Quick Answer

Submit the correct form before money moves and confirm payer acceptance in writing. For tax withholding on grant income for foreigners, use Form W-8BEN when the amount is non-service fellowship or grant support, and use Form 8233 when payment is tied to teaching, research, or other required services. After payment, check reported withholding against your records and move to recipient-side reclaim filing if the payer does not correct the issue.

You secured the grant. That validates your expertise. But getting the money into your account without losing too much to avoidable withholding is a separate job. For many global professionals, a meaningful share of funding disappears because the payment was classified incorrectly, the treaty claim was not set up in time, or the payer defaulted to automatic withholding.

Treat this as a financial control issue, not a back-office nuisance. The mindset shift is simple: your grant is revenue, your withholding position needs to be set before money moves, and every payment needs to be checked against what was supposed to happen.

This playbook breaks the work into three phases: set the withholding position before payment, verify what actually happened when funds arrive, and use the year-end filing process to correct what the payer did not fix. The goal is not just compliance. It is keeping control of your net award.

Phase 1: Pre-Payment Strategy (Assess & Act Before a Dollar Arrives)#

The most important move happens before the first disbursement. Once payment is released, you may be trying to recover withholding after the fact instead of preventing it.

For this phase, use these definitions consistently:

- A nonresident alien is someone who has not passed the green card test or the substantial presence test.

- The taxable portion of a scholarship or fellowship is the part that is not a qualified scholarship amount under IRC §117, for example, amounts not used for qualified tuition and related expenses.

- A treaty benefit is a possible reduced U.S. tax rate or exemption for a specific income item when your treaty covers that item and your documentation is accepted.

Set your withholding baseline#

Start with the default path, then confirm whether you qualify for a reduced one before the first disbursement.

| Withholding path | When it applies | What to confirm with the payer before first disbursement |

|---|---|---|

| Default withholding path | U.S.-source income not effectively connected with a U.S. trade or business is usually withheld at 30% unless an exception applies | How they characterized the payment, which rate they will apply, and which documents they require before scheduling payment |

| Scholarship/fellowship listed-rate path | Taxable part of a U.S. scholarship/fellowship paid to nonresident aliens is listed at 14% for F/J/M/Q visa holders, and 30% for other nonresident aliens | That they are treating the payment as scholarship/fellowship, not compensation for services, and which listed rate they plan to use if no treaty reduction is accepted |

| Possible reduced-rate treaty path | A treaty may reduce or exempt withholding if the treaty covers your income and required claim documentation is valid | Which form they require, whether they accept your treaty position, whether a U.S. or foreign TIN is needed for your claim (subject to exceptions), and the intake cutoff before payment release |

If any part of the award is compensation for services performed in the United States, treat that part separately. It is subject to graduated withholding rules and may require different claim documentation, such as Form 8233 for personal-services income.

Pressure-test treaty eligibility before you claim it#

Do not submit a treaty claim on instinct. Run a simple pass-fail check first:

| Check | What must be true | If it fails |

|---|---|---|

| Residency claim consistency | Your treaty-residency position matches your supportable facts and records | Fix it before disbursement |

| Income characterization fit | The payment type matches the treaty income category you are claiming | Fix it before disbursement |

| Treaty article match | The specific treaty article fits your facts; do not assume one article works across countries | Fix it before disbursement |

| Payer documentation readiness | You can provide the form and supporting information the payer needs to apply the rate | Fix it before disbursement |

If one item fails, fix it before disbursement. If the payer determines your claim is invalid, they must not apply the treaty rate.

Build and submit the W-8BEN packet#

For income that is not earned from personal services, the practical control point is a complete Form W-8BEN packet delivered to the payer before payment is processed. Give it to the withholding agent or payer, not the IRS.

