Quick Answer

An IRS offer in compromise can settle eligible tax debt for less than the full amount owed, but only when your facts support it and you pass strict eligibility gates. This guide recommends a compliance-first workflow: pre-qualify, compare OIC vs installment agreement, align the correct legal pathway and forms, build an evidence-linked packet, and escalate early when complexity or process friction appears.

You can run the IRS OIC decision in one sitting if you use a compliance-first playbook#

Use a compliance-first checklist to make a clear go-or-no-go decision on an Offer in Compromise based on your facts.

If you work across borders as a freelancer or consultant, you need a clean go-or-no-go system that lowers stress and keeps execution under control. The goal is simple: decide the next move now, then do the full filing work only after your records can support that choice.

An Offer in Compromise (OIC) is one possible path for tax debt relief, but it is not automatic forgiveness or the default option for everyone. The IRS says you should review other payment routes first, and it evaluates each case based on your specific facts and circumstances. If you can fully pay through an installment agreement, an OIC usually is not your first move for back taxes.

| Decision stage | What you do now | Go signal | No-go signal |

|---|---|---|---|

| Pre-qualify | Run the Offer in Compromise Pre-Qualifier Tool and check your IRS Individual Online Account | Tool output supports moving forward | Eligibility gaps appear |

| Estimate fit | Map the facts and circumstances the IRS will review, including whether full payment is feasible through other options | Your review supports moving forward with an offer | A full payment path looks feasible |

| Build packet plan | List the records you will align before filing your offer in your IRS Online Account | You can produce consistent records | Key records conflict or remain missing |

| Escalate early | Define when you will call a qualified tax professional | Complexity triggers are clear | You keep guessing on legal or factual issues |

If your income is uneven, multi-country, or both, keep the decision clean: pre-qualify, estimate, document, escalate. Where rules depend on program details or personal facts, confirm directly with the IRS or a qualified tax professional whose credentials you verify first.

The core terms that make OIC decisions predictable#

Learn these core definitions first, and your Offer in Compromise decision becomes a clearer go-or-no-go call.

| Pathway | When it fits | Forms |

|---|---|---|

| Doubt as to Liability | A genuine legal dispute about the correct tax debt | Form 656-L |

| Doubt as to Collectibility | You cannot fully pay | Form 656 with Form 433-A (OIC) and/or Form 433-B (OIC) financial disclosures |

| Effective Tax Administration | Full collection is possible, but full payment would cause hardship or be unfair and inequitable because of exceptional circumstances | Form 656 with Form 433-A (OIC) and/or Form 433-B (OIC) financial disclosures |

You have the workflow. Now use the vocabulary the IRS actually uses so your decision is based on criteria, not hope.

An Offer in Compromise (OIC) is an agreement with the Internal Revenue Service (IRS) that can settle tax liabilities for less than the full amount owed when criteria are met. The IRS reviews your facts and, in most cases, expects the amount offered to meet or exceed your Reasonable Collection Potential (RCP). RCP is the IRS measure of ability to pay, based on assets and anticipated future income.

| Term | Working definition | Decision impact |

|---|---|---|

| Offer in Compromise (OIC) | A formal IRS settlement path for qualifying liabilities | Use when your facts do not support a standard full-payment route |

| Reasonable Collection Potential (RCP) | IRS lens on what it can collect from assets and income | If your offer is below this level, your case is generally weaker |

| Doubt as to Liability | A genuine legal dispute about the correct tax debt | Use a liability dispute path, not a collectibility story |

| Doubt as to Collectibility and Effective Tax Administration | Collectibility means you cannot fully pay. Effective tax administration means full collection is possible, but full payment would cause hardship or be unfair and inequitable because of exceptional circumstances | Pick one legal pathway before you prepare forms |

| Installment Agreement | Alternative payment route for back taxes | If you can fully pay through this route, you generally will not qualify for OIC |

Your form set must match your legal pathway. For Doubt as to Collectibility or Effective Tax Administration, submit Form 656 with Form 433-A (OIC) and/or Form 433-B (OIC) financial disclosures. For Doubt as to Liability, file Form 656-L instead of the Form 656 plus 433 package.

