Quick Answer

Start with a three-step system: pre-engagement audit, written contractor agreement, and invoice-to-deposit controls. For a canadian agency hire us freelancer setup, confirm service location first, since work performed in Canada can trigger Regulation 105 withholding of 15% of gross pay and may require an R105 waiver timeline. Then lock scope and payment terms in writing, and run every payment through a traceable evidence packet from acceptance to bank deposit.

Working with Canadian clients can grow your business, but cross-border work gets expensive fast when you treat it like a domestic project. The first problems are usually predictable: vague scope, slow payments, and tax or onboarding issues nobody pinned down before kickoff.

You do not need to become a tax lawyer to avoid that. You need a repeatable way to vet the client, structure the agreement, and close the payment loop cleanly. This playbook walks through that three-stage process so you can protect scope, cash flow, and compliance without slowing good deals down.

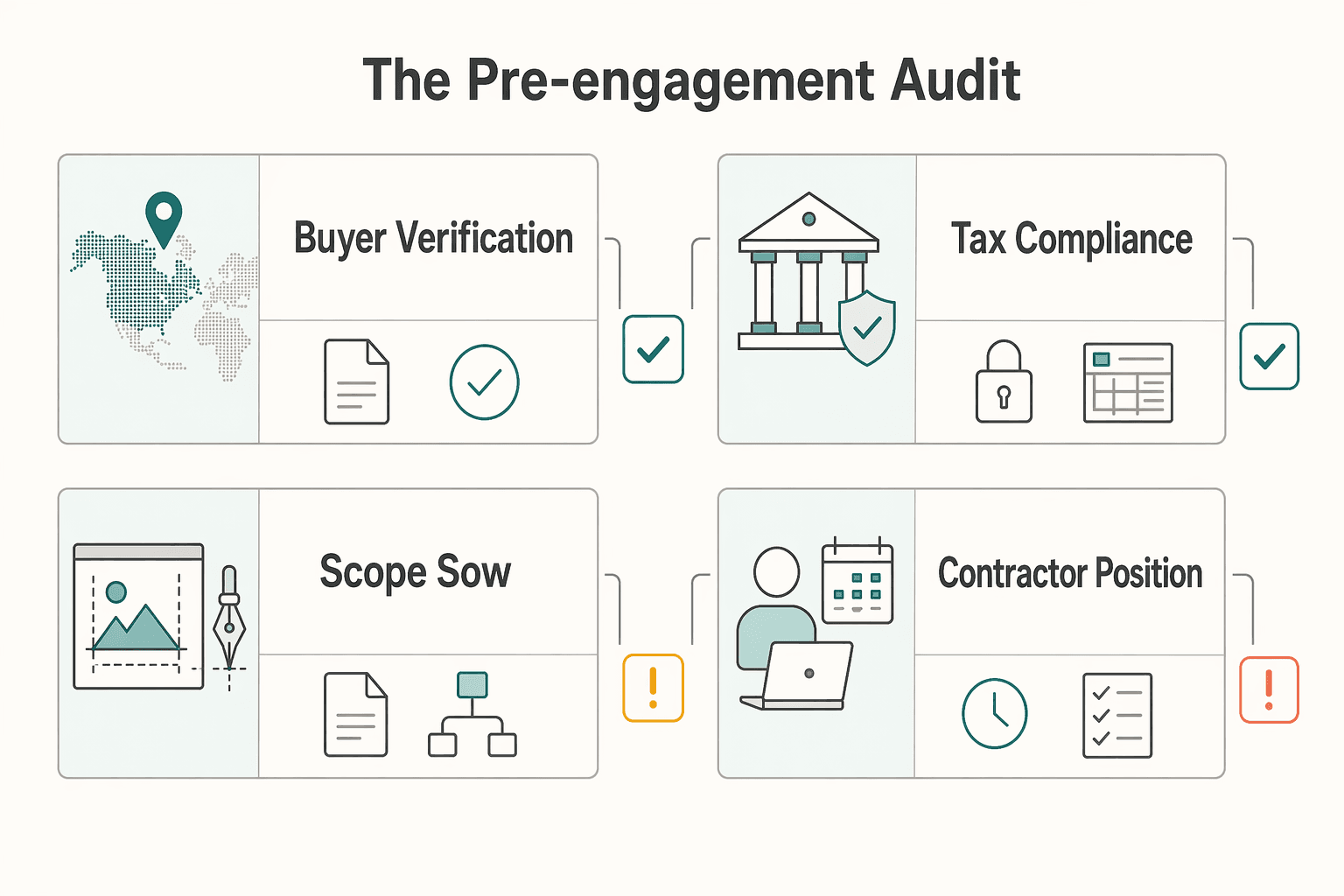

Stage 1: The Pre-Engagement Audit#

Before you say yes, check four things: who the client is, how finance will onboard you, what exactly you are delivering, and whether the working pattern still looks like contractor work. If any of those stay vague after one call, pause the deal.

