Quick Answer

Start with a Year of Assessment day ledger, then test your facts under Section 7 of the Income Tax Act 1967 before optimizing anything else. For malaysia tax residency, the common 182-day baseline is useful but not complete, so close counts and non-baseline pathways should stay provisional until you verify current HASiL guidance. If the outcome changes reliefs, rebates, or treaty treatment, strengthen documentation and seek review before filing.

Malaysia tax residency: classify your status before optimizing#

Malaysia tax outcomes can diverge quickly for mobile freelancers, so classify your status early and document it as you go.

This guide does three things: it helps you make a first-pass residency classification, shows you how to keep records you can defend, and flags the point where a DIY answer stops being reliable. Common pitfalls include loose day counting, assuming visa or immigration status settles tax status, and trying to rebuild travel history when it is time to file.

Your official starting point is HASiL. Its residence-status page points to Section 7 ITA 1967 for individual residence status and places Certificate of Residence in the same resource path. A practical order is to apply the status test first, then support your position with documents.

A useful working rule from the guidance here is that status is based on physical presence, not nationality or citizenship. A secondary explainer also states a baseline resident test at 182 days in a calendar year. If your facts are close to a threshold or depend on linked periods, treat summaries as directional and verify them against current HASiL materials.

Classification matters because the tax treatment can change materially. The same secondary source describes resident treatment as progressive rates with relief access, while non-resident treatment is a 30% flat rate with no reliefs or rebates.

Use one practical default now: keep a day log tied to primary travel records. This article is a practical explainer grounded in Malaysia residence-status materials, including the HASiL page timestamp shown as 20 / 11 / 2025 11: 05: 31 when reviewed. It is not personal legal or tax advice.

Related reading: Tax Residency in Croatia: A Guide for Nomads on the Adriatic.

Define the terms before you make decisions#

Start with the legal frame: Malaysia tax residency is a status for a basis year and Year of Assessment (YA). It is not a lifestyle label or your personal sense of where you are "based."

| Source | Individual residency? | Note |

|---|---|---|

| Section 7 | Yes | Legal frame for Malaysia tax residency; a single day-count baseline is not the whole law |

| Subsection 7(1B) | Yes | Included with Section 7 in the OECD summary of a Resident Individual |

| Public Ruling No. 6/2011 | Yes | Listed as Residence Status of Individuals |

| Public Ruling No. 5/2011 | No | The provided excerpt is about companies and bodies of persons, not individuals |

Under the OECD summary of Malaysia's rules, a Resident Individual is someone resident in Malaysia for the basis year for a YA under Section 7 and subsection 7(1B) of the Act. A Non-Resident Individual is an individual other than a resident individual. In practice, the point that matters is timing. You classify a specific YA, not your entire nomad life in one pass.

A core test is physical presence. The same summary says residency is generally based on days physically present in Malaysia, and that Malaysian citizenship does not automatically make someone a tax resident. So do not use passport or nationality as a shortcut.

Before you rely on any article, advisor note, or forum answer, check that it points back to the right legal materials:

- Section 7

- Subsection 7(1B)

- Residence Status of Individuals, Public Ruling No. 6/2011

One quick quality check helps here. If a source cites Public Ruling No. 5/2011 for individual residency, treat that as a warning sign, because the provided excerpt is about companies and bodies of persons, not individuals. Also, Section 7 includes more than one residency route, so a single day-count baseline is not the whole law.

That distinction matters in practice. A source can get the headline idea right and still be too thin for filing if it skips the relevant rule text, omits the relevant public ruling, or blurs one YA into another. Your goal is not to collect opinions. It is to identify which rule you are relying on for a specific YA and make sure your records match that rule.

Apply the day-count rule correctly the first time#

Do not rely on memory. For each Year of Assessment (YA), count physical presence days inside that YA. If your result is borderline around the common threshold, take the stricter position until you verify it and keep proof for any claim to HASiL.

Count against the YA, not against your trip story#

For residency analysis, the baseline in the provided material is physical presence in Malaysia, not nationality or citizenship, and the individual YA runs from 1 January to 31 December.

