Quick Answer

To open a bank account in the Netherlands as a foreigner, pick the right onboarding path based on whether you have a BSN and acceptable proof of a Dutch address, then confirm any limits in writing before sharing bank details. Prepare a document pack (ID, address proof, BSN if available), verify the account can receive inbound SEPA Credit Transfers with a small test payment, and keep a SEPA-capable fallback until the account is fully usable.

Stop "opening an account" - build a Get Paid in the Netherlands system that doesn't break under pressure#

The goal is simple: get paid predictably in EUR, reconcile cleanly, and avoid preventable blocks or delays caused by incomplete documentation or unclear onboarding status.

For freelancers, creators, and small teams, the real risk starts after you hit submit. It shows up when a client pays via SEPA Credit Transfer and you have to answer, "Why hasn't it arrived yet?" SEPA execution timing is often described as next-business-day for electronic payments, but edge cases can take longer. Paper-based instructions can extend the maximum to two banking business days. It also shows up when an account looks "done" in the onboarding UI, but verification is still pending.

Your setup (safe defaults, no guessing)#

Decision tree (BSN / no BSN):

| Your status | Safe default action | "Confirm safely" prompt |

|---|---|---|

| BSN in hand | Proceed with onboarding and immediately test a small inbound transfer | "After approval, can I receive inbound SEPA transfers immediately, or do you apply an activation step?" |

| No BSN yet | Start onboarding only if the bank explicitly allows it and states the deadline to add BSN | "Can I start without a BSN, and what happens if I miss the deadline?" Some guides mention a 90 day window, but verify with the bank. |

Document readiness checklist (reduce back and forth):

- Valid passport or ID. Many flows ask you to photograph the document, sometimes with a selfie.

- Proof you live in the Netherlands, especially if you hold a non-EU passport. Banks may request evidence such as a municipal registration extract.

- BSN if available. BSN (Burgerservicenummer) is the unique personal number allocated to everyone registered in the Personal Records Database (BRP).

Cashflow risk workflow (client by client)#

Before you share any Dutch bank details, run this:

- Rail choice: For EUR payments, SEPA Credit Transfer is a common option.

- Activation check: Assume "apply in 10 minutes" in an onboarding flow describes form completion, not full activation. Treat activation as unconfirmed until you receive an inbound test payment.

- Fallback ready: Keep a SEPA-capable backup receiving path active until the new account proves it can receive funds normally.

The mental model: your money lifecycle (collect → verify → reconcile → convert → payout)#

Treat the bank-account step as one part of a repeatable money lifecycle. Each stage should produce the proof the next stage needs. Once you see onboarding as one node in the system, you can name the identifiers and checks that actually move money. That is what keeps you steady when a client asks for "the right details" and a bank asks for "one more document."

The primitives (know these cold)#

You only need a few building blocks, but you should name them precisely.

| Component | What it is | What you use it for (operator view) |

|---|---|---|

| SEPA (Single Euro Payments Area) | A framework for euro payments under harmonised standards | Standardise EUR payment details so you don't reinvent instructions per client |

| SEPA Credit Transfer (SCT) | A payment instrument for euro credit transfers between payment accounts located in SEPA | Use it for euro bank transfers, for example paying invoices, between accounts in SEPA |

| IBAN | International Bank Account Number | Put it on invoices as the account identifier your client's AP team can pay |

| BIC | Business Identifier Code defined by the ISO 9362 standard | Provide it when a payer or setup screen asks for a bank identifier in addition to IBAN |

| BSN (Burgerservicenummer / Citizen Service Number) | A unique number for everyone registered in the BRP | Treat it as an identifier financial institutions may be obliged to use for clients |

Two facts matter in practice: SEPA standardises cashless euro payments across the region, and SCT works only for euro transfers between accounts located in SEPA.

