Quick Answer

Yes, you can often open bank account germany foreigner, but outcomes depend on profile fit, document fit, verification, and activation timing. The practical target is a usable Girokonto with a live German IBAN for inbound transfers, not just an approved application screen. Confirm whether Anmeldung is required, when transfers can be received, and which step unlocks full use. Keep a temporary receiving route active until the first inbound payment is posted.

Opening a Bank Account in Germany as a Foreigner Without Cashflow Surprises#

Run this in two tracks from day one: bank onboarding and payment continuity. The goal is to get a usable Girokonto without creating a gap in inbound client payments while approval is still in progress.

If you depend on client payments, predictable incoming payments come first. In practice, a Girokonto supports day-to-day money movement, and the IBAN is central for getting paid and covering local bills. The linked debit card matters once the account is active for daily use.

There is no universal checklist for foreign applicants. Requirements vary by bank, applicant profile, and country of application. Some providers let you start online from abroad, but not from every country, and non-resident cases can face extra friction.

Decision checkpoints before any application#

| Checkpoint | What to confirm | Article note |

|---|---|---|

| Country access | Can you start onboarding from your current country? | Some providers let you start online from abroad, but not from every country. |

| Usability timing | When can the IBAN actually receive transfers? | If a payment deadline is close, prioritize the option most likely to accept inbound transfers sooner. |

| Card readiness | When does the linked debit card become usable? | The linked debit card matters once the account is active for daily use. |

| Costs | Use monthly cost as a screening item; some guides show 0 to 20 euros per month, but that range is not universal. | Optimize fees after your payment flow is stable. |

- Confirm country access first: can you start onboarding from your current country?

- Confirm usability timing: when can the IBAN actually receive transfers?

- Confirm card readiness: when does the linked debit card become usable?

- Confirm costs as a screening item: some guides show

0to20euros per month, but that range is not universal.

If a payment deadline is close, prioritize the option most likely to accept inbound transfers sooner, then optimize fees after your payment flow is stable. Keep these four checks in one note per bank so you can compare options side by side instead of relying on memory. For contract hygiene while your payment setup is still settling, you might also find this useful: How to Use a Letter of Intent (LOI) in a Freelance Engagement.

Build the Mental Model Before You Apply#

Treat readiness as four gates, not one form submission: profile fit, document fit, verification fit, and activation fit. If any gate is incomplete, processing can stall.

For this guide, your target is a usable account, not just a submitted application. The practical question is not only whether you can start an application, but when the account is fully usable.

Checklist requirements can vary by applicant track, so confirm the exact checklist before you apply. Even when a process starts online, verification may still include in-person steps.

Check the four gates before you apply#

- Profile gate: confirm your exact applicant track.

- Document gate: confirm required files, consistency, and whether certification is required.

- Verification gate: confirm whether in-person steps are still required.

- Activation gate: confirm when IBAN details are issued and what must happen before full use.

One checklist for foreign minor students shows how profile-specific this can get. It requires in-person embassy or consulate attendance with both parents, certified documents, and two printed form copies. In that same flow, IBAN and BIC are sent after successful opening, and applicants must then transfer the minimum balance and service fee.

Execution quality matters. In that checklist, incomplete or incorrect applications cause delays, and changing form structure can trigger rejection. If your timeline is tied to visa steps, apply early and track dependencies so account setup is completed when you need it.

A useful operating habit is to mark each gate as open or blocked before you submit. If profile fit is clear but document fit is not, pause and fix the pack first. If documents are ready but activation details are vague, ask the bank to define the exact step that unlocks full account use.

Map Your Eligibility Profile Before Choosing a Bank#

Map your profile first, then compare bank features so you can deprioritize options that may not match your case.

Use a practical first split: EU resident, Non-EU resident, newly arrived in Germany, student, or business owner. Treat this as a screening tool, not a prediction of approval. For higher-uncertainty cases, prioritize banks that publish clear onboarding language for your profile.

If you invoice across borders, include VAT context in the same prep note. The cross-border SME scheme uses a Union turnover cap of EUR 100 000 for the current and previous calendar year. Certain cross-border B2C e-commerce supplies use an EU-wide EUR 10 000 threshold. Under OSS, registration is in one Member State of identification. For complex transactions, CBR can be used to request an advance ruling in the participating EU country where you are VAT-registered.

These are tax-context checks, not bank-approval rules. They can still help you validate fit before applying.

| Profile signal | Why it matters before applying | What to verify on the bank policy page |

|---|---|---|

| EU vs Non-EU status (if the bank distinguishes this) | May change onboarding steps or documents depending on bank policy | Exact wording for your nationality and residence status (if listed) |

| Cross-border activity | Affects compliance and payment needs | Whether the account supports your expected payment pattern |

| VAT setup | Shapes reporting and transaction context | Any account-use limits tied to business activity |

Before submitting, keep one note per bank with your exact profile lane and VAT-registration country, the policy page date and matching wording, any profile restrictions or country limits, and any stated onboarding route for your profile.

