Quick Answer

Yes. You can license existing photos to a UK buyer from the US when you lock usage permissions in writing, send an invoice finance can process, and complete requested tax documentation before funds move. Set the contract terms clearly, keep billing details aligned with the payer’s legal entity, and preserve one file containing the signed agreement, payment evidence, and compliance records so withholding or filing questions can be resolved quickly.

The Bulletproof Framework for Licensing Your Photography to the UK: A 3-Phase Guide to Securing Your IP, Your Payments, and Your Peace of Mind#

Treat this as a three-phase process and you keep control of your rights, reduce payment friction, and avoid preventable tax mistakes. When a UK magazine wants to use an image you already created, the usual non-creative risks are unclear usage terms, delayed or reduced payments, and paperwork gaps.

This guide covers one specific scenario: remote licensing of existing photos to a UK buyer. In UK copyright guidance, the creator is generally the first owner of copyright, and licensing means giving another person or organisation permission to use that work. You are not starting from scratch. You are defining the permission, the payment terms, and the records that support the deal if questions come up later.

Phase 1. Secure the asset (legal)#

Get clear on what the client is buying, and what you are not transferring. Your legal checkpoint is scope: image, use, territory, duration, and license structure.

Phase 2. Secure the payment (financial)#

Set the payment path before delivery so the transaction stays predictable. This is where you reduce delays and disputes. It is also where you avoid assumptions about royalty withholding, because treatment can vary by facts and treaty position.

Phase 3. Secure your compliance (operational)#

Match your paperwork to the payment position and keep the file clean. This is where treaty documents and, when relevant, HMRC processes such as DT-Individual help support the record if tax or finance questions come up later.

Scope check before you start: this framework is for licensing existing images across borders. If the deal includes travel to the UK for on-location paid work, that is a separate route under UK visitor and permitted paid engagement rules. That needs separate handling later. Work this guide phase by phase, and only move forward when each checkpoint is complete.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Phase 1: Secure the Asset (Your Legal Framework)#

Start with legal clarity before delivery. In this pack, the supported points cover UK registration/compliance basics. Treat photo-licensing contract terms as unresolved unless they are separately supported.

Step 1. Turn the compliance basics into explicit written decisions#

Use a short decision table so your team is aligned on what is supported here.

| Item to settle | Write the exact agreed wording | Confirm owner/sign-off |

|---|---|---|

| Self Assessment registration | A sole trader registers by registering for Self Assessment; first-time filers must register before using online filing. | |

| Required IDs | A National Insurance number is needed to register for Self Assessment, and online filing requires a UTR. | |

| Registration trigger | Register as a sole trader if you earn more than £1,000 in a tax year (6 April to 5 April). | |

| HMRC timing | The referenced guidance states: tell HMRC by 5 October 2025 for the previous tax year (6 April 2024 to 5 April 2025); after that, a penalty is possible. | |

| Filing route limits | Online filing can start on or after 6 April; some cases are excluded (for example, living abroad as a non-resident), and HMRC directs users to commercial software or other forms in those cases. |

Step 2. Confirm liability and contracting-party details early#

GOV.UK states that business structure affects legal responsibilities: a sole trader is personally responsible for all business debts, while limited-company liability is limited to the company.

Verify the contract name and signatory against the real legal entity. Beyond this liability baseline, this grounding pack does not establish drafting rules for governing law/forum, indemnities, warranty boundaries, cancellation handling, or reuse rights.

Step 3. Assign unresolved photo-licensing issues before delivery#

For this scenario, treat the following as unresolved in this pack. Do not rely on them without separate evidence or legal review.

| Topic area | Responsible party (you / client / n/a) | Evidence on file |

|---|---|---|

| Scope/channels/territory/duration/exclusivity terms | Not established in this pack | |

| Ownership/assignment/sublicensing/reuse rights | Not established in this pack | |

| Governing law/forum and dispute handling | Not established in this pack | |

| Indemnity and warranty allocation | Not established in this pack | |

| Model/property/trademark/endorsement clearance split | Not established in this pack |

If any required line has no clear owner and no supporting evidence, pause delivery until it is resolved.

