Quick Answer

Choose an eenmanszaak netherlands setup when your operations are still simple and you can accept personal exposure to business debts, then register cleanly through KVK and build controls immediately after filing. Use a staged workflow: confirm eligibility and address details first, complete registration accurately, and wait for Belastingdienst follow-up on VAT identifiers before assuming tax workflows are active. Revisit a BV once risk, contract stakes, or growth plans materially change.

What Does "Unlimited Liability" Truly Mean for Your Global Assets?#

Treat "unlimited liability" as a legal exposure question, not a tax registration question. If you are weighing an eenmanszaak netherlands setup, keep the main warning simple: clean VAT or GST registration evidence does not tell you whether a Dutch business claim can reach your personal assets, or how that plays out when some of those assets sit outside the Netherlands.

That distinction matters because administrative facts can feel more reassuring than they are. A regulator can confirm how to register, which identifier you receive, and how often you must file. None of that answers what happens if a client sues you, a contract dispute escalates, or enforcement is attempted against savings, investments, or property held in another country.

What this evidence confirms#

The material available for this section is Australian tax administration guidance, not Dutch liability law. It still confirms a few useful process points:

| Path | Setup | Filing / timing | Limits / notes |

|---|---|---|---|

| Standard GST registration | Needs an Australian business number before registration | Register within 21 days once required | Failing to register when required can lead to penalties |

| Non-resident standard GST registration | Can require extra identity proof and cannot be lodged electronically from outside Australia | BAS lodgment and payment can be monthly or quarterly | May increase processing time and you may need an Australian registered tax agent |

| Simplified GST registration | Create an AUSid account and online access; receives a 12-digit Australian reference number (ARN) | Must lodge and pay quarterly | Cannot issue tax invoices and cannot claim GST credits |

- In the Australian Taxation Office flow, standard GST registration requires an Australian business number before registration, and failing to register when required can lead to penalties. Once registration becomes required, the cited deadline is 21 days.

- For non-residents, standard GST registration can involve extra identity proof, may increase processing time, and cannot be lodged electronically from outside Australia. The ATO also says you may need an Australian registered tax agent. BAS lodgment and payment can be monthly or quarterly.

- Simplified GST registration is a different path for some non-resident businesses. A concrete checkpoint is creating an AUSid account and online access, after which the business receives a 12-digit Australian reference number (ARN). The tradeoff is explicit: you must lodge and pay quarterly, but you cannot issue tax invoices and cannot claim GST credits.

- The Australian Business Register defines a sole trader as a one-owner structure where that owner is legally responsible for business debts.

Those points are credible and practical if you are comparing registration paths or documenting offshore tax administration obligations. They still do not answer the question most readers actually mean when they hear "unlimited liability": what can be taken from you personally, through which legal route, and in which country?

The questions that still decide your real exposure#

Before you rely on a sole trader structure for larger contracts, work through these four checks and verify the current position with Dutch counsel.

| Check | What to verify | Examples named |

|---|---|---|

| Personal exposure mechanics | Which claims matter most and which personal assets may be exposed | Unpaid suppliers, tax debts, client contract damages, negligence, IP disputes, data issues, jointly held assets, assets held abroad |

| Cross-border enforcement | Where assets sit and how a Dutch judgment or settlement might be recognized or enforced | Bank accounts, receivables, investments, recognition, enforcement |

| Contract enforceability | Whether key contract terms will hold up | Liability caps, acceptance criteria, scope boundaries, jurisdiction clauses, choice of law language |

| Insurance fit | Whether the policy matches the work and covers the relevant exposures | Services, countries, claim types, defense costs, exclusions, retroactive dates |

- Personal exposure mechanics

Ask which claims matter most in your work: unpaid suppliers, tax debts, client contract damages, negligence, IP disputes, or data issues. Then ask exactly which personal assets may be exposed in those scenarios, including jointly held assets and assets held abroad.

- Cross-border enforcement

Liability on paper and collection in practice are not the same thing. Have counsel assess where your bank accounts, receivables, and investments sit, and how a Dutch judgment or settlement might be recognized or enforced in the countries that matter to you.