| Audit area | What to confirm | Article note |

|---|---|---|

| Buyer verification | Agency legal name, business address, website, signatory, budget approver, invoice approver, and payment method | Check that the legal entity on the contract matches the invoicing instructions and the signatory's email domain; a missing signatory, AP contact, or payment method is a payment-risk signal |

| Tax and compliance path | Which onboarding form finance requires for a U.S. contractor and where the services will be performed | U.S. persons should not use Form W-8BEN; services rendered in Canada can trigger 15% Regulation 105 withholding, and waiver or reduction requests may be due no later than 30 days before service start or first payment |

| Scope and SOW | Deliverables, format, due date, acceptance criteria, revision boundaries, communication protocol, client dependencies, and out-of-scope items | Vague scope or missing acceptance standards can lead to scope expansion, approval drift, and invoice disputes |

| Contractor position | Contract language and working practices that show the client controls the result, not how you do the work | If status is unclear, Canada offers a CRA CPP/EI ruling and the U.S. has Form SS-8 |

-

Verify the buyer. Ask for the agency's full legal name, business address, primary website, and the name and title of the person who can sign the agreement. Then confirm who owns budget approval and who actually approves invoices. A simple checkpoint is whether the legal entity on the contract matches the invoicing instructions and the signatory's email domain. If you cannot get a clear signatory, accounts-payable contact, and payment method before work starts, treat that as a real payment-risk signal, not admin noise.

-

Confirm the tax and compliance path before kickoff. For a U.S. freelancer, do not assume Form W-8BEN is the right document. The IRS instructions say Form W-9 is used to request the TIN and certifications of a U.S. person, and the W-8BEN itself says U.S. persons should not use it. Ask the Canadian payer's finance team which onboarding form they require for a U.S. contractor, and record the verified form in your onboarding pack before kickoff.

The question that matters most is where the services are performed. If any part of the services will be provided in Canada, Canadian non-resident withholding rules can be triggered. Under Regulation 105, the payer may have to withhold 15% of the gross amount paid, and if they do not have written CRA authorization, that withholding is mandatory. That is when to escalate to a cross-border accountant, especially if you will travel to Canada, work on-site, or split delivery between the U.S. and Canada. If a waiver or reduction may be needed, the request window is no later than 30 days before service start or first payment.

- Lock scope in a usable SOW. A Statement of Work helps only if finance, production, and legal would all read it the same way. Name each deliverable, the format, the due date, and the acceptance criteria for each item. Acceptance criteria should be explicit.

Include six basics every time: deliverables, acceptance criteria, revision boundaries, communication protocol, client dependencies, and out-of-scope items. A common failure mode is "design support" or "ongoing strategy" with no acceptance standard and no dependency list. That is where scope expands, approvals drift, and invoice disputes start.

- Protect your contractor position in how you work. Classification is fact-specific, so labels alone will not save you. Use contract language and working practices that show the client controls the result, not how you do the work. If the relationship starts to look like staff augmentation with daily control over your process, raise it early. Where status is genuinely unclear, Canada offers a CRA CPP/EI ruling and the U.S. has Form SS-8 for worker-status determinations.

For a step-by-step walkthrough, see How a US-based Marketing Agency can pay a UK-based video editor compliantly. If you want a quick next step on "canadian agency hire us freelancer," Try the SOW generator.