Phase 2: Secure the Payment (Your Financial Framework)#

Once the license terms are set, make payment execution just as explicit. Your goal is straightforward: no ambiguity on entity details, VAT handling, currency, or remittance instructions.

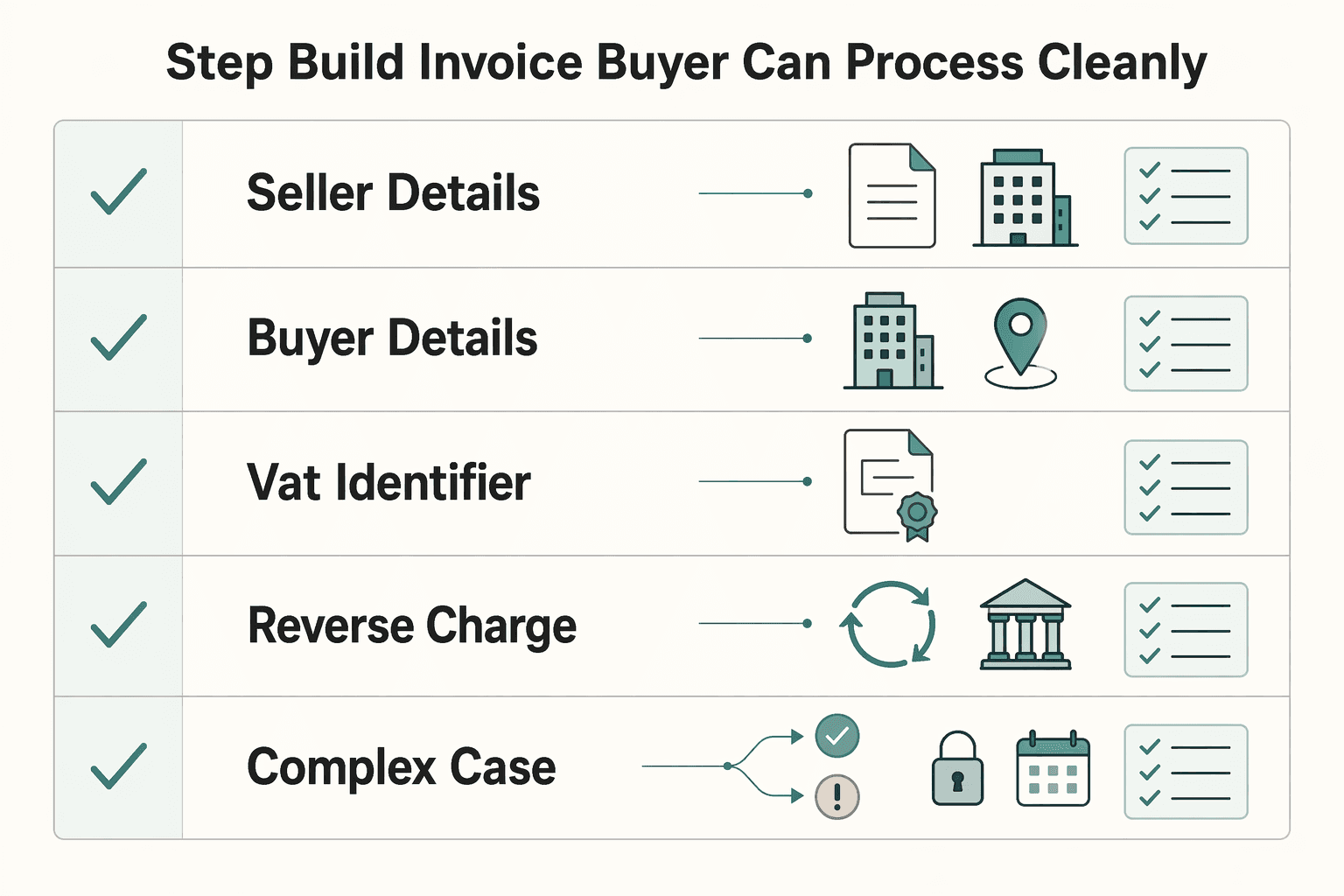

Step 1. Build an invoice the UK buyer can process cleanly#

A clean invoice is easier for AP teams to process. Delays are common when the contract entity, buyer records, and invoice fields do not match.