That means your ledger should follow the calendar year. Do not group days by visa validity, invoice cycles, or a rolling 12-month view. A stay that crosses New Year has to be split across two YAs. In a self-assessment system, memory is a risk, not a shortcut.

The cleanest approach is to keep one ledger per YA and record each travel segment as it happens. A simple worksheet can include date range, place, entry or exit note, and the file name or link for the document that supports the entry. If a date is unclear, leave it marked as unresolved rather than smoothing it over. That is much easier to fix while records are fresh than after months of travel.

What the official example supports#

The clearest worked example here is HASiL Scenario 7(1)(a), which adds two stay blocks within YA 2024:

- 1.3.2024 to 30.6.2024 = 122 days

- 1.8.2024 to 30.9.2024 = 61 days

- Total = 183 days

What this supports is narrow but useful: exact dates matter, and separate stay blocks in the same YA can be totaled. What it does not settle from the provided excerpts is every Section 7 pathway, all absence rules, or all border-hop edge cases.

Read that example with discipline. It helps you with aggregation inside one YA. It does not let you assume that every break, every short trip, or every year-end crossing works the same way without checking the actual rule you need. Use official examples for what they clearly prove, and no more than that.

Handle borderline and part-day issues conservatively#

The source set here does not include the operative wording for part-day counting mechanics, even though the materials indicate that part of a day in Malaysia is treated as physical presence for that day. If your outcome depends on an arrival-day or departure-day assumption, keep it marked as unresolved until you verify primary filing guidance and keep evidence.

A practical way to manage a close call is to maintain two running totals in your worksheet. Keep one total for clearly supported days and one for days that depend on an unresolved counting assumption. That keeps you from quietly converting uncertainty into certainty. When you later verify the rule, you can update the total without rebuilding the whole file.

| Travel pattern | What the provided material supports | How to run your YA ledger | Main risk |

|---|---|---|---|

| Continuous stay in one calendar year | Physical presence in YA is the core baseline | Count dates that fall within 1 Jan to 31 Dec for that YA | Missing an edge entry or exit date |

| Split stay in same YA | HASiL example totals two blocks to 183 days | Track each block separately, then total in-year days | Counting gap periods as presence |

| Frequent in-out trips | No definitive counting mechanics here beyond physical presence being central | Log each entry and exit as its own line item | Memory-based counts become unreliable |

| Year-end crossing | YA follows calendar year | Split at 31 Dec and 1 Jan into two ledgers | Misallocating days to the wrong YA |

If your count is close, keep the stricter interpretation until it is confirmed, and preserve your worksheet plus supporting records before taking a formal residency position.

Handle the other Section 7 pathways without guessing#

Do not treat the headline day-count baseline as a complete Section 7 analysis. If your residency position depends on another pathway, treat it as unresolved until you verify it from primary guidance.

That caution matters because the current source set is missing the legal detail you would need for a shorter-presence argument. One candidate source was inaccessible, noted as Access Denied - WAF Rule Reached, and the only substantive accessible excerpt is an accounting paper on tax havens, not Malaysia residency rules. This is not the place to infer legal conditions from memory or from loose summaries.

| Reference | What is supported here | What is not confirmed here |

|---|---|---|

| Inaccessible candidate source | Confirm details directly with HASiL or a qualified Malaysian tax adviser. | Any legal detail it might have contained for Section 7 pathways. |

| ScienceDirect accounting excerpt | It covers tax-haven effects (including post-2017 EU-list outcomes), not Malaysia residency law. | Any Malaysia-specific Section 7 test, limb, or counting rule. |

| Income Tax Act 1967 (Section 7) | It is the legal anchor this section is trying to verify. | Exact sub-threshold conditions or how shorter-presence cases qualify from the provided excerpts. |

Use a strict filing rule here: if you are relying on any non-baseline Section 7 pathway, confirm it against current primary official guidance, or get qualified advice before filing. If you cannot point to the exact rule text you are using, your position is not ready to file.