The compliance layer (KYC, AML) and your operator loop#

KYC is how institutions verify identity, assess risk, and monitor transactions. AML covers the rules and controls designed to prevent and detect money laundering.

| Stage | Action | Record |

|---|---|---|

| Collect | Issue invoice with your legal name, IBAN, and a single reference format you enforce | Invoice with your legal name, IBAN, and one reference format |

| Verify | Confirm the payer used the right beneficiary details and reference | Match funds to the invoice |

| Reconcile | Match bank-line to invoice-line, then store the proof | Invoice PDF plus bank confirmation |

| Convert | Only convert when you need another currency | Keep the conversion record with the invoice trail |

| Payout | Move money to personal pay only after you close the reconciliation loop | Reconciliation loop closed before payout |

Your job is to run a tight loop that produces clean evidence:

- Collect: issue the invoice with your legal name, IBAN, and a single reference format you enforce.

- Verify: confirm the payer used the right beneficiary details and reference so you can match funds to the invoice.

- Reconcile: match bank-line to invoice-line, then store the proof.

- Convert: only convert when you need another currency. Keep the conversion record with the invoice trail.

- Payout: move money to personal pay only after you close the reconciliation loop.

For example, a new Dutch client asks for "BIC too." You send the IBAN + BIC from your account, require the invoice number as the transfer reference, and reconcile as soon as it lands. If you automate anything, automate reconciliation first.

Related: Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Which path fits you: resident with BSN, no BSN yet, or non-resident?#

Pick your safest path by answering two questions: do you have a BSN, and can you prove a Netherlands address or local ties with documents a bank will accept? With the money lifecycle mapped, you can choose an onboarding route that does not fail mid-payment.

Your decision tree (BSN + proof)#

BSN (Burgerservicenummer / Citizen Service Number) is a unique personal number used for contact between citizens and the government. Banks treat it like a hard compliance key because Dutch banks are required to hold the BSN of their customers. Plan around that constraint.

Use this quick picker:

| Your status | What it usually means operationally | Your operator questions (ask before routing invoices) |

|---|---|---|

| Path A: In the Netherlands with a BSN | KYC can be more straightforward because you can provide the identifier banks must hold | "Do you support freelancer use on this plan (personal vs business expectations)?" "What name format will appear on my account for beneficiary matching?" |

| Path B: Relocating soon, no BSN yet | Some banks may start onboarding without a BSN, but you must manage the deadline and any pre-BSN limits | "Can I open without a BSN, and what is the deadline to add it?" Some guides mention ABN AMRO, ING, and bunq as banks that may allow this within 90 days, but you should confirm directly. "Can I receive inbound euro transfers right away, or will you restrict inbound transfers until I add my BSN?" |

| Path C: Non-resident invoicing Dutch clients | Non-residents can have limited choices when opening a bank account in the Netherlands. You may be able to invoice using a non-Dutch European IBAN, but some payers may refuse certain IBANs | "Will you pay by euro transfer to my IBAN, with the invoice number in the reference?" "Do you require a Dutch IBAN for vendor setup?" |

If you run Path B, keep your existing EU IBAN live on invoices until the bank confirms, ideally in writing, the BSN deadline and whether the account can receive inbound euro transfers without restrictions.

Edge-case prompt: residence permit and W documents#

If you hold a W-document, don't guess what a bank will accept. A W-document is a Foreign Nationals Identity Document (Vreemdelingen Identiteitsbewijs) with Type W or Type W2. Leave to remain (W-document) cards go to asylum applicants awaiting a final decision.

Your script to the bank (copy, paste, send): "I want to open a Dutch bank account. For ID and status, I have [document type]. Which document types do you accept for identity and for Netherlands address proof, and do you require a BSN at onboarding or within a set timeframe?"

What documents do you actually need - and which ones get rejected?#

Bring (1) valid ID, (2) proof of your Dutch address, and (3) your BSN if you have it. Banks vary, but those are common inputs in Dutch onboarding flows. Once you pick your path, stop guessing and build a document pack that survives first review and follow-up checks.

