Quick Answer

A prenuptial agreement for entrepreneurs should set clear rules for business ownership, growth, income, debt, and support before marriage. Even if you started the business before marriage, disputes can still center on appreciation and cashflow during the marriage. The practical approach is to prepare a concise decision brief, organize financial disclosure, keep records clean, and have local counsel convert your intent into enforceable terms.

You're not "planning for divorce" - you're protecting the asset you built (and the life you're building)#

A prenuptial agreement for entrepreneurs turns messy, high-stakes uncertainty into a written system for business assets, money, and risk. Treat the prenup conversation as professional planning, not fear. That framing changes how you prepare, how you talk with your partner, and how efficiently counsel can draft.

If you sell services (freelance, consulting, agency-of-one), your "business" is not a warehouse full of machines. It can include client contracts, receivables, intellectual property (IP), and reputation. In a divorce, those inputs can become a valuation fight and a property division problem, depending on your state law. Leave it vague and you invite the worst operator outcome: time drain, cashflow pressure, and distraction right when you need stability.

A prenuptial agreement is a written contract signed before marriage that outlines how financial matters will be handled if the marriage ends. In operator terms, it sets ownership rules, how you treat growth, and who carries which risks. Done well, it also creates clarity about money, debt, property, and expectations before marriage. That helps both people, not just the founder.

What your "business" actually is (and why that creates risk)#

Treat your business assets like a checklist, not a vibe. Get specific about what you are actually protecting:

| Business input | Examples named | Issue named |

|---|---|---|

| Contracts + pipeline | ongoing client agreements, renewals, referral relationships | valuation fight and property division problem |

| Receivables | invoices you already earned but have not collected | valuation fight and property division problem |

| IP | templates, content, code, methods, brand assets | valuation fight and property division problem |

| Reputation | the goodwill attached to your name and results | valuation fight and property division problem |

A practical, hypothetical example: you run a solo consultancy, you reinvest aggressively, and you keep cash low. Depending on the rules in your state, divorce can trigger a fight about business value or the "increase in value," and you can end up negotiating from a weak cash position while the business still looks healthy on paper.

