Quick Answer

For most nomads, renting is the safer default until cashflow and location plans are consistently predictable. This guide recommends a 10-minute cashflow-first system: pass a runway risk gate, run an all-in cost and break-even worksheet, and stress-test your exit plan. If liquidity or exit clarity is weak, choose Rent now or Rent while preparing to buy.

Renting vs. buying for nomads: a 10-minute cashflow-first decision system (not vibes)#

Treat this as a cashflow-posture decision first and a lifestyle decision second. Do not start with neighborhoods, aesthetics, or "settling down." Start with the operator questions that keep your business-of-one alive: how much liquidity you lock up, how fast you can exit, and what happens when a client pays late.

You are choosing between two kinds of risk. Renting buys exit speed and keeps more cash liquid when invoices slip. Buying concentrates risk into a single asset, adds ongoing obligations, and ties up capital you could have used for runway.

One more cashflow reality: early ownership can feel like "I'm paying a lot and building little." In the first few years of ownership, most of what you pay toward your mortgage can go to interest, not principal.

One illustrative scenario: a $300,000 purchase with 20% down creates a $240,000 mortgage, and at a 4% rate, the early payment mix can look like about $800 interest and $345 principal. If you plan to move again soon, do not assume "building equity fast" will rescue a short hold.

At-a-glance comparison (pick your default in 60 seconds)#

Use this as a decision prompt, not a universal truth.

| Criteria | Rent (Lease / Airbnb) | Buy (Primary / Investment) |

|---|---|---|

| Upfront cash | What is the deposit, first payment, and setup cost? | What is the down payment, closing cost, and initial setup cost? |

| Flexibility / exit speed | What does it take to leave early or switch cities? | What is your clean exit if you need to move (sell, rent out, other)? |

| Cashflow resilience (late client payments) | How much cash stays liquid if income slips? | How much cash gets locked up, and what payments continue regardless? |

| Cross-border complexity | What local rules, lease terms, or paperwork apply? | What local rules, property process, banking, and tax/admin pieces apply? |

| Break-even horizon | How long can you commit without strain? | How long can you commit without strain? |

| Failure modes | What could go wrong (churn, disputes, friction)? | What could go wrong (forced timing, vacancy, transfer or tax surprises)? |

You still need to validate local rules and your real numbers before you commit.

