Quick Answer

Superannuation for Australian freelancers is not a one-rule decision. If you are a sole trader or in a partnership, SG for yourself is generally not compulsory, but labour-based contractor arrangements can still create SG risk even with an ABN. The safest approach is to run a repeatable pre-invoice classification check, choose a cashflow-fit contribution method, and keep clear records you can defend later.

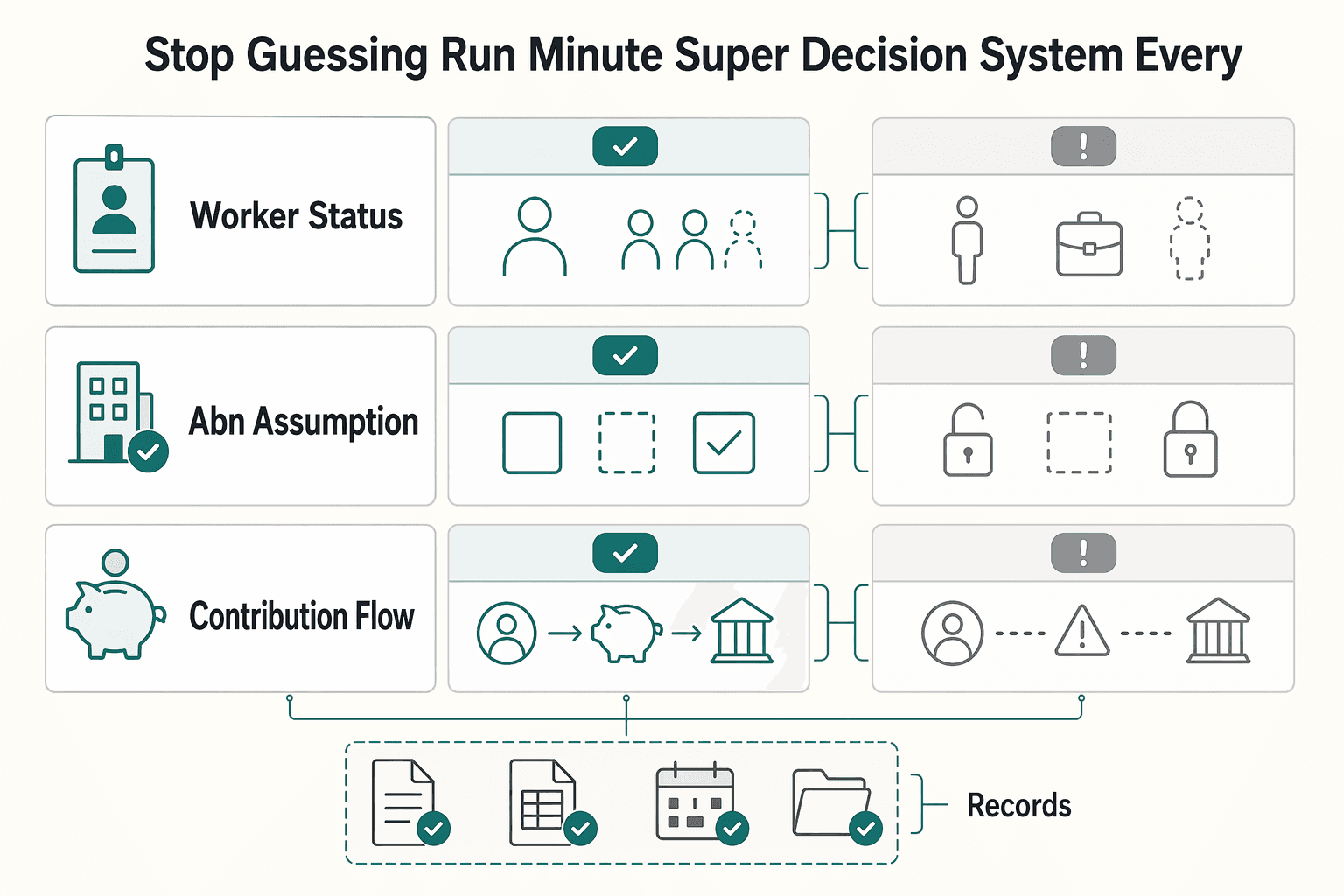

Stop Guessing and Run a 10 Minute Super Decision System on Every Client#

Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure. As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.

