Quick Answer

Selling your freelance business means proving a buyer can verify, transfer, and run the operation without founder-dependent chaos. Build a sellability-to-close workflow: score readiness, fix legal and operational gaps, prepare your due diligence packet before outreach, align major terms in an LOI, and run hard go or no-go gates through contract review, compliance checks, and handoff rehearsal.

You are not selling freelance labor you are selling a reliable asset#

When you sell your freelance business, buyers are paying for a reliable asset they can verify, transfer, and run, not for your personal hustle. A common mistake is mixing advice about winning clients with advice about closing an acquisition. Those are different jobs. This guide is a sellability-to-close playbook designed to reduce surprises before buyer conversations begin.

Even if you run a business-of-one, the sale only works if the business can keep operating when you step back.

If you run an agency, think like an operator preparing an ownership transfer. You are building an exit strategy, not pitching another service package. Buyers want evidence they can trust: clean records, clear contracts, repeatable delivery, and low owner dependency. A strong narrative helps, but operating discipline carries the deal once scrutiny rises.

| If you act like you are selling labor | If you act like you are selling an asset |

|---|---|

| Lead with your personal skill and availability | Lead with systems, contracts, and transfer readiness |

| Promise custom execution | Show repeatable operations and documented handoff steps |

| Treat diligence as paperwork at the end | Prepare Due Diligence materials before serious calls |

| Negotiate from confidence alone | Negotiate from verifiable risk controls and documented priorities |

Due Diligence is the investigation buyers run before closing. In many small business sale processes, buyers review four lanes: financial, legal, operational, and customer records. Organized records increase buyer confidence because you can answer hard questions quickly with evidence instead of explanations.

A focused prep pass should leave you with three practical outputs:

| Practical output | What it does |

|---|---|

| A working readiness scorecard for your business | Flags owner dependency, transfer risk, and documentation gaps |

| A Due Diligence packet checklist | You can assemble before sharing sensitive files |

| Your own decision gates | Tell you when to proceed, when to remediate, and when to pause |

What are you actually selling when you sell a freelance business?#

You are selling a transferable operating asset that a buyer can control and run, not just your personal freelance labor. Once you treat this as a transfer transaction, your next job is to define what the buyer actually acquires and how the transfer works. That is where the process stops being sales talk and starts being deal execution.

Use shared deal language early so both sides evaluate the same thing:

| Term | Plain meaning | Why it matters |

|---|---|---|

| Acquisition | A buyer purchases shares or assets of a business. | It sets the frame around control and transfer, not project work. |

| Exit Strategy | Your planned path to exit a business or investment position on acceptable terms. | It guides when to market, when to negotiate, and when to walk away. |

| Letter of Intent (LOI) | A usually non-binding preliminary document that aligns major commercial terms before full legal drafting. | It reduces confusion before legal detail expands. |

| Asset Purchase Agreement (APA) | The contract that states which assets transfer and which do not. | It defines deal scope precisely, including selective asset transfer where relevant. |

During due diligence, buyers test financial, legal, and operational evidence side by side. That is why transferability and low owner dependency can materially affect value and marketability. Documented delivery systems and solid contracts signal continuity beyond the founder.

Example: a buyer likes your client roster but worries every delivery decision still routes through you. Show a documented handoff process. Keep contract records current. Make ownership and transfer-rights status clear. That can reduce risk and help keep the deal moving.

Use this default before every buyer call. Treat it like a checklist, not a vibe test:

- Treat each claim as unproven until you can back it with a contract, a finance record, or an audit-ready operational log.

- State transfer scope in plain language first, then confirm it in the APA draft.

- Use the LOI to align major terms early, then tighten details in definitive agreements.

- Flag owner-dependent tasks and assign a replacement process before diligence deepens.

