Quick Answer

SOC 2 compliance for SaaS means running real security controls that an independent third-party auditor can test and document in a SOC 2 report. The practical path is to lock scope early, map controls to Trust Services Criteria, assign clear owners, and collect recurring evidence. This turns compliance into an operating system that supports buyer trust and reduces procurement friction.

Build Your SOC 2 Playbook Before a Big Client Forces the Timeline#

Build your SOC 2 playbook before sales pressure hits, so you control scope, evidence, and audit timing instead of reacting under stress. If you're pursuing soc 2 compliance for saas, treat this guide as a system, not a policy exercise. As the CEO of a business-of-one, you need a SOC 2 plan that protects your calendar as much as your customers. Use it to decide what to implement first, keep the right proof, and connect the work to clearer security controls, cleaner buyer conversations, and fewer fire drills.

When a big prospect asks for proof of trust during procurement, your team should not be digging through old tickets and scattered docs. You should be able to open one control tracker, show how controls run in day-to-day work, and explain your audit path without guessing.

| What to lock early | Why it matters | Safe default action |

|---|---|---|

| Scope boundaries | Scope drives effort, risk, and audit focus | Define which systems, teams, and customer-facing workflows your SOC 2 work covers |

| Readiness assessment | Early diagnosis prevents late surprises | Run readiness first, identify key service commitments, then map controls to selected Trust Services Criteria |

| Evidence rhythm | Auditors test operating effectiveness, not just policy text | Assign owners and collect recurring proof for each control in your normal workflow |

| Report narrative | Buyers need assurance they can review quickly | Prepare for a SOC 2 report that customers and their auditors can use to evaluate your control environment |

You also need clear boundaries around uncertainty. Timeline and cost vary by context and execution quality, so do not build false precision into your plan. AICPA does not set a minimum audit period for SOC 2 Type 2.

Some teams report readiness work of around one to two months. Some auditors see three months as the shortest practical testing window. Treat those as planning signals, not promises. Scope choices also change cost, especially when you add additional criteria.

Use this as your operating rule: lock scope first and start the evidence cadence early. Track unknowns in plain language, then move forward with disciplined work that supports SaaS growth instead of interrupting it.

If you want a deeper dive, read Taxes in Germany for Freelancers and Expats.

What SOC 2 Actually Means for a SaaS Operator#

SOC 2 means an independent third-party auditor tests how your SaaS business runs security controls, then issues a report buyers can evaluate. To use this playbook, you need a shared definition that keeps you out of busywork. Many teams lose time here by treating SOC 2 like a badge rather than an operating standard for trust.

A SOC 2 examination is an attestation on controls relevant to Trust Services Criteria (TSC), including security, availability, processing integrity, confidentiality, and privacy. AICPA sets the attestation standard that anchors this framework. For SaaS, security is mandatory, and you choose additional criteria based on the services you provide.

| Component | What it means in practice | Why operators should care |

|---|---|---|

| SOC 2 controls | Daily controls your team runs in real workflows | Auditors test design and operating effectiveness during the audit period, so consistent execution matters |

| SOC 2 report | Formal output from the examination | Customers, partners, and their auditors review it to evaluate your control environment |

| TSC selection | Criteria you include beyond mandatory security | Scope affects workload, evidence needs, and how clearly you show maturity |

Treat scope as a business decision. Start by defining it in plain language, then map it to controls.

- List the systems that process user data.

- Name the teams that operate or approve key control activities.

- Identify customer-facing workflows that touch systems and controls in scope.

- Mark what you will not include yet, so procurement conversations stay accurate.

If you're preparing for enterprise diligence, this matters quickly. Instead of saying, "we are SOC 2 compliant," describe what is in scope, show recurring evidence for core controls, and call out what will come later. That lands better than vague claims because it gives buyers something they can actually evaluate.

Keep this filter in place: if a control does not run in real operations, it does not strengthen compliance. If scope does not clearly reference the systems that process user data, it will not support a credible SOC 2 audit conversation.

The Mental Model That Turns Compliance Into Operating Discipline#

Run SOC 2 as a four-stage operating model: define scope, prioritize Common Criteria, run evidence rhythms, then test readiness before audit. Once your definition is locked, the job is execution. The goal is simple: make compliance look like normal operations, not a special project your team only does when a deal is on the line.