In practice, that means your notes should name the pathway you think applies, the exact source you still need to verify, and the fact pattern that matters. "I was there a lot" is not a filing position. "I am relying on a non-baseline Section 7 route, but the legal conditions are not confirmed from primary guidance yet" is at least an accurate status note. It is also a signal to stop optimizing before the rule is verified.

For a step-by-step walkthrough, see A Guide to Tax Residency in the Czech Republic for Nomads.

Know what changes when status changes#

If your Section 7 position is not settled, treat rate tables, reliefs, and rebates as provisional assumptions. A Resident Individual versus Non-Resident Individual classification can affect planning, so avoid locking in status-sensitive items too early.

This matters most when freelance income is uneven. If cash flow is lumpy, a wrong status assumption can distort your reserves for the whole Year of Assessment. Until your status is supportable, run two views: a likely-case estimate and a conservative reserve that does not depend on status-sensitive items you have not verified.

Status impact at a glance#

| Area | If treated as Resident Individual | If treated as Non-Resident Individual | Practical move |

|---|---|---|---|

| Tax assumptions | Use resident-side assumptions only after your status is supportable. | Use non-resident-side assumptions only after the same status check. | Do not choose a rate method before confirming residence status. |

| Relief and rebate assumptions | Keep these assumptions provisional until current guidance confirms them. | Keep these assumptions provisional until current guidance confirms them. | Keep core cash planning independent of unverified assumptions. |

| Admin follow-up | HASiL's Residence Status page links to Section 7 ITA 1967 and Certificate of Residence resources. | The same HASiL page provides the HASiL Contact Centre for follow-up. | Settle status first, then complete filing detail decisions. |

| CIC operations updates | Bursa Malaysia Digital says CIC changes affecting tax-residency-related personal information must be reported within 30 days. | Examples include changing tax residency details, address, or contact number to outside Malaysia. | Treat this as a separate operational update and verify any separate IRBM/HASiL filing obligations directly. |

Use this checkpoint before you finalize numbers: can you support your classification with your records and related account updates? If not, strengthen the evidence first.