Use this pre-payment packet checklist:

- Signed Form W-8BEN with core identity, residence, TIN as applicable, and treaty-claim fields completed accurately

- Brief submission note identifying payment type, treaty country, and treaty article position (if relevant to payer review)

- Supporting records you can produce quickly if requested, for example, award documentation, status or residency evidence, and tax ID evidence

- Internal receipt or tracking note showing who received the packet and whether it was accepted into payment processing

For timing, submit before first disbursement. Track form validity too. W-8BEN is generally valid through the end of the third succeeding calendar year unless circumstances change earlier.

If payer guidance conflicts with your treaty position or requested form type, escalate to the withholding or international tax team before release and keep the written exchange for Phase 2 verification. You might also find this useful: Indonesia Tax for Foreigners With a Defensible Filing Path.

Phase 2: Payment Verification (Verify & Document with Precision)#

Do not treat payment as finished once the funds hit your account. Verification here is a three-way reconciliation. Match the payer statement, your bank receipt, and Form 1042-S, then classify each mismatch first as either a data-entry error, a classification error, or a treaty-application error.

Use those labels on purpose:

- Data-entry error: invalid code or rate, blank required field, or values that do not reconcile.

- Classification error: the payment was reported under the wrong income type, which can change withholding treatment.

- Treaty-application error: your reduced-rate claim was not applied, often because required documentation or TIN details were incomplete.

Review the tax form against what actually happened#

Do not assume the 1042-S proves the payer got things right. Start with the payer statement and your bank receipt, then test the form against both. Confirm that gross amount, withholding, and net receipt reconcile to what was actually paid.

Form 1042-S amounts are reported in whole dollars, so check that gross income, withholding, and any repayment fields reconcile at the whole-dollar level. If they do not, flag it for correction. Use this validation table so you do not rely on an old field map:

| What you verify | What should match | What to note now |

|---|---|---|

| Gross income reported | Payer statement or award notice, including any split treatment | Record the current box reference after checking the current Form 1042-S instructions |

| Tax withheld and stated rate | Payer records and your net bank receipt | If withholding is below 30%, confirm the current-year chapter 3 exemption code field is completed, then record the current box and code references after verification |

| Income type and treaty reporting | Actual payment type and accepted claim documents | Record the current income code, exemption code, and recipient or TIN field references after checking the current-year instructions |

Validate coding before you assume the treaty failed#

Check classification first. If any portion of the award is compensation for services performed in the United States, that portion follows compensation withholding rules rather than scholarship or fellowship treatment. For independent personal services, amounts can still be reportable on Form 1042-S even when fully treaty-exempt.

Then check treaty mechanics. If a reduced rate was not applied, verify what documentation the payer had on file, including Form W-8BEN, W-8BEN-E, or Form 8233, and whether required TIN details were complete. Missing or incomplete documentation can trigger default 30% withholding, and an undocumented recipient can be treated at the maximum applicable rate.

Escalate discrepancies in the right order#

Start with the payer or withholding agent, because that party is responsible for withholding and reporting. Contact the named withholding, tax, international, or 1042-S contact and send one evidence packet:

- Submitted treaty/withholding documentation, such as Form W-8BEN, W-8BEN-E, or Form 8233, and any acceptance confirmation

- Award letter or payment notice

- Bank proof of receipt

- Form 1042-S with disputed fields marked

- TIN evidence and your short treaty-article note, if relevant

Request a written response covering:

- How they classified the payment

- Which withholding rate they applied

- Whether they will file a corrected Form 1042-S

- Expected correction timeline

If they confirm an error, ask them to confirm correction through their filing process, including IRIS where applicable. If you still have not received your recipient copy near filing season deadlines, ask whether they requested the one-time 30-day furnishing extension on Form 15397.

If payer-side correction is not resolved in time, move to recipient-side reconciliation on Form 1040-NR to claim a refund of overwithheld tax or pay underwithheld tax.

