Quick Answer

Yes: treat hiring a subcontractor as a controlled rollout, not a quick handoff. Finalize a Statement of Work, sign the independent contractor agreement, and complete classification notes before work begins; then pay only after accepted deliverables and a Form W-9 in your records. Keep one contractor entity name across agreements, invoices, and payout records so responsibility stays clear. That sequence reduces dispute risk and makes the process repeatable.

Hiring your first subcontractor without legal or payment surprises#

Start with a risk-control sequence, not an ad hoc handoff. As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Most early problems start small and get expensive later. A vague scope, verbal approval instead of signed terms, or money moving before the paperwork is complete can lead to missed deadlines, messy offboarding, and misclassification trouble. This guide lays out a practical sequence to help you avoid those patterns from the start.

Who this guide is for#

This guide is for independent professionals moving from solo delivery to a small delivery team. You still own the client relationship and want outside help without losing control of scope, documentation, or payment.

It is not for large general contractor operations with multi-crew site and trade compliance layers. The focus is practical: lightweight controls you can actually repeat as you scale outsourcing.

What clean delivery requires first#

Before you draft a contract, define the work in a clear Statement of Work (SOW). That first scope checkpoint gives both sides a concrete reference for deadlines, revisions, and acceptance. Then lock in two controls this guide keeps returning to:

- Collect pre-start documentation, especially a signed written subcontractor agreement with indemnification language and any proof you require, such as liability insurance.

- Approve payment against documented scope and acceptance, not urgency.

Use a simple go or no-go check before kickoff: the SOW is final, the agreement is signed, and required documents are in the file. If that check fails, pause the assignment.

The reusable sequence for growth#

Use the same order each time to reduce legal and payment surprises:

- Define scope and boundaries first.

- Put written terms in place.

- Collect required onboarding and compliance documents before work starts.

- Tie payment to documented deliverables and acceptance.

- Keep records organized from day one.

That is the sequence this guide keeps coming back to. It gives you a process you can reuse as outsourcing grows, without turning your business into paperwork for its own sake.

If you want a deeper dive, read The Department of Labor's New Independent Contractor Rule (2024).

Should you hire a subcontractor now#

Do not make this decision on instinct alone. Move forward when the need is repeatable, your handoff process is clear, and the work still makes economic sense after adding coordination overhead. If one of those pieces is missing, fix that first.

Run the checkpoint before you commit#

Use this practical screen before you commit:

| Checkpoint | What to confirm |

|---|---|

| Demand | Need is repeatable, not just urgent |

| Process | You can define the task, review the work, approve payment, and manage the relationship |

| Economics | The work still makes economic sense after coordination overhead is included |

- Demand is repeatable, not just urgent. One overloaded week is different from sustained need.

- Your process is documented enough to hand off. A useful sequence is requirements, source selection, financing, performance, and contract administration. In practice, ask yourself whether you can define the task, review the work, approve payment, and manage the relationship.

- The economics still hold with coordination work included. You are paying for execution and for the management overhead that comes with it.

Read the bottleneck correctly#

The right answer depends on the real constraint. If demand is inconsistent, adding delivery capacity can add coordination cost without solving the actual problem. If fulfillment capacity is the issue and your quality bar is already clear, outsourcing can help you deliver more reliably. A common failure mode is bringing someone in while the scope is still blurry. That usually increases coordination load instead of reducing it.

Pick one measurable outcome for the first hire#

Choose one success metric before kickoff, then review accepted work against it. Common choices include:

- Turnaround time for a standard deliverable

- Quality consistency under your Contractor standards

- Revision volume before client approval

Write the expected result into the SOW or scope document so the decision is based on evidence, not impressions. Need the full breakdown? Read How to Manage a Global Team of Freelancers.

Define scope and role boundaries before you post anything#

The boundary should be clear before you hire. The subcontractor should own a specific deliverable, while you keep client-facing authority and final acceptance. Put that in a written scope document so scope, decisions, and rework are settled before work starts.