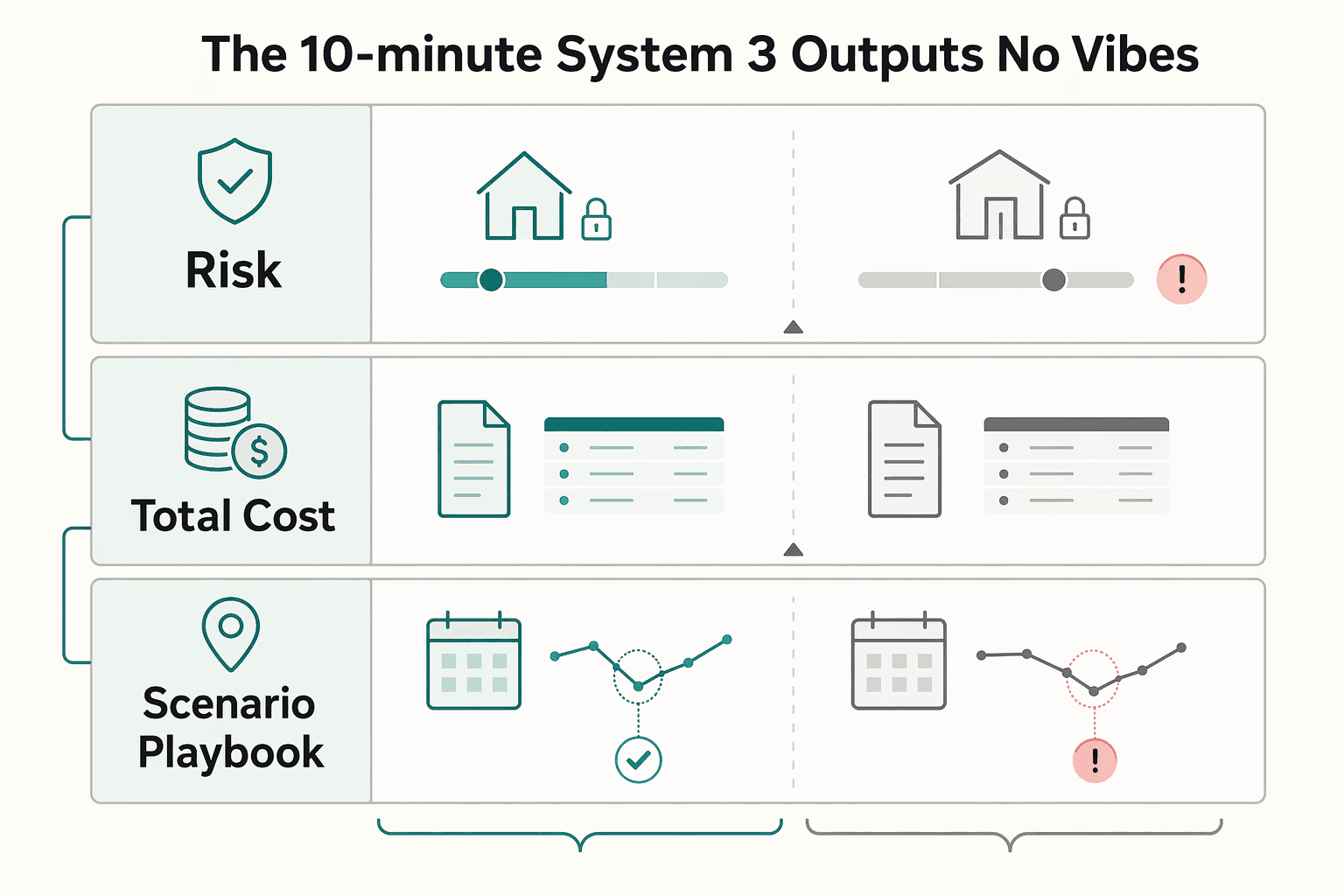

The 10-minute system (3 outputs, no vibes)#

Run this in order. Stop as soon as you have a clear answer.

| Step | Time | Choose this when | Output |

|---|---|---|---|

| Risk Gate | 1 minute | You cannot keep your runway intact after paying the upfront cost | Rent now |

| Total-Cost + Break-Even worksheet | 7 minutes | Buying requires you to lock up cash you might need to cover a late invoice | Rent while preparing to buy |

| Scenario Playbook | 2 minutes | You cannot name a clean exit if you leave sooner than planned | Rent now |

- Risk Gate (1 minute, pass or fail): If you cannot keep your runway intact after paying the upfront cost, choose

Rent now. - Total-Cost + Break-Even worksheet (7 minutes): List every cash outflow you control: rent- or mortgage-related payments, utilities, moving costs, and any bridging stays like Airbnb. If buying requires you to lock up cash you might need to cover a late invoice, choose

Rent while preparing to buy. - Scenario Playbook (2 minutes): Ask, "If I leave sooner than planned, what is my cleanest exit?" If you cannot name one, choose

Rent now.

Hypothetical operator scenario: you land a new client, revenue looks great, then their first payout slips. Renting can keep your cash liquid so you keep shipping work. Buying can stack late-payment stress on top of fixed housing stress in the same month.

Want a quick next step? Try the free invoice generator.

What problem are you actually solving: flexibility, stability, or cashflow control?#

Solve for one primary constraint (mobility, stability, or liquidity), then pick rent or buy as the tool that protects it.

If you cannot write the constraint in one line, you will drift into emotional decisions and justify them later.

Start with this sentence and copy it into your notes: "I am optimizing for (A) mobility, (B) stability, or (C) liquidity." Then commit to it. Your answer should reduce exposure to three nomad realities: cash-flow whiplash (late invoices, holds, ghosting), country friction (account access, compliance checks), and single-point failure (one bank, one income stream, one plan).