This section gives you a practical playbook to decide when super looks optional, when it may be mandatory, and what evidence to store each time. It is Australia-focused and built for day-to-day execution. It is not legal advice.

Where exact ATO legal thresholds are not fully visible in the available excerpts, use this system to flag risk early and confirm details before you lock terms.

| Decision point | What to check fast | Default action | What to document |

|---|---|---|---|

| Worker status | Employee vs independent contractor signals | If unclear, treat as high risk | Classification notes and contract terms |

| ABN assumption | Whether ABN is being used as a shortcut | Do not assume ABN removes SG exposure | ABN details plus reason for decision |

| Contribution flow | Wage-like cadence or business-revenue cadence | Match method to cashflow reality | Planned transfer method for retirement savings |

The core rule is simple: a label alone does not protect you. A person can operate as an independent contractor and still fall into superannuation guarantee pathways in some cases. Run the ATO eligibility check before you rely on assumptions.

Also avoid stale rules. Older memory about the former monthly earnings cutoff can mislead decisions now.

Imagine you onboard a client with tight control over how you work. You still have your own ABN, but you do not stop at the label. You run the check, record the outcome, and choose the contribution path that protects both compliance and working capital.

Run this before onboarding and before each invoice#

- Confirm classification risk first, then confirm pricing and payment terms.

- Record why you treated super as required, uncertain, or not indicated.

- Choose a contribution cadence you can sustain through uneven months.

- Store notes in one place so future-you can defend the call quickly.

Run it every time so you stay in control instead of reacting under pressure. Want a quick next step for "superannuation for freelancers australia"? Try the free invoice generator.

Build the Mental Model Before You Touch a Contract#

Anchor every client decision to super definitions first, then verify obligations before you sign or invoice. You already have a decision rhythm. Now lock the model so your calls stay consistent even when contract language changes.

For superannuation for freelancers australia, start with plain meanings you can apply fast. Superannuation is retirement savings invested through a super fund. Superannuation guarantee (SG) is the minimum compulsory employer super amount for eligible employees, and it can also apply to contractors paid mainly for labour. Current ATO employer guidance sets the benchmark at 12% from 1 July 2025. The ATO also signals a shift to payday timing from 1 July 2026.

Treat those as operating anchors, then confirm the latest details for your exact facts.

| Term | What it means for your workflow | Operator rule |

|---|---|---|

| Superannuation | Long-term retirement savings held in a super fund | Build self-employed super into your cashflow plan, not as an afterthought |

| SG | Compulsory contribution framework for eligible workers | Check SG exposure before final contract terms |

| Independent contractor | Commercial label in a contract | Do not stop at the label when SG risk exists |

| Employee for SG purposes | Status that can apply when payment is mainly for labour | Escalate and verify before you treat super as optional |

| ABN | Unique 11-digit business identifier | Never use ABN alone to decide SG treatment |

| Choice of fund | Worker nominates where compulsory SG goes | Capture fund choice early when SG may apply |

Run this classification script before contract approval#

| Check | What to do |

|---|---|

| Client purchase | Ask what the client actually buys: a deliverable outcome or mainly your labour. |

| Labour signal | If the arrangement points to mainly labour, treat SG as a live risk even when an ABN appears on invoices. |

| Verification | Run the ATO eligibility tool before you lock commercial terms. |

| Recordkeeping | Record your reasoning in the client file so you can defend the decision later. |

- Ask what the client actually buys: a deliverable outcome or mainly your labour.

- If the arrangement points to mainly labour, treat SG as a live risk even when an ABN appears on invoices.

- Run the ATO eligibility tool before you lock commercial terms.

- Record your reasoning in the client file so you can defend the decision later.

Imagine a client engages you for ongoing execution and expects your personal work each week. You hold an ABN, but you still run the SG check, log the result, and confirm whether fund choice steps apply. That is how you protect compliance and cashflow.

Use Moneysmart and the Superannuation calculator to plan contribution amounts for retirement savings, but treat calculator outputs as planning assumptions, not legal determinations. Then verify final obligations through current ATO guidance for your exact arrangement. If you want a deeper dive, read this guide.

Do You Actually Have to Pay Super as a Freelancer in Australia?#

Use a conservative triage: treat your own super as optional in sole trader or partnership setups, and treat labour-based engagements as potential SG risk until you verify them. Apply this model to client work so your super decisions stay consistent under pressure.

