Quick Answer

Canadians can set up a U.S. LLC, but they should choose the entity and state only after mapping where work happens and confirming cross-border tax treatment. The main risk is a Canada-U.S. classification mismatch that can create double-tax exposure, while federal treaty relief may not eliminate separate state obligations. Form first, then sequence banking, bookkeeping, BOI reporting, and recurring compliance reviews.

Before You Form a US LLC From Canada#

If you are considering a U.S. LLC as a Canadian, decide structure before you form anything. That one sequencing choice keeps tax and compliance decisions deliberate instead of reactive.

A U.S. Limited Liability Company (LLC) is a business structure in the United States. A non-resident U.S. LLC means the owner is outside the U.S., which raises cross-border considerations in Canada and the U.S.

Treaty context belongs at setup, not after problems appear. Article XXVI-A of the Canada-US tax treaty addresses collection assistance, and a U.S. Tax Court record filed in 2024 notes the CRA sent the IRS a mutual collection assistance request in 2017. The practical takeaway is straightforward: cross-border obligations can connect, so your records and filing posture need to work on both sides from the start.

Source quality matters here. Some public pages are useful summaries, but they are not legal authority. FederalRegister.gov prototype pages do not replace official editions. IRS Internal Revenue Bulletin synopses are reader aids, not authoritative interpretations. When a claim affects filings, money movement, or eligibility, confirm it against primary documents and advice tied to your province and U.S. state activity.

Start with a short operating brief before you spend on formation:

- Your business goal for the next 12 months.

- Where work is performed and managed by province and by U.S. state.

- Which contracts, clients, or payment rails require a U.S. entity now.

- Which assumptions need advisor confirmation before filing.

Use this guide in order:

- Confirm your near-term business goal.

- Map where activity actually happens.

- Validate treaty position and filing exposure with cross-border tax advice.

- Form only after those checks, then sequence banking, bookkeeping, and compliance.

The objective is durable operations, clean records, and fewer cross-border surprises. Keep decisions tied to your province, your state activity, and any program eligibility you care about.