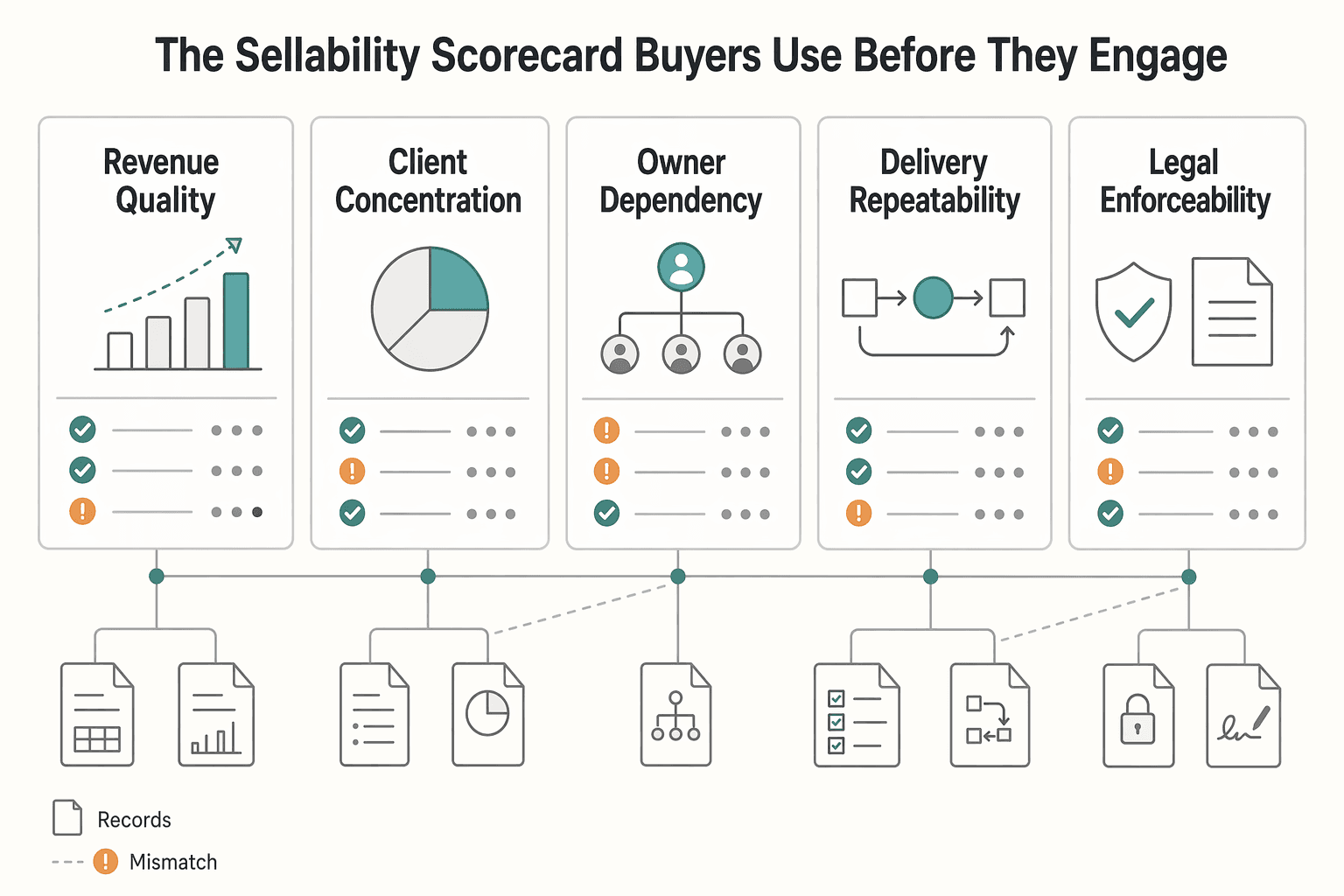

The sellability scorecard buyers use before they engage#

Use a weighted scorecard with hard pass or fail gates to decide whether buyers should engage now or after cleanup. Before buyer outreach, you need a filter that protects your timeline and leverage.

A scorecard helps you prioritize cleanup objectively and reduce late-stage surprises. Weak contracts often surface late in legal diligence and trigger buyer pullback. Build your scorecard around core diligence areas, including revenue quality, client concentration, owner dependency, delivery repeatability, and contract enforceability.

| Scorecard area | What to test | Pass gate example | Evidence artifact |

|---|---|---|---|

| Revenue quality | Stability of revenue and cash flow patterns | Trends look consistent and explainable | Monthly P&L, cash reports, renewal logs |

| Client Concentration | Revenue share tied to a small group of clients | Top 5 clients under 25 percent is one low concentration example, then adjust for your model | Client revenue mix by account |

| Owner dependency | How often the founder makes core decisions or handles delivery bottlenecks | Team or documented process can run key workflows | SOPs, delegation map, QA checklist |

| Delivery repeatability | Consistency of execution across engagements | Standardized intake, delivery, and handoff steps | Process docs, template SOWs, handoff records |

| Legal enforceability | Governing Law, Jurisdiction, and Arbitration language clarity, including whether forum wording is mandatory or permissive | Clauses stay consistent across core contracts | Master agreement clause matrix |

| Commercial downside control | Term and Termination rights and Limitation of Liability caps | Termination triggers read clearly and liability boundaries stay explicit | Redlined contract set, clause tracker |

When a gate fails, run a remediation sprint with dated actions. Do not write goals like "improve contracts." Write actions you can prove.

