Quick Answer

Yes, hong kong territorial tax can still be viable for mobile consultants when each income stream is classified correctly and backed by contemporaneous records. The article’s core rule is source over residency: assign the right tax head, test where profit-producing activity happened, and reconcile contracts, invoices, and payment evidence. Because foreign-sourced income exemption rules changed from 1 January 2024, older commentary can mislead. Escalate mixed-source, treaty, or conflicting-record cases before filing.

When Hong Kong territorial tax can still work for mobile consultants#

Hong Kong can still be a viable base for mobile consultants, but only when your filing position matches your facts. In Hong Kong SAR, profits tax turns on where profits arise or are derived, not on a blanket worldwide-income model.

Most expensive mistakes start with misclassification. Hong Kong does not use one general personal income bucket. Income is handled under separate heads such as profits, salaries, and property. A personal assessment election may help in some cases, but it does not replace source analysis.

Use this baseline rule: do not treat residency as the shortcut. Under the territorial principle, the deciding question is where profits arose or were derived. If your facts span more than one jurisdiction, use a conservative position and keep stronger records.

Foreign-sourced income exemption rules include changes effective from 1 January 2024. Older commentary can miss that change. Treat this article as a decision guide, not a loophole hunt.

Use this quick pre-check before you optimize anything:

- For each income stream, can you explain where profits arose or were derived?

- Do your contracts, invoices, and payment records tell one consistent story?

- If the Inland Revenue Department asks follow-up questions, can you support your position with records created at the time?

If you may be chargeable but have not received a return, notification may be required within four months after the end of the year of assessment. The next sections show how to test viability, document defensible positions, and decide when professional advice is the right next step.

Keep one working file open while you read. By the end, you should have a stream-by-stream label and a source position for each stream. You should also have a short list of unresolved assumptions that need review before filing, so this becomes action instead of passive reading.

If you only finish one task today, complete the pre-check and mark every uncertain assumption in plain language. That list becomes your escalation agenda and helps prevent last-minute guesswork.

What Hong Kong territorial tax means in plain terms#

At its core, Hong Kong territorial tax is a source question: where profits arose or were derived.

Hong Kong adopts the Territorial Source Principle of Taxation. Hong Kong Profits Tax generally applies to profits arising in or derived from Hong Kong, while profits sourced elsewhere are generally outside profits tax.

The practical issue is application. The principle is straightforward, but case-level outcomes can still be contentious. A broad label like offshore is not enough on its own.

Tax heads still matter at this stage. Hong Kong separates profits, salaries, and property. Classify the income stream first, then test source under the right head.

A useful way to read the rule is this: source analysis is an evidence test. If your records and narrative point in different directions, the legal label can be hard to defend. If they point in the same direction, your position is easier to explain during review.

Use this checkpoint before relying on a source position:

- List each income stream separately.

- For each stream, identify where the profit-producing activities happened.

- Confirm the correct tax head before testing source.

- Flag any stream where records and narrative do not align.

If your first explanation relies on a broad offshore statement, stop and rebuild the analysis from facts. That shortcut can lead to avoidable errors.

Create a short source note for each stream using the same order each time. Repetition is useful here because it makes inconsistencies visible across months, clients, and engagements. If you cannot explain a stream clearly with matching records, treat that position as uncertain until the facts are verified. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Know which tax bucket you are actually in#

Classification comes before optimization. Assign each income stream to the correct tax head before testing source.

Hong Kong does not use one unified personal income bucket. It applies separate heads, including profits tax, salaries tax, and property tax. The source principle is clear in concept, but its application can be contentious in specific cases.

Avoid blending unlike income into one story. Keep consulting revenue, employment pay, and rental income separate, then test each stream under its proper head.

Joint assessment may be available when beneficial, but it is not a shortcut around classification or source analysis. Use it only after each stream is correctly labeled.

Use this pre-filing check:

- List each income stream separately.

- Tag each item as profits, salaries, or property with a short reason.

- Keep one supporting record for each item.

- Flag any item that could fit more than one head for professional review.