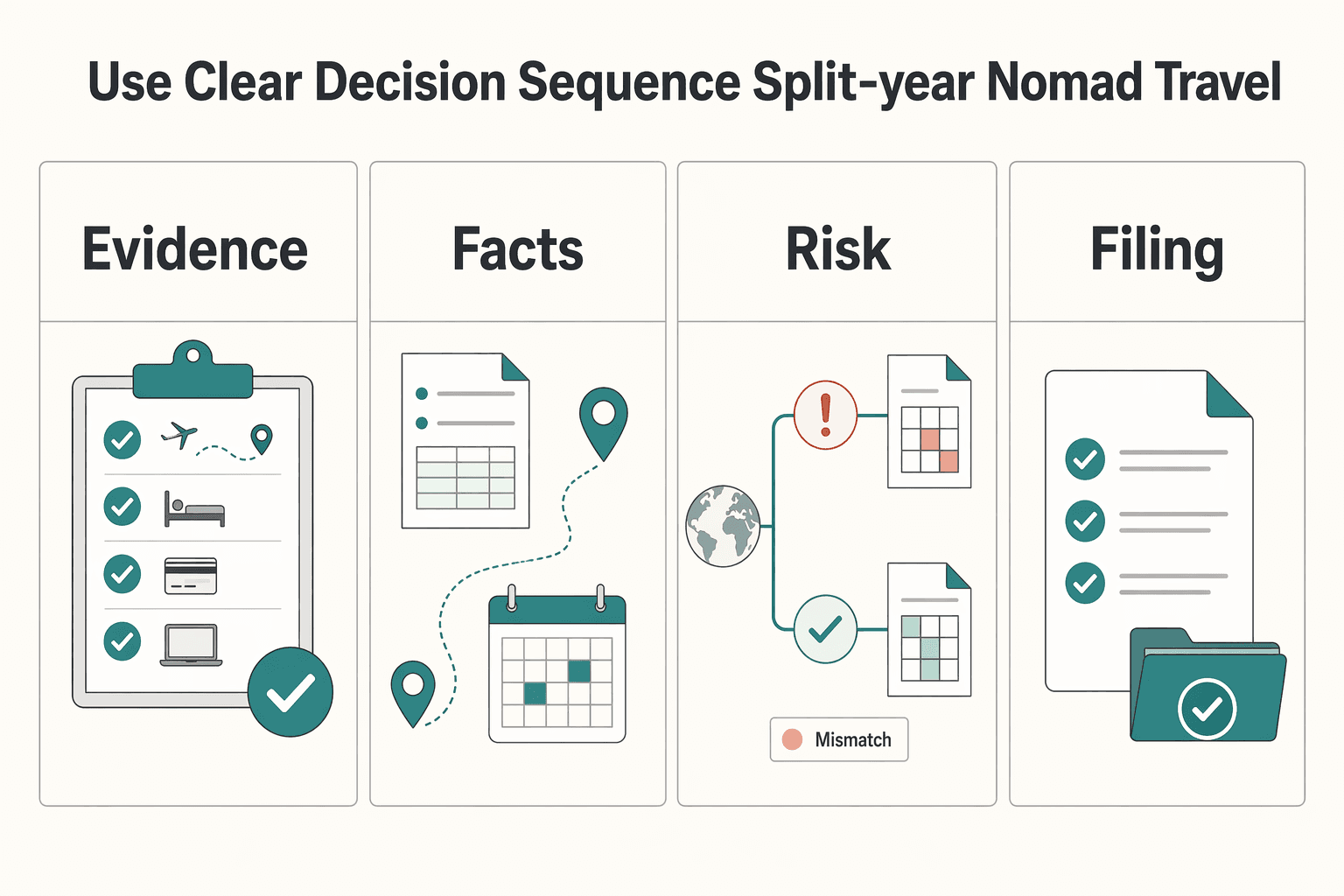

Use a clear decision sequence for split-year nomad travel#

Split-year travel is where otherwise careful people get sloppy. A conservative sequence is to build the facts first, set a provisional Section 7 view, check cross-border overlap risk, and then re-check before filing. Based on the provided materials, treat Malaysia-specific legal interpretation as unresolved until you confirm it in primary IRBM or HASiL guidance or with your advisor.

| Step | Action | Key detail |

|---|---|---|

| 1 | Build a YA timeline before labeling your status | Create a month-by-month log tied to records and mark unclear months as unresolved |

| 2 | Set a likely Section 7 bucket and record what could change it | Write down the exact missing fact or edge case that could flip the outcome |

| 3 | Check overlap risk early if another country may also claim residence | Compare the timeline you would give in Malaysia with the timeline you would give elsewhere for the same months |

| 4 | Add a pre-filing recheck date | Re-verify your YA timeline, unresolved gaps, and the Section 7 pathway you are relying on |

Step 1. Build a YA timeline before labeling your status#

Create a month-by-month log aligned to the relevant Year of Assessment, and tie each entry to records, for example passport and entry history. If any month is unclear, mark it as unresolved instead of guessing.

When travel is dense, work backwards from records you know you have. Start with clear border events, then fill the periods between them with accommodation and work-location notes. The point is not to create a beautiful spreadsheet. The point is to build a traceable timeline that someone else could follow without hearing your travel story first.

Step 2. Set a likely Section 7 bucket and record what could change it#

Classify your current position as a likely Section 7 outcome, not a final conclusion. In the same notes, write down the exact missing fact or edge case that could flip that outcome.

That second note is what keeps the classification honest. If the answer changes only if one arrival date is treated differently, write that down. If the answer changes only if you qualify under a non-baseline pathway you have not yet verified, write that down too. A provisional status note should show both your current view and the reason it is still provisional.

Step 3. Check overlap risk early if another country may also claim residence#

Before you optimize anything, test whether another country could apply a conflicting residency position to the same period. If the narrative changes from one country to another, keep assumptions conservative and resolve the conflict first.