- Contract enforceability

Registration details do not resolve contract-risk questions. Get a current Dutch law view on liability caps, acceptance criteria, scope boundaries, jurisdiction clauses, and choice of law language before assuming those clauses will hold up.

- Insurance fit

Insurance can reduce risk, but only if the policy matches the work. Verify the current legal position with Dutch counsel, then confirm with a broker whether your policy covers the actual services, countries, claim types, defense costs, exclusions, and retroactive dates involved.

A common failure mode is straightforward: someone sees "sole trader means owner is responsible for debts" in one jurisdiction, then assumes that statement answers Dutch asset exposure, contract validity, and overseas enforcement too. It does not. Keep a separate evidence pack for each question.

What to do next before signing higher-risk client work#

If the project carries meaningful financial or legal downside, do this before you sign:

- Build a short file with the draft contract, statement of work, client jurisdiction, payment size, any liability cap, and where your major assets are held.

- Ask Dutch counsel for a written view on personal exposure, contract wording, and enforcement risk for that exact fact pattern.

- Review Sole Proprietorship vs LLC: The Definitive Guide for Global Freelancers.

- Only then move to the registration steps in the next section. Registration is the admin step. Deciding whether you are willing to carry the risk personally comes first.

Related: How to Register as a Sole Trader in the UK.

Your Proactive Checklist for Compliant KVK Registration#

Handle KVK registration as a compliance sequence, not a quick admin task. Every new business must register with the Netherlands Chamber of Commerce, and missing or outdated KVK records can become an immediate diligence red flag.

Split the work into three steps: pre-booking checks, appointment prep, and first-week controls after registration.

| Stage | Action | Verification cue |

|---|---|---|

| Pre-booking | Split immigration/work-right checks from KVK filing preparation | Confirm your current eligibility status and the current requirements for your case before booking |

| Appointment prep | Complete the intake and save exactly what you submitted | Keep a PDF or screenshot so names, dates, and activity wording match at the appointment |

| Appointment prep | Bring your appointment confirmation and the documents required for your case | Verify the current fee and document requirements against current KVK guidance |

| First week after registration | Open a separate business account and start bookkeeping/invoicing immediately | Use that account only for business income/expenses, and label self-transfers clearly as an owner's draw |

Keep one version of your business activity#

Use one clear activity description across your intake, KVK record, and early invoices. Inconsistent wording creates avoidable friction later when records are reviewed.

Keep a small file from day one: what you submitted, appointment confirmation, your KVK extract once available, and later Belastingdienst correspondence. This paper trail helps you prove what was filed and when.

Build post-registration controls right away#

As soon as you have KVK registration, run all business flows through the separate business account and keep proof tied to each expense. For VAT input claims, the Belastingdienst requires supporting documentation.

For personal withdrawals, use a specific reference such as owner's draw. Vague transfers make records less transparent and make tax periods harder to review.

If you want the next operational step after KVK, read How to Obtain a 'VAT Number' as a Freelancer in the Netherlands.

If your work also touches regulated payment operations, see Netherlands Payment Platform Compliance: DNB Licensing and PSD2 Implementation.

How to Optimize Your Taxes as a Global Professional#

Tax optimization here is a verification sequence, not a deduction hunt. Confirm taxing rights first, then choose a relief path, then claim only what your records can support.

Work in this order, and save a checkpoint at the end of each step:

- Confirm tax residency first. Determine residency under the relevant domestic rules, then save the documents you relied on.

- Confirm taxing rights next. Separate residency from where income is taxed, and if a treaty may apply, identify the exact article before modeling outcomes.

- Confirm the relief method last. Choose FEIE, FTC, or a treaty position only after steps 1-2 are documented, then align records to that method.