Start with the legal frame. Superannuation guarantee (SG) is the minimum super employers must pay for eligible employees. If you operate as a sole trader or in a partnership, you do not have to pay SG for yourself. You can still make personal super contributions for retirement savings.

| Situation | Default position | What you do next |

|---|---|---|

| You earn as a sole trader or partner | Personal SG for yourself is not compulsory | Set a voluntary contribution rule that fits cashflow |

| The worker relationship is employment | PAYG withholding and super obligations apply | Confirm withholding and pay super at least quarterly for eligible employees |

| You engage an independent contractor mainly for labour | SG risk rises because this can be treated as employee status for SG purposes | Run an SG eligibility check before you finalize terms |

| You see mixed signals | Classification risk stays high | Escalate to ATO verification and document your decision |

An ABN does not decide SG by itself. You need to review the whole working arrangement, and labour-based contractor engagements can still trigger SG treatment. If uncertainty remains, treat it as high risk and verify before you finalize terms.

Use this triage before every contract#

- Identify your structure first: sole trader, partnership, or employee context.

- Check whether payment is mainly for labour.

- Do not use ABN as a shortcut rule.

- Verify unclear cases with the Australian Taxation Office (ATO) decision tool before final agreement.

- Log the decision in your workflow.

Imagine you sign a client engagement that depends mainly on your personal labour. You invoice with an ABN, but you still flag SG risk, run the check, and hold terms until you confirm classification. That one habit protects compliance and cashflow. Related: A Guide to Tax Residency in Australia for Digital Nomads.

Which Client Contracts Trigger SG Risk and Which Are Lower Risk?#

Contracts that pay for personal labour, remove delegation rights, and are not paid to achieve a defined result carry higher SG risk, while outcome-based contracts with a genuine delegation right usually sit lower risk. You already triaged whether super may apply. Now turn that into a contract worksheet you can run before onboarding and before every invoice.

For superannuation for freelancers australia, treat classification as an operations task, not a one-time legal guess. Start with the full working arrangement and do not rely on labels alone. An ABN identifies a business, but it does not decide whether an independent contractor falls into superannuation guarantee (SG) obligations. If contract terms look employee-like, you also increase sham contracting risk.

| Worksheet field | Higher SG risk signal | Lower SG risk signal | Evidence to keep |

|---|---|---|---|

| Payment basis | Client pays mainly for your personal labour and skills | Client pays to achieve a defined result | Scope, deliverables, acceptance criteria |

| Delegation | You must perform the work personally | Contract gives a real right to delegate | Delegation clause and any subcontract process |

| Role design | Work is not paid to achieve a defined result | Clear project deliverables tied to results | Statement of work and change log |

| Identity checks | ABN entered but details are inconsistent | ABN and legal name align in ABN Lookup and onboarding records | ABN Lookup result and onboarding notes |

Pre invoice decision gate#

- Mark each client as SG appears required, SG uncertain, or SG not indicated.

- Route every uncertain case to Australian Taxation Office (ATO) verification using arrangement-based questions.

- Record why you made the call, who approved it, and what would trigger a re-check.

- Re-run the gate when scope, control, or pricing model changes.

Imagine a client hires you for monthly delivery, requires your personal work, and rejects substitutes. You still invoice under your ABN, but your worksheet flags labour-heavy terms and no delegation. You classify the file as uncertain, escalate to ATO confirmation, and pause final terms until you resolve it. This approach protects cash flow and keeps your process consistent across clients.

How Does Your Business Structure Change the Super Playbook?#

Your business structure sets your super default, so every shift between sole trader, partnership, and PAYG wage setups needs a fresh SG review. Your contract gate tells you where SG risk sits. Now connect that gate to your operating model, because structure changes what you actually have to do next.

For superannuation for freelancers australia, keep the baseline simple. If you work as a sole trader or in a partnership, you do not have to pay superannuation guarantee (SG) for yourself. You can choose personal contributions for retirement savings.