Stage 2: The Bulletproof Agreement#

Once Stage 1 is clear, put the deal into a written independent contractor agreement before work starts. This is your main control point for cash flow, dispute risk, ownership clarity, and compliance posture.

| Agreement area | What to state | Article note |

|---|---|---|

| Compensation | Contract and invoice currency, accepted rails, invoice receipt, due-date rule, fees and FX, and a late-payment term verified before use | Before signature, the agreement, onboarding instructions, and invoice template should use the same payee name, currency, rail, and due-date language |

| Governing law and dispute resolution | Governing law, venue, notice method, and pre-claim steps | Use a forum and process you could realistically use if a dispute happens |

| IP, indemnity, and liability | When ownership transfers, what rights the client has before full payment, pre-existing materials you retain, indemnity boundaries, and liability-cap logic | A practical structure is ownership transfer after full payment, with a limited license for review and internal approval before that |

| Contractor status and permanent-establishment risk | Non-employment language that matches operations, control of work method, use of your own tools, outcome-based delivery, and no authority to bind the client | Avoid employee-style titles, staff performance systems, or authority to negotiate or sign for the agency |

- Compensation clause: protect cash flow with zero ambiguity.

Set payment terms so finance can execute them without guesswork.

| Decision point | What to state in the clause |

|---|---|

| Invoicing currency | Contract currency and invoice currency (for example, USD if that is your requirement). |

| Accepted rails | The payment method(s) you will accept. |

| Invoice receipt | When an invoice is treated as received. |

| Due date rule | Exact due-date wording tied to receipt. |

| Fees and FX | Who pays transfer fees and who carries conversion impact, if any. |

| Late payment | Current enforceable late-payment term pending legal/source-record verification. |

Before signature, confirm that the agreement, onboarding instructions, and invoice template use the same payee name, currency, rail, and due-date language.

- Governing law and dispute resolution: optimize for enforceability and practicality, not ego.

There is no universal "best" forum. Push for a forum and process you could realistically use if a dispute happens; compromise can still be reasonable if the commercial terms justify it. If you compromise, make the clause explicit on governing law, venue, notice method, and pre-claim steps. Keep process terms concrete so you do not create a second dispute about procedure.

- IP, indemnity, and liability: separate the moving parts.

Do not collapse ownership, license, indemnity, and liability cap into one paragraph. State when ownership transfers, what rights the client has before full payment, and what pre-existing materials you retain. A practical structure is: ownership of final deliverables transfers after full payment; before that, the client gets a limited license for review and internal approval only. Put indemnity boundaries and liability-cap logic in separate clauses so both sides can calculate risk from the contract or SOW. For enforceability-sensitive language, add local counsel review before signing.

- Contractor status and permanent-establishment risk: align contract text with real behavior.

Use non-employment language that matches operations: you control work method, use your own tools, and deliver outcomes rather than acting as staff. Also state that you cannot bind the client or act as its agent. Then run the engagement the same way in practice. Avoid employee-style titles, staff performance systems, or authority to negotiate or sign for the agency. If day-to-day control starts drifting toward employment-style supervision, document a reset in writing immediately. If you need a deeper triage path, see What to Do If You've Been Misclassified as an Independent Contractor.

Stage 3: The Seamless Operations Playbook#

After signature, your goal is simple: no gap between "work accepted" and "funds cleared." Run the same sequence every time: acceptance, invoice, payment rail confirmation, remittance match, funds posted, records archived.

Before invoice one, confirm these four items match across your docs: signed agreement, current SOW/change order, your payee and banking details, and the client's AP contact. If entity name, currency, due-date wording, or fee allocation conflicts anywhere, fix it first.

Issue an invoice AP can approve on the first pass#

Use this checklist for every invoice:

| Invoice item | Requirement |

|---|---|

| Your legal/business name | Include it on the invoice |

| Client legal name and billing contact | Include it on the invoice |

| Unique invoice number | Use a unique invoice number |

| Issue date | Show the issue date |

| Service date or billing period | Show the service date or billing period |

| Clear service description | Keep descriptions specific |

| Agreed currency | Show the agreed currency |

| Due date | Show the due date |

| Payment instructions | Include payment instructions |

| Line items | Map them to SOW milestones or approved changes |

If a line item cannot be traced to the SOW, expect delay. Keep descriptions specific so approval and later dispute review are straightforward.

Handle tax wording carefully. GST/HST treatment is fact-specific, and if GST/HST applies, the invoice must show the applicable rate. Verify GST/HST treatment for the specific supply from official or advisor records before using invoice tax wording. If services are rendered in Canada, escalate before billing: Regulation 105 applies to payments to non-residents for services rendered in Canada, section 105(1) states a 15% withholding amount, and CRA provides a waiver route via Form R105.