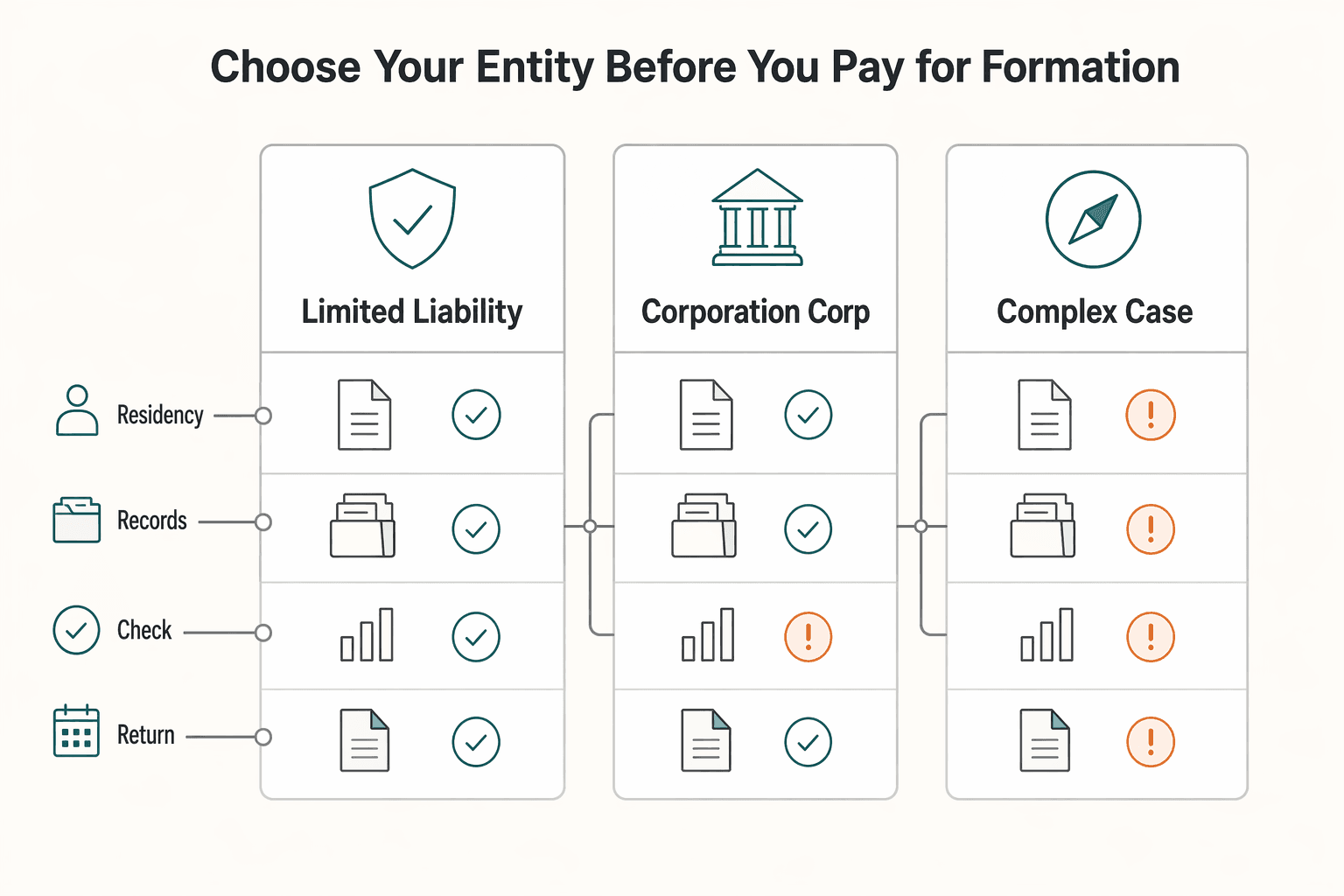

Choose your entity before you pay for formation#

Choose structure before you buy formation services. First decide whether you need a U.S. entity now or only after your next operating milestone. Use this as a screening tool, not a final tax or legal ruling.

| Path | Best near-term fit | What to validate first | Main risk if rushed |

|---|---|---|---|

| U.S. Limited Liability Company (LLC), including a non-resident U.S. LLC | You are considering a U.S. entity now | LLCs are commonly described as pass-through, but cross-border treatment can differ | CRA and IRS treatment differences can increase double-tax exposure |

| C corporation (C-Corp) | Possible alternative structure | This section does not provide enough evidence to determine fit | Paying for a structure before confirming fit |

| Sole proprietorship or partnership without a U.S. entity yet | Possible interim path | This section does not provide enough evidence to determine fit | Possible rework later if U.S. activity expands |

If you are still deciding whether to form now, compare your path against Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers and test the same facts against your own client pipeline.

Use decision rules before any formation spend:

- If you need a U.S. entity now, compare state filing fees and ongoing costs before filing.

- For entity comparisons beyond LLC setup steps, get cross-border legal and tax advice before filing.

Add one pre-filing checkpoint memo so you can defend the choice:

- Business objective for the coming year.

- Why this entity supports that objective.

- What was rejected and why.

- What would trigger reconsideration.

After the entity choice is clear, run setup in sequence. Choose a state, compare filing fees and ongoing costs, and file articles of organization. Then create an operating agreement, appoint a registered agent, and apply for an EIN.

If you use a formation vendor, keep responsibilities clear: the vendor handles paperwork, your advisor handles tax position, and you own the records and deadlines.

Understand the cross-border tax mismatch before filing#

Before you file, confirm how each country classifies the same LLC. In the U.S., an LLC is generally treated as a flow-through entity, with profits and losses passing to members. In Canada, CRA generally treats that same U.S. LLC as a corporation for tax purposes.

| Memo item | Why it matters |

|---|---|

| U.S. treatment assumptions and CRA treatment assumptions | Confirm how each country classifies the same LLC |

| Recognition timing differences | Timing differences can affect when foreign tax credits are available |

| Foreign tax credit limits | The same income can be taxed twice if credits are not available when expected |

| Expected treaty relief | Treaty relief may help, but relief can remain partial when classification mismatch drives the result |

| Go or no-go recommendation | Tie the recommendation to the stated assumptions before filing |

That split can create double-tax exposure even when the setup looks efficient on one side. Timing differences matter. If income recognition does not line up, foreign tax credits may not be available when expected, and the same income can be taxed twice.

Treaty relief is a checkpoint, not a blanket fix. The Canada-U.S. Tax Treaty may help in some cases, but relief can remain partial when classification mismatch drives the result. This is where half-correct advice gets expensive: the right rule, applied in the wrong order, can still produce the wrong outcome.