Use a simple label table early so you can spot conflicts before filing pressure starts:

| Income stream | Provisional head | Evidence that supports the label | Common misread |

|---|---|---|---|

| Independent consulting project | Profits tax (provisional) | Contract scope, acceptance record, invoice trail | Assumed to be employment because one client dominates revenue |

| Employment-style engagement | Salaries tax (provisional) | Day-level work records plus engagement terms | Treated as consulting based only on contract title |

| Rental income | Property tax (provisional) | Lease terms and payment records | Folded into consulting totals for convenience |

This table is a working draft, not your final filing position. Update it whenever facts change, then reconcile changes across contracts, invoices, and tax labels so old assumptions do not survive by accident. If you cannot label every stream clearly, pause planning and fix classification first.

Start with a viability check before you optimize#

Before comparing elections or trying to reduce tax, test whether your position is viable on the facts you can prove today.

Use a simple decision rule. If your key facts are incomplete or split across places, treat the position as higher risk and strengthen your records before taking a firm position.

Do not rely on a single label or status as a shortcut. If your outcome depends on assumptions you cannot document, treat it as uncertain and plan for professional review.

Write a one-page viability note before moving forward:

- Income stream and intended tax treatment.

- Where relevant work was performed in practice.

- Where key decisions and acceptance happened.

- What records already support your position.

- Which assumptions are still uncertain.

Be strict about what counts as support. A memory of where work happened is not enough when records say something else. If your note relies on assumptions you cannot tie to documents, mark those lines for escalation now, not during the final filing window.

Set a status beside each assumption: supported, partially supported, or unsupported. Then decide whether you can close the gap with records already in hand or whether that line needs professional review.

A good viability note also shows tradeoffs. If one interpretation gives a better tax outcome but depends on weak records, treat it as fragile. If another interpretation is less favorable but better supported, that may be the safer filing position.

If you cannot explain the fact pattern clearly in one page, your setup is not filing-ready yet.

Classify your working model before applying source rules#

Treat this step as your quality gate: map each income stream first, then apply source analysis. If you skip it, assumptions get mixed early and are harder to unwind later.

Hong Kong adopts a territorial source principle of taxation, so source remains the core question for profits. The headline principle is clear, but real cases can still be contentious. That is why early classification matters. It lets you fix weak labels and missing records before filing pressure sets in.

Split distinct income streams even if the payer is the same, and keep uncertain labels provisional until your records are complete.

Use a one-page working model per stream:

- Income stream name and payer.

- Provisional treatment note (to be confirmed).

- Engagement label: project-based, long retainer, or other working pattern.

- Control notes: who directs day-to-day work and who accepts output.

- Evidence on hand: contract, amendments, scope records, and payment records.

- Risk flag: clear, mixed, or uncertain.

Use scenario contrast as a screening tool. Different working patterns can lead to different source conclusions, so document why each label currently makes sense.

The value of this model is consistency over time. When new invoices, amendments, or delivery records appear, update the same stream sheet instead of creating a separate narrative. That keeps your filing story stable and makes contradictions easier to catch.

A practical checkpoint is monthly review. Re-read each stream label against recent activity and ask one question: if an external reviewer saw only these records, would the label still make sense? If not, update the label, gather missing records, or consult a professional adviser.

If you cannot label each stream and support it with contemporaneous records, pause optimization and escalate uncertain lines before you rely on a filing position.

Use a practical source test for business profits#

Hong Kong adopts a territorial source principle of taxation: only profits with a Hong Kong source are taxable here, while profits sourced elsewhere are not subject to Hong Kong Profits Tax. The principle is clear, but its application in particular cases can still be contentious.

| Source factor | Question to answer |

|---|---|

| Contract signing | Where terms were negotiated and executed |

| Service delivery | Where substantive work was performed |

| Decision control | Where key commercial or technical decisions were made |

| Invoicing | Where billing activity was prepared and approved |

| Acceptance location | Where deliverables were reviewed and accepted |

Apply source testing with one consistent method across income streams. Consistency helps when facts are mixed.

Use one sequence of questions for every income stream:

- Contract signing: where terms were negotiated and executed.

- Service delivery: where substantive work was performed.

- Decision control: where key commercial or technical decisions were made.