Think about the assignment in outcomes, not a step-by-step script. A results-focused scope keeps things tight without turning the subcontractor into the person managing your full client relationship.

Use a work order to draw the edge of the job#

Your written scope should make the start and stop points obvious:

- Name the deliverable, not the whole engagement.

Assign a bounded output, not broad ownership like "handle everything."

- Describe required results in observable terms.

Include output, quantity, due date, format, and how quality will be checked.

- State exclusions.

Note what is out of scope unless added in writing, such as strategy, client calls, or extra revision work.

If someone could read the document and still assume they own client messaging or approval decisions, the boundary is too loose.

Split responsibilities before work begins#

Separate lanes keep accountability clear from the start.

| Area | Contractor keeps | Subcontractor handles |

|---|---|---|

| Client communication | Client updates, scope changes, final commitments | Status updates to you unless you approve direct client contact |

| Revisions | Approves revision rounds and scope changes | Completes agreed revisions within scope |

| Sign-off authority | Final acceptance and client delivery | Submits completed work for review |

Define acceptance and rework in plain language#

"Delivered" and "accepted" are not the same thing. Write acceptance criteria tied to quality and quantity so approval is based on clear checks, not impressions.

Include:

- what you check, such as format, required components, deadline, and quality bar

- how you check, such as with a checklist, QA pass, or brief-to-output comparison

- what happens if it fails, including the correction path and when the work is treated as incomplete

Scope-related disputes are a common source of conflict, so vague acceptance language is expensive.

Add a simple escalation path now#

Decide what happens before the first issue shows up. Cover missed deadlines, quality misses, and handoff failures in the scope document or attached agreement.

Keep it simple:

- what triggers escalation

- who is notified and when

- what corrective step comes next

- when work pauses for written scope clarification

If you want a formal backstop, add a drafted mediation or arbitration clause in the broader agreement. Keep signed versions, scope changes, and acceptance notes together so decisions are documented.

Related reading: How to Manage an Offshore Development Team Across Time Zones.

Set your business structure before you delegate risk#

Pick the business entity that will take the subcontracting risk before work starts, then use that same entity everywhere. If subcontracting is still occasional and tightly bounded, keep the setup lean but documented. If it is becoming a repeat delivery model, treat an LLC as a serious next-step decision before you add more complexity.

This is an operating control, not a branding choice. Outsourcing can expand capacity, but it also expands risk, and handing off work does not automatically hand off every responsibility.

Pick one contracting party and use it everywhere#

Use one party name across the whole chain: the scope document, Independent contractor agreement, client invoices, and payment records. When those names drift, accountability gets blurry right when you need clean ownership for scope, quality, or third-party issues.

Use a simple decision rule#

If you are testing occasional overflow with one subcontractor on clearly bounded tasks, a Sole proprietorship may be workable when each assignment has a signed agreement, detailed scope, timelines, and quality standards.

If you are building ongoing capacity, filling specialization gaps repeatedly, or coordinating multiple subcontractors at once, pause and evaluate whether an LLC structure is the cleaner operating fit before scaling further.

If you want a deeper decision check, see When Should a Freelancer Upgrade from Sole Proprietor to an LLC?.

Verify the paper before kickoff#

Before work begins, run one consistency check:

- Contractor name matches across the agreement, scope document, invoice template, and filing records

- signer matches the business that is actually hiring the subcontractor

- payee and record-keeping names match the party receiving client revenue and paying the subcontractor

That keeps ownership clear and helps prevent avoidable delays and conflict once delivery is underway.

You might also find this useful: How to Delegate Work to a Virtual Assistant.

Prepare the minimum compliance packet before kickoff#

When you bring on a subcontractor, finish the minimum compliance packet before work begins. If status, scope, or tax details are unresolved on day one, your file is already weak. Use one Contractor name across every document, then track what you collected, reviewed, and cleared.