Translate lifestyle goals into operational constraints (then choose your housing lever)#

Use the same criteria across each goal so you can compare options cleanly:

| Primary goal | What you are really protecting | Rent-leaning default | Buy-leaning default |

|---|---|---|---|

| Mobility | Exit speed and low admin | Shorter commitments, simpler exits. Keep relocation cash set aside so a fast move does not hit operating cash. | Only if you can leave without scrambling (clear plan to sell or run it as an investment). |

| Stability | Predictable weeks, fewer moves | Longer lease or a monthly rental (a furnished home rented with a standard lease for 28+ days, usually 30+ except February). This often reduces churn; average stays run around three months in one cited guide. | Only if income timing stays predictable enough to support slower exits and fixed obligations. |

| Liquidity | Cash you can access on demand | Rent to avoid locking capital. Ring-fence deposits and bridging stays (like short-term rentals) so they do not contaminate runway. | Buy only after you can lock cash up without creating a runway problem. |

Operator note: the 30-day threshold matters in many cities because short-term rental regulations often stop applying there. That makes monthly rentals a practical middle lane between hotels and year-long leases.

Two non-negotiables (business-of-one protection rules)#

Set these before you shop listings:

- Runway minimum: choose a minimum runway you refuse to go below, track it monthly, and treat it as untouchable.

- Client concentration ceiling: if one client controls your month, you are not in a buying posture yet. One missed client payment or one surprise expense should not knock you over.

Hypothetical: you plan to "settle" but you still hop between short stays (for example, Airbnb) because projects pull you around. Treat that as a signal you need a renting-first season, or at least a monthly rental, while you stabilize payment timing and rebuild liquidity.

Renting as a nomad: when is it the safe default (and when does it quietly drain you)?#

Renting can give you a cleaner exit and tie up less capital than ownership, but "flexibility" can still create friction costs when your timeline stays uncertain.

Use renting as your default tool when you need optionality. Then make sure that optionality does not turn into slow financial leakage.

Renting fits when your timeline stays fuzzy for reasons you cannot fully control. Visa rules and border realities can force that fuzziness.

One traveler described what officials actually cared about at a crossing: "They wanted to just be sure that I had the money to leave right then or tomorrow." Renting can support that posture because it keeps your exit plan simple and your cash more liquid than ownership typically does.

Where renting wins (and where it bites)#

Use this comparison to separate "renting" into two very different execution modes:

| Criteria | Lease or monthly rental | Short-stay churn (hotels, Airbnb-style stays) |

|---|---|---|

| Exit speed | Medium to high (depends on notice terms) | High (you can leave fast) |

| Admin load | Lower once set up | Higher (repeat bookings, check-ins, address changes) |

| Budget clarity | Often higher (more predictable month to month) | Often lower (total cost can vary by stay) |

| Risk surface | Deposit and condition disputes | More repeated transactions and small surprises |

| Best for | A semi-stable base while you keep mobility | Transitional weeks when you validate a city |

A Digital Nomad Visa can also compress your planning horizon. In online commentary about Japan's digital nomad visa, one Hacker News commenter referenced a 180-day time frame and put it bluntly: "I think 180 days is too short for this to be worthwhile." Treat that as a caution flag against locking yourself into multi-year assumptions.

The quiet drain: churn and cash traps (plus your countermeasure)#

Renting drains you when you treat temporary housing as "just rent." Short stays can stack extra charges and time costs. You do not need perfect math, but you do need one place to review the pattern, even a simple monthly reconciliation.

Treat deposits like restricted cash. Landlords can take time to return them, and disputes happen. The countermeasure is boring but effective: keep deposit money clearly separated in your budget so you do not accidentally spend operating cash.

Hypothetical: you bounce between short stays while you "decide" on a neighborhood. If that pattern keeps repeating, stop optimizing the listing and start optimizing the system. Choose a longer rental for one cycle, cut churn, and rebuild liquidity.