Forum claims are weak evidence. If the bank policy page does not confirm the claim for your exact profile, do not use it as a decision input. A short profile map up front can save time compared with recovering from a failed first application.

Assemble the Document Pack That Prevents Rework#

Build one complete, provider-matched document pack before you apply. Incomplete or mismatched files can create avoidable back-and-forth, so prepare for one clean submission in your chosen lane.

Build a policy-matched pack#

- Start with the documents your chosen bank explicitly lists for your profile.

- Add lane-specific evidence only when the provider requires it, such as student-path financial-stability proof in visa or residence steps.

- Keep one clean digital upload set, and use the same final versions in every submission channel your route uses.

A useful context check comes from a non-official source: one guide describes blocked accounts as required for international students and some visa applicants, and says non-EU citizens may need to show financial stability before entering Germany and before visa or residence-permit issuance. Treat that as visa context, not a universal rule for every current-account path.

Another directional signal from a separate commercial source is that mortgage decisions may weigh financial profile and income stability more than nationality. This is not a current-account onboarding rule, but it supports a practical move: make income evidence clear early instead of relying on profile labels alone.

Evidence checkpoint before submit#

| Check | Requirement | Risk note |

|---|---|---|

| Name consistency | Same spelling and order across all documents and forms | Inconsistent files can create avoidable back-and-forth. |

| Date consistency | No conflicting issue or validity dates | Mismatches can create avoidable back-and-forth. |

| File consistency | One final version per document type with clear filenames | Do not mix old and new file versions during resubmission. |

| Channel consistency | Use the same final set across each submission channel you choose | Keep the same final versions in every submission channel your route uses. |

- Name consistency: same spelling and order across all documents and forms.

- Date consistency: no conflicting issue or validity dates.

- File consistency: one final version per document type with clear filenames.

- Channel consistency: use the same final set across each submission channel you choose.

If timing is tight, submit only when one primary application is complete, then keep a fallback option ready with the same verified files. Do not mix old and new file versions during resubmission, because mismatches can cause avoidable back-and-forth.

If you want a deeper dive, read Can Digital Nomads Claim the Home Office Deduction?.

Decide What to Start From Abroad and What to Defer#

Protect cashflow by splitting setup into two lanes: complete location-independent work before moving, and defer only the steps that need German registration or local delivery.

| Task | Start abroad or defer | Practical reason |

|---|---|---|

| Shortlist banks and check profile fit (EU/Non-EU, permit purpose, student or self-employed path) | Start abroad | Avoid applying to options that do not match your profile. |

| Pre-fill application data and prepare passport plus address documents | Start abroad | This cleanup is high effort and does not require being in Germany. |

| Final checks that may require proof of address registration (Anmeldung) | Defer until local registration is complete | Some onboarding steps depend on proof of German address registration. |

| Card delivery and first activation that may depend on local delivery | Defer | Delivery can affect when full usability starts. |

| Core local payments through a Girokonto (rent, salary, routine debits) | Defer until fully active | A checking account is usually central to everyday local payment flows. |

Treat your first days after arrival as admin-critical. Anmeldung timelines can be tight, and appointments may be hard to secure, so plan this step early and keep documents ready.

Do not assume every provider follows the same pre-arrival sequence. Some foreigners can open an account shortly after address registration, but that does not mean every bank supports the same path. Ask each bank which exact step needs local proof and whether use is limited before that step clears.

If a client payment is due soon, choose certainty over convenience. A temporary receiving path may bridge the gap while local onboarding finishes. Confirm it works for your profile and payment type before using it on live invoices.

Use this rule for timing and cutover:

- Mark your next payment due date and latest safe receive date.

- If that window is tighter than your realistic registration and activation window, activate a temporary receiving path now.

- Continue the primary German account application in parallel and complete local proof steps as soon as registration is issued.

- Switch billing details only after you verify inbound payments are landing as expected.

This split keeps pressure off the wrong step. You can make progress before arrival without pretending activation risk has disappeared, and you avoid sending first invoices to an account path that is not fully live.

Choose Online Convenience or Branch Certainty on Purpose#

Choose your channel based on verification clarity, not signup speed. Online-first can work when each verification step is explicit before you apply. For immigration-linked cases, branch support may be worth considering when document-review steps are unclear.