Build the packet in one place#

Keep the pre-start packet together so you can review it quickly and defend it later. At minimum, it should include an Independent contractor agreement, an Independent contractor status clause, a completed Form W-9, and a signed scope document.

| Item | Collect by | What to verify |

|---|---|---|

| Independent contractor agreement | Before first day of work | Correct legal names, signatures, core business terms, and whether needed defense or indemnification language is missing |

| Independent contractor status clause | Before first day of work | Language reflects a nonemployee relationship and matches how work will actually be done |

| Form W-9 | Before first payment, ideally before start | Subcontractor gives it to you, the requester, and line 1 name matches the TIN to reduce backup-withholding risk |

| Scope document | Before first day of work | Scope, deliverables, deadlines, acceptance criteria, and approver |

This timing split is an operating control, not a universal federal rule. A practical standard is simple: no agreement, status clause, or signed scope, no start. No W-9, no payment.

Document classification before work starts#

Do not treat the status clause as the whole classification analysis. The IRS points to three evidence categories: behavioral control, financial control, and relationship of the parties. DOL guidance frames the question around economic dependence versus being in business for oneself.

Your classification note should clearly answer:

- Behavioral control: Who controls methods, schedule, tools, and instructions?

- Financial control: Who bears business risk, provides tools, and has profit-or-loss exposure?

- Relationship of the parties: What do the agreement and the real working arrangement show about permanence, exclusivity, and responsibility?

Under DOL materials, actual working practices matter more than what is written only in a contract. Guidance is also in transition. The 2024 rule took effect on March 11, 2024, and on February 26, 2026 DOL announced a proposal to rescind it. A proposal is not a final change, so document that you reviewed current guidance.

If the facts are mixed and you cannot defend the classification, pause before kickoff. For worker-status uncertainty, the IRS process is Form SS-8.

Separate start approval from pay approval#

Use two gates so legal setup and payment approval do not get tangled together.

| Stage | Requirement |

|---|---|

| Before first day | Agreement signed |

| Before first day | Independent contractor status clause included |

| Before first day | Scope document signed |

| Before first day | Classification note completed |

| Before first payment | W-9 on file |

| Before first payment | Name and TIN checked |

| Before first payment | Payee name matches accounting records |

| Before first payment | Delivered work maps to the signed scope document |

Keep those gates separate. This prevents a common failure: the work is done, but payment stalls because tax details or legal-name checks were skipped.

Keep a verification log you can defend#

A short verification log is enough if it captures what mattered. Track the document, reviewer, review date, issue found, and cleared date, plus any mismatch notes if needed.

That makes the file defensible. You can show what was signed, what was reviewed, and who cleared each item. Watch for a contract-heavy, fact-light file. If the paperwork says "independent contractor" but the real arrangement shows tight control, fixed hours, exclusivity, and low business independence, reassess status before expanding the work.

Once the packet is complete, move to screening with the same discipline. The point is to evaluate delivery fit and compliance fit separately, then move forward only when both are clear.

Separate capability checks from compliance checks#

Do not let a strong candidate interview blur the compliance review. In one NYC RFP example, proposal evaluation and subcontractor compliance are treated as distinct parts of the process. Use the same logic in your own process: first assess whether the candidate can deliver the work, then confirm the person and business details you are actually engaging.

Use one short checklist for delivery fit and apply it consistently across candidates. Keep your notes tied to the real work, not portfolio polish.

Verify identity and claimed experience before access#

A strong interview is not enough on its own, especially in remote hiring. One documented anecdote describes a day-one identity mismatch, and another describes resume confusion from similar company names.

Before granting client access or production credentials, confirm that interview identity, work history claims, and business and payment details are internally consistent. If details conflict or remain unclear, pause and resolve that first.

Keep backup options so one miss does not stall delivery#

Maintain a small vendor list with at least one viable backup for each critical task. The goal is continuity. If one candidate drops, misses timing, or fails screening, you can keep delivery moving without restarting the search from zero. Track concise notes per candidate, including screening status, key checks completed, and current readiness, so decisions stay evidence-based.

Use a paid micro-test only as a controlled checkpoint#

A paid micro-test can be useful, but only if it is tightly controlled. Tie it to a real assignment, keep the scope narrow enough to review quickly, and define the deliverable, due date, and acceptance criteria in writing.