Ask your advisor for one written checkpoint memo before filing:

- U.S. treatment assumptions and CRA treatment assumptions.

- Where recognition timing differs.

- Where foreign tax credit limits may appear.

- Where treaty relief is expected to help and where it may stay partial.

- A clear go or no-go recommendation tied to those assumptions.

Push for plain language in that memo. If you cannot explain one income stream cleanly across both countries, pause and fix the structure first. Fast formation is easy. Fixing a mismatch later is usually slower and more expensive.

Separate federal tax from state tax obligations#

Treat federal and state tax as separate tracks. A clean U.S. federal position does not remove state obligations.

| Bucket | Core question | Why it matters |

|---|---|---|

| U.S. federal tax | How is the entity and owner income treated federally? | It sets federal filing posture, but does not clear state duties |

| State tax | Did your activity create duties in a specific state? | State income tax and sales/use tax can apply independently |

California is a useful example. The Franchise Tax Board (FTB) states that nonresidents pay tax on taxable income from California sources, including income from a California business, trade, or profession. For part-year residents, California treatment can include worldwide income during resident periods and California-source income during nonresident periods.

Residency is fact-specific. FTB guidance says residency is determined from all facts and circumstances, and FTB does not issue written opinions confirming residency for a specific period. That puts pressure on your documentation. Build and maintain your own support file for the position you take.

Operational changes should trigger an immediate state review. If your in-state or out-of-state activity shifts, review state tax exposure right away instead of assuming no office means no exposure.

Use one quarterly checkpoint memo:

- List each state where you had customers, inventory, or service activity.

- Flag possible state income-tax and sales/use-tax exposure for each state.

- For California activity, document residency facts separately from California-source income facts.

- Note whether part-year or nonresident return treatment applies, including the effective tax rate method when relevant.

- Log annual California filing-threshold checks by tax year against current FTB tables.

Keep this memo short and repeatable. One page each quarter is better than a long year-end reconstruction from memory. The goal is consistency: same fields, same definitions, same evidence standard each cycle.

Pick a state and formation stack with eyes open#

Choose a state you can justify in writing based on your real activity, not on branding or speed claims. Use this filter before filing.

| Decision lens | What to test | Practical implication |

|---|---|---|

| Operating footprint | Where your work is performed and managed | Real activity pattern should drive the decision memo |

| State-specific access limits | Whether state law limits who can build, own, or operate assets in your sector | State rules can narrow market access; a 2019 Texas law tied some new transmission-line rights to owners of existing facilities |

| Wyoming LLC question | Whether a Wyoming filing matches your real operating plan | Treat it as an option to test, not a default answer |

| Year-one admin capacity | Your ability to keep records, renewals, and notices current | Pick a setup you can maintain consistently |

After choosing a state, keep your formation documentation clean: filing records, internal governance documents, and a post-formation admin calendar.

For execution, assign an owner and a proof item for each setup task:

- Filing confirmations and key records.

- Bank and payment account setup with matching legal details.

- Bookkeeping category map for income, expenses, owner draws, and reimbursements.

- Calendar entries for renewals, notices, and tax checkpoints.

DIY can work if your structure is straightforward and you can keep deadlines. If you use a filing service, treat it as paperwork support. Tax decisions still belong with a qualified advisor.

A simple rule helps here: if you cannot explain your state choice in three clear sentences tied to actual operations, you are not ready to file yet.

Execute a first 90 days checklist in the right order#

In the first 90 days, keep the sequence simple: lock legal identity, activate money operations, review tax triggers based on real activity, then set recurring controls. This order keeps later steps tied to clean earlier records.

| Window | Primary focus | Examples in the section |

|---|---|---|

| Week 1-2 | Close legal setup and verify core identifiers | Formation records, registered agent details, EIN confirmation, BOI reporting |

| Week 3-6 | Activate money rails and classify transactions early | U.S. banking and payment rails, invoice categories, separate owner and business transactions |

| Week 7-10 | Run first U.S. federal tax and state trigger review | Review where work was performed, where services were delivered, and where customers are located |

| Week 11-13 | Reconcile and lock recurring compliance dates | Reconcile books, confirm owner draws or payroll treatment, lock a recurring compliance calendar |

Week 1-2 close legal setup and verify core identifiers#

Where applicable, complete formation records, confirm registered agent details, and track your Employer Identification Number (EIN) application through confirmation. How and where you need to register depends on your business structure and business location, and in some cases you may not need to register at all. Keep one canonical record for your legal name, formation state, and mailing details, then reuse those exact values across filings and accounts.