If your entity pays wages in an employer-style setup, you must pay SG for eligible employees in addition to salary and wages.

| Structure mode | Super default | Workflow consequence |

|---|---|---|

| Sole trader or partnership | SG is not compulsory for your own earnings | Build a disciplined self-employed super transfer routine tied to cashflow |

| PAYG wage setup | Employer SG obligations apply for eligible employees | Sync payroll, PAYG withholding, and SG processing as one control cycle |

| Contractor case with SG exposure | Employer-side SG steps can still apply | Confirm choice-of-fund and amount-to-pay steps before final approval |

Use current timing rules in your process design. The SG benchmark rate in ATO employer guidance is 12% from 1 July 2025. From 1 July 2026, employers must pay SG on payday. That timing shift matters operationally, so plan your workflow for payday SG when your structure puts you in employer territory.

Match structure to your system#

- Tie invoicing rules to structure. Personal contribution cadence for sole trader mode, payroll-linked controls for PAYG mode.

- Define who owns each task: classification, payroll entry, contribution approval, and record retention.

- Add a pre-invoice check that confirms structure has not changed since the last decision.

Add a structure changed trigger#

Imagine you move from project-based solo invoicing to paying regular wages through your entity. Your contract gate still works, but your super workflow must switch immediately. Re-run SG classification, update payroll controls, and log the change before the next invoice cycle.

Use current Australian Taxation Office (ATO) guidance as your final check whenever facts are mixed and structure details are changing. You might also find this useful: The Best Tools for Creating Professional Presentations.

How Do You Fund Super Without Breaking Cashflow?#

Fund super by matching contribution timing to your income pattern, then run that same rule after each cleared invoice. You already mapped SG risk and structure. Now you need a cashflow routine you will actually stick to.

For superannuation for freelancers australia, pick one funding model and run it consistently. If you pay yourself like a wage, use regular transfers into your super fund. If money lands as business revenue, use lump sums when cashflow allows. The goal is a plan you can execute in good months and bad months.

| Income pattern | Funding model | Cashflow guardrail | Admin check |

|---|---|---|---|

| Predictable pay cycle | Regular transfer | Transfer on a fixed date after core business costs clear | Confirm TFN and fund account details |

| Variable invoice cycle | Lump sum transfer | Move funds only after you hit your operating buffer | Record contribution type before sending |

Run an invoice linked funding loop#

| Trigger | Action |

|---|---|

| After each invoice clears | Move a planned amount into a holding bucket. |

| On your funding date | Transfer from that bucket to your super fund. |

| Admin details | Keep TFN and account details current to help your fund accept and process contributions. |

| If you want to claim a deduction | Send a notice of intent to claim form to your fund in the required process window. |

| Before you lock transfer amounts | Use the Superannuation calculator to test different contribution amounts and estimate retirement balance and fee effects. |

Imagine you hit two soft months, then one strong month. You keep essentials funded first, then send a lump sum contribution from the recovery month instead of forcing fixed transfers during the dip. You protect cashflow and still move retirement savings forward.

For planning context in Australian finance, Moneysmart notes that super contributions are taxed at 15% in this context. It also lists annual figures up to $30,000 concessional and $120,000 non-concessional contributions. Treat those as planning guardrails, then confirm current limits and specific rules with the ATO before year end or when your income pattern changes.

Create an Audit Ready Super Record You Can Defend Later#

Create one client file that records your SG decision, evidence, and escalation path so you can defend each super call later. Now that you have a super rule, lock in the reasoning behind every decision. This is the control that keeps your process consistent when facts shift across clients and over time.

For each independent contractor engagement, log the classification outcome and what evidence you used. Also record why you treated it as a potential superannuation guarantee (SG) case, including fund-choice steps where relevant. Do not rely on memory.

SG outcomes change with work arrangement details, so your log should show the decision logic you applied on that date.

Build one defendable client file#

Keep the record digital and keep it together for at least 5 years so you can retrieve it fast during a review. Store these core artifacts in one folder or workspace per client.

| Record element | What to capture | Why it protects you |

|---|---|---|

| Classification decision log | Outcome, decision date, evidence summary, optional contribution or potential SG | Shows a repeatable process based on work arrangement facts |

| Contract evidence | Signed contract version, scope, delegation terms, pricing model | Proves what you agreed, not what you later remember |

| Identity and admin checks | Legal name match, super fund and TFN workflow notes where relevant | Reduces processing and mismatch errors |

| Clarification trail | Communication notes and any ATO guidance references | Shows you escalated uncertainty instead of guessing |

| SG operational notes | If SG risk exists, include choice of fund and next action owner | Turns compliance into a clear action list |

Reuse this one-page checklist each cycle#

Run this checklist on a regular operational cadence, and also run it any time scope, delegation, or pricing changes. Rules vary by work-arrangement facts, so your SOP should explicitly say that uncertain cases go to Australian Taxation Office (ATO) guidance.