Treat the result as decision evidence, not a formality. If execution or consistency is weak at this stage, do not expand scope yet.

Related: The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

Before kickoff, draft a clean baseline agreement and scope with the freelance contract generator.

Choose pricing and payment controls that protect margin#

Margin usually disappears through a bad price model or weak payment gates. Use fixed-fee when scope and acceptance are clear. Use capped hourly when scope is still moving.

Match price model to scope reality#

The price model has to match the actual work, not the version you hope it will become.

| Situation | Pricing approach | Control |

|---|---|---|

| Scope is stable and acceptance is easy to verify | Fixed-fee | Use milestone sign-off |

| Scope is uncertain or likely to change | Capped hourly | Require weekly review |

| You cannot explain what "approved" means in one short paragraph | Do not use fixed-fee yet | Approval is not defined clearly enough |

Use fixed-fee only when the written scope clearly defines output, handoff format, revision limits, and the person who accepts the work. Tie payment to milestone acceptance so payout follows approved progress, not effort that may still need rework. Fixed-fee breaks down when delivery depends on discovery, ongoing client feedback, or open-ended revision rounds. Those are the same conditions where scope creep, rework, and untracked labor can erode margin quickly.

Hourly works better when timing is uncertain or inputs change week to week, but it still needs limits. Set a cap, require weekly review, and record work against the approved scope document so margin drift shows up early. Without a cap, review cadence, and clear task boundaries, you end up paying for activity instead of outcomes.

A practical decision rule:

- If scope is stable and acceptance is easy to verify, use fixed-fee with milestone sign-off.

- If scope is uncertain or likely to change, use capped hourly with weekly review.

- If you cannot explain what "approved" means in one short paragraph, do not use fixed-fee yet.

Make payment contingent on proof#

Set payout prerequisites in writing before work starts, then apply them consistently. At minimum, require an approved scope document, confirmation that deliverables met acceptance criteria, and the documents in your intake packet.

If your process includes Form W-9, keep it as a pre-payment gate instead of collecting it late. Also confirm that payee name, business details, and submitted documents match what was screened.

Keep the document hierarchy aligned. Public contract templates often use an order of precedence so conflicts are resolved by ranked documents. You can apply the same idea by keeping your agreement, scope document, and payment terms consistent.

Before you approve payout, the file should answer three questions without extra follow-up: What was ordered? Was it accepted? Are required documents on file?

Add repeat-hire controls before volume grows#

Most control gaps show up on repeat payments, not the first one. Add three lightweight controls now:

- Set a pre-work approval checkpoint for pricing model, cap or milestone amount, and current scope document version.

- Track payouts by vendor, not only by project. Your Vendor list should show pricing model, latest documents received, total paid to date, and any approved exception.

- Route exceptions, such as early payment, a scope add-on, or over-cap hours, through the same vendor record so decisions stay visible and consistent.

In one public-sector example, New Jersey state-contract terms require valid business registration for the contractor and each named subcontractor before contract entry. They also require a complete subcontractor list with addresses before final payment. That does not automatically apply to private engagements, but it shows how tightly some environments tie payment to record completeness.

Choose traceable payout methods#

Payment timing is not universal, so set it in your agreement and scope document. For the payment method, choose traceable electronic rails where possible.

ACH is described as faster to process than some alternatives. Cash can increase tax risk and reduce auditability. Paper checks can be delayed or lost, and they can also slow cash flow when clearing takes time.

If Gruv Payouts fits your setup, use it where supported to keep payout operations traceable and easier to review later.

Negotiate contract terms that prevent predictable disputes#

Once pricing and payment controls are set, the next job is to cut down the disputes you can already see coming. Most of them trace back to the same places: scope, status, communication, IP, and exit rights in your Independent contractor agreement.

Use the agreement to settle the work boundary#

Unclear scope is a common dispute trigger, so settle the boundary in writing. Keep the master agreement focused on relationship rules, then attach or reference a scope document that states deliverables, acceptance, delivery format, and revision handling. If no document clearly defines what "done" means, the disagreement usually moves straight to rework and payment.