In practice, the sequence is predictable: estimate RCP, choose one legal pathway, and prepare the matching forms. If your facts conflict, escalate to a qualified tax professional.

Do you qualify for an IRS offer in compromise right now?#

Run a hard-gate check first, and move forward with an IRS offer in compromise only when every gate passes today.

Before you draft your Form 656-B package, run eligibility as a set of hard stops. This helps you avoid spending time on a packet the IRS may not process.

Topic No. 204 and the Offer in Compromise Pre-Qualifier Tool give you the structure. Start with filing compliance. You must file all required returns and make required estimated payments.

Next, confirm you have no open bankruptcy, because the IRS will not consider an offer while bankruptcy stays open. If you have employees, confirm you made federal tax deposits for the current quarter and the prior two quarters before you move toward an offer package.

| Gate | What to verify now | Stop signal | Immediate action |

|---|---|---|---|

| Filing compliance | Required personal and business returns are filed, and required estimated payments are current | Missing or late filings, or missed estimates | Pause OIC, bring filings and payments current, then recheck |

| Bankruptcy status | No open bankruptcy case | Any open bankruptcy case | Wait until discharge and closure, then reassess |

| Employer deposits | Current quarter and prior two quarters of federal tax deposits are complete | Any deposit gap | Fix deposits first, then restart eligibility review |

| Pre-Qualifier output | IRS.gov/OICtool results support screening eligibility | Tool flags ineligibility or uncertainty | Treat as no-go for now, remediate gaps, rerun |

A common blocker is filing compliance. If required returns are missing or estimated payments are not current, pause the packet work and fix that first.

Use this checklist before you pursue this path:

- Save your OIC tool results as working notes for advisor review.

- Record each gate as pass or fail with a date and owner.

- If any gate fails, pause Form 656 prep and remediate first.

- If all gates pass, move to documentation with a qualified tax professional.

This is the practical way to avoid a non-processable submission. Run the gates, fix what fails, then come back with a file the IRS can actually work.

Should you pursue OIC or choose an installment agreement instead?#

Choose the path that matches your real ability to fully pay, because if you can fully pay through an Installment Agreement, the IRS usually will not accept an offer in compromise.

If you pass the gates, the next move is strategy. You are not picking the "best" program. You are picking the path your numbers can support with the lowest execution risk.

| Decision criteria | Installment Agreement | Offer in Compromise (OIC) |

|---|---|---|

| Affordability test | Built for paying in full over time, including a short-term pay-in-full option up to 180 days | Built for settling tax debt for less than the full amount when criteria are met and full payment is not realistic |

| RCP fit | Usually the right path when you can fully pay | IRS expects the offer amount to be at least your Reasonable Collection Potential (RCP) |

| Upfront cost signal | Setup fee can be lower, such as $22 online with direct debit or $107 by phone, mail, or in person with direct debit | Form 656 Booklet package includes a $205 application fee unless you meet low-income certification |

| Documentation load | Varies by case and IRS requirements | Requires the Form 656 package and an IRS investigation process |

| Execution risk | While pending, IRS is generally prohibited from levying, and collection time can be suspended or prolonged | Submission does not ensure acceptance, and investigation can run up to 24 months |

Use RCP as your pivot. If your cash flow and assets support full payment over time, start with an Installment Agreement. If your records show you cannot fully pay and your offer logic aligns with RCP, the OIC path can make sense.

When evidence is incomplete, default to the safe path:

- Choose the lower-risk payment path first.

- Clean records and resolve missing inputs.

- Revisit OIC only after your file supports a coherent RCP story.

| Known now from Topic no. 204 and Form 656 Booklet | Unknown until IRS review |

|---|---|

| Full-pay ability usually blocks OIC, OIC is evaluative, and fees/process rules are defined | Final acceptance, exact review pace, and final terms for your case |

The four-step OIC operator framework for business-of-one workflows#

Run OIC as a four-step operator checklist with clear owners, because structure reduces non-processable filings and costly rework.