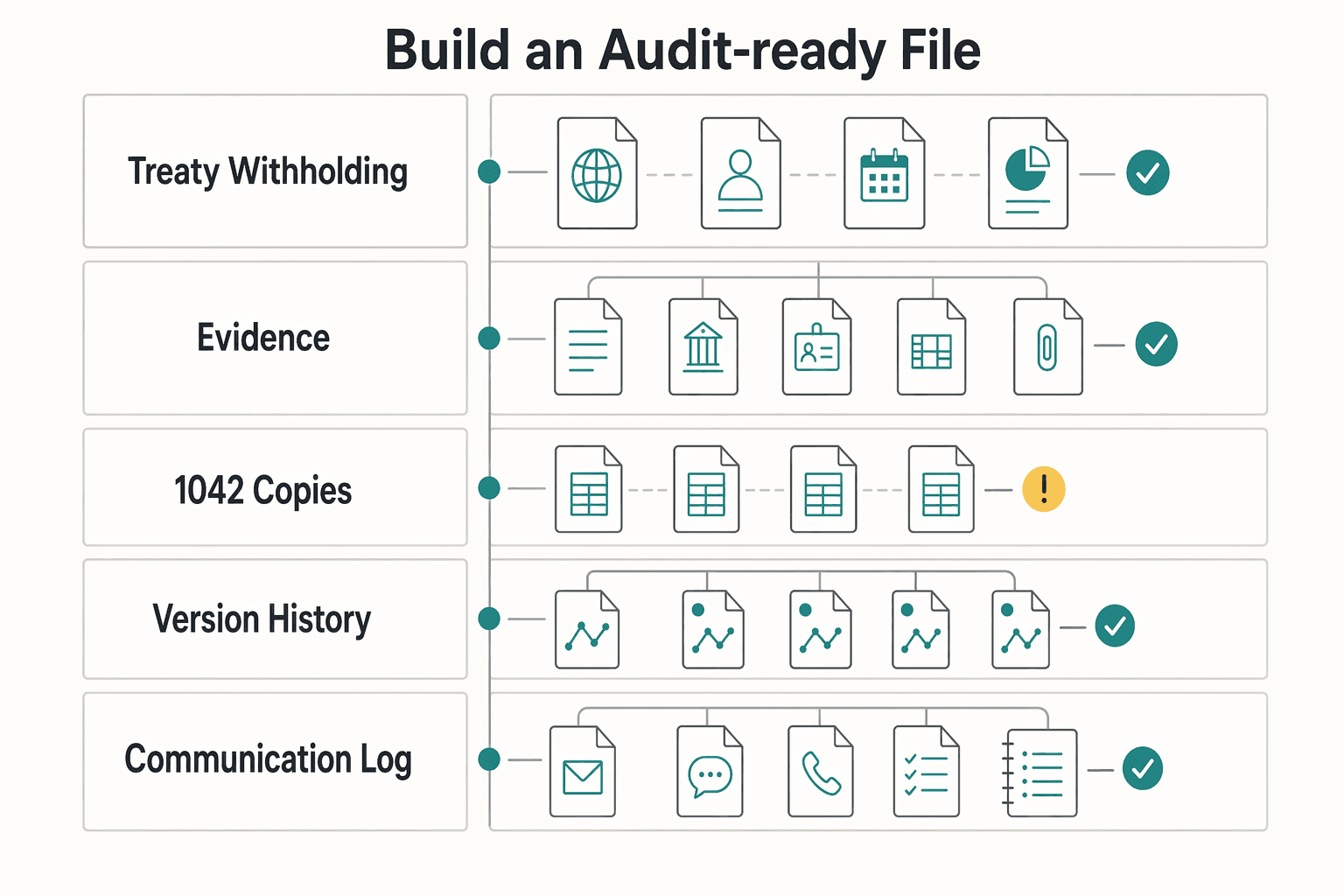

Build an audit-ready file#

A clean file saves time twice: once when you escalate to the payer, and again if you need to file for a refund. Build one compliance folder per award and keep it updateable. Use a consistent filename pattern such as YYYYMMDD_Payer_DocType_v01.pdf, and increment the version only when a document changes.