Use a four-stage model your team can operate consistently#

Treat this as a practical sequence, not a rigid rulebook. AICPA anchors the Trust Services Criteria (TSC), and SOC 2 evaluates controls relevant to security, availability, processing integrity, confidentiality, and privacy. A common starting point is Security (the Common Criteria), then adding criteria that match your services.

| Stage | Core operator question | Output that proves progress |

|---|---|---|

| Define scope | What systems process user data, and where are boundaries? | System description with boundaries, components, data flows, and in-scope workflows |

| Prioritize Common Criteria | Which security controls reduce real risk first? | Control set mapped to Security criteria with named owners |

| Run evidence rhythms | Can we show controls running in normal operations? | Time-stamped artifacts collected on a repeatable cadence |

| Prepare readiness checks | Would a SOC 2 audit reviewer see operating discipline? | Gap log, remediation actions, and an audit-ready evidence trail |

Prove control execution, not policy volume#

A policy can exist on paper while a control fails in production. Auditors care about operating proof, not the number of documents you can attach. For Type 2 readiness, you need controls that run consistently over the observation period, commonly framed as 3, 6, or 12 months.

Hold yourself to a simple standard: a control only counts if your security program operates in the real world. In practice, that means:

- Assign one owner to every control.

- Define the control cadence in plain language.

- Store artifacts where your team can retrieve them quickly.

- Review exceptions and remediation status in a recurring forum.

When you answer a customer questionnaire, policy PDFs alone are not enough. Show access reviews, incident workflow records, and change approvals tied to specific controls. That is operational compliance, and it builds confidence fast.

Working rule: if you cannot name the owner, cadence, and evidence for a control, treat it as not operational yet.

Related: Working Remotely in Latin America: A Visa Guide.