Do not let AP guess your U.S. tax form. Form W-9 is used to request the TIN of a U.S. person; if AP requests a different U.S. withholding form, verify before payment is held in tax review.

Choose the payment rail that minimizes surprises#

Pick the rail based on settlement predictability and reconciliation quality, not headline speed.

| Payment method | Settlement predictability | Fee transparency | FX control | Dispute handling | Reconciliation effort |

|---|---|---|---|---|---|

| Traditional bank wire | Strong once released; Lynx wires are fast, irrevocable, and have real-time settlement finality | Current fee range and settlement timing pending official/provider verification. | Strong if contract fixes currency and fee allocation | Hard to reverse once sent | Moderate if payment reference is complete |

| ACH-linked account transfer | Good on business days; ACH runs 23 1/4 hours each business day with four settlements, not continuous weekend/holiday settlement | Current fee range and settlement timing pending official/provider verification. | Usually good if provider supports invoice currency | Provider-specific timing and exception handling | Low to moderate if invoice reference passes through |

| Remittance transfer service | Varies by provider and funding method | Current fee range and settlement timing pending official/provider verification. | Check quoted rate and spread | If remittance-transfer rules apply, disclosures and a 30-minute cancellation window may apply | Low at small volume; higher if references are inconsistent |

Use this script with each invoice:

Please remit this invoice in the agreed currency using your preferred bank or payment provider. Include the invoice number and SOW reference in the payment reference, and email remittance advice on the send date. Payment is due under the period stated in our agreement, and transfer fees/FX treatment follow the contract.

Build an audit-ready record set when funds land#

As soon as payment clears, file one linked packet: signed agreement, SOW/change orders, approval messages, invoice, PO (if any), remittance advice, provider confirmation, bank proof of deposit, and related tax correspondence (GST/HST, withholding, R105). Use one identifier across all records, for example: client code + contract ID + invoice number.

Your five-minute test: for any payment, you should be able to show scope, billing basis, amount sent, amount received, and the reason for any difference. Keep a tracker with invoice sent date, due date, amount, currency, rail, sender reference, cleared date, and any fee/FX shortfall.

Keep daily income/expense records and supporting transaction documents. CRA's baseline retention is 6 years from the end of the relevant tax year; U.S. citizens and resident aliens are taxed on worldwide income, and the IRS general assessment limitation reference is 3 years. For cross-border files, ask your advisor which retention rule should control. Escalate early if services are performed in Canada, withholding appears, or invoice tax treatment is still unverified. For a related walkthrough, see How to Pay US Subcontractors from Canada.

Cross-Border Quick Reference#

What tax form should you give a Canadian client?#

Verify the payer, the payee, and whether payment is to you personally or to a business entity before you share tax documents. There is no single universal form for every setup, so the current required form must be verified with the payer's finance or tax team before AP defaults to a document. What to do next: get payer/payee status confirmed in writing before onboarding documents are finalized.

Should you charge GST/HST on your invoice?#

Treat GST/HST as a verification step, not a default. Confirm treatment for the specific supply before invoicing, and if tax applies, show the applicable rate on the invoice. What to do next: if service location or registration status changed from the original setup, pause and recheck before you send the bill.

Is a Canada U.S. freelancer contract legally binding?#

It can be, but enforceability depends on how clearly the agreement is formed and documented across jurisdictions. If your contract terms, scope records, or approval trail are unclear, enforcement risk goes up fast. What to do next: align your independent contractor agreement and SOW on scope, payment terms, and jurisdiction before work starts.

What payment method should you choose?#

Choose the method that gives you predictable settlement and clean reconciliation, not just the fastest-looking transfer path. Compare each option on fee transparency, FX handling, settlement reliability, and reconciliation burden; no single method is always cheapest or fastest. What to do next: confirm in writing how remittance data will appear and who absorbs transfer fees and FX costs before invoice one.

Do you need to report income from a Canadian client?#

Treat cross-border freelance income as tax-relevant and keep a full payment trail from contract to deposit. Do not rely on platform history alone, especially where withholding-related issues can create delays or later corrections. What to do next: archive each cleared payment file immediately and confirm current filing requirements for your setup.

We covered related payment workflow details in The Best Way for a German Agency to Pay a US-Based Freelancer.