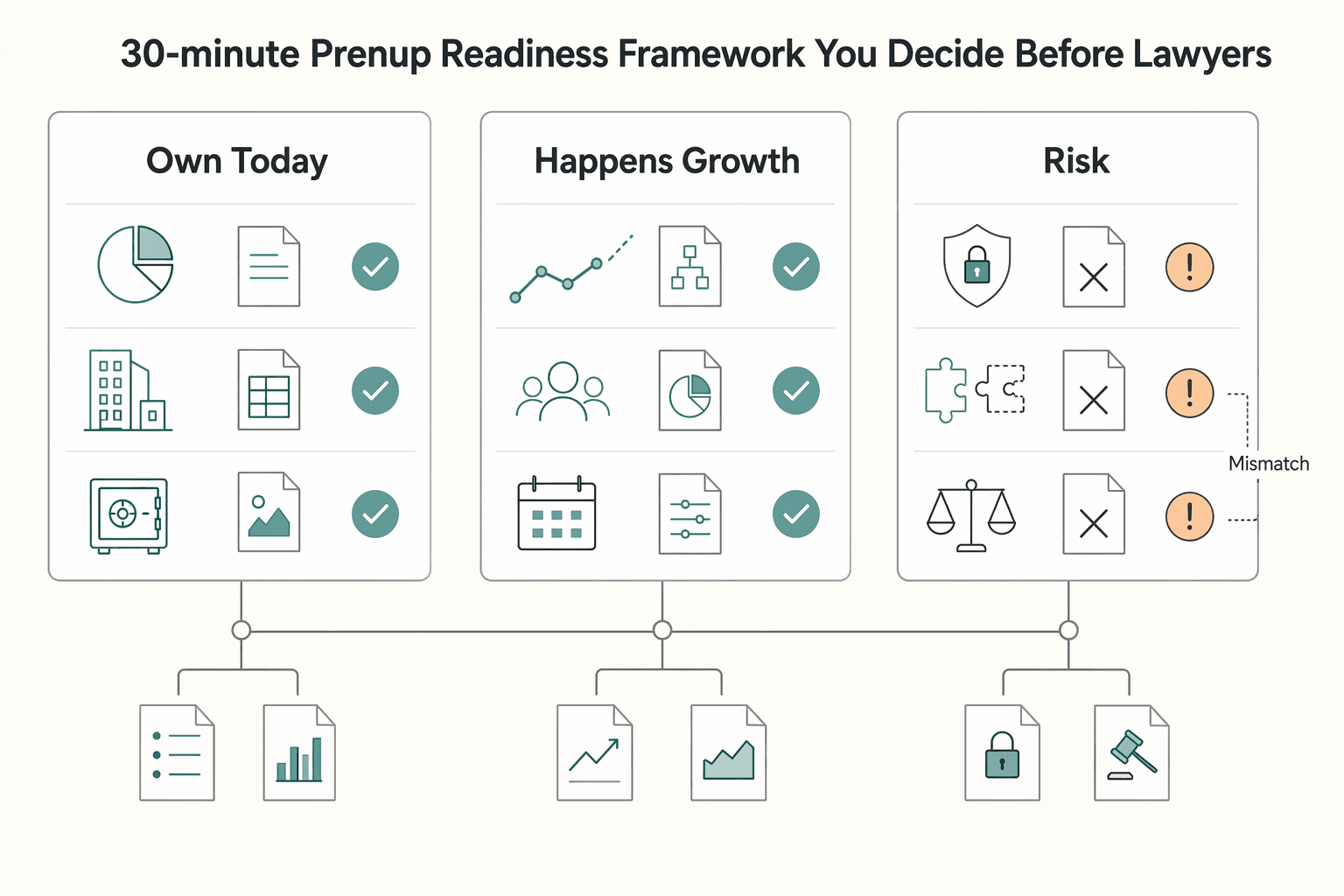

The 30-minute prenup readiness framework (what you decide before lawyers)#

Your job is to produce a clean, defensible brief. Counsel's job is to translate it into enforceable language under your state law and jurisdiction. Use this 30-minute readiness pass:

| Decision | What to write down | Why it drives outcomes |

|---|---|---|

| What you own today | Entity ownership, key IP, major contracts, current cash and receivables | Sets the baseline for business assets and asset protection |

| What happens to growth | Your intent for business appreciation and reinvestment | Helps reduce ambiguity that can trigger valuation disputes |

| What risks stay personal vs shared | Business debts, guarantees, tax obligations, liability exposure | Helps avoid "surprise" shared burdens during property division |

Keep one safety default in mind: laws vary by state and jurisdiction, and enforceability can hinge on process. For example, in Colorado, factors like full financial disclosure, voluntary agreement without coercion, and fair terms can matter. Use this guide to decide the business questions, then confirm the local details with counsel instead of guessing. If you want a quick next step, try the SOW generator.

The mental model: the prenup is a "deal memo" for your marriage and your venture#

A prenup can function like a deal memo that puts key money decisions in writing up front. The point is to stop debating vibes and start deciding levers. That keeps the lawyer bill focused and keeps the partner conversation fair.

Translate legal labels into operator decisions (without pretending the internet knows your state)#

Different places use different rules, so do not get stuck memorizing labels. Use these terms as labels for questions you must answer with counsel:

| Term you'll hear | Operator translation | Why you should care in marriage and legal planning | Your safe default |

|---|---|---|---|

| Prenuptial Agreement (Premarital Agreement) | The written agreement you use to clarify financial expectations and what happens if you split | If you do not spell things out, you may be relying on default rules you did not choose | Draft your intent clearly, then have counsel confirm enforceability and required process |

| Separate Property | "What do we want treated as mine/yours, and what do we need to do to keep it that way?" | The line can get messy fast if you mix accounts, titles, payments, or recordkeeping | Keep documentation clean and ask counsel what behaviors blur the lines in your jurisdiction |

| Community Property | "Does our jurisdiction treat some categories of value as jointly owned by default?" | If a joint-ownership framework applies, it can change how you plan around income, assets, and business value | Ask counsel what system applies where you live and plan terms accordingly |

| Business Appreciation | "If the business grows during the marriage, how do we want to treat that growth?" | This is often where conflict shows up, because growth is real money and hard to untangle | Pre-agree on a growth rule and a valuation approach, then document consistently |

Hypothetical: you run a solo studio. You keep the entity in your name, but you pay household bills from the business account and reinvest most profits. If divorce happens, you can invite a dispute about what counted as business versus household cashflow, and how to treat growth.