- Invoicing: where billing activity was prepared and approved.

- Acceptance location: where deliverables were reviewed and accepted.

This is a practical method for repeatable analysis, not a statutory checklist. If facts are split across places, treat the stream as mixed and strengthen your records before taking a source position.

Do not use bank account location as proof of source. Receiving funds in or outside Hong Kong does not, by itself, establish where profits were sourced.

Keep a claim log for each stream, tied to evidence you can produce quickly:

- Signed contract.

- Statement of work or change order.

- Travel or work-location records where relevant.

- Delivery evidence, such as client sign-off or written acceptance.

To make the claim log useful, track both supporting and conflicting records. If one invoice description suggests a different delivery pattern than your source position, mark the conflict and resolve it. Ignoring contradictions can increase filing risk.

Use plain labels for each stream state:

- Clear: records align with one source narrative.

- Mixed: facts point to more than one location and need deeper analysis.

- Uncertain: records are incomplete or contradictory.

This label is not a legal conclusion. It is a control step that tells you whether to proceed, strengthen documentation, or escalate.

Label each stream clear, mixed, or uncertain. If your evidence and narrative conflict, use conservative treatment and get advice before filing with the HKIRD.

Handle employment edge cases without guessing#

Employment-style income needs a cautious call. Keep your position provisional until your core facts are clear.

| Control | Article guidance |

|---|---|

| Log where services were actually performed | As consistently as possible |

| Tie your records | To calendar entries and related engagement documents |

| Mark unclear periods | Immediately instead of rebuilding them later |

| Reconcile logs | Against invoices and delivery records on a regular schedule |

| Flag periods | Where your narrative changed after documents were created |

Hong Kong adopts a territorial source principle of taxation: only profits with a Hong Kong source are taxable in Hong Kong, and profits sourced elsewhere are not subject to Hong Kong Profits Tax. The principle is clear, but applying it in specific cases can be contentious.

Do not assume one contract label settles treatment. If a stream can reasonably be read more than one way, avoid relying on a single clause or a reconstructed pattern.

This section does not set employment-test rules or threshold mechanics. It gives practical controls so you do not guess:

- Log where services were actually performed as consistently as possible.

- Tie your records to calendar entries and related engagement documents.

- Mark unclear periods immediately instead of rebuilding them later.

- Reconcile logs against invoices and delivery records on a regular schedule.

- Flag periods where your narrative changed after documents were created.

Use a common internal documentation standard across months. If records are uneven, treat conclusions as provisional until gaps are resolved.

Red flag: contract wording points one way, but day-to-day records point another.

Another red flag is late reconstruction. Rebuilding locations or timelines near filing time can introduce avoidable conflicts.

If facts are incomplete, records conflict, or your position depends on assumptions you cannot evidence, take a conservative treatment and consult professional advisers before filing.

Build a documentation pack that can survive review#

Your position is only as strong as the records behind it. Make each income stream traceable from agreement to payment and delivery.

Hong Kong operates on a territorial basis of taxation, taxing locally sourced profits and earnings rather than worldwide income. The Inland Revenue Department (IRD) oversees tax regulations with filing and reporting requirements, so your file should show what happened, when it happened, and which stream each record supports.

Use a consistent pack for each stream. Depending on your work, that can include:

- Signed contracts and dated amendments.

- Scope or delivery records.

- Invoice and payment records that can be matched.

- Service-delivery evidence.

- A timeline linking agreement, delivery, invoicing, and payment.

If mobility or time apportionment is relevant to your position, keep contemporaneous records that explain your approach and how you applied it.

If treaty or CDTA analysis is part of your file, document assumptions and open questions clearly, and cross-reference the underlying records.

File discipline matters. Use stable names, consistent dates, and one source of truth for each document so old versions do not reappear during review. If a record is corrected, keep the updated file and note what changed. That avoids silent contradictions between draft and final packs.

Keep a simple index at the top of each stream file showing where each key document lives. During review, this can cut search time and lower the chance of relying on outdated versions.

Review your files regularly while facts are fresh, and resolve conflicts early so you are not rebuilding the story during filing season.