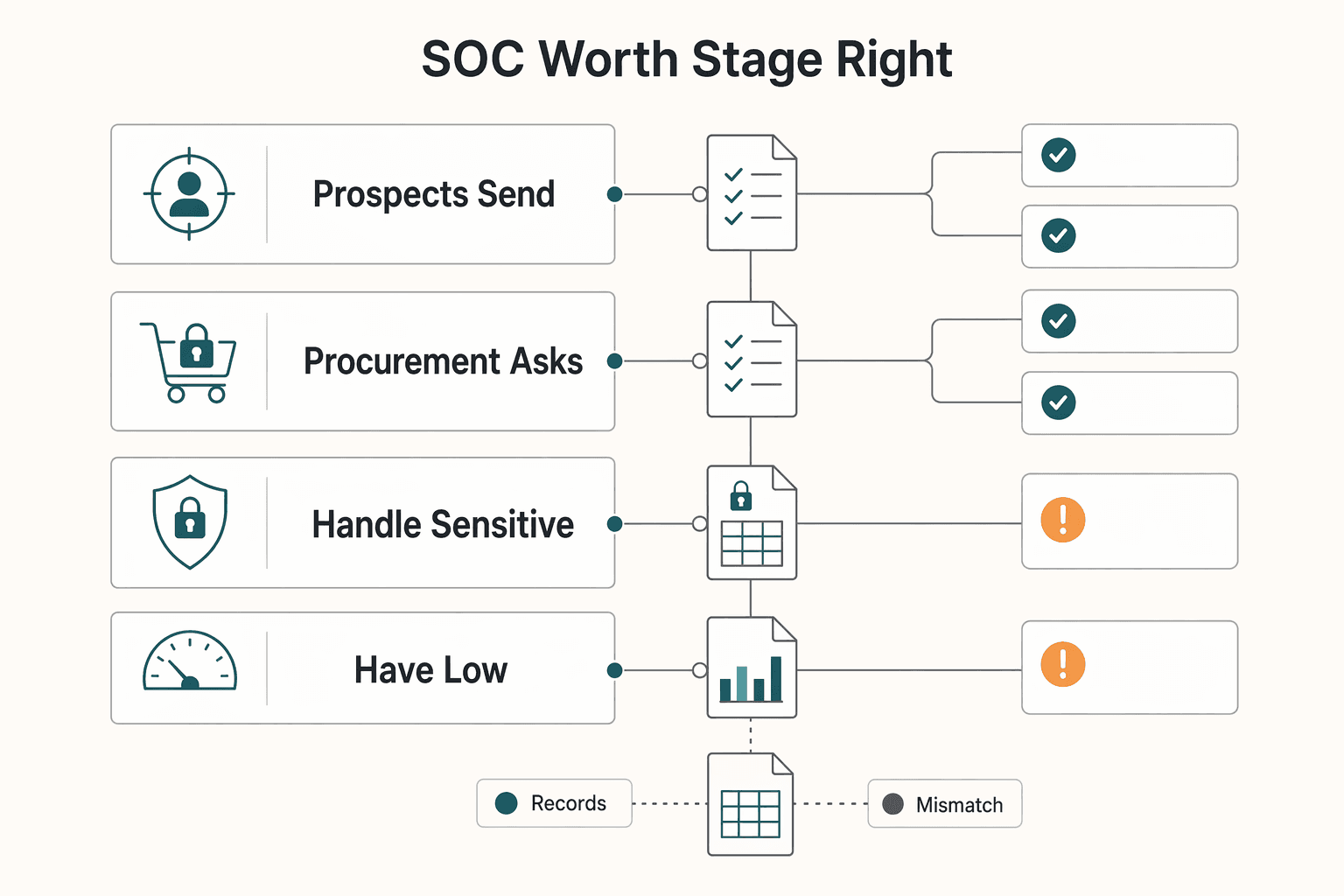

Is SOC 2 Worth It for Your Stage Right Now?#

SOC 2 is worth starting now when buyer demand and security risk outweigh your team's ability to absorb procurement friction. With an operating model in hand, make this a stage decision, not a fear response. SOC 2 timing is a business choice tied to risk, market access, and your ability to run controls consistently.

A SOC 2 report gives buyers an independent auditor attestation on how your controls operate. Law does not require SOC 2 for every SaaS company, but many customers still ask for it before they sign. If your pipeline already includes security review gates, waiting often turns into avoidable drag during trust checks.

| Decision signal | What it tells you | Practical move |

|---|---|---|

| Prospects send security questionnaires early | Buyer diligence already drives your sales cycle | Start now and map answers to SOC 2 controls |

| Procurement asks for a SOC 2 report | Market access risk is immediate | Prioritize readiness and plan your audit path |

| You handle sensitive customer data | Data security gaps can create outsized downside | Accelerate core controls and evidence collection |

| You have low enterprise pressure and thin bandwidth | You may burn resources too early | Defer full audit, but build foundational controls now |

Treat sales acceleration as possible, not guaranteed. Stronger compliance signals can increase trust, but no single outcome applies to every stage.

Plan conservatively. Preparation and completion can take over a year in some cases. A Type 2 review usually examines control performance over a multi-month period, often 3 to 12 months.

Run this start now or defer checklist#

| Situation | Default action |

|---|---|

| Active deals require SOC 2 evidence | Start now |

| Security questionnaires repeatedly block legal or procurement progress | Start now |

| Customer demand stays low but you can still assign control owners and collect evidence | Defer with intent |

| You cannot sustain control cadence yet | Defer only briefly, then set a clear restart date |

If you're selling to larger teams, the goal is not to promise instant revenue lift. It is to show disciplined controls, answer security audit questions quickly, and remove uncertainty step by step.

Rule of thumb: start SOC 2 when commercial pressure and risk exposure outgrow your current operating proof.

What Should You Do in the First 90 Days of SOC 2 Work?#

Use the first 90 days as a practical sequencing window: lock scope, operationalize controls, and build evidence an independent third-party examination can test clearly. Once you decide to start, treat this period as setup for a system you can keep running, not a universal clock for every team. The objective is to support trust with operational proof, not create paperwork theater.

SOC 2 can cover controls relevant to security, availability, processing integrity, confidentiality, and privacy, and organizations use SOC 2 reports when they need detailed assurance information. Start with scope before anything else. If you skip scope, your control list drifts, your evidence gets noisy, and compliance starts competing with product delivery.

| Phase | Primary objective | What good output looks like |

|---|---|---|

| Scope first | Define scope and a minimum control set mapped to the Trust Services Criteria (TSC) in scope | Named in-scope services, systems, and data flows, plus a control baseline tied to real SaaS workflows |

| Build operating rhythm | Assign owners and launch recurring evidence collection for in-scope controls | Each control has an owner, cadence, and artifact location with time-stamped proof |

| Readiness review | Run readiness checks against SOC 2 expectations and patch weak execution | Gap log with severity, remediation owner, and target fix date |

| Audit preparation | Package a clean trail for external review | Artifact index, control narratives, and exception history ready for walkthroughs |

Use readiness to pressure-test operations, not to declare victory. A Type I lens checks control design at a point in time. A Type II lens checks operating effectiveness over time. If you plan for Type II later, collect evidence now in a repeatable rhythm so you do not rebuild the trail from scratch.