The 5-part "deal memo" your prenup should cover#

Do not negotiate like a law student. Approach it like a founder, and cover the levers that actually drive outcomes:

| Part | What it covers | Examples named |

|---|---|---|

| Ownership | What stays separate, what becomes shared | IP, client contracts, brand assets |

| Growth | How you want to treat business growth during the marriage | how you will measure it |

| Cashflow | How you plan to handle money moving out of the business | salary, distributions, retained earnings, household spending |

| Downside | Who is responsible for business-related risk | business debt, personal guarantees, taxes, lawsuit risk |

| Exit mechanics | What happens if you separate | buyout option, valuation method, timeline, dispute process |

If you want one operational habit that supports all five, start with clean accounts and consistent allocations. See The 'Profit First' Method Part 2: Setting Up Your Bank Accounts.

Do entrepreneurs need a prenup if the business started before marriage?#

Yes, because pre-marriage ownership does not automatically settle growth, income, or valuation fights. This is a common operator trap: you can own the venture pre-marriage and still face costly property-division conflict later.

Why "I started it before we met" doesn't finish the job#

Owning the venture pre-marriage can support a "separate" story, but divorce disputes rarely stop at "who formed the LLC." They move fast toward what grew during the marriage, why it grew, and who should share in that growth.

Without a prenup, your marriage follows state default rules on property, debt, and support. Those defaults can pull your business into a debate even if your cap table never changed.

Here's the practical risk for business-of-one operators: usually not "they take half the company," but "you fund a valuation and a settlement process while still trying to ship client work." Cashflow pain is the killer. If you depend on receivables, retainers, and your own delivery hours, even a short disruption can cascade into missed deadlines and lost clients.

Use this decision table to stay concrete:

| What you assume | What can still become disputed | What a prenup can clarify (high leverage) |

|---|---|---|

| "I owned it before marriage, so it's separate." | Portions of premarital equity or the increase in value during the marriage may be characterized as marital property "in some circumstances." | How ownership and any business-related increase in value get handled if divorce or separation happens |

| "No one can claim it because equity never moved." | State default rules still apply, and the boundaries around business-related rights and interests can become a dispute. | How much of a stake, if any, a future spouse has in the business, and how business-related assets and debts are handled |

| "We'll be reasonable if it ever happens." | Default state law rules apply if you do nothing. | The operating rules you both agree to before emotions and deadlines collide |

Hypothetical: you built a solo consultancy before marriage. Years later, the fight centers on growth and value during the marriage, not just formation date.

Safe-default behavior that plays well in most jurisdiction conversations#

Do these before you draft, so counsel can protect you cleanly under your state law:

- Inventory what existed pre-marriage: client contracts, receivables, IP (code, course content, domains), brand assets, and key accounts. Save creation dates and assignment paperwork.

- Keep business records clean: make it easy to show what the business owns, what you own personally, and what happened when.

- Address growth explicitly: decide, in writing, how you'll treat the business's increase in value during the marriage.

- Flag jurisdiction differences early: state rules vary, so ask local counsel how your state's default framework could treat business interests and value growth if you do nothing. Do not guess based on what you've heard about any specific state.

The 30-minute prenup readiness framework: decide these 7 items before you draft anything#

Decide your boundaries and rules in plain English first, then have counsel convert them into terms that can hold up in your situation. With your separateness story clearer on paper (for example, separate accounts and records of pre-marriage assets, where relevant), you are ready to make the decisions that drive most property division outcomes.

Talking about prenups feels weird. Try not to make it personal. Keep it about systems and risk allocation, not character.

How to run a quick session (so it stays productive)#

- Set a timer. One conversation. No drafting.

- Use "decision language," not legal language: "If X happens, we do Y."

- Write answers as bullet points you can hand to counsel as a term sheet.

- If you hit a values conflict, stop and park it. Do not negotiate in circles.

Hypothetical: you run a solo design studio. Your partner supports your workload during a busy season, and you reinvest profits instead of taking bigger draws. If you never define what counts as shared contribution, a divorce can turn reinvestment decisions into leverage. You reduce that risk by choosing a growth rule and an income rule upfront.

