, hard to collect from, or costly to serve? |

| Payment rail | What evidence suggests payout holds, verification issues, disputes, or access interruptions? |

| Compliance | What official rule or filing instruction could fail if your facts change? |

| Pricing | What evidence suggests this price is mismatched to buyer response or deal viability? |

If you prefer a checklist format, use these same prompts:

- Client: What evidence suggests this client could be slow to approve, hard to collect from, or costly to serve?

- Payment rail: What evidence suggests payout holds, verification issues, disputes, or access interruptions?

- Compliance: What official rule or filing instruction could fail if your facts change?

- Pricing: What evidence suggests this price is mismatched to buyer response or deal viability?

Set your review window based on decision impact. Keep low-impact checks short; go deeper when the downside is material.

Before proceeding, confirm you have all three:

- At least one disconfirming signal

- At least one source you trust for this decision

- A clear trigger for re-checking the decision

Step 2. Peer challenge with explicit roles#

Do not ask peers for a generic review. Assign two clear roles in your personal board:

- Assumption challenger: argues the strongest case against your current conclusion

- Feasibility checker: tests whether this can be executed with current capacity, documentation, and timing

Treat this split as an operating structure, not a formal doctrine. The goal is to prevent "good idea, weak execution" decisions.

Before you move forward, log unresolved risks and assign an owner for each one. If a risk depends on outside input, name who closes it and what evidence closes it.

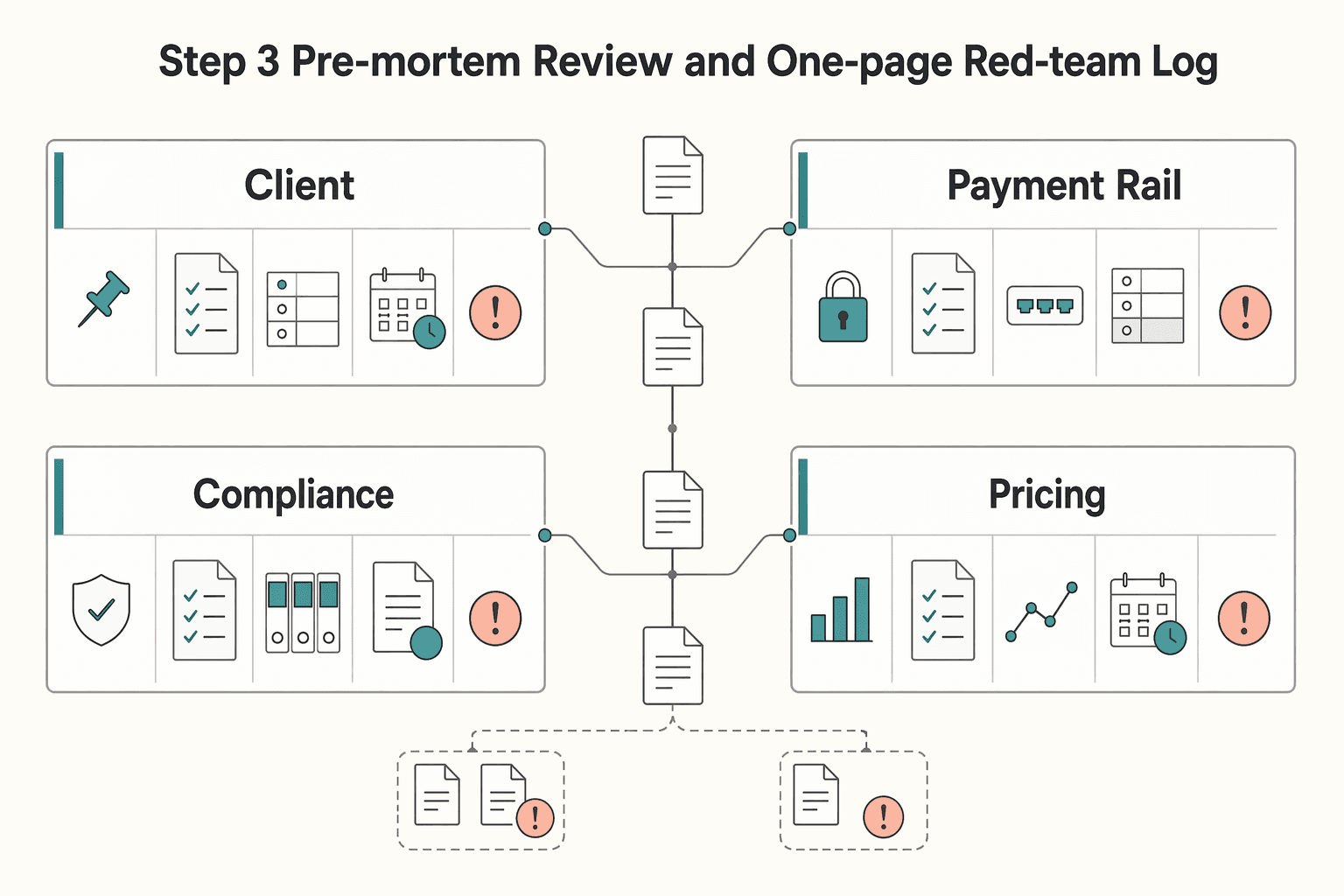

Step 3. Pre-mortem review and one-page red-team log#

Run a short pre-mortem: assume this decision fails, then define what you would see early if that failure is starting.