Buying as a nomad: when does it pay off - and what can blow up your plan?#

Buying can work for a nomad when you treat it as a long-horizon operating decision with a clear exit plan, not as a lifestyle upgrade.

Your job is the same: protect cashflow first, then optimize comfort.

A cleaner way to think about it is to choose your lane up front: are you buying a stable base for personal use, or buying an investment you'll operate, even if you're not physically there? Mixing the two is where people get surprised.

| Decision lens | Buy as a stable base (personal use) | Buy as an investment (rental business) |

|---|---|---|

| Primary goal | Predictability and stability | Return on capital and diversification |

| What you optimize | Daily life, routines, a consistent address | Occupancy, pricing, expenses, asset management |

| What can surprise you | Ongoing obligations, maintenance, time cost | Vacancy, repairs, admin load, local rules, management risk |

| Exit plan you need | "If I move, can I sell or carry it?" | "If demand changes, can I hold, rent, or sell?" |

| Safe default for nomads | Less common unless you truly anchor | Viable, but it is a separate business model |

If you want the investment lane, treat it like a real estate operator, not a traveler with a side project. Start here: How to Invest in Real Estate as a Digital Nomad.

The non-obvious tradeoff: ownership adds operational surface area#

Buying introduces ongoing tasks that renting often hides: insurance decisions, maintenance coordination, document storage, vendor management, and recurring deadlines. That admin load matters for a business-of-one because it competes with delivery time, invoicing, and collections.

If you already struggle to reconcile your books monthly, ownership will not make your life simpler.

Here is the operator move: write a one-page owner SOP before you close. Include (1) who handles repairs, (2) what gets paid when, (3) where documents live, and (4) the exact steps you will take if you need to leave quickly.

Failure modes that hit nomads harder (and your countermeasure)#

Plans usually break where flexibility meets fixed obligations. Ownership gives you less room to maneuver if your schedule, location, or workload changes.

Countermeasure: require a downside plan you can actually execute quickly, not "eventually."

How do you compare total cost (not just rent vs. mortgage payment)?#

Compare the decision using an all-in view, because the monthly rent or mortgage line can hide costs that actually break cashflow.

You want a decision you can defend in your Ledger, not a vibe you cannot explain later.

A simple all-in housing cost worksheet you can re-run#

Treat your all-in housing cost as "everything housing pulls from cash, plus the cash you lock up upfront." Keep it as a dated note alongside your Ledger exports so you can audit the decision later.

| Cost bucket | Renting (lease, short-term stays) | Buying (primary, investment) | Operator note |

|---|---|---|---|

| Monthly core | Rent | Mortgage payment (and any required payments) | Do not compare rent to mortgage alone. |

| Beyond the monthly check | Utilities and other ongoing living costs | Utilities, taxes, insurance, supplies, repairs | A $1,000 mortgage can become $1,500 (or more) once you add everything else. |

| Moving and transition costs | Moving expenses, temporary stays between places | Moving expenses | If you move often, transitions can be real money. |

| Upfront and "stuck cash" | Security deposit and rent in advance | Down payment and purchase costs (including closing-related costs) | Renting typically only involves a security deposit and a few months' rent in advance. That cash still matters when you protect runway. |

| Cross-border considerations (when abroad) | Flexibility to test life in a new country before committing | Foreign property laws, tax implications, and market fluctuations to weigh | Keep this bucket explicit if you are relocating internationally. |

Cash discipline: separate "locked-up" cash (like deposits or down payments) from "operating runway" cash in your notes, so you do not confuse liquidity with affordability.

Stress-test the decision across time and uncertainty#

Instead of looking for a universal cutoff, run a few scenarios based on how long you expect to stay put, how often you relocate, and how much uncertainty you can tolerate. Buying can bring extra complexity, especially abroad (property laws, taxes, market swings). Renting can be a lower-upfront, more flexible way to test a place before you commit.