| File item | What to keep |

|---|---|

| Treaty/withholding form | Final signed form such as W-8BEN, W-8BEN-E, or Form 8233, plus any rejected draft versions |

| Award records | Award documents and payment schedule |

| Payment evidence | Payer statements or remittance records and bank proof |

| 1042-S copies | Original Form 1042-S and any corrected Form 1042-S |

| Version history | One-page version history showing what changed and when |

| Communication log | Date, contact, role, summary, and promised next step |

This becomes your support pack for refund claims and for cleaner repeat execution in future filing cycles. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Before you finalize your compliance file, use the W-8 form generator to review form fields before sharing documents with the payer.

Phase 3: Post-Year Reconciliation (Reclaim & Optimize)#

Once payer correction is no longer dependable, stop waiting and move to the return. If your Form 1042-S withholding does not match your documented treaty position, the issue is no longer just a payer correction problem. It is now a formal refund workflow on Form 1040-NR.

Payer-side overwithholding adjustments can be time-limited, so use a clear trigger. Stay in payer-correction mode only while you have a written correction path and timeline. Switch to return filing when that path is no longer reliable.

Know when the handoff happens#

Move to Form 1040-NR filing when one or more of these are true:

| Trigger | Action |

|---|---|

| Your Form 1042-S withholding conflicts with your documented treaty position | Move to Form 1040-NR filing |

| The payer will not confirm a corrected Form 1042-S with a clear date | Move to Form 1040-NR filing |

| The payment classification is still disputed as filing season approaches | Move to Form 1040-NR filing |

| You received Form 1042-S by the March 15 benchmark and it is still incorrect | Move to Form 1040-NR filing |

For nonresidents, claiming a refund of overwithheld U.S. tax is handled through Form 1040-NR.

Build the return package the way the IRS will read it#

Build the return around the documents that prove what was paid, what was withheld, and how the income should be treated. The highest-risk issue is still classification, so check that before you file.

| What to prepare | What to verify before filing | Why it matters |

|---|---|---|

| Form 1040-NR | Use the current-year form and confirm your filing window. Calendar-year filers generally use April 15 if they had wages subject to withholding, or June 15 if they did not. If needed, request an automatic six-month extension with Form 4868. | This is the formal refund claim. |

| Form 1042-S | Attach Form(s) 1042-S to the front of the return and recheck gross income and withholding against your final payer records. | It is the core third-party withholding evidence. |

| Withholding entry on Form 1040-NR | Enter chapter 3 or 4 withholding from Form 1042-S on line 25g after confirming current instructions. | This is the instructed withholding line for 1042-S amounts. |

| Schedule OI | Complete applicable items and include Schedule OI with Form 1040-NR. | It is a required companion schedule in this filing path. |

| Income classification | Confirm whether the amount is not effectively connected FDAP income, typically Schedule NEC, or compensation for services. | Misclassification can invalidate the reconciliation approach. |

| Support file | Keep your Form 1042-S copies, award letter, payer correspondence, and your classification and treaty notes together. | You need a clean evidence file if the claim is questioned. |

Classification is the highest-risk check. If any part of the award was tied to required teaching, research, or other services, that part is compensation and should not be handled as purely noncompensatory scholarship or fellowship income.

Escalate early when facts are mixed#

Bring in a tax professional when any of these apply:

- the payer will not issue a corrected Form 1042-S and the mismatch is material

- you are uncertain whether treaty benefits apply to this payment type

- the award includes both grant amounts and required services

- payer treatment and your documentation conflict on compensation versus noncompensatory treatment

- Form 8233 may be relevant based on service-related facts or treaty-claim constraints

If classification or treaty treatment is unclear, resolve that first, then file.