You have a strategy choice. Now run execution like an operator: set up the workflow, assign ownership, and define what "done" looks like at each step.

| Step | What you do | Owner | Checkpoint | Escalate when |

|---|---|---|---|---|

| 1. Pre-qualify hard gates | Use the Offer in Compromise Pre-Qualifier Tool and IRS Individual Online Account to check eligibility, then confirm filed returns, at least one billed tax debt, and required federal tax deposits if you have employees | You | Pass or fail log for each gate | Any gate fails, or tool output looks unclear |

| 2. Estimate collectibility | Build your Reasonable Collection Potential (RCP) view from income and asset capacity, then map your pathway as Doubt as to Collectibility or Effective Tax Administration | You plus tax professional if needed | One clear pathway statement with supporting notes | You cannot defend pathway choice with records |

| 3. Assemble forms and evidence | Prepare Form 656 with Form 433-A (OIC) and/or Form 433-B (OIC), then align each figure to supporting documents | You | Document checklist marked complete and internally consistent | Numbers conflict across forms, or records stay incomplete |

| 4. Submit, monitor, and escalate | File through IRS channels, track every notice, and manage deadlines as a case file | You | Status log with next action and owner | You cannot resolve an issue directly with IRS channels |

Two rules keep this safe. Pre-qualification never guarantees acceptance, so treat tool output as screening, not approval. Also, a returned offer is not the same as a rejected offer. A rejection can carry an appeal window, while a returned offer generally does not.

Use these operating defaults for back taxes and any IRS settlement decision:

- Keep one working file with forms, notes, and status history.

- Assign one owner per step, even if that owner is you.

- Escalate to Taxpayer Advocate Service (TAS) when you cannot resolve the problem directly.

- If you qualify for low-cost representation, use Low Income Taxpayer Clinics (LITCs).

Build an audit-ready application packet before you submit#

Build your OIC packet as a claim-to-evidence file, because consistency helps keep your submission processable and defensible.

Treat the packet as a set of claims that each must tie to evidence. Use Form 656-B as your spine, then link every statement in your offer to a document before you submit.

| Packet component | Required now | Conditional evidence | Control check |

|---|---|---|---|

| Form 656-B workflow | Use the current booklet instructions and required forms list | Add only pathway-specific items that apply to your case | Your checklist shows complete or not applicable for every line |

| Form 656 claims | Enter only claims you can support | Add clarifying records when facts look unusual | Each claim points to a document in your file |

| Form 433-A (OIC) and Form 433-B (OIC), if applicable | Provide full financial disclosures that match your profile | Include business records when business activity drives the numbers | Totals and narratives match Form 656 without contradictions |

| Supporting attachments | Attach copies of required records, not originals | Add extra documentation when a claim needs context | Every attachment has a clear purpose tied to a form field |

| Fee and payment status | Include the standard application fee and required payment items, or document low-income certification status when it applies | Add follow-up proof if your status changes | Your packet shows one complete fee path, not mixed signals |

Before you file, run a Taxpayer Bill of Rights quality pass. Ask direct questions:

- Can you explain what you filed and what the IRS will review, in plain language?

- Can you show how each number supports what you reported?

- Can you challenge a mismatch quickly with additional documentation?

- Can a tax professional follow your file without asking for missing basics?

Finish inside your IRS Individual Online Account workflow where supported. Recheck eligibility, confirm payment status, and file only after your checklist shows complete evidence links. Catching one inconsistency before submission can prevent avoidable delays.

How do globally mobile freelancers avoid cross-border mistakes during OIC prep?#

Separate debt resolution from reporting compliance, then tie both tracks to the same records so your OIC stays accurate.