What cross-border traps do nomads miss when renting or buying abroad?#

Cross-border traps usually show up in tax reporting, documentation timelines, and cash-movement friction, not in the rent price or the mortgage rate.

This is where the housing decision becomes a compliance and operations decision, not just a real estate preference.

Cross-border trap matrix (renting abroad vs buying abroad)#

| Trap category | Renting abroad (lease, Airbnb) | Buying abroad (primary, investment) | Safe operator move |

|---|---|---|---|

| U.S. tax reality (if you're a U.S. taxpayer) | You can still create a tax footprint even if you "feel temporary." | Ownership can add more filings and more recordkeeping. | Treat taxes as a system. Keep a monthly "tax folder" workflow, not a once-a-year scramble. |

| FEIE misconceptions | People assume "excluded" means "invisible." It does not. | Same misconception, with more paperwork to reconcile. | Remember: you claim the foreign earned income exclusion only if you file a return reporting the income. |

| Time-based eligibility | Short stays can break your plan if you rely on day counts. | Same risk, plus harder exits if you must move to fix eligibility. | If you plan around FEIE's physical presence test, you need 330 full days abroad in a qualifying 12-month period (they do not have to be consecutive). |

Operator checklist: don't let "nomadic" become "undocumented"#

- Define your tax posture in writing: If you want FEIE, confirm you (1) have foreign earned income, (2) maintain a foreign tax home, and (3) meet a qualifying test (physical presence or bona fide residence).

- Use the IRS numbers as guardrails: For tax year 2026, the maximum FEIE is $132,900 per qualifying person. Do not build a plan that quietly assumes more exclusion than allowed.

- Treat timing as a cost: If your short-term housing stretches because local paperwork takes longer than expected, log that as an avoidable ops failure, not "cost of travel."

Should freelancers with variable income buy abroad - or keep renting?#

Freelancers with variable income often do better renting until their own cashflow tracking shows they can lock up capital without putting business operations at risk.

Here the housing decision stops being a real estate debate and becomes financial planning for a business-of-one.

Run a cashflow Risk Gate (based on your own records, not optimism)#

Your first move: pull up your Ledger and look at reality. Not your best month, your actual pattern.

| Check | What the article says |

|---|---|

| Payout reliability | Do your Payouts arrive when you expect them to, or do you regularly see delays, partial payments, or "we'll pay next week" loops? |

| Volatility stacking | If your income swings and you also plan to lock cash into a down payment, you stack two risks on top of each other. |

| Time horizon clarity | If your ability to stay in a place depends on time-limited approvals or renewal uncertainty, treat that as an exit-risk multiplier. |

Use those checks as decision gates:

- Payout reliability: If your Payouts regularly arrive late, treat that as a rent signal, not a buying signal.

- Volatility stacking: If your income swings and you also plan to lock cash into a down payment, you are stacking two risks at once.

- Time horizon clarity: If your ability to stay depends on time-limited approvals or renewal uncertainty, treat that as an exit-risk multiplier. Ownership does not pair well with unclear exit paths.

Core concept: down payment lock-up is payment-protection risk. Money tied up in a property cannot cover an invoice gap, a client pause, or a surprise move. Renting keeps more liquidity available to absorb shocks.

Renting vs buying for variable-income nomads (operator comparison)#

| Criteria | Rent abroad | Buy abroad |

|---|---|---|

| Liquidity | Keeps cash accessible for ops and invoice gaps | Locks cash into an illiquid asset |

| Commitment level | Time-boxed, easier to change cities | High, slower to unwind if plans change |

| Exposure to income volatility | Lower fixed commitment per month | Higher commitment plus cash lock-up |

| Flexibility for "cost of living arbitrage" | High, you can relocate fast to optimize costs | Low, you anchor to one market |

| Operational overhead | Lower paperwork surface area | Higher ongoing admin, plus exit logistics |

Hypothetical: your income looks "stable" because one client pays well. Then they pause a project. If you rent, you can downshift quickly. If you bought, you must carry the commitment while you scramble to replace revenue.