The document pack (operator-safe defaults)#

Banks vary, but several Dutch-facing guides converge on a few repeat requirements:

| Document type | What "good" looks like | Notes you should plan for |

|---|---|---|

| Identity document | A valid passport or national ID that you can photograph clearly | Some identity checks require a photo, sometimes with a selfie, of your Dutch ID card, residence permit, or international passport. |

| Proof of your Dutch address | An official document showing your Netherlands address, for example a tenancy agreement, rental contract, or statement from your landlord | Many checklists specifically call for official proof of address. |

| BSN (Citizen Service Number) | Your BSN when available, recorded consistently in your admin | Some banks may let you open without it if you provide it within 90 days. This is often mentioned for ABN AMRO, ING, and bunq, but you should confirm directly. |

| Residence status (when applicable) | Dutch residence permit | Bring it when your status makes it relevant, including some non-EU/EEA student situations. |

One scenario-specific edge case: if you apply through ING as a student before you have a BSN, some university guidance notes ING can still open the account if you bring a specific statement of student registration. Treat that as "bring exactly what they ask for," not a loophole.

"Rejected" usually means "not verifiable": preventable friction#

You can't control every review decision, but you can control clarity.

- Lock identity formatting: Use the same legal name order and spelling everywhere you submit.

- Make the address match exactly: Copy the address line-by-line across documents, including unit formatting and postal code spacing. Consistency beats "close enough."

- Expect "where did the money come from?" questions: Banks may use a risk-based assessment of the origin of the funds. Keep supporting documentation ready so you can answer quickly if asked.

ABN AMRO vs ING: which is "best" for freelancers (without gambling on marketing claims)?#

Pick the bank that minimizes onboarding uncertainty and time-to-cash risk for your exact status, not the one with the loudest expat banking headlines. With your doc pack ready, compare ABN AMRO and ING the way you would compare any other critical part of your stack: by activation path, daily usability, and the things that can keep client payments from landing cleanly.

Use a simple scoring framework (so you don't get listicle'd)#

When you compare Dutch bank accounts, you are really buying three things: an onboarding path you can complete, a usable account you can invoice through, and predictable cashflow.

Use this scorecard and fill it in from official checklists and support answers, not vibes:

| Criteria | What to verify | ABN AMRO (signals to verify) | ING (signals to verify) |

|---|---|---|---|

| Onboarding path | App vs branch. Can you start and finish without BSN? | ABN AMRO's app listing says you can open a personal account in the app, and that you can open a current account using an international passport in many cases. | Some third-party messaging says you can start without BSN and even before you've landed in the Netherlands. Treat that as a lead, then confirm with ING. |

| Plan clarity | Monthly package cost and what "without extra services" means | ABN AMRO BasisPakket Betalen at €4.30/month (standard) | ING OranjePakket at €4.00/month, and OranjePakket met Korting at €3.55/month (both "without extra services") |

| Cashflow risk controls | Any activation holds, payment limits, support escalation path | Ask directly about inbound SEPA Credit Transfer availability and any restrictions tied to KYC/AML completion. | Same questions. Don't assume "approved" means "fully active for client money." |

The questions to ask before you submit (copy/paste script)#

Send this in support chat or email, then save the transcript:

| Question | Confirms | Save |

|---|---|---|

| Can I complete onboarding without a BSN? If yes, what is the deadline to add my Burgerservicenummer? | Whether you can onboard without a BSN and the deadline to add it | Support chat or email transcript |

| Can I receive SEPA Credit Transfer payments immediately after approval, or are there activation holds tied to KYC/AML? | Whether inbound SEPA is available immediately after approval | Support chat or email transcript |

| Which proof-of-address documents do you accept for the Netherlands, and what file formats do you support? | Accepted proof-of-address documents and file formats | Support chat or email transcript |

Safety rule: don't route client payments to a brand-new account until the bank confirms "can receive inbound SEPA with no restrictions," ideally in writing.

Start with the bank's official onboarding checklist, then use support chat to close the gaps. Treat third-party summaries as directional, not definitive.