Use this quick boundary checklist:

- Name the exact deliverable, not just a service category.

- State the handoff format, such as source files, exports, or final approved copy.

- Define who can request changes and when revisions become new scope.

- Set confidentiality duties tied to real risks, including return or deletion of sensitive materials at offboarding.

- Include termination rights and what gets paid if work stops midstream.

If you include termination for convenience, pair it with cleanup terms for in-progress work, approved milestones, and credential access on the termination date.

Keep status language explicit, but do not rely on labels alone#

Include an Independent contractor status clause, but do not treat the label as proof by itself. Written contracts are only one relationship factor. Classification still depends on the full facts, including behavioral control, financial control, and relationship factors, and DOL guidance applies a multifactor economic reality analysis.

Write the clause to match how the work is actually performed, then operate that way in practice. If the relationship becomes long-term, exclusive, and open-ended, treat that as a misclassification red flag and reassess before expanding the engagement. For a deeper breakdown, see Independent Contractor Status: The Most Important Clause for Avoiding Misclassification.

Set communication rules that protect client delivery#

Communication terms need to work like operating rules, not general intentions. Put three items in writing: the approved channel, expected response window, and escalation path for blockers. Avoid broad phrases like "timely communication." Use standards that match your client commitments, and confirm them early in the first assignment.

Match IP terms to the actual output#

Do not assume payment transfers ownership. Copyright ownership does not automatically transfer just because work is commissioned, and work-made-for-hire treatment applies only in specific situations.

If you need control over reuse, edits, sublicensing, or transfer to a client, put assignment or license terms in writing. If the subcontractor keeps preexisting tools or templates, carve those out clearly and define the usage rights you are buying.

Onboard the first 30 days with checkpoints#

The first 30 days are for verification, not optimism. You are trying to confirm two things early: the work meets your standard, and the documentation holds up in practice before you expand scope.

Start with access, documents, and one tightly defined assignment#

For Day 1 to 3, keep the first assignment narrow and testable. Confirm in writing what "done" means, delivery format, who approves, and where handoff happens.

Your first checkpoint is document completeness. For standard client work, that means the agreement and first scope document are fully signed and stored before meaningful work starts. If the work sits inside a federal-aid contract chain, treat missing required forms or certifications as a stop signal, not an admin cleanup task.

Check the work product, not just responsiveness#

In Week 1 to 2, review early deliverables against the scope document and track correction patterns. Fast replies do not matter much if handoffs are incomplete, revision notes are missed, or acceptance criteria are not met.

Use a short review after each early delivery:

- Did the deliverable match the exact assignment, including format and completeness?

- Were revisions minor clarifications, or did you need to restate core instructions?

- Did the handoff create extra cleanup, missing-file follow-up, or status confusion?

- Is the same issue repeating after feedback?

Repeated misses after clear feedback usually point to a scope, fit, or capacity problem.

Add compliance screening where the project requires it#

If the project touches public or federally funded work, add eligibility screening in the first two weeks. A key check is whether the provider and its principals certify they are not presently debarred, suspended, proposed for debarment, declared ineligible, or voluntarily excluded.

If they cannot make required certification statements, require an attached explanation in the proposal package and review it before expanding access or scope. Keep any exception documentation in the vendor file, including notes tied to the three-year lookback language in the certification process.

Use weeks 3 and 4 to decide scope, not to hope#

By Week 3 to 4, make a decision based on evidence from delivery quality, revision pattern, handoff reliability, and document status.

- Continue and expand scope when work is acceptable, feedback is absorbed, and the handoff reduces your load.

- Limit scope when the output is usable but still needs close supervision.

- Replace from your Vendor list when the same operational issue repeats, documents stay incomplete, or required certification issues remain unresolved.

If the first month already needs constant rescue, expanding scope usually increases risk instead of fixing it.

For a step-by-step walkthrough, see The Legal Difference Between a 'Joint Venture' and a 'Subcontractor' Relationship.