Safe default checklist for constrained teams#

| Action | Included detail |

|---|---|

| Lock scope in one page | Systems, boundaries, and exclusions |

| Map controls | TSC priorities in your scope |

| Assign one accountable owner | Per control |

| Set one evidence cadence | Your team can sustain |

| Keep a live gap log | Remediation dates |

On a lean SaaS team preparing for a customer security request, you should be able to open one tracker, show who runs each control, and produce current evidence quickly. Working rule: if a control lacks an owner, cadence, or proof, treat it as not implemented yet.

How Do You Build Audit Ready Evidence Without Slowing Product Delivery?#

Build a lean evidence rhythm where each SOC 2 control has an owner, a recurring proof package, and a direct link to day-to-day delivery work. A practical plan only works if evidence collection does not hijack your shipping cadence. The core of SOC 2 is simple: collect verifiable evidence on a recurring basis so compliance and delivery stay aligned.

Treat evidence as operational proof. A SOC 2 Type 2 review evaluates control design and operating effectiveness over time. It typically spans a 3 to 12 month window, so one-time cleanup will not hold up. Type 2 also demands more coordination and evidence than Type 1, so your process must be simple enough for a real team to run every cycle.

| SOC 2 controls area | Recurring proof package (safe default) | Owner check before review |

|---|---|---|

| Security and access | Access review records, approval logs, exception notes | Confirm completeness and unresolved gaps |

| Availability controls | Incident records, change logs, recovery follow-through | Confirm controls ran in normal operations |

| Data protection | Data handling records, retention or deletion evidence, linked tickets | Confirm traceability from policy to execution |

| Change management | Release approvals, testing traces, rollback records | Confirm artifacts match shipped changes |

Use a lightweight dashboard to keep the system honest and fast:

- Control status by owner.

- Missing artifacts by control area.

- Open exceptions with target remediation dates.

- Links to current proof packages for SOC 2 report review.

- Business tags such as "security questionnaire," "procurement," or "renewal" to connect evidence work to buyer-risk conversations.

In an enterprise deal cycle, you should not need to pull engineers into a week of ad hoc evidence hunts. Export the latest package, answer the security audit questions, and flag one open exception with a clear fix date. That does not guarantee sales acceleration, but it can reduce procurement friction and preserve momentum.

Working rule: if evidence does not help an auditor verify control operation and does not help your team run better, do not collect it.

Where Do Requirements Vary and How Do You Confirm Safely?#

Treat AICPA and Trust Services Criteria as fixed guardrails, then validate implementation choices with your auditor before fieldwork. Once the evidence rhythm is running, the remaining risk is interpretation. Teams can still create deficiencies by making silent assumptions about scope, control intent, or evidence packaging, so a simple confirm loop is worth it.

Separate fixed rules from design choices#

In a SaaS SOC 2 program, some elements are fixed. AICPA criteria anchor what your system description must cover, and the Trust Services Criteria define the control lens. Your team still chooses scope and control design based on your product, data security flows, and risk profile.

| Fixed framework elements | Business specific choices |

|---|---|

| Use AICPA description criteria for the system narrative | Define which systems, teams, and workflows enter SOC 2 scope |

| Map controls to relevant Trust Services Criteria categories | Select which trust services categories your report includes |

| Present clear control intent and operating evidence | Choose tools, workflows, and owner cadence that prove execution |

The criteria provide a shared baseline, but implementation still depends on your operating model, compliance priorities, and customer expectations.

Run a safe confirm loop before fieldwork#

Use one loop for every scope or control decision in your security audit prep:

- Document the assumption in plain language.

- Validate the assumption with your auditor.

- Update the control narrative and owner instructions.

- Test evidence quality against real artifacts before fieldwork starts.

If you sell one product in several regions and a new enterprise buyer asks deeper trust questions, keep the framework but tighten the evidence and narrative for that segment instead of rewriting your whole program.

If you operate across countries or regulated segments, treat obligations as variable inputs. GDPR can apply even when your company sits outside the EU if you offer services to EU individuals or monitor behavior there. HIPAA duties apply to covered entities and can add mandatory requirements in regulated healthcare contexts. SOC 2 supports readiness, but it does not replace those legal obligations.

When you communicate externally, stay precise: coverage varies by market/program. That keeps claims accurate when control environments differ by product or geography.

Run the Framework and Build Trust You Can Prove#

Run SOC 2 as a system: define scope, operate controls, and communicate results with precision. By this point, you have the pieces. The win is not memorizing terminology. It is running a program that produces audit-ready evidence and clear buyer answers while keeping delivery moving.

The 2017 Trust Services Criteria give your team the lens for security, availability, processing integrity, confidentiality, and privacy. An independent third-party examination evaluates how your controls work, then produces your SOC 2 report. Type I shows control design at a point in time. Type II evaluates design plus operating effectiveness over a period of time. That distinction should shape how you speak about your compliance posture.