A simple internal check helps: compare the timeline you would give in Malaysia with the timeline you would give elsewhere for the same months. If the two stories rely on different "home base" narratives or different counting assumptions, do not ignore that tension. Flag it before filing season compresses your options.

Step 4. Add a pre-filing recheck date#

Set one checkpoint before filing to re-verify your YA timeline, unresolved gaps, and the Section 7 pathway you are relying on. At that checkpoint, confirm that you and your advisor are using the same facts and the same current IRBM or HASiL materials.

This recheck matters because travel files usually get messier with time, not cleaner. By the point you are preparing the return, you want decisions to be about classification, not about trying to remember where you were.

Turn the 4-step sequence into a live monthly log so your day count and evidence stay filing-ready: Use the Tax Residency Tracker.

Manage dual residency before filing season pressure#

If Malaysia and another country can both treat you as resident for the same period, treat it as a dual-residency risk until you verify the position for that filing period.

Work in sequence. Confirm your likely domestic-law position in Malaysia first, then check whether a relevant and effective DTA could affect treaty treatment for that same period.

Keep two questions separate#

- What is your likely domestic-law position in Malaysia for that Year of Assessment?

- Is there a Double Tax Agreement between Malaysia and the other country that is relevant and effective for your period?

Keep these separate until the facts are stable. If you jump straight to treaty language, you can miss a basic domestic-law error or rely on treaty timing that does not apply to your filing dates.

Use the actual Malaysia treaty text#

Malaysia publishes DTAs through HASiL, and Malaysia states it has two categories: complete DTAs, which cover all income types, and limited DTAs, which cover certain income only. Confirm which type you are reading before you assume it can address a residence conflict.

Residence treatment in dual-residency situations can differ by treaty. Use the specific Malaysia treaty for that country pair, not a model summary. HASiL notes that OECD Model provisions may be adopted, omitted, or only partly adopted, and that some Malaysian treaties also adopt UN Model provisions.

Verify treaty timing before relying on it#

"Has a treaty" is not enough. HASiL distinguishes between entry into force (EiF) and entry into effect (EiE), and those dates are not interchangeable for filing.

| Checkpoint | Why it matters |

|---|---|

| Status shown as signed, terminated, or currently in force | Signed is not the same as currently in force |

| EiF and EiE timing | Provisions may not apply to your tax period yet |

| Unique gazetted Order Number | Anchors the exact agreement you reviewed |

If treaty residence could affect your filing, keep a copy of these treaty-status details with your YA records.

Keep the domestic-law analysis in place#

Treaty outcomes are specific to each agreement. The applicable treaty text and status dates do not, on their own, resolve every domestic-law residency question, so verify both sides before filing.

When filing pressure builds, keep the default simple: document your domestic-law position, then test treaty residence using the currently effective DTA for that period. If either side is unclear, get advisor review before filing.

Build your evidence pack before anyone asks for it#

Your position is easier to defend when your records are organized, so build a Year of Assessment (YA) evidence pack now. For residency analysis, keep a day-count worksheet that links each claimed day to documentation you can retrieve quickly.

| Record set | What to keep | Why it matters |

|---|---|---|

| Travel evidence | Passport stamp scans, flight itineraries, boarding passes, booking confirmations, and other entry or exit records you actually received | Helps anchor where you were and when you crossed borders |

| Accommodation timeline | Lease dates, hotel invoices, rental receipts, and a simple start and end log by address | Helps explain location when travel records are thin |

| Work-location notes | Calendar entries, meeting logs, client notes, invoices, or other dated records showing where you worked | Adds context for frequent in-and-out travel patterns |

| Day-count worksheet mapped to YA | One line per day with country, city, arrival or departure note, and a link or filename for supporting proof | Turns raw records into a reviewable filing file |

Organize this by YA, not only by trip folder. If one trip crosses year-end, split it across the relevant YA records.

A good evidence pack is easy to review under pressure. Name files consistently, keep the worksheet in the same folder as supporting documents, and use the same labels across your records. If your worksheet says "entry record," the file should be easy to find without opening ten attachments.