Sanity checks before first payment#

Release the first payment only after four checks pass. If one fails, pause and fix the file first.

- Confirm the file is complete enough to pay.

Keep the signed Independent contractor agreement and completed Form W-9 on file before payment. On the W-9, verify the exact legal name and Tax ID match the payee in your records. Incomplete W-9 or payment setup details can delay payment, often by about 7-14 days in practice.

- Match the payment to accepted work, not effort alone.

Approve payment against the agreed scope document and acceptance criteria. Confirm the delivered files, format, and revision status match what was approved, not just that the subcontractor was responsive. If core corrections are still open, treat it as a delivery issue first.

- Review classification notes before paying as a contractor.

Before deciding how to treat service payments, confirm your business-relationship classification notes are current and match how the work is actually performed. The DOL FLSA classification final rule took effect on March 11, 2024, and DOL announced a new NPRM on February 26, 2026, so this remains an active area. If your notes are missing, stale, or contradictory, review before paying as an independent contractor.

- Make the bookkeeping record tie out cleanly.

Make sure the payment amount, recipient, and approval record all match in your Contractor bookkeeping process. Keep the agreement, W-9, scope document, acceptance note, and payment record together so year-end reporting is straightforward. This is the checkpoint that prevents small admin mismatches from turning into larger tax or audit issues later.

Keep tax and audit records clean from day one#

Audit-ready records come from consistency, not year-end cleanup. Treat each subcontractor payment as one documented chain from the start: W-9 details, approved work, payment record, and any corrections tied together.

Track each payment for Form 1099-NEC review#

Once you determine someone is an independent contractor, collect Form W-9 first and use it to verify the payee legal name and TIN in your payment record. Tag each payment for 1099 review as it is made, not at year-end.

For business payments to a non-employee for services, the IRS FAQ states reporting on Form 1099-NEC at $600 ($2,000 for payments made after December 31, 2025) or more. If backup withholding applies, report any amount of federal income tax withheld. Also keep an exception flag, because the IRS notes there are situations where Form 1099-NEC is not required.

Keep one searchable file per Vendor list entry#

Store each vendor file so the full evidence pack is easy to pull up in one place. For each Vendor list entry, keep:

- signed Independent contractor agreement

- completed Form W-9

- scope document

- invoice

- acceptance or approval note

- payment confirmation

- credits, corrections, or revised invoices

Keep the completed W-9 in your files for four years.

Reconcile monthly so gaps are caught early#

A monthly reconciliation is usually enough to catch problems before year-end. Check your vendor list against accounting records and confirm:

- no one was paid without a W-9 on file

- threshold-related payments are flagged for 1099 review

- each payment ties to approved work and payout evidence

- corrections or reversals are clearly linked

If payments begin to look like employee wages rather than contractor services, reassess treatment before continuing with 1099 handling. Wages and other employee compensation generally belong on Form W-2, not Form 1099-NEC.

Maintain a simple audit trail#

Keep a short log that shows inputs, approvals, payouts, and corrections, with links back to source documents. When a payment changes, note what changed and why so each final number stays traceable.