- Assign one owner to each weak gate and set a target completion date.

- Define the exact artifact that proves completion.

- Re-score the gate only after you collect the artifact.

- Keep a short decision log for issues that still affect business valuation.

Example: if one client drives most revenue and you still approve every deliverable, reduce that risk before buyer outreach by documenting approvals, redistributing client communication, and tightening contract terms so continuity does not depend on you.

How should you value the business and choose a deal structure?#

Treat Business Valuation as a negotiation range tied to risk, durability, and transferability, then choose the acquisition structure that best protects price and close certainty. Your scorecard shows where risk lives. Valuation and structure are where you turn that risk into terms a buyer can actually price.

Business Valuation produces a conclusion or calculated value. That output can be a single amount or a range. Use the willing buyer and willing seller frame, then pressure-test the range against diligence quality.

In practice, valuation starts the conversation. Better evidence and cleaner risk allocation can move the final number.

| Structure path | What transfers | Liability and scope impact | Typical negotiation effect |

|---|---|---|---|

| Asset acquisition via Asset Purchase Agreement | Selected business assets and defined rights | Buyer can select assets and negotiate which liabilities to assume | Can support cleaner risk boundaries when drafting stays precise |

| Stock acquisition | Equity ownership of the entity | Scope centers on control of the entity rather than selected assets | Can simplify transfer mechanics in some deals |

Legal protections directly shape pricing confidence. Indemnification allocates who pays if specific losses surface after close. Limitation of Liability sets a damages ceiling. When these clauses read clearly and align with your operating reality, buyers can price downside with more confidence.

Use these decision gates before you sign an LOI:

- Anchor your price ask to a valuation range, not one fixed headline number.

- Choose structure first, then draft scope and assumed liabilities in detail.

- Confirm whether the transfer is an applicable asset acquisition that triggers purchase-price allocation reporting and Form 8594 filing expectations for both sides.

- Tie every risk claim back to evidence from finance, contracts, and operations.

Example: two buyers offer similar headline value, but one asks for broad indemnification with weak liability caps. The safer deal may carry a slightly lower price, yet it protects your downside and raises close reliability.

For a deeper walkthrough, use How to Perform a Business Valuation for a Small Agency before final term negotiation.

Build your diligence packet before the first buyer call#

Build a buyer-ready diligence packet before outreach so you control what gets shared, when it gets shared, and how risk gets interpreted. As conversations get serious, buyers will test your core claims. This is where the process shifts from strategy into proof.

Use a practical sequence, not a universal legal rule. Start with a signed Non-Disclosure Agreement (NDA). Then prepare a draft Letter of Intent (LOI) template. After that, build an indexed Due Diligence folder.

The NDA creates a confidentiality gate before you release sensitive files. A draft LOI helps you align key terms before full diligence. That way, you avoid dumping documents with no deal frame.

| Packet component | What to include | Risk it reduces |

|---|---|---|

| NDA gate | Signed NDA and clear counterparty details | Uncontrolled disclosure of sensitive operating and client data |

| LOI prep | Your preferred LOI structure, deal assumptions, open points | Misalignment on major terms before deeper review |

| Due Diligence index | Indexed folder map for key business, legal, operational, and customer records | Slow responses, missed files, and inconsistent narratives |

| Contract and IP proof | Active Statement of Work (SOW) files, Work for Hire language status (where supported), written and signed Assignment of Rights records | Ownership uncertainty and transfer disputes |

| Risk disclosure logs | Known risk notes, exceptions, dependencies, and remediation status | Late surprises during confirmatory review |

Example: a buyer likes your growth story, then asks who owns key deliverables tied to active client work. You can answer in minutes because your SOW set is current, your Work for Hire status is explicit where supported, and your Assignment of Rights documents are already signed and indexed.

Run this quick pre-meeting checklist before sharing sensitive files:

- Confirm the NDA is fully executed by the buyer entity.

- Decide which folders you will share now and which you will hold until LOI alignment.

- Spot-check active SOWs for scope, deliverables, timelines, responsibilities, and signature completeness.

- Mark each critical deliverable as Work for Hire where supported by contract and applicable legal conditions, or attach signed Assignment of Rights proof.

- Update your risk logs with current status.