You might also find this useful: The Best Budgeting Methods for People with Irregular Income.

The cashflow cost model: stop comparing monthly fees and start pricing "time-to-cash"#

Model the real cost of a Dutch bank account as fees + FX leakage + ops time + payment friction, then choose the setup that gets invoices to cleared funds fastest and cleanest. Once onboarding and activation risk are handled, the cheapest monthly plan can still cost you more if it creates slow reconciliations, short payments, or messy FX documentation.

Build a fee impact worksheet that matches your inflows#

Start simple. Build a one-page worksheet you can reuse for any Dutch bank account option, including ABN AMRO, ING, or alternatives. Track volume by rail, then attach the bank's fee schedule to your reality.

| What to track | Why it matters for time-to-cash | Fill it in like an operator |

|---|---|---|

| Inbound payments via SEPA Credit Transfer (EUR) | SCT runs in euros and between accounts in the Single Euro Payments Area, which reduces "what rail did they use?" confusion | Count inbound SCTs per month, note typical invoice size, and record any incoming SCT fees, if any. |

| Card payments | Faster authorization can still create dispute work and refund admin | Count transactions, note dispute handling steps and evidence you need. |

| International wire (non-SEPA) | Wires can route through intermediary banks, and each intermediary may deduct fees, creating short payments and long traces | Count how many clients pay this way, and flag them as "high reconciliation overhead." |

| FX events (non-EUR income) | Conversions create margin uncertainty unless you can see the markup, timestamp, and export a record for tax and audit | Count conversions per month. Require downloadable history showing rate and time. |

For example, a client insists on paying by wire. Your invoice lands short because an intermediary bank deducted a fee. You now burn cycles matching the payment, chasing the delta, and explaining it to your accountant. That cost never shows up in the €4 monthly plan comparison.

Prevent hidden cost traps (and write safer terms)#

Two common traps create avoidable chaos:

- Wire fee split confusion (OUR/SHA/BEN): OUR means the sender pays all transfer fees, SHA means fees are shared, and BEN means the receiver pays all fees. SHA can still lead to deductions before funds reach you, which creates short-paid invoices and reconciliation mess. Default to SEPA Credit Transfer in EUR when possible.

- Intermediary bank deductions on non-SEPA wires: An intermediary bank can sit between the sending and receiving banks. Each bank in the route may deduct its own fee, and the route can vary. Expect variability and design around it.

Operational comparison checklist (run on ABN AMRO and ING):

- Fees: monthly plan, debit card, extra cards, cash withdrawals, incoming and outgoing SEPA.

- FX: visible markup, rate timestamp, exportable conversion records.

- Support: how they handle inbound transfer traces, including reference tracking and investigation workflow.

Margin protection standard (add to payment terms where appropriate): request that clients pay invoices in EUR via SEPA Credit Transfer to your IBAN, and require a single payment reference format, for example the invoice number. This reduces FX ambiguity and helps prevent unmatched deposits.

How do you get paid reliably in the Netherlands (SEPA, iDEAL, and dispute-aware rails)?#

Pick the payment rail that matches your risk tolerance and reconciliation capacity, then enforce one invoice standard and one follow-up workflow. Reliability comes from constraints you enforce, not from hoping every payer behaves.

1) Choose rails by risk profile (and by who pays you)#

A credit transfer is initiated by the payer and moves money from the payer's account to the payee's account. That matters because the payer initiates the payment, so you have less control over how references and payer details show up unless you set clear instructions.