Add BOI reporting in this same step. BOI reporting is handled through FinCEN under the Corporate Transparency Act of 2021, and it is generally not annual. Treat it as an initial filing plus updates or corrections when information changes. If timeline guidance conflicts across sources, verify current filing timing before submission.

Practical checks for this phase:

- Confirm legal name formatting is identical across state filing, EIN record, and bank onboarding.

- Store acceptance notices in one location with date and version.

- Record who is responsible for BOI updates and how changes are escalated.

- Capture one internal note describing what was filed and what still depends on confirmation.

Week 3-6 activate money rails and classify transactions early#

Bring U.S. banking and payment rails live only after your identifiers match. That reduces downstream friction in payouts, tax forms, and reconciliations.

Define invoice and transaction categories now. Doing it early reduces cleanup work later and improves visibility as activity grows.

Keep owner and business transactions separate from day one. That supports the LLC boundary between personal assets and business finances and can simplify recordkeeping when questions arise.

Practical checks for this phase:

- Use one invoice template with consistent payer fields.

- Require memo lines for transfers that could otherwise look personal.

- Document approval steps for payouts and owner draws.

- Run a weekly reconciliation cadence until transaction volume is stable.

Week 7-10 run first U.S. federal tax and state trigger review#

Run your first tax trigger review against actual operations, not formation-day assumptions. Registration and filing expectations vary by structure and location, so review where work was performed, where services were delivered, and where customers are located.

Document potential triggers, decisions, and owner actions in a short memo. Even a no-change result should go in the file so you can show the review happened.

Practical checks for this phase:

- Compare original assumptions to live activity.

- Flag any new state touchpoints and assign follow-up.

- Record open questions for advisor review with target dates.

- Mark uncertain classifications as pending rather than final.

Week 11-13 reconcile and lock recurring compliance dates#

Reconcile the books, confirm owner draws or payroll treatment is applied consistently, and lock a recurring compliance calendar. Each obligation should have an owner, due date, and proof item, including BOI update checks when beneficial ownership information changes and recurring federal and state review dates.

Practical checks for this phase:

- Verify calendar reminders exist in more than one place.

- Confirm proof items are specific enough to survive turnover.

- Close or escalate unresolved items before the next quarter begins.

- Archive the first 90-day checklist as your baseline for future cycles.

A clean first quarter gives you a repeatable pattern. The immediate benefit is fewer avoidable filing surprises. The longer-term benefit is faster reviews because your records already show sequence, ownership, and evidence.

Build money operations that are audit-ready from day one#

Audit-ready money operations start with one traceable path from invoice to payout to reconciliation. If someone asks what happened, your records should answer with dates, approvals, and supporting documents.

Build one traceable money path#

Use one path for every transaction: invoice issued, cash received, payout approved, ledger posted, reconciliation completed. Keep statuses fixed and date-stamped so timing is clear and versions do not conflict during tax prep.

For cross-border activity, keep records in one source of truth, not in side trackers. Update transaction tags when U.S. customer activity changes, because the U.S. trade-or-business threshold can be relatively low and activity at any point in the year can matter for U.S. tax treatment.

A practical implementation pattern:

- Lock status names so team members do not invent new labels.

- Require a document link before a transaction can move to final status.

- Capture who approved each payout and when.

- Reconcile to bank statements on a defined cadence.

Keep books and records as your source of truth#

Treat your ledger as the primary record and link supporting evidence to each material movement. This reduces filing friction and improves your position if activity is reviewed later.

Books and records are a recognized audit focus area. Use older IRS audit technique material as an examination lens, not as current law, and resolve conflicts with current guidance before filing.

Two habits make this practical:

- Record decision notes at the time of classification, not after quarter end.

- Preserve the evidence version used at the time of decision.

Add a pre-close cross-border verification checkpoint#

Before period close, run a short completeness check:

- Payer details are complete and consistent across invoice, bank record, and ledger.

- Payee details match your legal entity records.

- Jurisdiction notes are complete for where services were delivered and managed, when relevant.

- Material transactions are linked to supporting documents and close status.