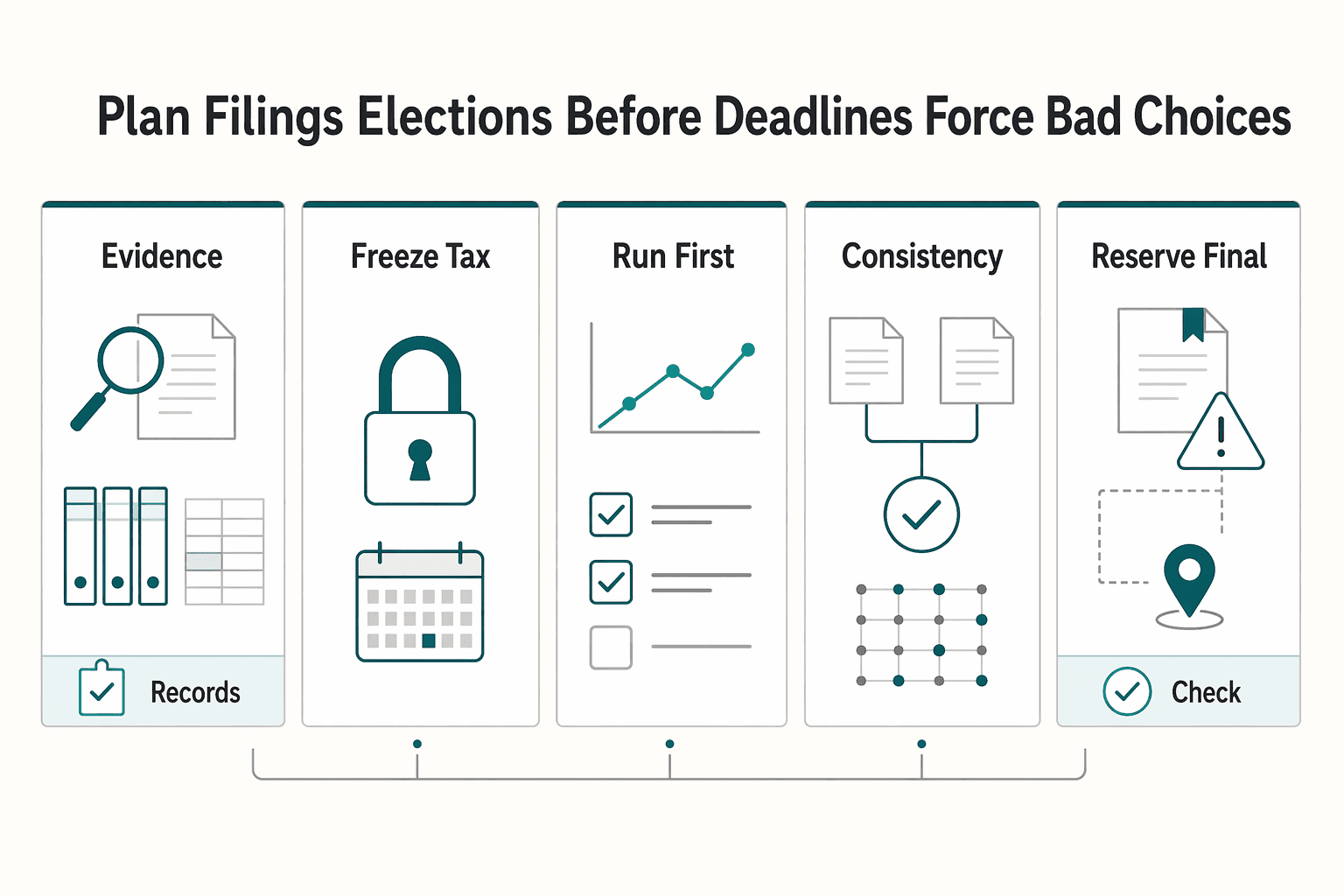

Plan filings and elections before deadlines force bad choices#

The safest pre-filing move is sequence control: finish source classification first, then compare filing elections.

| Pre-filing step | Article guidance |

|---|---|

| Close document intake | Before first-pass calculations; treat late items as exceptions |

| Freeze tax bucket labels by stream | Before any election modeling |

| Run a first-pass computation | Log material assumptions |

| Check consistency | Across contracts, invoices, and declared tax labels |

| Reserve a final review window | For adviser input and disclosure wording |

The provided excerpts are not authoritative guidance on Hong Kong filing elections, so keep this as planning discipline and confirm jurisdiction-specific rules with a qualified adviser.