Use this operator matrix:

| Rail | What it is in practice | Operational upside | Primary risk you must design for | Setup dependencies |

|---|---|---|---|---|

| SEPA Credit Transfer (EUR) | Payer-initiated bank transfer to your bank account, for example an IBAN-based transfer | Clean paper trail; simple matching when the reference stays consistent | Missing or messy references create unmatched deposits and slower tracing | You need a bank account that can receive the relevant inbound EUR transfers. Confirm any account or onboarding limits with your bank. |

| Card payments | Customer pays via card through a provider | Checkout-friendly for some buyers | Disputes and chargebacks require proof, policy clarity, and tight refund terms | Processor account, evidence workflows, clear service delivery records |

| iDEAL | Widely used online in the Netherlands and lets customers pay directly through their bank | Familiar for Dutch customers | You must align contracts and eligibility before you promise it at checkout | A PSP provides iDEAL. You typically need an iDEAL contract with a Dutch bank or a Collecting PSP. Non-Dutch organisations can also offer **iDEAL \ |

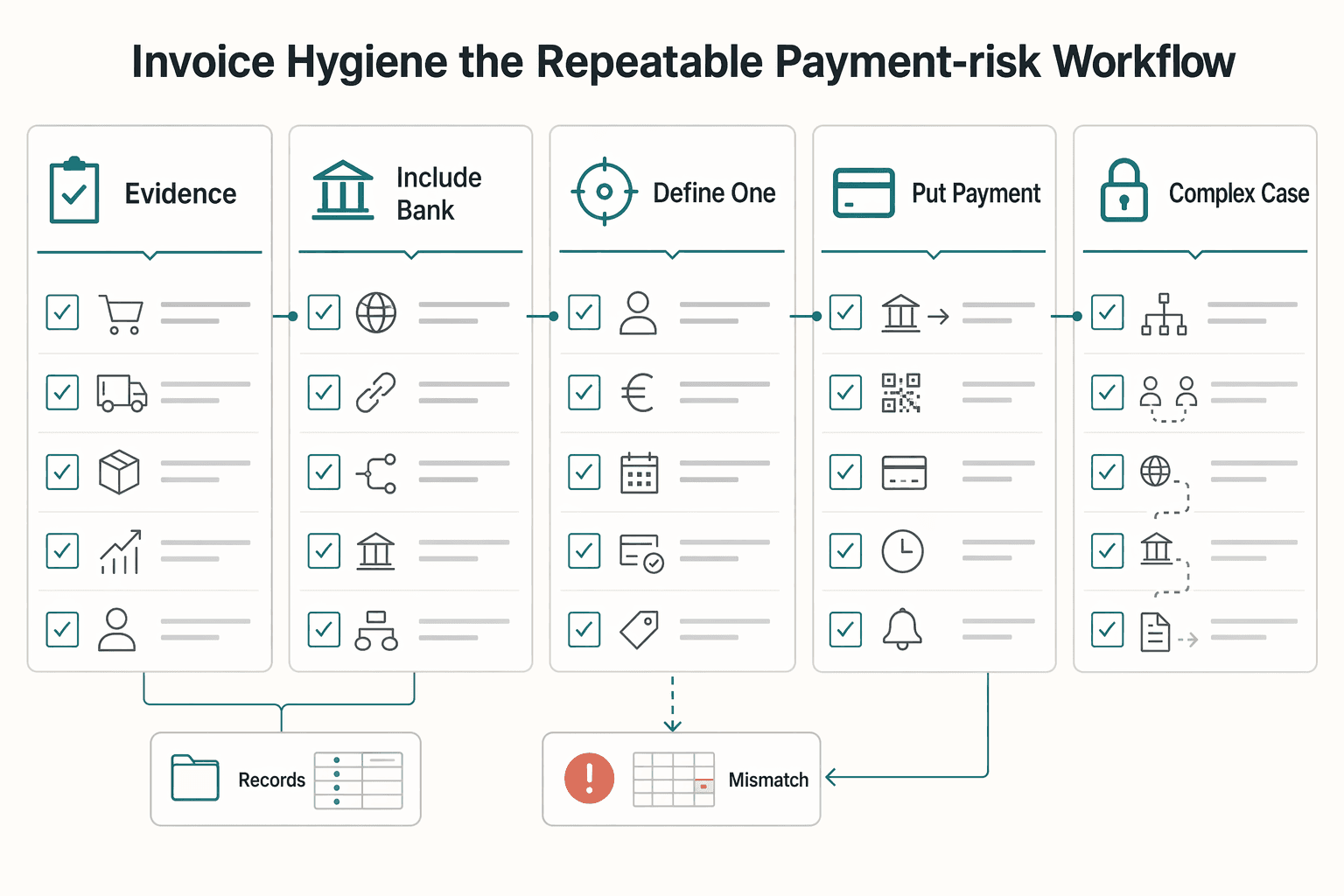

2) Invoice hygiene + the repeatable payment-risk workflow#

Lock an invoice template that reduces human error, especially when you're using a new account for the first real inbound payments.

Invoice hygiene (operator standard):

- Use one legal name format that matches your bank's KYC record. Copy it from your bank profile; don't "pretty it up."

- Include the bank details your payer needs, for example your IBAN, and add BIC if a payer requests it.

- Define one reference rule, for example: "Reference must equal invoice number only."

- Put your payment terms in writing, for example due date and any late-fee language if you use it.

Client-by-client workflow (run it every time):

- Before work: set a deposit + milestone schedule, choose your payment terms, and confirm the payer entity name you will invoice.

- During payment: send the invoice with a single allowed reference format. Schedule reminders before the due date.

- After receipt: reconcile reference to invoice, then store evidence, including bank confirmation and invoice PDF, for audit readiness.

When rules vary, don't guess. Ask your bank or PSP for requirements and limits in writing, especially for iDEAL enablement.

Want a quick next step while you set this up? Try the free invoice generator.

Client says "paid" but nothing arrived - what's your troubleshooting flow?#