Keep the administrative trail too#

Treat this as a conservative recordkeeping workflow, not a statement of HASiL process rules; confirm exact official documentation requirements with HASiL directly.

If a Certificate of Residence may matter, keep a separate admin folder with dated notes, correspondence, draft materials, and the exact government pages you reviewed. The practical default is to preserve what you relied on and when, rather than reconstructing it later.

For any guidance page you use, save the page title, access date, and a copy. The Malaysia travel advisory extract shows an issue date of February 22, 2026. It tells travelers to review "entry and exit requirements," which is useful as a freshness check and an immigration-record prompt.

If you enroll in STEP, keep that record too: the same advisory says enrollment helps the U.S. embassy or consulate contact you or your emergency contact in an emergency.

It also helps to keep a short note explaining why each saved page mattered. The value is not literary; it is that, months later, you can still tell the difference between a page you relied on and a page you saved while browsing.

Use one verification rule#

As a conservative rule, have each claimed day trace to at least one primary record. If a day exists only in memory, treat it as unverified until you can match it to dated evidence.

Primary records are event-close items, such as stamp images, boarding passes, or lodging invoices. Supporting notes can add context, but they should not be your only proof for important days.

If a record is weak but still useful, keep it and label it honestly. That preserves the trail without overstating what it proves. The goal is to know which days are solid, which days need follow-up, and which assumptions should not be used in a final filing position.

Set escalation triggers and when to hire a pro#

If your filing position depends on interpretation, unclear facts, or weak records with real money at stake, escalate before you file.

After you assemble your evidence pack, run one test: can you explain your full tax-year timeline without filling gaps from memory? If not, treat it as advisor-review territory. Escalate if any of these apply:

- your position depends on special tax-residency treatment, a cross-border residence position, or uncertain treaty interpretation

- your status changed mid-year and you cannot map events cleanly into one tax-year narrative

- your planned filing position relies on assumptions you cannot support with dated records for a potential audit review

This is a practical risk call, not a panic call. Audit remains a core part of tax compliance, and authorities continue refining how they use data and analytics. Weak files are harder to defend later than to fix now.

Use a simple threshold: uncertainty, money at stake, and weak records means you should get advisor review before submission.

One useful mindset shift is to escalate while the facts are still easy to reconstruct. Do it before you have built your budget, return draft, and personal assumptions around an answer you hope is right. A short review early is usually cleaner than a late scramble to defend a position built on incomplete files.

Understand how DE Rantau fits and where it does not#

DE Rantau helps with immigration permission in Malaysia, but it does not decide your tax status. For filing, Malaysia tax residency is still determined under the Income Tax Act 1967, especially Section 7, for each Year of Assessment.

| Item | Track | Note |

|---|---|---|

| DE Rantau approval | Immigration check | Helps with immigration permission in Malaysia, but it does not decide your tax status |

| Professional Visit Pass (PVP) dates | Immigration check | Described as three (3) to twelve (12) months |

| Renewal records | Immigration check | Up to an additional 12 months |

| YA day-count record | Tax check | Part of the tax check alongside your Section 7 basis |

| Section 7 basis | Tax check | Used for Resident Individual or non-resident status for each Year of Assessment |

Treat this as two parallel checks that you reconcile before you file:

- Immigration check: DE Rantau approval, Professional Visit Pass (PVP) dates, and renewal records, with the pass described as three (3) to twelve (12) months, with up to an additional 12 months.

- Tax check: your YA day-count record and your Section 7 basis for Resident Individual or non-resident status.

The control that matters is date matching. A valid pass period does not automatically make you a Resident Individual, and visa permission does not replace Section 7 analysis. Section 7 includes multiple residence circumstances, with physical presence of 182 days or more as a common baseline.

The most avoidable mistake here is assuming, "I have the pass, so I must be resident." If your DE Rantau timeline, actual presence, and Section 7 position do not align, resolve that mismatch before submission. For visa mechanics, read A Guide to the Malaysian Digital Nomad Visa (DE Rantau).