If you are a U.S. taxpayer, keep one boundary clear: FEIE is not a no-filing shortcut. You still report the income on your U.S. return, and FEIE requires a foreign tax home. For physical presence, verify the current IRS rule directly against your travel log before relying on it.

| Framework | What it does | Verify before use | Core records | Common failure mode |

|---|---|---|---|---|

| FEIE | Excludes qualifying foreign earned income | Foreign tax home, current eligibility tests, and the current limit are verified | Travel log, presence evidence, filed return, housing exclusion workpaper if used | Treating FEIE as no-filing, or relying on unverified eligibility |

| FTC | Credits eligible foreign taxes | Tax was actually imposed and each Form 1116 is handled by a single category | Category-specific Form 1116 support and proof of tax paid | Mixing categories or combining records across categories |

| Treaty position | Can change treatment in specific cases | Exact treaty article matches your facts; disclosure implications are reviewed where applicable | Treaty-article memo, residency support, consistent filing position | Using treaty language without article-level support |

Do not blend these mechanisms. FEIE and FTC solve different problems, and FTC category separation on Form 1116 is a hard workflow boundary. If you are also considering a foreign housing exclusion, compute that before finalizing FEIE amounts.

For Dutch-side planning, keep entrepreneur relief and the 30% ruling as separate gates from your U.S. relief method. Eligibility and applicability should be validated against current guidance before you model outcomes. If the ruling is part of your planning, read A Deep Dive into the Netherlands' 30% Ruling for Skilled Migrants.

VAT is a separate decision track from income-tax relief:

| VAT path | Client mix fit | Input VAT recovery impact | Switching consideration |

|---|---|---|---|

| Standard VAT | Useful when your commercial model expects VAT-charging workflows | You can recover eligible input VAT under normal rules | Assess admin load and transition effects before changing regimes |

| KOR | Consider only if your profile fits the scheme scope | Limited recovery can change net cost structure | Verify the current threshold and switching consequences before opting in |

For implementation, the practical next step is How to Obtain a 'VAT Number' as a Freelancer in the Netherlands. If treaty analysis is part of your file, use How to Make a Defensible LOB Call Under the US-Netherlands Tax Treaty.

The Strategic Choice: Eenmanszaak vs. BV for High-Earners#

Choose based on risk fit, not status labels. As your earnings grow, ask whether your current structure still matches your business model, risk level, and expansion plan.

| Factor | Eenmanszaak | BV |

|---|---|---|

| Legal baseline | No legal personality; you are the sole owner, and personal assets can be exposed to business debts | A limited-liability company form |

| Strategic fit | Can still fit when simplicity is the priority and your current risk profile is acceptable | Often evaluated when personal-risk exposure or expansion needs become harder to manage in a sole proprietorship |

| Decision risk | Wrong fit can increase personal risk or limit growth | Wrong fit can also limit growth if the structure no longer matches how the business operates |

There is no universal "best" structure and no single income line where everyone must switch. Reassess when your risk profile, operating model, or expansion plans change, and validate the legal and tax implications against current rules before deciding.

If you stay with an eenmanszaak, keep the operational basics clean: register with KVK using DigiD, and track post-registration steps, since KVK passes your details to the Belastingdienst. Also remember you can hold a maximum of one eenmanszaak.

A BV can improve separation, but it is not a blanket shield in every scenario. Keep your structure choice aligned with how you actually run the business and review it periodically as your exposure changes.

Related: Can Digital Nomads Claim the Home Office Deduction?.

We covered this in detail in Taxes in the Netherlands for Expats and Freelancers.