| Risk type | Bias-driven assumption | Early failure signal | Threshold to set now |

|---|---|---|---|

| Client | "This client will be straightforward." | Approval or scope behavior starts drifting from plan | Decision-specific threshold pending verification from client records |

| Payment rail | "This payment route is safe enough." | Payout, verification, or account access friction appears before steady-state use | Decision-specific threshold pending verification from platform and account records |

| Compliance | "My current setup still applies after this change." | Official guidance does not cleanly support the changed fact pattern | Current compliance threshold pending official verification |

| Pricing | "This price point will hold." | Win-rate or cycle-time movement starts pressuring pipeline quality or cash flow | Decision-specific threshold pending verification from pipeline records |

Capture the output in a one-page red-team log with five required fields: assumption, disconfirming evidence, decision, owner, next review trigger. Add unresolved risks if any remain open.

This is how bias control becomes operational: you stop treating challenge as a one-time exercise and start using it as a repeatable decision system. That sets up the final step, where disciplined decision-making becomes a durable competitive advantage.

You might also find this useful: this guide.

From Cognitive Bias to Competitive Advantage#

You turn confirmation bias from a recurring risk into a manageable process when you use the same decision workflow every time: revenue audit, compliance stress test, then red-team check before any choice that can affect clients, filings, or cash flow.

Step 1. Use one decision gate#

For each high-impact decision, open a one-page log with five fields: assumption, evidence, disconfirming evidence, decision, and next review trigger. If you cannot name one trusted source and one fact against your preferred choice, do not move to a go/no-go call. This matters even if you are experienced, because bias is not a beginner-only problem.

| Trigger | Instinct-led move | Evidence + disconfirming check | Go/no-go rule |

|---|---|---|---|

| New client | Say yes because they feel like a fit | Check margin, admin load, and payment pattern, then identify why this account could become high effort or slow pay | Go only when the record supports the story |

| Compliance change | Trust a thread, creator, or old assumption | Verify against regulator guidance or filing instructions, then look for exceptions and penalty exposure | No-go until rule and facts align |

| Payment setup | Pick what feels familiar | Test payout timing, holds, disputes, and fallback paths, then identify where cash could get stuck | Go only when failure points are acceptable |

Step 2. Match the check to the risk#

Use stronger evidence as downside increases. If a tax or filing claim came from social media, treat it as unverified until you confirm it against primary guidance. For payment decisions, evaluate reliability and cash predictability, not just convenience.

Step 3. Run one live decision this week#

This framework gives you practical gains: better client selection, cleaner compliance decisions, and more predictable cash flow. Pick one live decision this week and run the full workflow before you commit.

We covered this in detail in How to use a 'Decision Journal' for your freelance business.

Frequently Asked Questions

What are the biggest financial risks of confirmation bias for independent professionals?

The biggest risk is not one bad call. It is a chain of decisions made on too little information, where you keep an option because it feels familiar and never test the downside. If you cannot point to one disconfirming fact before you commit, treat the choice as higher risk than it looks. Next action: log the assumption behind your next important decision and write down one fact that would prove it wrong.

How does this bias affect compliance decisions?

It creates a gap between what you think is true and what official requirements actually say. Projection bias can make you assume a setup that works today will still work after your circumstances change, even when the facts have changed. For decisions tied to formal rules, verify against the original official guidance, then set a review trigger if one issue stays unresolved or your facts change.

What is a practical way to reduce confirmation bias in freelance decisions?

Use a simple three-check routine: name your assumption, find one disconfirming fact, then set a review trigger. Your checkpoint should be concrete. You should be able to state one source you trust, one fact against your preferred decision, and one condition that would make you revisit the call. Capture it in a one-page log with assumption, disconfirming evidence, decision, owner, and next review trigger.

Can confirmation bias lead me to choose the wrong tools or payment setup?

Yes. Familiarity often turns into selective questioning. A red flag is when you ask questions designed to reaffirm your first choice instead of testing where it breaks. An instinct-led choice asks, “Does this feel easy?” An evidence-led choice asks, “What could fail, and how would I know early?”

How do I know if I am choosing clients based on bias instead of evidence?

If your reasons are mostly about liking them, relating to them, or assuming they work the way you do, watch for affinity bias and the false-consensus effect. Those biases can make you overrate “good fit” and underrate objective signals. In practice, the failure mode is simple: you keep asking for signals that confirm the relationship is good instead of checking the record.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ccs.neu.edu/home/amislove/publications/Pymetrics-FAccT.pdftrusted

- cia.gov/resources/csi/static/Tradecraft-Primer-apr09...trusted

- cmsw.mit.edu/dev/wordpress/wp-content/uploads/2016/06/270...trusted

- elon.edu/u/imagining/surveys/vii-2016/algorithm-impac...trusted

- hhs.gov/sites/default/files/ocio/eplc/EPLC%20Archive...trusted

- irs.gov/newsroom/irs-assesses-162-million-in-penalti...trusted

- merage.uci.edu/research-faculty/research-colloquia/index.htmltrusted

- mykcai.kcai.edu/ICS/icsfs/mm/22-23coursecatalog.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Thinking, Fast and Slow for Freelancers Who Want Better Clients

Treat thought leadership as risk control for your business, not just a visibility tactic. The real shift is from fast, reactive client chasing to slower, deliberate asset building. You publish to reduce risk before the next dry month, pricing call, or bad-fit project shows up.