Execute the next checkpoint#

| Decision area | Safe default action | Output you should have |

|---|---|---|

| Scope | Finalize in-scope systems, data flows, and owners | Signed scope record and control map |

| Control operations | Run recurring evidence cadence for security controls and related criteria | Dated artifacts linked to each control |

| Readiness | Schedule a pre-audit validation pass | Gap log with owners and remediation dates |

| Buyer communication | Define approved language for security audit responses | Reusable response pack aligned to your SOC 2 report |

Working rule: if a control lacks clear owner accountability or auditable evidence, fix that before you expand scope.

If a prospect asks for proof during procurement, route the request through your formal channel, share the right report through your confidentiality process, and use authenticated access and NDA controls when required.

Communicate trust with disciplined claims#

Keep external messaging precise. Say you completed a SOC 2 examination and specify Type I or Type II correctly. Do not overstate coverage or scope. If you need a public-facing trust artifact, use SOC 3 language as a high-level companion to your SOC 2 materials.

| Artifact | What it shows | Use note |

|---|---|---|

| Type I | Control design at a point in time | Specify Type I correctly |

| Type II | Design plus operating effectiveness over a period of time | Specify Type II correctly |

| SOC 3 | High-level companion to your SOC 2 materials | Use as a public-facing trust artifact |

If you want compliance-first financial workflows with audit-ready records, request access or talk to sales to confirm coverage for your use case.

You might also find this useful: The Best High-Interest Checking Accounts for Freelancers.

Frequently Asked Questions

What does SOC 2 compliance for SaaS actually mean?

SOC 2 compliance for SaaS means you run defined controls and an independent CPA firm examines them against Trust Services Criteria. The output is a SOC 2 report about your controls for security, availability, processing integrity, confidentiality, or privacy. It is not a self-declared label.

Why do SaaS companies pursue SOC 2 in the first place?

Many teams pursue SOC 2 because customers and stakeholders use it as a trust signal. It helps you show disciplined security and risk management practices. Market pressure usually drives this decision more than a universal legal requirement.

Is SOC 2 worth the cost for a small or independent operator?

No universal cost or ROI rule fits every SaaS business. Use a practical trigger: start when customer diligence, trust expectations, or risk exposure creates real friction. If those pressures stay low, keep building your control foundation and time the audit when demand becomes clear.

What should a SaaS team prepare before a SOC 2 audit?

Define scope first. Select your Trust Services Criteria scope, and include Security as the baseline. Then implement internal controls aligned with that scope before the third-party audit begins.

What are Trust Services Criteria and Common Criteria in practice?

Trust Services Criteria give you the categories your audit can cover: Security, Availability, Processing Integrity, Confidentiality, and Privacy. In practice, Security serves as the required baseline, and management can select additional criteria as appropriate. Common Criteria are treated as the baseline expectations within that Security scope.

What is the difference between SOC 2 controls and a SOC 2 report?

SOC 2 controls are your day-to-day operational practices. A SOC 2 report is the auditor’s attestation output on those controls. Think execution versus the formal report that documents what was examined.

How should we talk about SOC 2 publicly without overclaiming?

Say you completed a SOC 2 attestation and mirror your SOC 2 report language accurately. Do not say "SOC 2 certified," because SOC 2 uses attestation, not certification. If you hold Type I only, describe it as a point-in-time result. Reserve ongoing effectiveness claims for Type II coverage over its audit period.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- commission.europa.eu/law/law-topic/data-protection/rules-business...trusted

- hhs.gov/hipaa/for-professionals/covered-entities/ind...trusted

- cobalt.io/learning-center/soc-2-compliance-for-saasexternal

- isc2.org/Insights/2026/01/reframing-security-as-a-tru...external

- isms.online/soc-2/controls/audit-ready-evidence-how-to-d...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

Working Remotely in Latin America Without Visa Guesswork

Treat this move as a verification project, not a booking sprint. If you are planning a remote-work move in Latin America, the first practical step is to separate what is clearly supported now from what still needs direct government confirmation before you spend money or lock dates.

The Best High-Interest Checking Accounts for Freelancers

Stop optimizing for the highest advertised rate. Optimize for net yield plus predictable money movement, because that is what keeps your freelance cashflow stable. If you run a business-of-one, treat checking like your cashflow control panel, not an investment product. Once checking becomes a system, you can choose a setup that survives late invoices, odd payout timing, and vendor auto-bills. Then interest becomes a bonus instead of a trap.