Close the loop for next year#

Do not waste a messy year by repeating it. After filing, document the root cause in one line, for example, incomplete documentation, payer coding error, or unresolved service classification. Then update your pre-payment packet and keep a repeatable reconciliation checklist so the next grant cycle starts with tighter controls.

That only works if you classified the payment correctly in the first place, which is why the support-versus-services split deserves its own check.

For broader tax-planning context, see A Guide to the 'Net Investment Income Tax' (NIIT) for High-Earning Freelancers.

A Critical Distinction: Is Your Grant Actually Payment for Services?#

This is where many withholding problems start. Before you file anything, classify the payment correctly. Support amounts and service-compensation amounts usually follow different treaty form paths, and mixing them can break your claim.

A scholarship is an amount paid to aid studies. A fellowship grant is an amount paid to aid an individual's study or research. Personal services compensation is payment for past, present, or future employment services. Primary purpose means who the work mainly benefits. If the study or research is primarily for the grantor's benefit, or performed under the grantor's direction or supervision, that portion is not pure scholarship or fellowship support.

| Payment purpose | Required duties | Who benefits primarily | Likely treatment | Treaty form path |

|---|---|---|---|---|

| Supports your study or research | No significant required duties | You, as educational or research support | Scholarship or fellowship support | Usually Form W-8BEN for non-personal-services income |

| Paid in exchange for teaching, research assistance, deliverables, or other required work | Yes | Grantor or employer receiving services | Personal services compensation | Form 8233 for personal-services income |

| Mixed award, part support and part required services | Yes, for part of award | Split by component | Hybrid | Split and document each component by withholding agent and income type before filing |

For hybrid awards, use a split-and-document approach. Allocate amounts by purpose, keep the award letter and duty language, and ask the payer to confirm in writing which amount is noncompensatory support versus service compensation before you submit forms.

In a same-withholding-agent case, Form 8233 can sometimes include both treaty-exempt compensation and treaty-exempt scholarship or fellowship amounts. That only works when you are also claiming a compensation-for-services treaty exemption with that same agent. Also remember that Form 8233 filings are segmented by withholding agent and by income type.

If your contract says "fellowship" but payer coding or expected reporting treats it as wages, stop and reconcile that first. Request the payer's written withholding analysis, the compensation-versus-support breakdown, the required-duty basis, and which reporting form they will issue. If you are using Form W-8BEN for a treaty exemption, confirm it includes your payee TIN.

Escalate to a qualified tax professional if treaty wording is unclear, facts are mixed across support and services, payer treatment conflicts with your documents, or the payer says treaty eligibility fails. Form 8233 requires correct treaty-term interpretation.

For a step-by-step walkthrough, see Japan Tax for Foreigners Who Work Across Borders.

You Are the CEO of Your Award#

If you want the net award you expected, treat withholding as an operating task with three checkpoints: before payment, during payment, and after year end. That is what being the CEO of your award means in practice.

Do not assume the withholding agent will infer your facts or apply treaty treatment without your input. If you are a nonresident alien, taxable noncompensatory scholarship, fellowship, or grant amounts are generally subject to withholding, typically 30%, with potential reduction to 14% (or a lower treaty rate) for eligible students, researchers, or grantees. To claim treaty relief, notify the payer of your foreign status and submit the correct form. Use Form W-8BEN for non-personal-services income and Form 8233 for personal-services compensation.

- Phase 1: Pre-payment setup.

Pass if income classification is clear, the correct form is submitted, and the payer confirms the withholding treatment you expect. Fail if the form path does not match the income type, service-compensation amounts are treated inconsistently with your expectations, or treaty eligibility is flagged as doubtful.

- Phase 2: Payment-period verification.

Pass if actual withholding on early payments matches the expected treatment. Fail if you see default withholding, graduated withholding on service-compensation amounts, or unexplained treatment changes.

- Phase 3: Post-year reconciliation.