If critical information is missing, hold final classification until corrected. Filing obligations may still apply even when no final U.S. tax is due, so keep this checkpoint short and strict to block avoidable errors before they enter filed documents.

Validate platform controls before you depend on them#

If billing, payments, and accounting are split across tools, test compliance gates and audit exports early. Confirm exports preserve timestamps, status history, and document links so your records remain usable when filing questions arise.

Run a sample export and test it end to end:

- Can you tie one invoice to one payment and one ledger entry?

- Are edits traceable with date and user context?

- Are document links preserved after export?

- Can someone else reproduce your result from the export package alone?

If any answer is no, fix the control gap before relying on the platform during filing season.

Create a compliance and tax evidence pack you update continuously#

A clean ledger is necessary but not sufficient. You also need a living evidence pack that shows why each filing position is supportable. Update it at every close so decisions stay tied to records instead of memory.

Define the minimum pack before adding edge cases#

Start with four folders and keep them current:

| Folder | What it holds |

|---|---|

| Entity records | Formation and governing records, plus current ownership details |

| Owner records | Identity and tax-status documents used for owner-level reporting positions |

| Tax profile data | Current filing profile, reporting assumptions, and period notes on changes |

| Cross-border transaction support | Reconciled statements and invoice-to-payment support for material transactions |

Keep filing evidence separate from general reference notes so reviews stay focused and advisor requests can be answered without reconstructing context.

Add one cover page for each close period:

- What changed this period.

- Which assumptions stayed the same.

- Which items are pending resolution.

- Who approved the close package.

Add FATCA, Form 8938, FBAR, and FinCEN checkpoints#

Run the same checkpoint review each period.

| Checkpoint | What to test | Evidence to retain |

|---|---|---|

| Form 8938 applicability | Whether specified foreign financial assets exceed the applicable threshold for the filer | Threshold test worksheet and asset snapshot |

| Form 8938 filing method | If required, confirm Form 8938 is attached to the income tax return | Return package copy showing the attachment |

| FBAR (FinCEN Form 114) | Whether a separate FBAR filing duty exists even if Form 8938 is filed | Determination memo and filing confirmation, when applicable |

| FATCA scope | Whether assets fall within reportable specified foreign financial asset categories for the filer | Asset classification notes and supporting account records |

Document threshold logic clearly. Form 8938 thresholds vary by filer type, and filing Form 8938 does not replace separate FBAR obligations when FBAR is otherwise required. If a taxpayer is not required to file an income tax return for the year, Form 8938 is generally not required.

Flag owner-level filing-position changes without guessing#

Maintain an owner-level risk flag for changes in filing positions where relevant. If ownership facts, entity status, or foreign-asset records change, open a review item and record the final determination in writing.

Avoid informal assumptions such as it looked similar last year. Filing facts can shift quietly over a year, and that shift can affect filing posture.

Enforce a no-orphan-data rule#

Set one hard rule: every filing position must map to traceable records and reconciled statements. If a position cannot be tied to a document trail, mark it unresolved before final filing decisions so advisor review stays fast and year-end close remains confirmation rather than reconstruction.

Watch for trigger events that change your risk profile#

Treat trigger events as mandatory review points. When core inputs change, update compliance positions from current records, not old assumptions.

Common trigger events:

- Capital, ownership, or payout-pattern changes.

- Changes in ownership or control that may affect beneficial ownership information on file.

- New or revised agency guidance or orders you rely on.

Each trigger should produce a dated review memo with three parts:

- What changed and when.

- Which filings or determinations may be affected.

- What immediate actions were taken.

Any change in ownership or control should also trigger a banking compliance check. Under FinCEN's CDD Rule, covered financial institutions must identify and verify beneficial owners of legal entity customers. Confirm your bank's update requirements and retain its acknowledgment.

Use FederalRegister.gov to monitor developments, but do not treat its XML rendition as legal notice on its own. For legal research, verify against an official edition and save the version you relied on. Apply that same check when guidance shifts, including FinCEN's exceptive-relief order dated February 13, 2026. Trigger reviews should happen when facts change, not only when deadlines approach.