- Prepare a response tracker so you can answer buyer requests and data room uploads quickly.

Which contract clauses can lower price or kill the deal?#

Clause quality can delay closing and affect price before formal due diligence ends, so you should triage every core agreement before buyer counsel reviews it. You have a packet. Now make sure the contracts inside it hold up under scrutiny.

Buyers care about one question: can this revenue transfer cleanly without hidden legal friction? Weak clauses create friction fast because diligence requests expand as review continues. If you cannot answer clause questions quickly, buyers slow timelines, renegotiate value, or pause the process.

| Clause area | What buyers test | Deal risk when weak | Triage action |

|---|---|---|---|

| Termination rights | How and when the contract can be ended under the agreement or law | Unclear end rights and obligations can create transfer and revenue continuity concerns | Amend ambiguous termination language |

| Assignment of Rights transferability | Whether contracts allow assignment or require consent | Revenue may not transfer cleanly at close | Keep only if transfer language is explicit, otherwise Replace or amend |

| Governing Law and Jurisdiction | Which law applies and where disputes must or may be filed | Enforcement uncertainty and higher dispute cost risk | Amend inconsistent forum language and remove ambiguity |

| Arbitration clause | Whether parties must arbitrate future disputes | Process uncertainty if clause conflicts with forum terms | Keep when it aligns with forum terms, otherwise Amend |

| Indemnification and Force Majeure | Loss allocation and whether non-performance may be excused for events beyond control | Unexpected loss exposure or disputes over performance relief | Amend unclear indemnity scope and force majeure language |

Use this pre-diligence triage checklist for each agreement:

- Keep: clear transfer rights, consistent dispute clauses, and balanced liability language.

- Amend: ambiguous wording, inconsistent legal venue terms, or terms that no longer match current operations.

- Replace: missing assignment language, materially unclear indemnification terms, or missing force majeure language where business continuity risk exists.

Example: a buyer likes your valuation, but finds three top client agreements that block assignment without consent. The path forward is not debate. It is remediation: secure consent paths and update contract language before confirmatory review.

If you want a drafting companion, use How to Create a Buy-Sell Agreement for a Partnership.

How do cross-border clients change risk and closing steps?#

Cross-border clients add complexity, but you can keep control by running legal transfer, payment operations, and tax compliance as separate workstreams. Apply the same discipline you used in contract triage across each jurisdiction and entity involved.

Run three workstreams in parallel#

| Workstream | What you own | Evidence for Due Diligence | Close gate |

|---|---|---|---|

| Legal transfer | Map assignment rights, consent requirements, governing law, and jurisdiction by client contract | Contract matrix, consent tracker, amendment log | No unresolved transfer blocker |

| Payment operations | Map invoice to receipt to payout flow for each cross-border path | Traceable payout records, reconciliation packs, approval logs | No unexplained reconciliation break |

| Tax compliance | Test owner and entity reporting obligations by form, program, and country | Filing checklist, advisor memos, submission confirmations | No open filing uncertainty |

FBAR (FinCEN Form 114) requires covered U.S. persons to report foreign financial accounts when aggregate value exceeds $10,000 at any point in the year. You file FBAR through FinCEN's BSA E-Filing System, not with the IRS. File by April 15, and use the automatic extension to October 15 when needed.

Form 8938 covers specified foreign financial assets. For certain U.S. taxpayers, the base threshold starts at $50,000, and higher thresholds can apply based on facts. Form 8938 does not replace FBAR, so you must test both obligations separately.

Set a hard verification gate#

Jurisdiction and entity setup can change treatment quickly, and program status can change over time. Require a formal verification pass before signing and again before close.

| Verification check | What to confirm |

|---|---|

| FinCEN status | Confirm current FinCEN program status and filing expectations for your exact fact pattern |

| Local requirements | Confirm local country requirements for each relevant jurisdiction |

| Workflow controls | Confirm policy-gated workflows for approvals, exceptions, and record retention |

Example: if a buyer can trace each payout path and match it to reconciled records, diligence can stay focused on transfer terms instead of avoidable cleanup. That can improve close readiness, but it does not replace legal and tax sign-off.

Close the deal with a low-surprise handoff plan#

Use a written close plan with explicit go/no-go gates so ownership transfer stays auditable, controlled, and low surprise.

Turn your diligence work into execution rules before signatures: define pre-close operations, set buyer access boundaries, and keep asset and liability schedules complete. Put those terms in the sales agreement, then run legal and advisor review before final sign-off so decisions are based on documented facts, not momentum.