A consistent packet can still fail if your cross-border reporting is out of sync. An Offer in Compromise (OIC) deals with IRS debt resolution and potential tax debt relief. It does not cancel parallel filing duties tied to foreign accounts and assets.

| Track | What it decides | Core forms | Filing channel and timing |

|---|---|---|---|

| IRS settlement track | Whether your OIC resolves eligible back taxes | OIC application and supporting financial disclosures | IRS process for OIC review |

| Cross-border reporting track | Whether foreign account or asset reports are required | FBAR (FinCEN Form 114) and Form 8938 | FBAR is filed electronically through FinCEN, not with a federal return. Form 8938 is attached to your annual return and follows that return due date, including extensions. |

Run separate checklists with shared evidence#

Use a strict do-not-mix-assumptions rule. Keep one checklist for OIC strategy and another for cross-border reporting decisions, then connect both to one document vault.

| Item | What it covers | Key details |

|---|---|---|

| OIC checklist | OIC strategy | Claims in your OIC application, financial disclosures, and consistency checks for your IRS settlement narrative |

| Cross-border checklist | Cross-border reporting decisions | Decide if Form 8938, FBAR, or both apply, including whether aggregate foreign account value crosses the FBAR $10,000 trigger |

| Shared evidence | Both tracks | Account statements, income records, and ownership documents used by both tracks |

Keep Schedule SE and disclosures in sync#

For globally mobile freelancers, Schedule SE is your anchor because it computes self-employment tax from net earnings. Run a monthly close routine. Update income by source, reconcile net earnings for Schedule SE, and verify those same earnings match the cash flow and ability-to-pay story in your OIC disclosures.

If your work location or account mix changed midyear, log the change immediately. Then re-run both checklists before filing.

A simple example: a digital nomad moves countries, opens a new foreign account, and keeps billing the same clients. The fix is not new assumptions. It is updated records, then separate validation for OIC, FBAR, and Form 8938 decisions using the same source file and a licensed tax professional. For broader mobility controls, use The Ultimate Digital Nomad Tax Survival Guide for 2025.

Submit, monitor, and escalate without losing control#

Choose your filing channel, then run a deadline-driven case system so your OIC stays on track even when IRS timelines move slowly.

| Path | Use when | Action |

|---|---|---|

| Appeals hearing | You receive a rejection | Request an Appeals hearing in writing within 30 days |

| Taxpayer Advocate Service (TAS) | Case friction creates hardship or a communication breakdown | Contact TAS to see whether you qualify for assistance |

| Low Income Taxpayer Clinics (LITCs) | You need representation and qualify | LITCs can represent taxpayers in audits, appeals, collection disputes, and court |

Treat your OIC like an operations project. Choose your submission path up front, then manage it like a case file.

Submit through IRS Individual Online Account when you want one place to check eligibility, make payments, and manage online workflow. Use the paper path in the Form 656-B (Offer in Compromise Booklet) when your process depends on mailed records and physical packet controls.

| Control point | What to do | Why it matters |

|---|---|---|

| Submission channel | Pick online account or Form 656-B paper workflow before filing day | Prevents last-minute channel switching errors |

| Case log | Record every IRS letter, request, and your response date | Keeps your IRS settlement process auditable |

| Evidence versions | Tag each document update to the matching Form 656 data point | Stops contradictions across revisions |

| Timeline posture | Plan for a potentially long review period, including investigations that can take up to 24 months | Reduces panic and bad reactive decisions |

| Payment handling | Assume initial payment generally applies to outstanding liability | Keeps cash planning realistic for back taxes |

Build your monitoring rhythm#

Assign one owner, one backup, and one weekly review block. Log inbound IRS notices the day they arrive, set due dates immediately, and draft responses before you chase final documents.

If the IRS can process your file, expect written status communication and possible follow-up requests. If the IRS cannot process it, expect your package back with an explanation. Correct it, then resubmit with a clean change log.

Escalate by trigger and keep a next move ready#

Escalate based on triggers, not stress. If you receive a rejection, request an Appeals hearing in writing within 30 days to preserve that path. If case friction creates hardship or a communication breakdown, contact Taxpayer Advocate Service (TAS) to see whether you qualify for assistance.

If you need representation and qualify, use Low Income Taxpayer Clinics (LITCs), which can represent taxpayers in audits, appeals, collection disputes, and court.

If the IRS accepts your offer, move immediately into a five-year compliance checklist to protect your tax debt relief outcome. If the IRS does not accept it, review other IRS resolution options and keep your next action under your control.