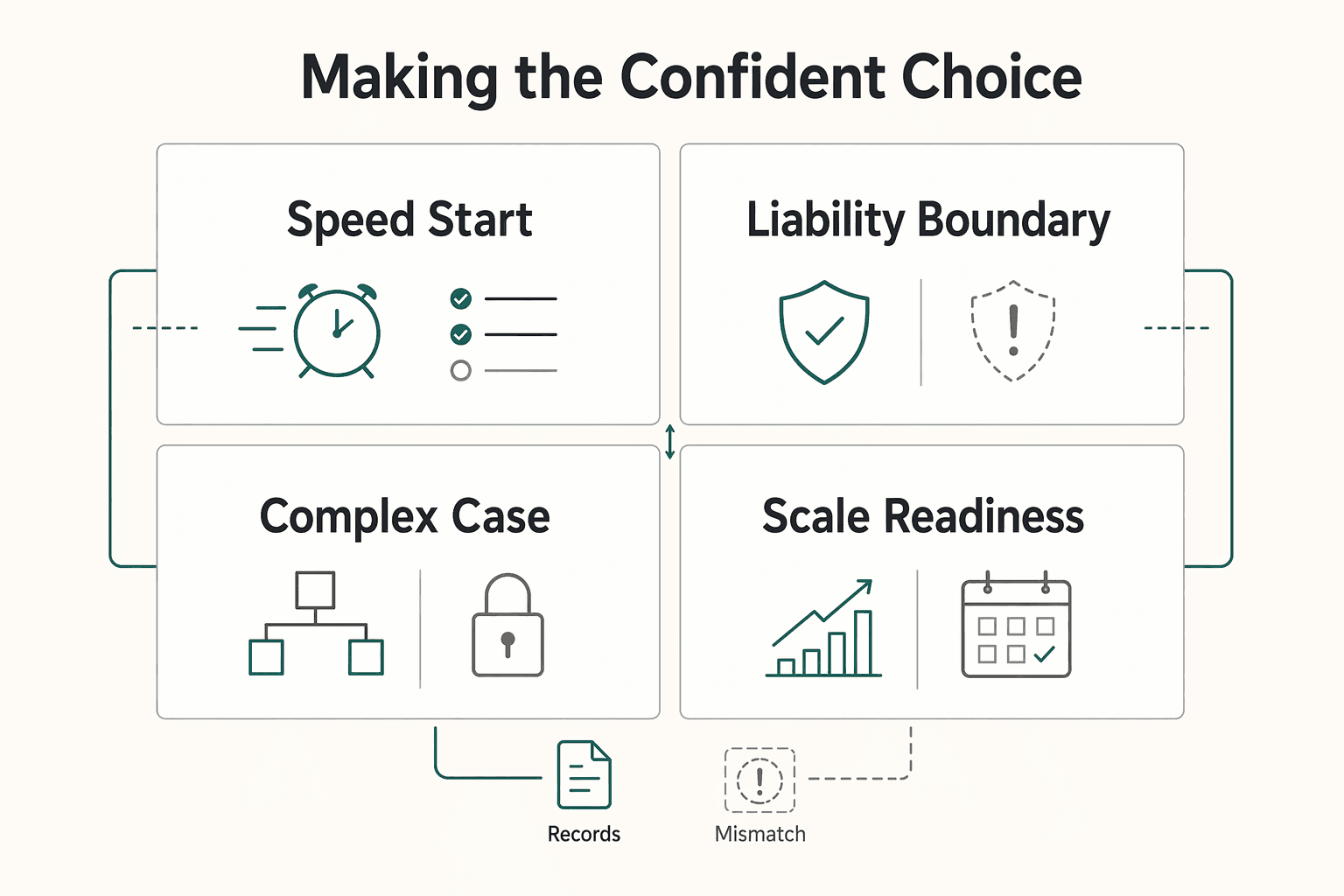

Your Final Blueprint: Making the Confident Choice#

Choose based on liability exposure, profit pattern, and buyer requirements, not on a default template. Stay with an eenmanszaak when your setup is still simple and exposure is manageable; prepare a BV when risk, ownership complexity, or scale needs are increasing.

Use this three-part checklist:

- Income pattern: If income is uneven and most profit supports your personal living costs, an eenmanszaak can still fit. If profits are consistently above your personal draw, model a BV with current verified numbers before you decide.

- Risk exposure: If a single dispute, debt, or claim would create serious pressure for you personally, prioritize a BV review. With an eenmanszaak, there is no separate legal person, and this evidence does not resolve the full personal-asset reach in every scenario.

- Long-term goals: If you expect share-based ownership or external funding, a BV is usually the stronger fit. If you are building a focused solo practice, an eenmanszaak can remain a practical structure.

| Decision factor | Eenmanszaak | BV |

|---|---|---|

| Speed to start | Direct sole-proprietor route | Incorporation route with added legal setup |

| Liability boundary | No separate legal person | Separate legal entity |

| Admin complexity | Fewer corporate formalities | More legal and administrative upkeep |

| Scale readiness | Strong for tightly scoped solo operations | Better fit for shares, funding, and broader growth |

If you stay with an eenmanszaak, tighten execution now: keep your KVK registration current, use clear liability language in contracts, maintain professional liability insurance, and keep invoices, contracts, and banking details aligned with your registered business data.