Key decisions (operator version)#

| Decision | Your exact prompt | Output to bring to counsel |

|---|---|---|

| Asset boundary | "What stays Separate Property, and what do we willingly share?" | Asset list (entity ownership, trademarks, client list, cash) plus a "shared" carve-out |

| Growth rule | "How do we handle Business Appreciation?" | Choose: fully separate, shared by formula, or shared only with spouse labor or capital contribution |

| Income rule | "Do salary, distributions, and retained earnings follow different rules?" | A simple classification policy for variable freelancer cashflow |

| Debt rule | "Who owns business risk?" | Debt Responsibility list: business cards, tax bills, lawsuits, personal guarantees |

| Support expectations | "What support guardrails feel fair?" | Negotiation intent for Spousal Support triggers and limits (counsel confirms what's workable) |

| Documentation and operations | "What habits prove our story?" | Commitments: separate accounts, clean invoicing, consistent owner draws, ledger-style tracing (see The 'Profit First' Method Part 2: Setting Up Your Bank Accounts) |

| Location and enforcement reality | "Where could this actually get enforced?" | A list of potentially relevant jurisdictions (rules vary): marriage location, residence, incorporation, asset location, likely filing venue |

Write your answers so a neutral third party can execute them without guessing. That is what drives real asset protection.

What exactly counts as "separate" vs "shared" business value - and where people get burned?#

Without a prenup, a spouse's interest in a family business may be treated as marital property, and the business or a portion of it could be divided in divorce. What feels "separate" versus "shared" often comes down to the facts on the ground, especially when the business grows during the marriage or the household benefits from the business.

The most common failure mode looks like this: you start with clean Separate Property (you owned the entity, key IP, the core assets), then you run household and business life through the same pipes. No one "steals" anything. You just make it easier to argue that appreciation belongs in the shared bucket, especially if the business grows during the marriage, a spouse contributes, or business income supports the household.

Term check: "premarital property refers to assets you owned before getting married." That sounds simple, but business value does not behave like a checking account. It shows up in components, and each component invites a different argument. (And in some places, even if you started the business before marriage, growth in its value during the marriage could still be divided on divorce unless a prenup says otherwise.)

Break business value into components (so you can write rules for each)#

| Component of business value | What it includes (examples) | Why people get burned |

|---|---|---|

| Pre marriage core | Shares, intellectual property, established client relationships, brand assets | They assume "I started it" ends the discussion, then they never document what existed before marriage. |

| Post marriage financial build | Retained earnings, reinvested profits, equipment, investments made through the business | They treat reinvestment like a private decision, but a divorce fight can frame it as value created during the marriage. |

| Goodwill tied to labor | Reputation, repeat business, relationships you personally maintain | They ignore how much of the value tracks their ongoing work, which varies by jurisdiction and facts. |

Hypothetical: you run a solo consultancy. You keep rates steady while you reinvest into tools and subcontractors. Years later, someone can argue that your foregone income and reinvestment created shared upside. You reduce ambiguity by writing down, in a prenuptial agreement, how you want business interests (including growth during the marriage) handled if the marriage ends.

Documentation that matches your story (audit-ready, not obsessive)#

Run a paper trail that supports your boundary decisions:

- If you choose to separate business vs household flows, keep bank activity and invoices consistent with that flow (it can make tracing easier, even if outcomes still depend on local law).

- Pay yourself with a repeatable owner draw pattern, not random transfers that look like shared spending.

- Preserve contracts and records that show which business assets existed before marriage (shares, IP, retirement accounts tied to your company).

Finally, treat "community property" and similar labels as a flashing sign that local rules matter, not as a shortcut. Confirm with local counsel what your jurisdiction treats as marital value vs separate value, and do not rely on internet examples from the wrong place.

The "risk-control clauses" your prenup should borrow from good client contracts (yes: Governing Law, Jurisdiction, Dispute Resolution, Termination)#

A prenup can clarify what happens to assets, debts, and spousal support if things go sideways. Once you have your ownership and value boundaries, the next question is whether the agreement is clear about the outcomes you want, and what your local law will enforce.

This works best when you convert "we'll figure it out" into a system. The basic job is to clarify the distribution of assets in the event of divorce and, where allowed, address other issues like alimony. It can also outline what happens to property, debts, and spousal support in the event of separation, divorce, or death. That gives you room to plan for failure modes, not just ownership.