Use a fixed pre-filing cycle:

- Close document intake before first-pass calculations, and treat late items as exceptions.

- Freeze tax bucket labels by stream before any election modeling.

- Run a first-pass computation and log material assumptions.

- Check consistency across contracts, invoices, and declared tax labels.

- Reserve a final review window for adviser input and disclosure wording.

Only compare election outcomes after classification is stable. If scenario testing forces re-labeling or source changes, stop and fix classification first.

Sequence protects decision quality. When election analysis starts before stream labels are stable, numbers can look precise while underlying assumptions are still moving. That creates false confidence and rework close to filing.

Keep an issues log during the pre-filing cycle. Each unresolved item should show owner, required evidence, and the decision it could affect. This makes it clear which points are minor cleanup and which points can change filing position.

If records are still incomplete near filing time, use the most defensible position supported by documents already in hand and escalate unresolved items through professional advice.

Know when to escalate to a professional#

Escalate before filing when your position depends on contested facts, unclear treaty or CDTA treatment, or unresolved evidence gaps.

Use this escalation checklist before sign-off:

- A material stream can reasonably be sourced to more than one jurisdiction.

- A treaty or CDTA interpretation would materially change the outcome, and you are not confident in that reading.

- Your offshore non-taxable position relies on inference instead of consistent records.

- Contracts, invoices, and tax labels do not reconcile for one or more material lines.

- You are close to filing with unresolved source, treaty, or classification assumptions.

Offshore claims often receive close review, especially when the record trail is thin. Claims can fail when evidence is inconsistent, incomplete, or contradictory.

Source or taxability characterization is another trigger. If key facts can plausibly be read more than one way, escalate and document what is still unresolved.

Timing is a trigger too. Some non-IRD guidance notes profits tax returns may be due within one month of receipt from the IRD, so treat your actual notice as controlling. If core source or treaty issues are still open in the final filing window, escalate immediately.

Escalation works best when it is structured. Send your adviser a concise packet that includes stream labels, core facts, conflict points, and the decisions that depend on each unresolved issue. Clear inputs can produce faster and more useful advice.

Avoid late escalation based on urgency alone. Fast advice on messy records can still leave core uncertainty unresolved. A cleaner handoff, even slightly earlier, can reduce risk and last-minute rewrites.

For a clean adviser handoff, provide a one-page fact pattern, stream-level source labels, treaty or CDTA questions, and the contradictions you could not resolve.

Use Gruv records to reduce compliance stress#

A traceable record chain from collection to conversion to payout can make your filing narrative easier to defend and easier to review.

For each material line, keep one stable transaction reference and map it to the related contract, invoice, payment event, and payout event. When conversion is involved, keep linked timestamps and any available rate context in the same trail so reviews stay clear.

Keep each record pack clearly scoped by reporting period, entity or account owner, and included channels. Update packs in dated increments instead of mixing periods or rails into ad hoc sheets.

Before filing, run one consistency checkpoint:

- Freeze the cut date and the records for that scope.

- Reconcile totals to external statements and flag unmatched lines.

- Keep plain-language notes for material edits, including who changed what and why.

- Reopen only affected lines when a mismatch appears, and log the correction the same day.

If you run multiple payout rails, apply one normalization rule across rails before assigning tax labels. Keep labels tied to the same transaction records and evidence set, not separate side sheets, so totals stay consistent across reviews.

Use stream-level mapping, not global totals, for tax labeling. A clean month-end total can still hide stream-level errors if labels were assigned too early or without source checks. Map labels where the record is created, then keep that label attached through reconciliation.

When a mismatch appears, record the reason for correction in plain language. Future reviews are much easier when the file shows why a change happened, not just that numbers changed.