| Invoice item | Grounded detail | Article note |

|---|---|---|

| Seller details | A unique invoice number, plus your seller name, address, and contact details | At minimum, include these fields |

| Buyer details | The buyer's full legal entity name and address as their finance team records it | Delays are common when the contract entity, buyer records, and invoice fields do not match |

| VAT identifier | Any VAT identifier the buyer asks you to show, copied exactly as provided | Copied exactly as provided |

| Reverse-charge indication | Include a reverse-charge indication where applicable | HMRC requires a reverse-charge indication for services in scope, but not one fixed sentence |

| Reverse-charge wording example | "Reverse charge: customer to pay the VAT to HMRC." | A clear option |

| Entity-name check | Compare your PO, contract signature block, or AP onboarding email against the invoice | If the named entity differs anywhere, stop and fix it first |

Before you send it, compare your PO, contract signature block, or AP onboarding email against the invoice. If the named entity differs anywhere, stop and fix it first. At minimum, your invoice should include:

- A unique invoice number, plus your seller name, address, and contact details.

- The buyer's full legal entity name and address as their finance team records it.

- Any VAT identifier the buyer asks you to show, copied exactly as provided.

- A reverse-charge reference where applicable. HMRC requires a reverse-charge indication for services in scope, but not one fixed sentence. A clear option is: "Reverse charge: customer to pay the VAT to HMRC."

Under reverse charge, the UK customer accounts for the VAT. If place-of-supply rules mean no UK VAT is chargeable, do not add UK VAT anyway. Keep the treatment clear so the buyer's finance team can approve the invoice without extra back-and-forth.

A practical control is to ask the client to confirm billing entity details and whether they want a VAT number shown, in writing, and keep that record with the invoice.

Step 2. Invoice in USD when you want control of your net cash result#

Use USD invoicing as a cashflow choice, not as a legal absolute. HMRC allows invoice amounts in any currency, even if the buyer later has to convert values to GBP for VAT accounting.

The benefit is operational. You set and track your receivable in the currency you budget in. That can reduce margin drift from inconsistent conversion practices.

Do not assume USD removes FX risk. If the client wants to convert or pay in GBP, do not accept vague wording like "rate on the day." Get these points agreed in writing first:

- Conversion source

- Rate date

- Who pays conversion fees

If they cannot define those points, keep the invoice in USD and ask for USD remittance.

Step 3. Choose a payment rail you can predict and reconcile#

Choose the payment rail based on fee clarity, settlement predictability, dispute exposure, and bookkeeping effort, not just speed.

| Payment option | Fee transparency | Settlement predictability | Dispute risk | Reconciliation effort |

|---|---|---|---|---|

| Faster Payments | Provider and bank dependent; confirm charges up front | Available day and night, 365 days per year, with real-time behavior, but timing is not guaranteed instant in every case | Not a card-scheme chargeback rail | Low when payer includes invoice reference |

| Bacs Direct Credit | Provider and bank dependent | Follows a cycle of less than three days, so predictable but not instant | Not a card-scheme chargeback rail | Medium because batch timing can lag invoice timing |

| CHAPS | Usually disclosed by sending bank | Sterling same-day system, typically within 6am to 6pm, Monday to Friday | Bank of England describes CHAPS payments as irrevocable and settlement risk-free | Low for large one-off payments |

| Card payment | Processor pricing may be visible, but total dispute cost can be unclear | Payout timing depends on processor terms | Chargeback is not a legal right and recovery is not guaranteed | Medium to high due to dispute or admin overhead |

If the client is paying a UK account, share the payee name exactly as your receiving bank or provider shows it. Confirmation of Payee checks rely on sort code, account number, and payee name, so naming mismatches can slow things down.

Step 4. Run this check before you send#

Before you release the invoice, confirm these four points. Fix anything unclear before you send it:

- Invoice fields are complete and match the contracting entity.