Run a two-step flow: classify the rail first, then request the exact trace data your bank can act on. The goal is to turn "we paid" into bank-practical evidence, fast.

Step 1: Classify the payment type (so you don't chase the wrong system)#

Start with one question: "Was this a SEPA Credit Transfer in EUR, or an international wire (SWIFT)?" The rails behave differently, and so do the identifiers your bank will request.

- SEPA Credit Transfer (EUR): Funds are usually credited to the beneficiary's PSP by the end of the next business day. Some banks note it can take until the end of the following banking day to appear, depending on processing variations between banks.

- International wire (SWIFT): Ask immediately for the UETR. With SWIFT gpi, SWIFT payments feature a unique reference, the UETR, which can help banks locate the transfer status across the network.

Step 2: The no-drama checklist (in order), plus an escalation cadence that keeps you sane#

Use this checklist in order. It prevents spirals and keeps the burden of proof where it belongs.

| What you request | SEPA Credit Transfer | International wire (SWIFT) | Why it matters |

|---|---|---|---|

| Invoice PDF (the exact one) | Yes | Yes | Aligns amounts, beneficiary, and reference expectations |

| Proof of payment (screenshot or PDF receipt) | Yes | Yes | A payment receipt gives the bank something to trace |

| Beneficiary details used | IBAN, beneficiary name | IBAN, beneficiary name, BIC if shown | Catches typos and mismatches fast |

| Trace identifiers | Any reference they entered, if any | UETR, sending bank SWIFT details | Gives your bank something concrete to search |

Operator cadence (not a bank rule):

- First message: Request the receipt plus the beneficiary details they used. For wires, request the UETR in the same message. Restate your payment terms and that you'll resume work when funds clear.

- Next follow-up: Ask the client to request a trace from their bank. In parallel, contact your bank with the same packet: invoice, IBAN, beneficiary name, receipt, and UETR if available.

- If it drags: Send a formal payment chase note that references the contract and invoice, and pause scope until resolution.

If you're using a new bank account setup, treat your first inbound payments like test runs.

When funds show as received but unavailable: reply to your bank quickly with the documentation they request, often things like the invoice and contract. Then standardize future inbound patterns, such as the same payer entity and consistent reference, to reduce back-and-forth.