If you want a deeper dive, read Liability Insurance for Freelance IT Consultants: Do You Need It?.

Scenario playbook + decision checklist: pick "Rent now", "Buy now", or "Rent while preparing"#

Pick "Rent now", "Buy now", or "Rent while preparing to buy" based on which option preserves liquidity and operational control first.

Then optimize for comfort or upside. This is the moment you choose a posture you can defend, not a vibe.

Scenario playbook (three outputs you can reuse)#

Use this table as your operator filter. You do not need perfect certainty. You need a defensible default tied to your budget and recent income timing.

| Output | Choose this when... | What you optimize | Guardrails so it doesn't backfire |

|---|---|---|---|

| Rent now | Your location plan still changes, or your income pattern still surprises you | Flexibility, fast exits, low lock-up | Cap commitments you can't unwind quickly. Treat move costs as a recurring line item in your budget. Keep a written "exit on short notice" plan. |

| Buy now | You can commit to a single base and your income arrives with consistent timing | Stability, long-horizon cost control | Protect a runway in your budget before you commit. Pre-model two exits: "sell" and "rent it out." If you cannot explain the exit in one page, you are not ready. |

| Rent while preparing to buy | You want ownership eventually, but ops still look fragile | De-risking, documentation, repeatability | Tighten collections and reduce reliance on any single client. Keep your housing decision behind a readiness checklist, not a mood swing. |

Hypothetical: you feel "ready" because revenue looks strong, then one anchor client stretches payment timing. If you rent, you can adjust without turning housing into a crisis. If you buy, you stack business volatility on top of fixed obligations.

Decision checklist (printable)#

Run this like a pre-flight check. If you answer "no" to any line, default to Rent now or Rent while preparing.

| Check | Question |

|---|---|

| Time horizon | Can I write a simple plan for where I want to be and why? |

| Cashflow | Does my recent income show predictable timing, not just high totals? |

| Runway | Did I protect a runway in my budget, separate from "down payment" money? |

| Liquidity | Can I lock capital without touching emergency reserves? |

| Exit | Can I name the fastest exit path and list the costs I will eat if plans change? |

| Auditability | Can I explain this decision to Future Me in one page with assumptions and worst-case notes? |

Use the checklist as more than a scorecard:

- Time horizon: If you cannot write the plan, you do not yet have one.

- Cashflow: High totals are not enough if timing is erratic.

- Runway: Down payment money is not runway.

- Liquidity: If capital lock-up would force you to touch reserves, you are not ready.

- Exit: A vague exit is not an exit.

- Auditability: If Future You cannot follow the assumptions, you made a mood decision.

The bottom line: use the safe default (rent) until your cashflow system earns you the right to buy#

Treat renting as your default posture when uncertainty is high, and treat buying as something you earn with repeatable cashflow and clear operations. That is not "rent forever" or "buy ASAP." It is control first, commitment second - especially if you still cannot explain, in plain language, how ownership would behave under stress.

A useful mental check: one Hacker News commenter summed it up as "The Flexibility of Renting Is Undervalued" (and also argued the stability of buying is undervalued). Translate that into ops: if flexibility is your current edge, protect it. If stability is what you are truly optimizing for, make sure you can support it without wishful thinking.

A practical decision table you can reuse#

| Decision output | Choose this when... | What you do next (operator steps) | What to avoid |

|---|---|---|---|

| Rent now | Your plan still has meaningful unknowns, and you don't want housing to become a second system | Keep the commitment light. Write down what would have to be true for you to buy (cashflow, admin bandwidth, exit plan), then revisit | Treating "renting" as drifting: no process, no notes, no decision triggers |

| Rent while preparing to buy | You want a base, but you're not ready to commit without proof | Build a simple, repeatable paper trail (income in, bills out, buffers) and a downside plan, then rerun the decision | Shopping the dream before you've stress-tested the downside |

| Buy now (with guardrails) | You'd still want to own the asset even if your plans change, and you can support the ongoing work | Separate "home" math from "investment" math, and document how you'll handle operational load | Calling it "passive" without a plan for who does the work |

Here is the reality check that keeps this honest: rental property income rarely behaves like a salary. Jetstream describes long-term rentals as able to provide a steady income stream, but also notes they can create cashflow challenges because profit margins are often tight. Jetstream also describes vacation rentals as attractive for higher profit margins, but requiring "a lot more work" to start and maintain.