- Payment rail and any FX responsibility are agreed.

- Receiving account details are validated, including exact payee name for UK bank payments.

- Remittance instructions are clear, including the payment reference to use.

Payment problems are usually much easier to prevent than to unwind after AP has already queued the invoice.

You might also find this useful: A Deep Dive into the 'Royalties' Article of the US-UK Tax Treaty for Authors.

Phase 3: Secure Your Compliance (Your Operational Framework)#

Handle compliance while the invoice is still easy to fix. Lock down three things early: what tax documents the client wants, how you will classify the income in your own books, and whether UK filing is actually in scope.

Step 1. Send tax documents during vendor setup#

Send requested tax documentation during vendor setup, not after AP has already queued the invoice. If the client asks for residency or tax-classification paperwork, send a complete copy with your onboarding documents.

That gives the client's finance team what they need to classify your vendor profile on their side.

Get written confirmation that your documents were received and ask whether any finance or compliance review is still open. Then confirm whether any open review changes your invoiced amount or commercial terms before payment moves forward.

Step 2. Keep your bookkeeping treatment consistent#

Keep your bookkeeping treatment consistent from the start. Whether you operate personally (for example, as a sole trader) or through a company, keep one clear classification path across the contract, invoice, and accounting records.

| Document | What the article says to keep |

|---|---|

| Signed license | Keep a complete deal file with the signed license |

| Invoice | Keep a complete deal file with the invoice |

| Payment confirmation | Keep a complete deal file with the payment confirmation |

| Bank statement | Keep a complete deal file with the bank statement |

| Relevant email trail | Keep a complete deal file with the relevant email trail |

| Requested tax paperwork | If the client requested tax paperwork, store that copy in the same file |

Keep a complete deal file with the signed license, invoice, payment confirmation, bank statement, and relevant email trail. If the client requested tax paperwork, store that copy in the same file.

Consistency matters. If your contract, invoice, and remittance notes describe the same work in different ways, clean that up early so year-end filing is simpler.

Step 3. Verify whether UK filing is actually in scope#

Treat possible UK filing as a separate verification step, not an automatic result of remote licensing. If UK filing does become relevant, timing and access rules matter.

| Checkpoint | Timing or rule | Article note |

|---|---|---|

| Notify HMRC | 5 October if you need to complete a return for the previous year in the stated circumstances | Late notification can lead to a penalty |

| Reactivate an existing account | If you had a Self Assessment account before, reactivate it first | Filing without reactivation may delay your return |

| Online filing start | Online filing can be done on or after 6 April after the tax year ends | You need your Unique Taxpayer Reference (UTR) to sign in |

| Payment deadline | 31 January | If filing is in scope |

| Online filing availability | Online filing is unavailable in some cases, including people who lived abroad as non-residents | Use commercial software or other forms |

HMRC says you must notify by 5 October if you need to complete a return for the previous year in the stated circumstances, and late notification can lead to a penalty. If you had a Self Assessment account before, reactivate it first; HMRC warns that filing without reactivation may delay your return.

If filing is in scope, online filing can be done on or after 6 April after the tax year ends, and you need your Unique Taxpayer Reference (UTR) to sign in. The payment deadline is 31 January.

HMRC also states that online filing is unavailable in some cases, including people who lived abroad as non-residents. In those cases, use commercial software or other forms.

Step 4. Separate remote licensing from physical UK work#

Decide early whether this is remote licensing only or work that puts you physically in the UK. That one fact changes the risk profile and tells you what to check next.

| Trigger | Main risk type | Required next action before accepting |

|---|---|---|

| You license existing images and perform all work from the US | Documentation and classification risk | Confirm requested tax documentation, align contract/invoice language, and store payment records in the deal file |

| You create or edit new work remotely from the US for a UK client | Scope and income-classification risk | Define in writing what is being delivered, where work is performed, and whether the buyer is purchasing a license, services, or both |

| The client asks you to be in the UK for a shoot, scouting, direction, or other on-site work | Immigration and possible local filing exposure | Verify your current UK work-permission and filing position from official guidance before accepting dates, travel, or deposits |

Use this as a hard checkpoint before you say yes. Then make sure you have the follow-through in place:

- Confirm in writing that the client received your requested tax documentation and whether any onboarding review is still open.