Conclusion: You Are the CEO of Your Global Business#

The goal is not to memorize every cross-border rule. The goal is to make a few checks non-negotiable in how you sell, sign, and close each engagement.

Build the process into how you work#

Turn the big ideas into repeatable behavior. Once you build the audit, contract, and operations steps into your process, each new deal becomes easier to control.

| If you wing it | What you do now |

|---|---|

| Let AP choose the tax form | Verify payer, payee, and withholding context before sending a Form W-9 or Form W-8BEN |

| Assume contractor language settles everything | Treat the agreement as one factor, then match scope, control, approvals, and payment behavior to the actual relationship |

| Discover withholding issues after invoicing | Confirm whether services will be provided in Canada and whether Regulation 105 could apply |

| Keep only invoices | Keep the contract, SOW, invoice, remittance advice, bank proof, and any CRA or IRS correspondence together |

Verify service location before you sign#

Verify the facts that matter before you sign. The biggest one is service location. If any services will be provided in Canada, Regulation 105 can require 15% withholding on the gross amount, and if the payer has no CRA written notification, that withholding is mandatory. If a waiver may be needed, raise the R105 waiver application early, normally 30 days before services begin in Canada or 30 days before the first payment is due.

Close each job with a complete evidence pack#

Document the job at closeout so the file can survive a tax or payment dispute. Your minimum closeout checklist is:

- final signed agreement and SOW

- approved invoice and payment reference

- bank deposit proof

- notes on GST/HST treatment if reviewed

- any T4A-NR, waiver, or ruling-related correspondence

Escalate when classification is fuzzy, GST/HST treatment is unclear, or work will happen in Canada. CRA says you can request a ruling for GST/HST certainty, and IRS guidance is clear that no single classification factor decides status. Use this standard on every cross-border freelance engagement to help reduce payment friction, scope risk, and compliance surprises without slowing good deals.

Frequently Asked Questions

What tax form should you give a Canadian client?

Verify the payer, the payee, and whether payment is to you personally or to a business entity before you share tax documents. There is no single universal form for every setup, so the current required form must be verified with the payer's finance or tax team before AP defaults to a document. What to do next: get payer/payee status confirmed in writing before onboarding documents are finalized.

Should you charge GST/HST on your invoice?

Treat GST/HST as a verification step, not a default. Confirm treatment for the specific supply before invoicing, and if tax applies, show the applicable rate on the invoice. What to do next: if service location or registration status changed from the original setup, pause and recheck before you send the bill.

Is a Canada U.S. freelancer contract legally binding?

It can be, but enforceability depends on how clearly the agreement is formed and documented across jurisdictions. If your contract terms, scope records, or approval trail are unclear, enforcement risk goes up fast. What to do next: align your independent contractor agreement and SOW on scope, payment terms, and jurisdiction before work starts.

What payment method should you choose?

Choose the method that gives you predictable settlement and clean reconciliation, not just the fastest-looking transfer path. Compare each option on fee transparency, FX handling, settlement reliability, and reconciliation burden; no single method is always cheapest or fastest. What to do next: confirm in writing how remittance data will appear and who absorbs transfer fees and FX costs before invoice one.

Do you need to report income from a Canadian client?

Treat cross-border freelance income as tax-relevant and keep a full payment trail from contract to deposit. Do not rely on platform history alone, especially where withholding-related issues can create delays or later corrections. What to do next: archive each cleared payment file immediately and confirm current filing requirements for your setup. We covered related payment workflow details in The Best Way for a German Agency to Pay a US-Based Freelancer.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- consumerfinance.gov/rules-policy/regulations/1005/34trusted

- ecfr.gov/current/title-12/chapter-X/part-1005/subpart...trusted

- hbs.edu/ris/Publication%20Files/17-096_813abb74-09c5...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- canada.ca/en/revenue-agency/services/tax/international...external

- frbservices.org/resources/resource-centers/same-day-ach/feda...external

- nacha.org/content/abcs-achexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay US Subcontractors from Canada

Engaging U.S. talent can be a strong growth move for a Canadian business. The challenge is making the cross-border mechanics feel routine on your side and invisible on theirs. If payments, compliance, and reporting are sloppy, you create financial risk, waste time, and look less credible to the people you want to keep. When they are handled well, your back office starts to work in your favor.