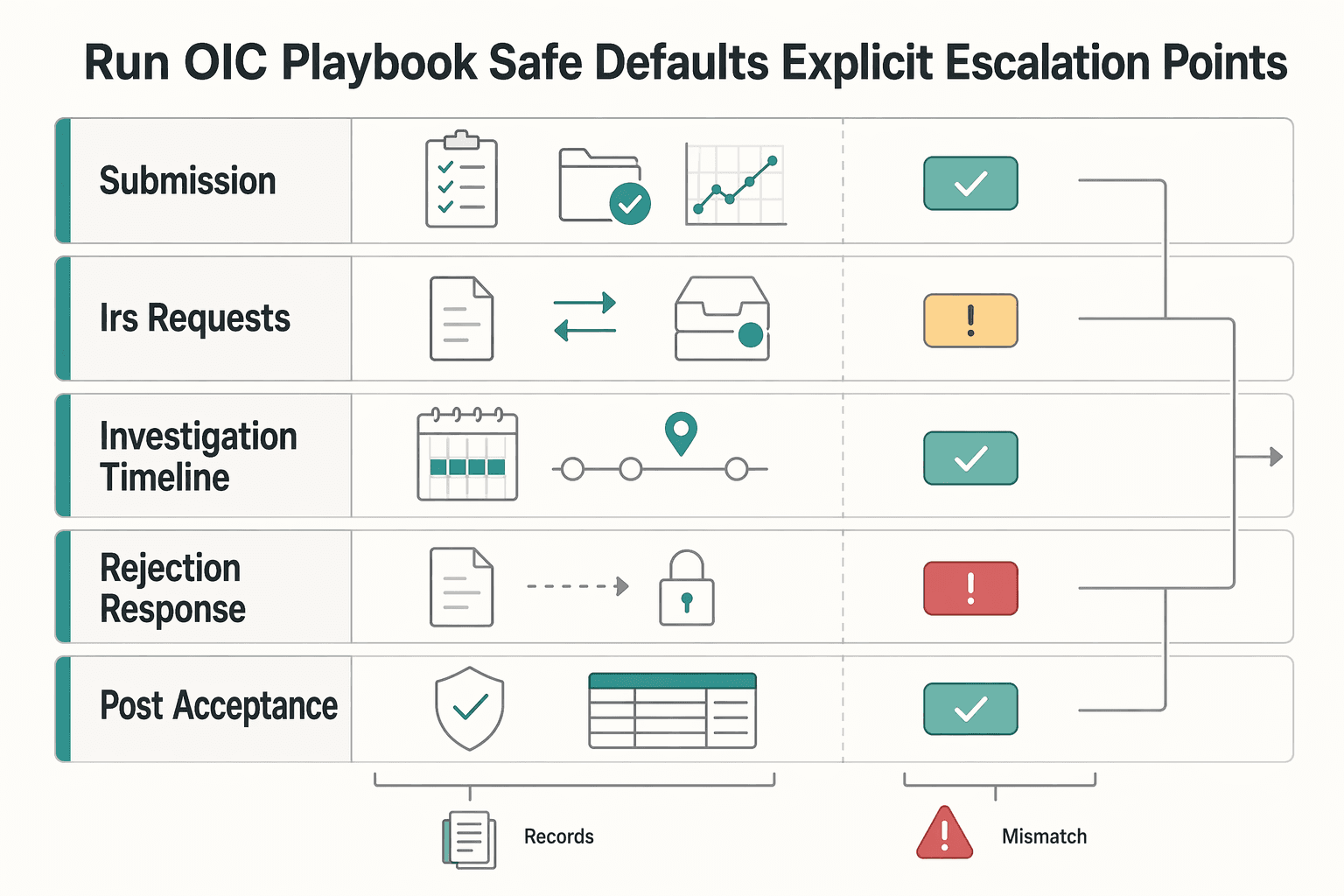

Run the OIC playbook with safe defaults and explicit escalation points#

Run OIC as a controlled system: gate decisions, track evidence, and escalate on triggers instead of stress.