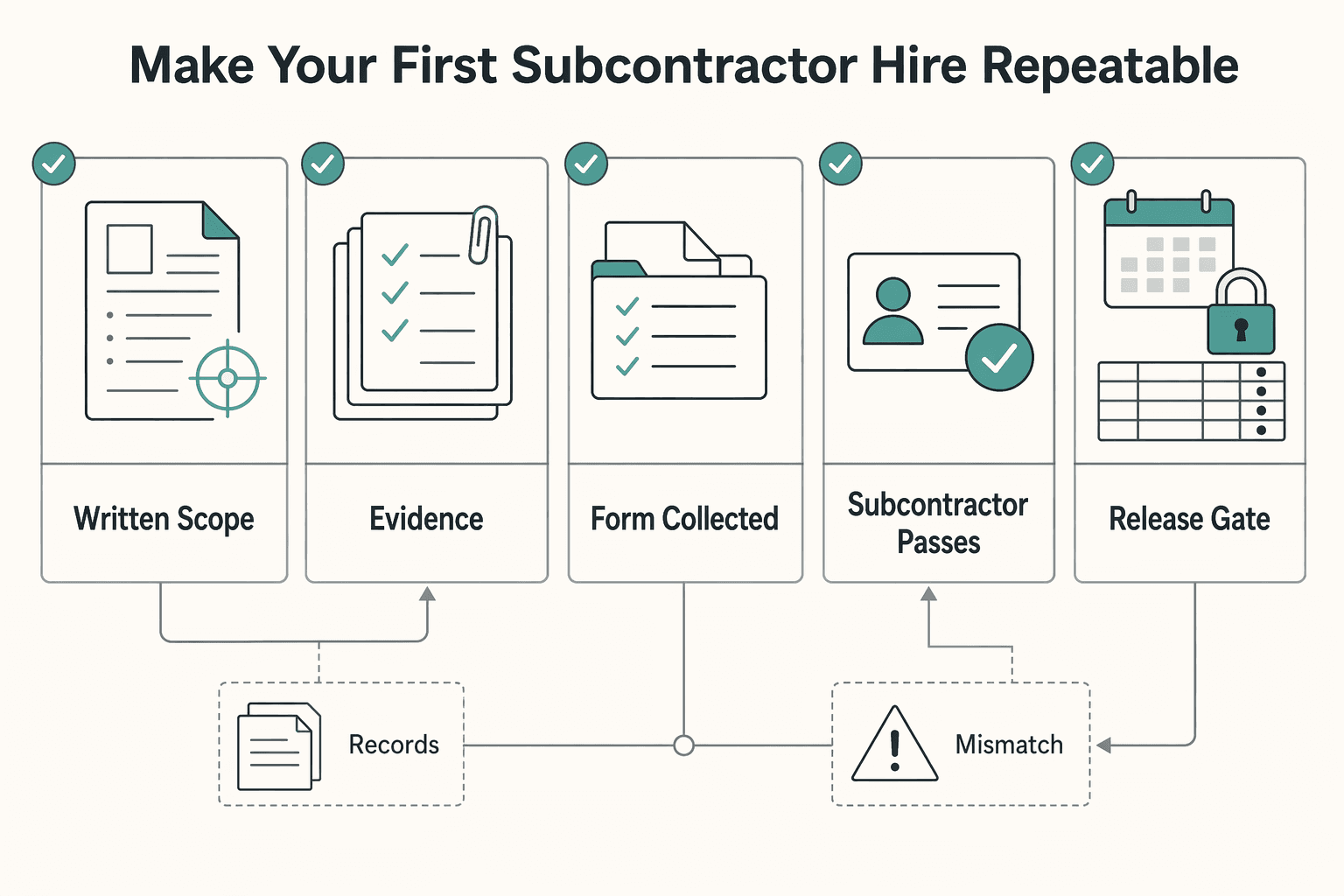

Make your first subcontractor hire repeatable#

The goal is not just to make one hire work. It is to build a sequence you can reuse: scope first, compliance packet second, screening third, then payment controls. That order helps you avoid the common result of subcontracting without structure: more rework, more confusion, and more stress.

1. Scope first. Start with a written scope document before candidate outreach. Define the scope and deliverables in writing, including what completion and approval look like.

If you cannot describe "approved" in plain language, pause and tighten the scope first. Vague scope usually pushes management work back onto you and cancels out the capacity you were trying to add.

2. Build the compliance packet before kickoff. Once scope is clear, complete the paperwork before execution. At minimum, make sure written scope exists, required contracts are signed, and Form W-9 is collected and filed so your records are ready if you later need to issue Form 1099-NEC.

Treat completeness as the key control. Document decisions as you go, not later: who approved scope, when documents were signed, what changed, and who accepted delivery.

3. Screen with evidence, not urgency. When you are overloaded, availability can look like fit. Screen for fit against your written scope: work samples, communication quality, revision behavior, and follow-through.