If evidence for a material line is incomplete, use conservative treatment and escalate for professional review rather than forcing a clean close. Related: The 'Compliance Moat': Why RegTech is a Defensible Strategy.

Conclusion#

Hong Kong can still work for mobile consultants, but only when your facts and records support a source-based position.

Use a conservative rule from start to finish: classify each income stream, test source in a consistent order, and keep evidence that matches what happened in practice. Before filing, run a final consistency check across narrative, tax labels, and documents.

Avoid shortcut logic. Bank account location does not determine source, and residency is not a reliable shortcut for profits tax outcomes outside treaty context. Also avoid assuming offshore always means untaxed, especially after the refined FSIE changes effective from 1 January 2023 and expanded from 1 January 2024.

If you want a practical closeout, use this sequence. First, finalize stream labels and source notes. Next, reconcile records and resolve conflicts. Then escalate unresolved treaty, mixed-source, or classification questions before filing. This order can reduce rework and improve decision confidence.

Treat unresolved assumptions as explicit risks, not background noise. When each risk has an owner, evidence request, and next decision date, filing choices are easier to control under deadline pressure.

Next step: run your viability check now, document assumptions in writing, and escalate early where uncertainty remains. If your result depends on treaty interpretation, mixed-source facts, or unresolved assumptions, get professional review before filing and consider whether an advance ruling path is appropriate.

Frequently Asked Questions

Does Hong Kong tax foreign income for freelancers and consultants?

For profits tax, Hong Kong applies a territorial source principle: profits with a Hong Kong source are taxable, while profits sourced elsewhere are generally outside Hong Kong Profits Tax. The practical task is to support your source position with records that stay consistent across the full file. If your stream is mixed across locations, do not assume offshore treatment until your evidence is strong and internally consistent.

Does tax residency matter less than source under Hong Kong rules?

Profits tax is addressed through source determination under the Inland Revenue Ordinance and common law principles. The FSIE economic substance requirement is treated separately and does not change how source of profits is determined. If your position relies on residency or treaty points, verify those separately before filing.

What actually counts as Hong Kong-sourced income in practice?

There is no single shortcut that resolves source for every case. The principle is clear, but outcomes can be contentious in fact-heavy cases. Keep your narrative and records internally consistent for each stream. If your documents and story diverge, treat the stream as uncertain until the conflict is resolved.

Does getting paid into a Hong Kong bank account make income taxable in Hong Kong?

This grounding pack does not provide a rule that bank account location, by itself, determines profit source. Base your position on source analysis under the Inland Revenue Ordinance and common law principles, supported by documentation. If the fact pattern is unclear, treat the position as uncertain until you verify it.

How should I apply the 60-day rule without miscounting days?

Confirm the 60-day rule mechanics, thresholds, and day-count method with the relevant authority before filing, and get professional advice if your eligibility is unclear.

When should I use personal assessment or joint assessment?

Joint assessment may be chosen if it is more beneficial. For detailed personal assessment or election rules, confirm the current criteria before making an election.

When should I stop self-assessing and hire a cross-border tax professional?

Escalate when source can be argued more than one way, your records conflict, or your filing depends on assumptions you cannot evidence. Escalate earlier if deadlines are tight, since some returns may be due within about one month of issue. Professional input is most useful before filing, when corrections are still low-cost. Bring a structured handoff pack so advice can focus on real decision points, not document cleanup.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/event/115th-congress/senate-event/LC64382/texttrusted

- home.treasury.gov/system/files/136/2022-National-Money-Launder...trusted

- hsgac.senate.gov/subcommittees/investigations/library/files/r...trusted

- mgaleg.maryland.gov/cmte_testimony/2023/wam/12610_03032023_12451...trusted

- state.gov/reports/2024-investment-climate-statements/h...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Why RegTech Becomes a Defensible Compliance Moat

RegTech becomes a moat only when it makes compliance decisions easier to execute and defend. The buying decision comes down to one question: does this investment create durable capacity, or does it add overhead your team must carry?

Set Up a Solo 401(k) for Crypto With Audit-Ready Controls

Set up your **solo 401k crypto** plan as a sequence, not a product search. Build plan structure first, verify provider claims in writing, then fund and transact.