- Confirm current UK work-permission and filing requirements from official guidance before accepting any on-location UK assignment.

- Keep your compliance handoff file ready: requested tax form, signed contract, invoice, remittance proof, bank statement, and supporting records for year-end tax work.

For a step-by-step walkthrough, see How a US-based Marketing Agency can pay a UK-based video editor compliantly. Before you send client tax paperwork, create a clean first draft you can review against your contract terms with the W-8 form generator.

What If a Problem Arises? Your Strategic Plan#

When a compliance issue comes up, keep the response simple: identify the Self Assessment issue, pull your records, reply in writing, and set the next check-in date.

Step 1. Identify the problem type before you reply#

Label the issue in one line first: late-notification risk, missing UTR/sign-in details, account reactivation, recordkeeping gaps, or online filing eligibility. That keeps your response focused and stops the thread from turning into a mixed argument.

If the issue may affect UK filing, verify HMRC steps before you reply. Check whether you may need to notify HMRC by 5 October for the previous tax year, whether you have a Unique Taxpayer Reference (UTR), and whether you need to reactivate an existing Self Assessment account. HMRC also notes that filing can be delayed if an existing account is not reactivated, and late notification can lead to a penalty.

Step 2. Pull the governing text and your evidence file#

Work from HMRC Self Assessment guidance and your filing records. Use exact details from your account and records instead of relying on memory.

Keep one complete record set: bank statements or receipts, key filing details (including UTR and account status), and notes on online filing eligibility.

| Problem | What to check | Your first response | Escalation trigger |

|---|---|---|---|

| Late notification risk | Whether you need to complete a return for the previous tax year | Confirm whether HMRC must be told by 5 October and record your action date | HMRC is notified after the deadline and penalty risk applies |

| Filing access issue | UTR and sign-in readiness | Verify UTR and account access before filing | You cannot proceed with filing access |

| Existing account inactive | Whether reactivation is required | Reactivate the account before filing | A return is filed without reactivation and is delayed |

| Recordkeeping gap | Whether core records are complete (for example bank statements or receipts) | Rebuild missing records before filing | Missing records prevent an accurate return |

| Online filing eligibility issue | Whether you lived abroad as a non-resident | Confirm whether this online service is available before submission | You may not be able to use this online service |

Step 3. Send a factual written notice#

Keep the notice short and document-led, so the issue, the checkpoint, and the next requested action are clear. A reusable structure helps:

- Issue summary: "I need to complete Self Assessment for [tax year], and the blocker is [registration / UTR / reactivation / records / filing eligibility]."

- Checkpoint reference: "Key checkpoint: [5 October notification / account reactivation before filing / online filing eligibility]."

- Requested action: "Please confirm the next step by [date]."

- Documentation status: "Current records available: [bank statements / receipts / account details]."

Step 4. Set the next checkpoint and route support#

End every message with one clear follow-up date and put it on your calendar.

Use the key compliance checkpoints as anchors: 5 October for telling HMRC when required for the previous tax year, and 31 January for paying the Self Assessment bill. If your filing position is still unclear, get qualified tax support early and share your full record file.

Related reading: How a French Micro-Entrepreneur Can Invoice a US Client

Conclusion: You Are Now in Control#

Stay in control by running the same pre-delivery checks every time. Define the license clearly in the contract, make the payment path clean in the invoice, and sort the withholding paperwork before funds move.

Protect your IP by making the license specific. State the exact permitted use in the signed agreement, and make sure the contract says which law applies. Before delivery, confirm that the signed terms match the actual use being purchased.

Protect payment by removing ambiguity. Issue an invoice with the required details, including a unique identification number, and set a written due date. If no payment date is agreed, UK guidance says payment is due within 30 days of getting the invoice, goods, or service. If payment is late, statutory interest may apply at 8% plus the Bank of England base rate for qualifying B2B debts.