For a first engagement, use a small paid pilot tied to a real assignment. Keep it low risk and easy to review so you can evaluate both output and reliability inside your process.

4. Add payment controls that match approval. Tie final payment to completion and approval, not effort alone. A practical checkpoint is to hold final disbursement until the job is completed and approved.

Use this checklist for your first run:

- Written scope and deliverables are approved.

- Required contract documents are signed and stored.

- Form W-9 is collected and filed.

- The subcontractor passes a small paid pilot.

- Final payment is released after approval.

Complete this checklist once, then run one low-risk pilot assignment before scaling. That gives you a safe way to find process gaps while the stakes are still small.

This pairs well with our guide on How to Hire Your First Salesperson.

When your checklist is stable and you need repeatable disbursement controls, review Gruv Payouts.

Frequently Asked Questions

What is the difference between a contractor and a subcontractor?

A contractor is the business your client hires, while a subcontractor is a person or business you hire to furnish supplies or services under that client work. In plain terms, the client relationship sits with you, and the subcontractor supports delivery. The label alone does not settle worker status, so you still need to determine whether the worker is an employee or an independent contractor.

When should I hire my first subcontractor instead of doing the work myself?

There is no universal timing rule, so treat this as a business decision, not a milestone decision. A practical signal is recurring demand with a clear scope and enough margin after subcontractor pay and rework risk. If demand is inconsistent, adding delivery cost too early can create more pressure than relief.

Which documents do I need before a subcontractor starts work?

Use a practical starter set: an independent contractor agreement, a written scope document, a completed Form W-9, and your worker-classification notes. On the W-9, confirm the taxpayer name and TIN align to reduce backup-withholding issues. Most disputes come from unclear scope and acceptance terms, so define those up front.

How should I set payment terms to avoid disputes and margin leaks?

Set payment terms around acceptance criteria, not just effort spent. For stable scope, fixed-fee milestones tied to approval are usually cleaner. For changing scope, capped hourly terms with regular review create a clear stop point. Put scope, acceptance, and required vendor documents in writing before payment.

Do I need a Form W-9 before paying a subcontractor?

Collect it before first payment. That gives you the TIN you may need for information reporting and helps reduce avoidable payment delays. Keep the completed W-9 in your records, and remember it goes to you as the requester, not to the IRS.

What is Form 1099-NEC and when does it apply to subcontractor payments?

Form 1099-NEC is used to report nonemployee compensation. IRS FAQ language currently says to report payments totaling $600, or $2,000 for payments made after December 31, 2025, when reporting conditions are met. Not every payment goes on Form 1099-NEC: credit card, payment card, and certain third-party network transactions are reported on Form 1099-K.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/subpart-2.1trusted

- acquisition.gov/far/37.602trusted

- copyright.gov/circs/circ30.pdftrusted

- copyright.gov/help/faq-definitions.htmltrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- dol.gov/agencies/whd/fact-sheets/13-flsa-employment-...trusted

- dot.ny.gov/portal/pls/portal/MEXIS_APP.PA_PLAFAP_ADMIN....trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Independent Contractor Status for Cross-Border Freelancer Contracts

A label helps, but it does not decide status on its own. What matters in practice is control: who decides the method, the sequence, and the day-to-day execution of the work.

When Should a Freelancer Upgrade from Sole Proprietor to an LLC?

Forming an LLC is usually an operations decision before it is a tax decision. If you are weighing a move from sole proprietor status to an LLC, start with exposure, contract risk, and how money moves through the business. Treat federal tax treatment as a separate choice, and verify it through IRS guidance instead of assumptions.

The Department of Labor's New Independent Contractor Rule (2026)

The right way to operate right now is simple: treat the DOL action as a live proposal, not settled law. The Wage and Hour Division published a Notice of Proposed Rulemaking on 02/27/2026 for worker status under the Fair Labor Standards Act, listed as RIN 1235-AA46. The proposal says WHD would rescind the analysis now codified at 29 CFR part 795 and return to the Department's 2021 approach, with modifications. It also proposes using the same analysis when FMLA or MSPA coverage is in play.