At this point you have enough to act. Stay in execution mode. Move only when your checklist, Form 656 data, and supporting records match, and let official IRS communication drive timing.

| Decision point | Safe default | Escalate when |

|---|---|---|

| Submission | Use IRS Individual Online Account for eligibility checks, payments, and online filing, and keep one documented submission path end to end | Your channel creates missing records, duplicate steps, or deadline risk |

| IRS requests | Log every notice, owner, due date, and evidence version in one case file | IRS requests additional information and your current file cannot answer quickly |

| Investigation timeline | Plan for a long review window that can run up to 24 months | Delays create hardship, confusion, or unresolved rights questions |

| Rejection response | Prepare appeal materials in advance so you can act fast | You receive a rejection letter and need to submit a written appeal within 30 days |

| Post-acceptance compliance | Run a five-year compliance calendar for returns, payments, and documentation | You see a risk of missed filing or payment obligations |

Use this closeout checklist before you file for tax debt relief or choose an alternative for back taxes. Keep it in your working file and mark it off as you go.

- Confirm one submission path and one source of truth for case status.

- Validate every open assumption with written IRS guidance or a qualified tax professional.

- Respond to IRS information requests by deadline, because missing a request can cause the IRS to return your offer without appeal rights during processing.

- If process friction blocks progress, contact Taxpayer Advocate Service (TAS). TAS support is free for qualifying taxpayers.

- If you need representation, check Low Income Taxpayer Clinics (LITCs), which can represent eligible taxpayers in audits, appeals, collection disputes, and court.

If you travel and work across borders, do not improvise. Keep the case log current. Submit the exact document version tied to the Form 656 line item. Confirm the response with your tax professional and hit the deadline.

This playbook reduces rework and forces clear decisions. Run the gates, build an evidence-linked packet, and escalate on triggers. Then apply the same operator discipline to your broader mobility workflow with The Ultimate Digital Nomad Tax Survival Guide for 2025.

Frequently Asked Questions

What is an IRS Offer in Compromise?

An IRS offer in compromise is an agreement between you and the Internal Revenue Service (IRS) that may settle eligible tax debt for less than the full amount owed. Treat it as a structured IRS settlement path, not as automatic debt forgiveness.

Who qualifies for an OIC?

Run the hard gates first. You must file required returns, make required estimated payments, and not be in an open bankruptcy proceeding. If you run a business with employees, make current and prior two quarters of required tax deposits before you apply for an offer in compromise.

How does the IRS use Reasonable Collection Potential in an OIC decision?

The IRS uses Reasonable Collection Potential (RCP) to measure ability to pay. It reviews assets, income, and overall collection potential when it evaluates an offer. If your numbers show full payment capacity, the IRS usually expects full payment through other paths.

What are Doubt as to Liability, Doubt as to Collectibility, and Effective Tax Administration?

Doubt as to Liability means you have a genuine dispute about whether the tax debt exists or about the correct amount. Doubt as to Collectibility means your assets and income cannot fully cover the liability. Effective Tax Administration applies when the tax is legally owed and collectible, but collecting in full would create hardship or an unfair outcome under exceptional facts. Choose the basis that matches your facts and build your packet around it.

Is the Offer in Compromise Pre-Qualifier Tool a guarantee of acceptance?

No. The Offer in Compromise Pre-Qualifier Tool is a preliminary eligibility check, not an approval. Use it to decide stop or go before you invest in a full packet. Keep expectations realistic because investigation timelines can run long and may take up to 24 months in some cases.

Can you apply for OIC if you are in bankruptcy?

No, not while bankruptcy stays open. Wait until the case closes or the court discharges it, then reassess eligibility. Submitting early wastes time on your back taxes plan.

Should you try an installment agreement before applying for OIC?

In many cases, yes. If you can fully pay through an installment agreement or other means, you generally will not qualify for OIC. Compare both paths with your numbers, then let a qualified tax professional stress test your assumptions before you file.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Best Digital Nomad Cities for Entrepreneurs and Startups

Choosing a nomad base for your company is an execution decision first. Lifestyle matters, but it belongs in the second round. The costly mistakes usually show up after the city-ranking stage, when a place that looks great online turns into a slow or expensive setup once you start invoicing, signing contracts, and working against real deadlines.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.