The decisions to discuss (and what you're really choosing)#

You cannot assume every jurisdiction will honor every term. You can still act like an operator: define the decision you want, then ask counsel to translate it into enforceable language under the rules that apply to you.

| Decision area | What you decide in plain English | Why it matters for business assets |

|---|---|---|

| Division of property | Who keeps what, and how property gets treated if you separate or divorce | Avoids vague "we'll split it fairly" conversations when the cap table and cash are real. |

| Ownership of specific assets or a business | What stays separate vs shared, especially around equity and business interests | Protects continuity and reduces pressure to unwind ownership at the worst time. |

| Debts | Which debts stay with whom | Keeps business liabilities from quietly becoming "ours" in practice. |

| Spousal support / alimony | Whether and how spousal support is handled | Sets expectations up front instead of negotiating under stress. |

| Termination (sunset clause) | Whether the agreement has an expiration concept later (a "sunset clause" ties to an agreement having an expiration date) | It can increase perceived fairness, but enforceability varies by jurisdiction. |

| "Process" (where allowed) | How you'll handle disagreements or updates in a way your jurisdiction recognizes | Reduces ambiguity when emotions spike, even if some process ideas can't be locked into the contract. |

Hypothetical: you run a cross-border consultancy, you move twice, and you keep equity separate but pay household costs from uneven business months. If you never define the basics clearly, you can spend your first legal budget fighting about the rules and framing instead of protecting cashflow and client work.

Operator checklist (bring this to counsel)#

- List every relevant jurisdiction (marriage location, current residence, expected moves, incorporation, asset location).

- Write a one-paragraph "what happens if we split" summary you would actually stand behind under stress.

- Define your debt boundary in writing (business tax debt, lawsuits, personal guarantees).

- Keep your money systems aligned with your story (separate accounts, consistent owner draws). If you need a clean setup, use The 'Profit First' Method Part 2: Setting Up Your Bank Accounts.

When should we start the prenup process before the wedding - and what's the clean sequence?#

Start early enough that you can negotiate, draft, review, and sign well before the wedding. Rushing the process close to the date can create avoidable problems later, and the details can hinge on state law.

A practical benchmark: treat at least six weeks before the wedding as an operational floor, not a universal legal rule. You want enough lead time that neither of you feels cornered, and your counsel can handle jurisdiction-driven surprises without a deadline forcing bad decisions.

A safe operator timeline (work backward)#

Plan on starting months ahead, not weeks, and set an internal "done by" date that lands comfortably before the wedding. Your goal is to remove urgency from legal planning so you can negotiate cleanly. Use this simple timeline logic:

| Phase | What "done" looks like | Risk you avoid |

|---|---|---|

| Decisions + disclosure | You both understand what you're treating as separate vs marital property, and the basic debt boundaries | Misunderstandings about what exists, who owns what, and what's on the table |

| Drafting + review | Each side reviews a full draft with counsel | Surprise terms and rushed concessions |

| Signing | You sign after a calm final read-through | Later claims that timing or pressure drove the deal |

The clean sequence (low friction, high clarity)#

This is a practical workflow, not a legal requirement. The point is clean inputs and enough time, because marriage can have huge legal implications for business ownership depending on your state's laws.

| Step | What to do | Details named |

|---|---|---|

| 1. 30-minute decisions | Decide the core rules first | what each owned before marriage; how to handle business growth during marriage; debt responsibility; support intent; relevant state law/jurisdiction issues |

| 2. Financial disclosure packet | Make it easy to understand what is there | business financial statements; key contracts or customer concentration context; debt list; snapshot of pre-marriage assets treated as separate property |

| 3. Business baseline | Set a starting point if you own a company | consider a date-of-marriage value for the business in the agreement |

| 4. Term sheet alignment | Align on the business rules before drafting | you and your partner align before lawyers trade drafts |

| 5. Counsel drafting, revisions, then final signing | Iterate until both of you recognize the deal | drafting, revisions, final signing |

For the disclosure packet, include business financial statements you already rely on to run the company, key contracts or customer concentration context (if relevant), a debt list (credit cards, loans, tax obligations, personal guarantees), and a snapshot of pre-marriage assets you treat as separate property (entities, IP, cash).

Hypothetical: you run a consulting LLC, you reinvest unevenly, and you expect the business to grow after marriage. If you skip clear disclosure and a baseline, you can end up leaving major questions (like what was "pre-marriage" vs what grew during the marriage) to be argued about later.