One more operator note if you're thinking, "I'll just hire management": some property managers market "Guaranteed Rent." One review describes Nomad Property Management as a tech-enabled property management service offering "Guaranteed Rent" and low monthly fees (4-6%), and says reviews focus on a promise to deposit rent on the 5th of the month even if the tenant does not pay. Treat any guarantee like a contract feature: read the fine print and confirm what is actually covered.

Next step if you want to move toward ownership: The Ultimate Guide to Getting a Mortgage as a Freelancer.

Frequently Asked Questions

Is renting or buying better for digital nomads?

Renting is often the safer default for nomads because it preserves flexibility and typically requires less upfront cash. It also lets you test a city and your admin load before you add longer-term obligations. Buying can deliver stability and equity, but it pulls in property laws, taxes, and slower exits. Use renting as your default posture until your location plan and cashflow stop surprising you.

When does buying beat renting for a nomad?

Buying beats renting when you can hold long enough that a slow exit does not turn into an emergency, and you would still want to own the asset even if you leave. One nomadic couple framed ownership as a next step after “the constant hassle of finding a place to stay.” If housing search friction is eating your operating energy, ownership can reduce churn, but only if you can handle the cash lock-up and the exit plan.

What risks do nomads miss when buying property abroad?

Nomads can underestimate legal, tax, and market complexity when buying abroad. You also inherit exit timing risk: you might need to move now, but selling takes time. If you cannot explain your exit path and the likely friction in plain language, you are not ready.

Should freelancers with variable income buy abroad?

Freelancers with variable income should default to renting until they can absorb income timing surprises without stress. Buying adds large upfront costs like down payment and closing costs, plus ongoing insurance and maintenance. If you still want to buy, build documentation readiness first using The Ultimate Guide to Getting a Mortgage as a Freelancer.

Can a longer time horizon justify buying property?

A longer planned stay can change the decision, but it does not automatically justify buying. It does not remove exit friction, property-law complexity, or the risk of market fluctuations. Use a longer horizon as permission to plan, not permission to lock capital.

What’s the simplest way to estimate break-even without overcomplicating the math?

Use a two-column total-cost list, then sanity-check the exit costs before you trust the result. Keep it concrete: | Cost bucket | Rent | Buy | |---|---|---| | Upfront | First month’s rent, deposit, utilities | Down payment, closing costs | | Ongoing | Rent and utilities | Insurance and ongoing maintenance | | Mobility | Moving and temporary stays | Selling frictions if you leave | If your “buy” column includes unknowns you cannot bound, you have not earned a break-even calculation yet.

What paperwork should I expect (tax, compliance, banking) when moving money across borders for housing?

Expect banks and counterparties to ask for identity checks and documentation (for example, contracts and proof of funds), and plan for delays on large or unusual transfers. Build lead time into your housing plan so a transfer delay does not force expensive short-term housing. Keep a clean folder with contracts, proof of funds, and transfer receipts so you can answer questions fast.

Try a related tool

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Getting a Mortgage as a Freelancer Without Guesswork

Start by reconciling your income file before you compare rates. For a **mortgage for freelancers**, the first gate is simple: can an underwriter read your documents cold and see one consistent income story?

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.

Liability Insurance for Freelance IT Consultants: Do You Need It?

**Treat your insurance decision like risk management, not online shopping.** As an independent IT consultant, you can face a negligence allegation, a client financial-loss claim, and legal defense costs even when you delivered in good faith. One bad dispute can drain time, focus, and cash before anyone proves fault. If you run solo, you are the CEO of a business-of-one, and risk decisions are part of the job.