Protect compliance by treating withholding as a document process, not an assumption. UK domestic rules can require deduction on royalties unless treaty relief applies, and the UK-US treaty royalties rule is central to that analysis. If withholding appears, get the payer's written basis if you can, keep remittance evidence, and check whether Form US-Individual 2002 is needed for relief at source or repayment. Keep your records for at least 5 years after the 31 January submission deadline for the relevant tax year.

| Area | Reactive workflow | Controlled workflow |

|---|---|---|

| Dispute risk | Scope and governing law are inferred from email threads | Signed license states permitted use and governing law |

| Payment predictability | Due date and invoice setup are inconsistent | Invoice has required details and unique number, with a written due date |

| Tax handling clarity | Withholding is discovered after remittance | Treaty position, withholding basis, and document pack are prepared upfront |

For your next UK licensing deal, run this checklist before delivery and keep the related documents together:

- Confirm license scope and governing law in the signed agreement.

- Confirm invoice completeness, unique invoice number, and written due date.

- Confirm withholding position and whether Form US-Individual 2002 may be needed.

- Confirm recordkeeping: signed agreement, invoice, remittance advice, payment proof, publication evidence, and key emails.

This pairs well with our guide on How a UK Creative Director Should Invoice a US Client from their LTD Company to Optimize for Taxes.

Frequently Asked Questions

Do I charge VAT to a UK client as a US photographer?

This grounding pack does not confirm VAT treatment for this specific scenario. Do not lift VAT treatment from a template, including reverse-charge wording, without checking your specific deal. Ask the client’s finance team how they want the invoice handled and keep that instruction in writing. Before sending, check your invoice against that instruction and your signed agreement.

What clauses should I lock down in the agreement?

This grounding pack does not establish required clause wording for this scenario. As a practical safeguard, keep scope, payment terms, and dispute/jurisdiction terms clear in writing, then match your invoice to the signed terms.

Is my US copyright automatically protected in the UK?

This grounding pack does not verify the copyright outcome for this specific cross-border case. Keep an evidence pack with raw files, metadata, dated drafts, publication proof, and the signed license. If rights expand, update the scope in writing before reuse.

How do I get paid from the UK without avoidable fee surprises?

Choose a payment method based on invoice-currency control, transparent FX disclosure, and payout traceability. If you want to reduce exchange-rate risk, set and document your invoicing currency clearly in both contract and invoice. Reconcile remittance advice to your statement so you can track gross amount, FX conversion, fees, and net received.

Do I need to fill out a W-8BEN for a UK client?

This grounding pack does not establish whether Form W-8BEN is required here or how withholding applies. Complete only the current form you are eligible to sign, and ask the payer to confirm in writing whether they will withhold and why. Keep the form, payer correspondence, remittance advice, and any deduction records together.

What is the difference between remote photo licensing and an in-person UK shoot?

This grounding pack does not provide specific tax or immigration outcomes for remote licensing versus in-person UK work. If someone tells you UK filing is required, verify early: HMRC says you can notify by registering for Self Assessment, notification can be due by 5 October for the previous tax year, you may need a Unique Taxpayer Reference (UTR) for online filing, and you may need to reactivate an existing account before filing. HMRC also says some people who lived abroad as non-residents cannot use its standard online filing service and should use commercial software or other forms; where filing applies, send your return after 5 April and pay by 31 January. To pressure-test your payout path and total transfer cost, use the payment fee comparison tool.

Try a related tool

Tomás breaks down Portugal-specific workflows for global professionals—what to do first, what to avoid, and how to keep your move compliant without losing momentum.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Work for Hire vs Assignment of Rights for Freelancers

A freelance agreement is not just about price and scope. It decides who controls the rights in the work. If the ownership language is loose, rights can move earlier than you expect, cutting down your control once the work is delivered or used.

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

How to Find the Best Deals on Flights

If you are planning a move or a long stay, the right way to find cheap flights is to choose the fare that supports the trip you are actually taking, not just the one with the lowest headline price. A cheap fare can still be the smart choice, but only if it gets you there on a schedule you can use, leaves you functional when you land, and gives you booking records you can work with later.