Your "bring-to-counsel" packet: templates, scripts, and a one-page checklist you can execute this week#

Build a "bring-to-counsel" packet your lawyer can draft from. The point is to reduce back-and-forth, give counsel a clear picture of what you want, and keep the agreement focused on your real-world assets and outcomes.

In Ontario, a prenup is officially called a marriage contract under the province's Family Law Act. The useful frame is the same either way: build financial clarity before you walk down the aisle. You do not argue feelings. You document rules.

One-page marriage contract brief (operator template, not a legal requirement)#

Use this as your one-page brief to counsel. Treat it as a starting point, not a mandatory format.

| Decision area | What you write (one sentence) | Why it matters in separation/divorce |

|---|---|---|

| Separate Property | What you brought in (entities, IP, accounts) | Stops commingling stories early |

| Business Appreciation | How you treat growth during marriage | Reduces valuation fights |

| Income handling | Salary, distributions, retained earnings rule | Prevents cashflow ambiguity |

| Debt Responsibility | Business cards, taxes, guarantees boundary | Limits leverage through liabilities |

| Spousal Support intent | Guardrails you feel good about | Avoids surprises, flags local limits |

| Jurisdiction / forum questions | Any cross-border ties you want counsel to sanity-check | Reduces "where do we fight" ambiguity |

| Dispute Resolution options | How you want disputes handled (if available) | Sets a calmer, cheaper path |

Hypothetical: you run a solo studio and reinvest aggressively. Without a written appreciation rule and a clean "what counts as income" policy, you hand a future dispute the ambiguity it needs to get expensive.

Execution week plan: conversation + audit habits + safety check#

Partner script (tight + fair): "I'm not trying to 'win.' I'm trying to protect the business so we're not forced into a valuation fight if we ever separate. Let's define what's mine, what's ours, and what support looks like so we both have certainty." Then ask: "What would make this feel fair to you?"

Audit-ready habits (start now):

- Separate business and personal accounts.

- Set a consistent owner draw policy, then follow it.

- Document reinvestment decisions (what you reinvested, why, and when).

- If you run Profit First, keep allocations consistent and traceable. Use this setup guide if you need to tighten the system: The 'Profit First' Method Part 2: Setting Up Your Bank Accounts.

Safety check: confirm what's actually doable and enforceable with Ontario counsel, especially if you have assets, residence ties, or business activity outside Ontario. Rules vary by jurisdiction, so do not assume what you've heard elsewhere applies to you.

Quick checklist (copy/paste):

- List pre-marriage assets + IP (Separate Property)

- Define growth/appreciation rule (Business Appreciation)

- Define debt boundary (Debt Responsibility)

- Decide support guardrails (Spousal Support)

- Flag any cross-border ties (to discuss Jurisdiction / forum and Dispute Resolution with counsel)

- Start early; avoid last-minute signing before the wedding

- Assemble your key financial documents for counsel review

The safe default: decide the business boundaries now, document them, then let local counsel make it enforceable#

Decide the business boundaries now, document them, then let local counsel make your intent enforceable. The operator move is to stop debating theory and start capturing your actual business reality. Clarity beats vibes, especially when your income rides on client work and clean cashflow.

If you do nothing, you leave three high-stakes topics to future you, under whatever law and jurisdiction ends up applying later: who owns what, how value and income are treated, and who is on the hook for liabilities. That is not a moral failure. It is an operational risk. And it tends to surface during high-stress moments when negotiation quality drops and your attention belongs on clients.

What "safe default" looks like (without pretending you can DIY the law)#

Run this like legal planning plus asset hygiene, not like a philosophical debate. You decide your boundaries in plain English, then you document evidence that supports those boundaries. Use this table as your "no surprises" map:

| Risk area | The failure mode | What you document now (non-legal, factual) |

|---|---|---|

| Ownership boundary | You rely on "I started it" without records | Entity docs, cap table or ownership statement, IP list, key client contracts |

| Value story | The line blurs between labor, reinvestment, and personal finances | Timeline of major business milestones, reinvestment notes, compensation method |

| Liability boundary | Personal and business liabilities mix | Debt list (cards, loans, guarantees), who signed, what account paid it |

| Cashflow separation | Commingling muddies what's business vs personal | Separate accounts, clean transfers, consistent draw or salary notes |

Hypothetical: you run a solo consulting shop, you pay household costs from the same account that receives client retainers, and you reinvest irregularly. You do not need a lecture to see the problem. You need cleaner lanes and receipts that match your story.