If you are moving toward a BV, prepare in sequence: confirm entity setup documents, verify KVK details are current, align contracts so the correct entity signs, and then re-run your tax and liability review before switching. Weak legal setup can lead to disputes, ownership issues, or failed deals.

For a deeper structure comparison, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

For a step-by-step walkthrough, see Opening a Bank Account in the Netherlands as a Foreigner.

Frequently Asked Questions

Should I stay with an eenmanszaak or move to a BV?

Stay with the sole trader route when your work is still straightforward and you can personally tolerate the risk that comes with business debts. Revisit a BV when the main issue is no longer setup speed but your own exposure, because KVK is clear that with an eenmanszaak you run a personal risk if the business incurs debts.

Next step: use the income, risk, and growth checks from the previous section, then pressure test your client contracts and insurance before you decide.

Can an expat register a Dutch sole proprietorship, and what should I check first?

Potentially, but do not treat business registration as proof that your residence or work position is fully cleared. KVK says only the owner can register, you need a DigiD, and the home address you submit must match the address where you are registered with the municipality in the BRP.

Next step: confirm your municipal registration details first, then complete the digital form step by step and check every address field before you submit.

Do I always need an in-person KVK appointment?

No. KVK says some registrations are completed digitally, and in those cases you do not need to make an appointment, but many registrations still require one. You can schedule an appointment up to 8 weeks in advance, and some locations may not have availability within a week, so last minute planning can create avoidable delay.

Next step: start the online registration early, then book the first suitable slot if your case is routed to an appointment.

How is tax handled after I register?

Registration does not mean every owner is automatically handled the same way for tax, but KVK does pass your details to the Netherlands Tax Administration after registration. If you are subject to VAT, the Tax Administration sends your turnover tax number and your VAT ID number within 2 weeks of registration. If nothing arrives after 2 weeks, KVK says you should contact the Tax Information Line.

Next step: wait for the Tax Administration response before assuming your VAT position is active, and if you need the operational details, read How to Obtain a 'VAT Number' as a Freelancer in the Netherlands.

How should I think about tax differences between a sole trader and a BV?

Start with your real numbers and your risk profile, not with internet claims about a universal switch point. This grounding pack does not support a fixed revenue or profit threshold, and it does not support assuming every entrepreneur qualifies for the same Dutch tax benefits.

Next step: model both structures using your last 12 months of income, costs, and drawings, then get current tax advice before you restructure around a headline number.

Can I use the 30% ruling as a freelancer?

Do not assume the 30% ruling applies the same way across every setup or that it automatically fits independent work. Eligibility, timing, and how the ruling interacts with your exact position need fresh verification before you build a structure decision around it.

Next step: treat this as a separate tax analysis and start with A Deep Dive into the Netherlands' 30% Ruling for Skilled Migrants.

What if my business address is different from my home address?

That is possible, but it creates a document check you should prepare for before filing. If your visiting address is different from your home address, KVK may ask for proof that you can use that address, such as a copy of the lease, purchase, rental, or service contract signed by both parties. Your home address in the filing must match your municipality record in the BRP.

Next step: gather the address evidence before registration and make sure the home address in your filing matches your municipality record exactly.

Can I have more than one eenmanszaak or use several activities and trade names?

You cannot have more than 1 eenmanszaak, but one registration can cover multiple activities and trade names. That flexibility is useful, but KVK warns that changing or adding activities can affect taxes, insurance, or permits, so this is not just an admin update.

Next step: update KVK before you start invoicing under a new activity or name, and recheck your insurance and permit position at the same time.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- aei.pitt.edu/34780/1/A27.pdftrusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- archive.org/stream/annualreportifudofhumanrights2019/Ann...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

A Deep Dive into the Netherlands' 30% Ruling for Skilled Migrants

Treat this as a managed compliance asset, not a payroll perk. Official pages now refer to the expat scheme, formerly the 30% ruling. The key operational change is that from 1 January 2025 you can no longer elect partial foreign tax liability in your return. Transition relief still runs through 2026 for some people who were already using the scheme before 2024. That makes your cohort, filing timing, and asset profile worth checking early.