Use the next 30 days as a planning template, not a guaranteed timeline. Set short benchmarks plus one realistic final deadline, and pause when evidence is incomplete. The goal is controlled closing momentum, not speed at any cost.

Run a 30 day close sprint#

| Window | Primary objective | Required output | Go or no-go gate |

|---|---|---|---|

| Days 1 to 7 | Finalize scope of transfer | Complete asset and liability schedules, updated risk log, transfer list | Go only if no material asset or liability remains unclear |

| Days 8 to 14 | Lock legal execution | Sales agreement with pre-close operating rules and access boundaries, attorney review notes | Go only if legal review confirms accuracy and completeness |

| Days 15 to 21 | Validate tax reporting mechanics | For qualifying business asset transfers, align allocation using the residual method and confirm Form 8594 responsibilities for buyer and seller | Go only if both sides confirm filing responsibility and timing |

| Days 22 to 30 | Rehearse Day One continuity | Handoff runbook, owner map, customer communication plan, and TSA contingency plan if a TSA is used | Go only if service continuity holds under rehearsal |

Use hard gates before you sign#

| Gate | What to confirm |

|---|---|

| Scope integrity check | Confirm transferred assets and liabilities are fully listed and internally consistent |

| Execution authority check | Confirm who runs operations before close, who can approve exceptions, and who owns each close-day action |

| Tax reporting check | For qualifying transfers, confirm residual allocation workflow and Form 8594 ownership/timing on both sides |

| Recordkeeping check | Archive the final close pack and retain core records in line with the three-to-seven-year guidance range |

Example: if a buyer asks for broader data access late in the process, apply the agreed access boundary in the sales agreement, grant only what supports close readiness, and log every exception.

For a grounded final step, run one advisor validation pass and one internal close rehearsal before signing. Confidence comes from evidence, not hype. Want to confirm what is supported for your specific market or program? Talk to Gruv.

Frequently Asked Questions

How do I sell my freelance business and not just sell my services?

Treat the sale as a transfer of assets or stock, not a pitch for new client work. Build the package around transferable contracts, clean financial records, and repeatable delivery systems that another operator can run. Then formalize terms in a sales agreement so the deal stands on documented facts, not founder charisma.

What makes a small freelance agency truly sellable to buyers?

Buyers reward verified financial performance, predictable revenue trends, and operational independence from the founder. Sellability improves when workflows are documented, delivery quality is consistent, and clients renew under clear contract terms. Buyers pay for durability they can verify.

How is a small agency valued before a sale process starts?

Start with a business valuation so you can negotiate from evidence. Use the income approach to test projected revenue against risk, the market approach to compare recent similar sales, and the assets approach to subtract liabilities from asset value. For a deeper walkthrough, see How to Perform a Business Valuation for a Small Agency.

What should be in a freelancer or agency Due Diligence packet?

Include core financial statements, active contracts, and a clear liabilities schedule. Buyers typically match financial records to contract terms and risk notes to confirm the story holds together. Add licenses and regulatory compliance documents so the buyer can confirm legal standing quickly.

Can I still sell if my revenue is concentrated in a few clients?

Yes, you can still close, but disclose concentration risk early and show a mitigation plan. High customer concentration increases downside if one client cuts spend or leaves, so buyers will scrutinize that risk closely. Your exit strategy should include specific actions to reduce dependence before final pricing.

What compliance issues matter if my clients are international?

Separate tax and reporting review from commercial negotiations so you do not miss filing obligations. Form 8938 and FBAR serve different programs, and filing one does not automatically satisfy the other. FBAR review starts when aggregate foreign account values exceed $10,000 at any time during the year, while Form 8938 can begin at $50,000 for unmarried U.S. filers, and thresholds vary by filing status and residency, so confirm your facts before close.

What are the most common deal-breakers in an agency Acquisition?

Incomplete documentation kills momentum fast, especially when assets or liabilities stay unclear in sale paperwork. Buyers also pause when they find weak evidence on performance stability, unresolved liabilities, or concentration risk that is not addressed. Keep the deal package complete, auditable, and internally consistent if you want a low-surprise close.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

How to Perform a Business Valuation for a Small Agency

---

How to Create a Buy-Sell Agreement for a Partnership

**Treat your buy-sell agreement for partnership as core operating infrastructure, not paperwork for later.** Freelancers and consultants move fast on client delivery, but shared ownership risk keeps running in the background until one partner leaves, becomes disabled, goes bankrupt, or goes through a divorce.