Pass if Form 1042-S matches your records for reportable income and tax withheld. Fail if Form 1042-S conflicts with what was paid or claimed. If too much was withheld, file an income tax return to claim a refund.

| Stage | Passive recipient behavior | Likely outcome | CEO immediate next action |

|---|---|---|---|

| Before payment | Waits for payer direction | Wrong form path or default withholding risk | Confirm classification, submit Form W-8BEN or Form 8233, get written confirmation |

| During payment | Checks only after funds are short | Errors can continue across payments | Verify first remittance against expected withholding and document discrepancies |

| After year end | Accepts reporting as-is | Mismatched reporting or missed refund recovery | Reconcile Form 1042-S to your file and correct or reclaim as needed |

If form classification, treaty eligibility, or reporting treatment is unclear, pause and get qualified tax review before proceeding. If treaty applicability is in doubt, check the actual treaty provisions before relying on a reduced rate. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

If your process includes treaty claims, withholding corrections, and ongoing cross-border payment operations, contact Gruv to confirm fit and coverage for your workflow.

Frequently Asked Questions

What is the standard tax withholding on a US grant for a foreigner?

It depends on what part of the payment is taxable and how the payer classifies it. Start by separating qualified education expenses, such as required tuition, fees, and related enrollment costs, from amounts used for room, board, travel, or other personal costs, which are taxable. The default path is often 30%. The taxable part of a scholarship or fellowship can be listed at 14% for F/J/M/Q visa holders and 30% for other nonresident aliens, unless a valid treaty claim changes the result. Before you rely on any rate, confirm the payer’s treatment and later check it against Form 1042-S.

How can I reduce the tax withholding on my US grant?

The main lever is timing. Act before payment by confirming whether the award is non-service grant or fellowship income or compensation for services. If it is non-personal-services income and you are claiming treaty treatment, notify the payer of your foreign status and submit Form W-8BEN before payment. If it is payment for teaching, research, or other required services, use Form 8233 instead. Then confirm the payer’s expected withholding and reporting path, verify any listed-rate treatment that may apply, and reconcile the result on Form 1042-S.

Which form do I use to claim tax treaty benefits on grant income?

Use Form W-8BEN when the income is not earned from personal services. Use Form 8233 when payment is for teaching, research, or other services, because that is compensation treatment. The decision point is simple. If services are required as a condition of payment, use Form 8233 and give it to the withholding agent before payment, then verify that Form 1042-S matches that treatment.

Is a W-8BEN required for all foreign grant recipients?

No. Use Form W-8BEN when the payer requests it for non-personal-services income, whether or not you are claiming a reduced rate or exemption. For personal-services compensation, use Form 8233 instead. Submit the right form before payment processing, make sure required fields are properly completed, including TIN when required, and confirm expected withholding with the payer. Then check Form 1042-S at year end and escalate quickly if reporting does not match what was confirmed.

What if I receive a Form 1042-S with the wrong amount of tax withheld?

Treat it as a fixable error, not a final outcome. First reconcile the form to your records and treaty position, then ask the payer to review or correct the reporting if it does not match the expected treatment. If tax appears overwithheld or underwithheld on Form 1042-S, file Form 1040-NR to claim a refund or pay underwithheld tax, and attach a copy of Form 1042-S to support the claim.

Where can I find official IRS guidance on this topic?

Start with Publication 519 before you make filing decisions so you can confirm status and filing context. Before payment, use IRS guidance on claiming treaty benefits and withholding on specific income to choose between W-8BEN and Form 8233. Use Publication 901 and treaty tables as quick reference, then check the full treaty text before you cite an article to the payer. At year end, use the Form 1042-S instructions and the Form 1042-S guide while you reconcile income, withholding, and reporting codes.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Form 1042-S for Foreign Persons With U.S.-Source Income

A Form 1042-S is usually a compliance record, not a crisis. It shows that your payer, as the withholding agent, reported certain U.S.-source amounts paid to you as a foreign person, how that income was categorized, and any withholding.