- Classification still matches the current work arrangement.

- Contribution method still fits your current cashflow routine.

- Documentation is complete and stored in the client file.

- Any new ambiguity has an open escalation with a clear owner.

- Retirement savings actions align with your current superannuation plan.

Put This Super System on Autopilot Before Your Next Invoice#

Run one repeatable pre-invoice routine on every client so your super decisions stay compliant, cashflow-aware, and defensible. You now have the pieces. The win is turning them into a standard operating rhythm you actually run.

In superannuation for freelancers australia, the order matters. If you skip classification, you can misread an independent contractor arrangement. If you skip documentation, you lose your audit trail. If you skip review, changing contract terms can quietly break your assumptions.

Run this four step sequence on every client#

| Step | What to do |

|---|---|

| Classify the engagement first | Check whether the work arrangement points to SG exposure, including labour-heavy contractor arrangements where SG can still apply. Do not use ABN status as your decision shortcut. |

| Choose the contribution method second | If SG applies, pay on time, to the right super fund, and at the correct rate. If you operate as a sole trader or partnership for your own income, you can make personal super contributions to keep retirement savings moving. |

| Document the decision third | Save the decision basis, contract terms, fund-choice records, and key admin evidence in one file. Keep required super records for 5 years. |

| Review on a clear trigger | Recheck the file before invoicing when contract terms or payment structure changes, and recheck at your regular admin cadence. |

Imagine this scenario: a long-running client shifts from outcome-based work to mostly personal labour. You rerun classification before the next invoice, update the file, and adjust your workflow immediately.

Start today and operationalize it#

Run the checklist on one active client today, then add it to onboarding and invoicing SOPs:

- pre-invoice classification check

- contribution path decision

- evidence saved in one place

- uncertainty escalated to current ATO guidance and your accountant or tax agent

That is how you keep self-employed super practical, reduce compliance surprises, and run stronger operations.

Frequently Asked Questions

Do freelancers in Australia have to pay super?

Not always. If you operate as a sole trader or in a partnership, you generally do not have to pay superannuation guarantee for yourself, but you can still make personal contributions to your super fund. Start with your operating structure, then confirm unclear cases with the Australian Taxation Office (ATO).

If I have an ABN, can a client still owe me super?

Yes. An ABN does not decide SG liability on its own, and it does not automatically remove a client’s obligation. If a client pays you mainly for your labour, SG rules may still require super contributions.

When is an independent contractor treated as an employee for superannuation guarantee purposes?

Focus on the actual work arrangement, not just contract labels. When payment is mainly for labour, SG rules may classify that independent contractor as an employee for superannuation guarantee purposes. Re-run this test when engagement terms change.

Does being a sole trader, partnership, or PAYG setup change whether super is compulsory?

Yes. Your setup changes the workflow and risk points you need to manage. Sole trader and partnership operators usually handle self-employed super through personal contributions, while PAYG wage setups may involve employer-style super obligations. When you change structure, recheck your decision process before the next pay or invoice cycle.

Can I make personal super contributions if SG is not compulsory in my case?

Yes. You can add your own money directly to super even when SG is not compulsory for you personally. This gives you a controlled way to keep retirement savings moving without waiting on a client-driven SG outcome.

How should I handle super contributions when my freelance income is irregular?

Moneysmart outlines two practical paths depending on how you pay yourself: regular transfers when you pay yourself a wage, or lump-sum transfers when business cash flow allows. If you pay SG for eligible workers, follow required timing in your payroll process, including payday-based timing from 1 July 2026.

What should I document if my contract terms change during a long client engagement?

Revisit your classification when terms change during a long engagement. ATO guidance flags changing circumstances that are not reconsidered as a high-risk pattern. Record what changed, your updated decision, and any uncertainty you need to escalate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

The Best Tools for Creating Professional Presentations

Use a 2025-2026 validation sweep each quarter: confirm one monthly software baseline ($15/month), one collaboration baseline ($30/month), and one premium workflow baseline ($60/month) before changing client-facing tool commitments.