Your next move: a simple operator workflow before you paper anything#

Keep it boring and repeatable. Draft a one-page brief: what sits inside the business, what stays personal, what you consider shared with any partners, and your intent around growth, income, and debts (use the same language you would use with a business partner).

Build a disclosure pack that a stranger can audit: recent financial snapshots, a contract list, an IP list, and a liabilities list. Clean up your money lanes: separate business inflows and owner pay, then document transfers consistently. If you need a practical setup, use The 'Profit First' Method Part 2: Setting Up Your Bank Accounts as an operations reference.

Then involve local counsel to confirm what your jurisdiction recognizes and to draft language that actually holds up, especially if you operate cross-border or across multiple entities. Want to confirm what's supported for your situation? Talk to Gruv.

Frequently Asked Questions

Do entrepreneurs need a prenup if they started the business before marriage?

Yes. Even if the business started before marriage, it can still be worth setting clear rules for how business-related property, debts, and support will be handled if the relationship ends. Use a prenuptial agreement to write down your ownership boundary, your income rule (salary, draws, retained earnings), and your debt responsibility rule. Treat it as asset protection and legal planning, not a prediction of divorce.

What should a prenup include for a freelancer or consultant specifically?

Include terms that map to how you actually make money: receivables, client contracts, IP, and the bank accounts that touch that cashflow. Jointly notes that prenups typically cover “spousal support (alimony)… and even provisions for businesses owned by one or both spouses,” so put your business assets in scope explicitly. Add a simple rule for what counts as “income” versus reinvestment so you avoid ambiguity later.

When should we start the prenup process before the wedding?

Start as early as you can once you both agree you want rules, because rushed negotiation creates avoidable stress and risk. Put together a simple “bring-to-counsel” packet, then book counsel and share it before venue deposits and travel plans lock you in. You want time for questions, edits, and calm decision-making.

Can a prenup be fair and still protect the business?

Yes, if you negotiate fairness as clarity, not vague “trust.” UL Lawyers frames a prenup (a “marriage contract” in Ontario) as a tool “to lay out a clear plan for financial matters, like assets and support,” so write rules that protect the business while also defining support expectations your partner can live with. Hypothetical: you spell out what business value you each intend to treat as staying with the business owner, and you also agree on a clear support approach if the business hits a down cycle.

Do rules differ by state/country, and how do we confirm safely?

Yes, rules differ by jurisdiction, so do not copy a friend’s prenup or an internet template and call it done. UL Lawyers puts it bluntly: “If you don’t create your own rules, the province’s default laws will apply,” so ask counsel what defaults apply where you live and where you hold assets and run the business. Bring a written list of those locations.

What if we are already married, can we use a postnup?

Ask local counsel about options for an agreement after marriage, and do not assume every jurisdiction treats a “postnup” the same way as a prenup. Keep the goal the same: define property, debts, and spousal support expectations in writing. Follow your counsel’s lead on what information you should exchange and document.

How do we handle business appreciation if one spouse supports the other’s work behind the scenes?

Treat that support as a real contribution and define it, instead of leaving it to interpretation during a dispute. If you want to address appreciation and behind-the-scenes work, write a clear rule (for example: shared upside by a formula, defined compensation, or a capped claim) and match it to your recordkeeping. You protect the business and respect the marriage when you name the contribution and the outcome upfront.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- digitalcommons.law.villanova.edu/cgi/viewcontent.cgitrusted

- omeka.urbeuniversity.edu/files/original/7643dd59ba6f5774f2cd939152ef2...trusted

- repository.law.umich.edu/cgi/viewcontent.cgitrusted

- scholarcommons.sc.edu/cgi/viewcontent.cgitrusted

- emilyrubensteinlaw.com/blog/how-premarital-agreements-can-protect-y...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

The 'Profit First' Method Part 2: Setting Up Your Bank Accounts

Most freelancers who try Profit First open a few extra bank accounts and call it done. That's the wrong move.

A Deep Dive into Wise's API for Automated Payments

**If your payment process depends on manual follow-ups, your cashflow will drift, and small misses will compound into real risk.** Manual runs force you to chase approvals, confirm receipts, and update statuses by hand, usually across inbox threads, checks, and spreadsheets. Every extra handoff adds delay. Sooner or later someone asks, "Was this paid yet?" and nobody can answer with confidence.