Run a 12-month compliance cadence you can sustain#

A sustainable annual cadence is a loop: monthly record quality, quarterly tax review, annual filing checks. Keep it small enough that you will actually maintain it during busy periods.

| Cadence | Core check | Evidence to keep |

|---|---|---|

| Monthly | Close books, validate transaction tags, and review new activity for possible compliance impact | Close report, tag exception log, activity notes |

| Quarterly | Re-run tax estimates, then confirm assumptions still match operations | Estimate worksheet, assumption memo, owner checkpoint notes |

| Annual | Complete entity renewals and state reports, then test Form 8938 and FBAR applicability separately | Renewal receipts, return package, foreign-asset test worksheet |

Use the annual foreign-asset checkpoint as a formal decision, not a quick scan. Form 8938 applies when specified foreign financial assets exceed the applicable threshold, and thresholds vary by filer status. IRS guidance cites a $50,000 aggregate-value threshold in some cases, with higher thresholds for joint filers or taxpayers residing abroad. When required, Form 8938 must be attached to the annual income tax return. For tax years beginning after December 31, 2015, certain specified domestic entities, including domestic corporations closely held by a specified individual, can also be in scope for Form 8938.

Keep FBAR as a separate annual check. Filing Form 8938 does not remove a separate FinCEN Form 114 requirement when FBAR filing is otherwise required. Treat them as two distinct determinations each year and store both in the same evidence pack.

Add one owner checkpoint each quarter to confirm the structure still fits your growth plans and cross-border complexity. If anything is unclear, open a dated review item that quarter instead of waiting for year-end filing season.

A cadence only works when it survives real workload. If you miss a checkpoint, log the miss, complete the review, and adjust the schedule so it does not repeat.

Conclusion#

Structure first, execution second. Fast filing alone is not risk control.

Before paying for setup, complete two working documents: a go or no-go decision table and an implementation checklist with owners and deadlines. Those two documents give you a baseline you can recheck whenever operating facts change.

Use this verification habit for every material compliance decision:

- Treat FederalRegister.gov web pages as informational, not final legal authority. The site states its web version is a prototype, not the official legal edition, and its XML does not provide legal or judicial notice.

- Verify legal text against an official Federal Register edition, and save the exact edition and reference you relied on.

- Track federal filing status early. The IRS Internal Revenue Manual includes a section titled

Business Master File (BMF) Return Delinquency, which is a practical reminder to treat delinquency risk as active, not background admin.

At execution time, revalidate jurisdiction and program-specific requirements before you act. If anything is unclear, pause, log the open issue, and resolve it before you move money or sign commitments. Review tools only after you confirm traceable records and fit for your market or program.

Frequently Asked Questions

Can a Canadian legally own a U.S. LLC?

Yes. Non-U.S. residents can generally form and own a U.S. LLC without U.S. citizenship or a green card, although foreign ownership does not make reporting simple. S-corporations are commonly cited as a key exception. Keep ownership, tax profile, and filing obligations documented from the start.

Why can a U.S. LLC create double taxation risk for Canadians?

Because the same entity can be classified differently in each country. A single-member LLC is commonly treated as a disregarded entity in U.S. tax treatment, and LLC income is often treated as pass-through, while Canadian treatment may not align. That mismatch can cause the same profit to be taxed in both countries, with treaty credits offering only partial relief in some cases.

Does the Canada-US Tax Treaty remove all U.S. tax obligations?

No. Treaty relief can help in some cases, but credits may provide only partial relief when a classification mismatch drives the result. Federal and state obligations still need separate testing. Treaty analysis should be part of formation planning, not an emergency fix.

When is a C-Corp a better choice than an LLC for a Canadian founder?

A C-Corp can be worth evaluating when early planning shows recurring LLC mismatch risk. The article notes U.S. C-corps may reduce double-tax outcomes in some cross-border structures if planned early. Test that choice against your expected income pattern, retained earnings plan, and state exposure.

Is a Wyoming LLC automatically the best option for Canadians?

No. A Wyoming filing does not override tax exposure where business activity actually occurs. Choose a state based on your operating reality and your ability to maintain compliance records, not on one-state marketing claims.

Do I still owe state tax if I qualify for treaty relief at the federal level?

You may. Federal treaty relief may not eliminate separate state filing and tax duties, so state compliance should be treated as its own determination if activity creates state nexus. Build quarterly state reviews into your calendar so it does not become a year-end surprise.

Are LegalZoom or ZenBusiness enough for cross-border compliance?

Not on their own. They can help with formation paperwork, but they do not replace cross-border tax analysis, classification decisions, or annual filing controls. Use them for administrative execution and keep structure and filing posture decisions with qualified cross-border advisors.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.