If you can't open a Dutch bank account yet, what's the safest interim setup?#

Use the simplest SEPA-capable receiving path you can operate cleanly today, then layer reconciliation and compliance records so onboarding doesn't block revenue. If you're waiting on a bank decision or missing paperwork, your job is to keep collections stable while reducing future friction.

Decide based on the constraint (paperwork, onboarding, non-local setup)#

Start with a blunt diagnosis:

| Constraint | What it means | Safe default |

|---|---|---|

| Onboarding still in progress | Banks may still scrutinise applications due to strict legislation and acceptance policies | Plan for friction, not speed |

| Local paperwork not ready yet | A bank may ask for documentation you cannot provide yet | Keep a non-Dutch fallback active so cashflow does not depend on one approval path |

| You already have a SEPA-zone business account | You may not need a Dutch bank account just to collect EUR | Keep collecting via your existing EU IBAN until your Dutch account works end-to-end |

In practice, don't make revenue depend on a single approval path. Keep your current SEPA-capable fallback live until the Dutch account works end-to-end, especially if onboarding is still in progress or local paperwork is not ready.

Interim options + risk controls (so you stay paid and audit-ready)#

Use this decision table, then confirm acceptance with each client and test with a small payment first.

| Interim setup | When it fits | Operator tradeoffs | Safe operating rules |

|---|---|---|---|

| Existing EU IBAN (SEPA Credit Transfer in EUR) | You already run an EU account and invoice Dutch B2B clients | Some payers may still push back. That can drift into "IBAN discrimination" if someone cannot make or receive a SEPA credit transfer. | Put the IBAN on the invoice, require EUR via SEPA, and run a test payment before routing a high-stakes invoice |

| Modular stack (collect → track → convert → payout) | You serve many clients and want redundancy if one onboarding stalls | More moving parts, more reconciliation work | Assign one "receiving endpoint" per client type, document every transfer hop, and export statements regularly |

Risk controls during the interim period:

- Don't route a large one-off payment to a brand-new endpoint until you've proven the account works normally for inbound payments and you can access funds without surprises. Stage changes; don't rely on hope that KYC/AML won't trigger.

- Standardize invoice references and payer naming with one reference format and one legal name format. You can't guarantee zero holds, but you can eliminate avoidable ambiguity.

While you bridge the gap, protect runway with a conservative cash plan: The Best Budgeting Methods for People with Irregular Income.

If you want a deeper dive, read Can Digital Nomads Claim the Home Office Deduction?.

Conclusion: your one-hour setup + the reusable checklist you'll use for every client#

Stop optimizing for account opening, and start optimizing for a resilient "Get Paid in the Netherlands" system that survives verification, admin drift, and client-side payment chaos. You now have the rails, including SEPA and iDEAL, and the friction points, including document acceptance, bank onboarding, and BSN context. The final step is to lock the workflow so it runs the same way for every new client.

The focused setup plan (run this as one clean pass)#

1) Pick your path and pre-ask the limits before you route money. Whether you use a Dutch bank account or another provider, treat it as compliance onboarding. Banks perform customer due diligence (CDD), which includes identifying you and verifying your identity using reliable, independent documents or data. Start with a clean doc pack and get clarity on operational limits in writing where you can:

- Identity: passport or ID.

- Official proof of address, such as a tenancy agreement. Confirm what your bank accepts.

- Status documents if relevant: a Dutch residence document (model 2012 or model 2020) for longer stays, or a W-document if you applied for asylum and await a decision.

- BSN number context: BSN is a unique personal number allocated to everyone registered in the BRP. If you do not have it yet, ask what, if anything, changes once you add it.

2) Standardize invoices like an operator. SEPA is designed to make cross-border euro payments as easy as national euro payments, and a SEPA Credit Transfer (SCT) must run in euros between accounts located in SEPA. Your invoice should make paying boring:

- Lock your legal name spelling and formatting, and keep it consistent with your bank profile.

- Always include your IBAN and include BIC if the payer asks for it.

- Set reference rules and reminders. Add payment terms you can enforce, including due date, milestones, and any late-fee language only if appropriate for your contracts.