A practical reconciliation step helps. Put the immigration dates and the tax-residency timeline on the same page. That makes it easier to spot gaps between permission to stay and actual presence, and it reduces the risk that you treat one as proof of the other.

Related: London, UK: A Guide for Expats and Remote Workers.

Conclusion#

Classify first, optimize second. If your status call is wrong, every later filing choice sits on a weak base.

Keep a defensible evidence file throughout the year, not right before filing. If you also have company issues in the mix, keep them separate: for companies, the core checkpoint is where management and control are exercised, supported by governance records in the basis year (for example, whether at least one Board meeting on management and control was held in Malaysia).

Most mistakes come from messy facts and broad assumptions. In cross-border cases, do not assume treaty logic always applies; where no treaty applies, domestic scope can be wider. Use this closing rule:

- If your facts are straightforward and well documented, keep the file organized and recheck it before filing.

- If your position depends on uncertain cross-border classification or treaty applicability, get professional review before you file.

- If you cannot evidence the facts behind your filing position, fix the records first.

The available evidence here is limited for Malaysian individual residency specifics, so treat gray-area individual positions as escalation cases and get a second set of eyes before you file: Talk to Gruv.

Frequently Asked Questions

What is the core Malaysia tax residency day-count rule?

The common baseline is physical presence in Malaysia for 182 days or more in the relevant basis year for a Year of Assessment. That is the starting point most people use under Section 7 of the Income Tax Act 1967. If your total is close to the threshold, verify your count carefully before taking a filing position.

Are Malaysian citizens automatically treated as tax residents?

No. Citizens of Malaysia are not automatically tax residents. Residence is generally determined under Section 7, not by citizenship alone.

Does part of a day in Malaysia count as a full day for residency counting?

Yes. The provided materials indicate that being in Malaysia for part of a day is treated as physical presence for that day. If your outcome depends on edge-date counting, verify your dates carefully before filing.

Is the common day-count threshold the only way to qualify as a Resident Individual?

No. Section 7 includes more than one residency circumstance, so the common baseline is not the only pathway. The full legal conditions for the other pathways are not set out here, so confirm them before assuming you qualify.

What happens if both Malaysia and another country treat me as resident?

This is where a Double Tax Agreement (DTA) can matter, because DTAs generally include tie-breaker tests for treaty purposes. But a treaty outcome does not automatically remove Malaysian domestic-law analysis. Income can still be assessable to Malaysian tax, so you still need to work through your Malaysia position for the same period.

Do I need a Certificate of Residence, and when is it usually relevant?

You may need one when you must evidence Malaysian residence status. The provided material does not set out exact eligibility, required documents, or processing steps. It does confirm that HASiL’s Residence Status page links to both Section 7 ITA 1967 and a dedicated Certificate of Residence page.

Does holding a DE Rantau visa automatically make me a Malaysia tax resident?

No. The provided materials do not show any rule that a DE Rantau visa automatically determines Malaysia tax residency. Assess tax residence under Section 7 for each YA.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/law/view/documenttrusted

- bsee.gov/sites/bsee.gov/files/tap-technical-assessmen...trusted

- congress.gov/event/118th-congress/senate-event/LC74704/texttrusted

- digitalcommons.law.byu.edu/cgi/viewcontent.cgitrusted

- federalreserve.gov/aboutthefed/boardmeetings/files/npr-expanded...trusted

- federalreserve.gov/reportforms/formsreview/fry14q_20111216_f.pdftrusted

- irs.gov/irm/part21/irm_21-008-004rtrusted

- lawcat.berkeley.edu/record/1112555/files/fulltext.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

London, UK: A Guide for Expats and Remote Workers

Get two calls right early and the rest of the move gets easier: how you'll be in the UK, and where you'll work when conditions are less than ideal. Make those decisions before you lock dates or prepay a long stay. If you book first and sort the basics later, admin and work reliability usually collide in your first week.

Planning Your Move With the Malaysia Digital Nomad Visa (DE Rantau)

Treat this as a verification-first playbook, not a travel pitch. If you cannot confirm current rules from official Malaysian sources, the best move is to pause before planning anything else.