3) Build a troubleshooting flow before something breaks. If a client claims they paid via wire and nothing arrives, ask for proof of payment and request the UETR, if available. That gives you a concrete reference your bank can use when investigating.

Safe default checklist (copy/paste)#

- I confirmed with my bank whether I can receive inbound SEPA Credit Transfer right now, and I documented any limits, for example holds, caps, or missing info.

- My invoice legal name matches my bank profile exactly, including order and characters.

- Every invoice includes: IBAN (and BIC if needed), a single reference format, a due date, and clear milestones.

- I keep a stored doc pack: ID, official proof of address, BSN (if I have it), plus any relevant residence documents and sample contracts or invoices for verification questions.

Frequently Asked Questions

Can a foreigner open a bank account in the Netherlands?

Yes. Access-NL states that once you have your BSN you can go to any bank of your choice to open a bank account. In practice, banks may ask for more than just identification, so treat this as an onboarding workflow you run end-to-end, not a form you fill once.

Can I open a Dutch bank account without a BSN?

Sometimes, yes, but you must confirm the deadline and the limitations before you route client payments. Access-NL states ABN AMRO, ING, and Bunq offer the possibility to open an account without a BSN if you provide it within 90 days. ABN AMRO also states you need to provide your BSN within 120 days to enjoy the full benefits of their services. Ask in writing whether inbound SEPA Credit Transfer works before you provide your BSN, and what changes after you add it.

What documents do I need to open a bank account in the Netherlands as a foreigner?

Start with the non-negotiable: KVK (Netherlands Chamber of Commerce) says most banks will at least ask for a valid proof of identification. In practice, banks may also ask for additional documents (for example, proof of address), and some banks that let you start without a BSN still require you to provide it later. Bring clean, matching records (same legal name and address format across documents) to reduce back-and-forth.

How long does it take to open a Dutch bank account (really)?

No one can promise a universal timeline because banks control verification and may request more documents mid-process. Separate "application submitted" from "account fully usable for getting paid," especially if you still wait on a BSN or other documents. Keep a SEPA-capable fallback active until you successfully receive and reconcile a test payment.

Which bank is better for expats/freelancers: ABN AMRO vs ING?

Neither wins by default. Score them against your constraints (BSN timing, your document situation, and how quickly you can run a test inbound transfer). Access-NL indicates both ABN AMRO and ING may allow opening without a BSN if you provide it within 90 days, but policies and account limitations can differ. Pick the bank that gives you the clearest written answer on: "Can I receive SEPA immediately, and what changes when I add my BSN?"

Do I need a Dutch bank account to get paid by Dutch clients?

Not always. Business.gov.nl states: "If you already have a business bank account in the SEPA Zone, you do not need to set up a new one." De Nederlandsche Bank also explains SEPA enables cross-border euro payments "at no extra cost" compared with domestic payments within SEPA, which supports using a non-Dutch IBAN when your client can pay via SEPA.

What is iDEAL and do I need it for my business?

iDEAL is "the most widely used online payment method in the Netherlands," allowing people to pay directly through their bank (per iDEAL). You don't need iDEAL for every business, but it can matter if you sell to Dutch consumers who expect it at checkout. Hypothetical: if you run B2B consulting, prioritize clean SEPA invoicing first. If you run a consumer shop, evaluate iDEAL earlier because it can influence conversion.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- abnamro.nl/en/personal/payments/open-an-account/index.htmlexternal

- government.nl/topics/personal-data/citizen-service-number-bsnexternal

- iamexpat.nl/expat-info/money-taxation/banking-in-the-net...external

- ing.nl/en/personal/payments/bank-accounts/open-an-a...external

- westernunion.com/blog/en/nl/opening-a-bank-account-as-a-forei...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

The Best Budgeting Methods for People with Irregular Income

Budgeting with irregular income works better when you separate "money arriving" from "money you're allowed to spend," then run the same transfer routine each cycle.