For visa-linked cases, keep one distinction clear. A blocked account is a special account used as financial proof in certain situations, including international students and other visa applicants. The same evidence set says non-EU citizens may need to prove financial stability before entering Germany, and that this can matter before visa or residence-permit decisions. That does not mean every foreigner opening a standard current account needs a blocked account.

Use this checkpoint list before you choose online-first or branch-first:

- Confirm your profile details in writing, including EU or non-EU status, visa context, and permit stage.

- Confirm what usable means at that bank: account opened versus fully verified for incoming payments.

- If PostIdent appears in your flow, ask exactly where it sits and whether activation depends on it.

- If your case includes visa-stage financial proof, ask when blocked-account documents are reviewed.

- Pick the route most likely to be fully usable before your next payment deadline.

Plan for timing uncertainty between application, verification, and full activation. Keep any temporary receiving path active until your main account is confirmed as fully usable.

If the bank cannot explain the full activation path in plain language, treat that as a risk signal and move to your fallback route. Clarity before submission is often more useful than marketing claims about convenience.

Use a First-14-Days Sequence Instead of Random Applications#

Use an early sequence as guidance, not a guaranteed timeline. Clear dependencies first, then switch payment flows only after the account is actually usable.

Start with document consistency and any local prerequisites that apply to your case. Then run one clean primary application from start to finish: if your bank uses an online flow, open the form, complete it carefully, and use an email address you can access throughout setup.

After submission, complete the verification step the bank assigns without delay. Treat this as an activation gate, not a minor admin task.

Before moving invoices or household payments, confirm stable account access and that the account is ready for regular use. One advisory source notes that rent, utilities, internet, and insurance are commonly paid by transfer, so switch payment details only when your account is usable.

Use one decision rule: if verification is still incomplete, keep your temporary receiving route active. If verification is complete and the account is usable, switch payment details once and keep the rest of your setup stable.

Avoid random multi-bank submissions during this period. A cleaner path is one primary application, one fallback option, and one clear switch point once your main account is usable.

Catch Rejection Triggers Early and Reduce Them#

Start with one red flag: do not use VAT guidance to predict retail bank approval. VAT Cross Border Rulings, the cross-border SME scheme, and OSS are tax tools, so using them as onboarding signals creates avoidable errors.

The SME EUR 100 000 threshold and the 35 working days process window are VAT administration markers, not bank-account acceptance criteria. Keep those numbers in your tax process only.

Use this quick control set before acting:

- Keep tax and banking decisions in separate checklists.

- Treat EU VAT pages as tax references, not onboarding rules.

- For VAT operations, align steps with the relevant scheme guidance (for example, OSS registration/declaration/payment or SME scheme eligibility and notification).

Use one mitigation rule when VAT and onboarding decisions overlap:

- Decide the VAT path first (CBR, cross-border SME scheme, or OSS, as applicable).

- Change one variable at a time in your tax workflow.

- Reassess after each confirmed VAT step before making additional process changes.

A common mistake is mixing tax-process fixes with unrelated onboarding strategy changes at the same time. Apply one VAT correction first, then reassess so you can see what changed.

Build a Reliable Get-Paid Setup for Freelancers After Opening#

Treat your new account as a payment setup, not a finished task. Keep a backup receiving path active until the first live client payment lands, then tighten intake and payout discipline.

| Control | Rule | Timing or risk |

|---|---|---|

| Invoice reference | Include one unique invoice reference for the client to place in transfer remittance data. | Use one tracked intake path for every invoice. |

received status | Mark a payment as received only after the booking appears with matching amount and reference. | Do not rely on a client saying funds were sent. |

cleared for payout status | Mark cleared for payout only after settlement is confirmed, not when a client says funds were sent. | Schedule outgoing obligations from settled cash, not initiation signals. |

| SEPA direct debit | Keep the signed mandate linked to the invoice. | Flag the payment as refundable for the first 8 weeks. |

| SEPA credit transfer | Electronic submissions are generally processed within one banking business day; paper submissions can take up to two banking business days. | Treat confirmed bank settlement records as the trigger for payout release. |

| SEPA remittance format | SEPA Extended Remittance Information supports 140 unstructured characters and up to 999 structured entries of 280 characters. | Standardize remittance data early for cross-border clients. |

Start by separating account opening from payment operations. A Girokonto supports incoming transfers and routine outgoing payments, but approval alone does not prevent cashflow mistakes.

Use one tracked intake path for every invoice:

- Include one unique invoice reference for the client to place in transfer remittance data.

- Record expected amount, payer legal name, due date, and expected rail before payment is sent.

- Mark a payment as

receivedonly after the booking appears with matching amount and reference. - Mark

cleared for payoutonly after settlement is confirmed, not when a client says funds were sent. - For SEPA direct debit, keep the signed mandate linked to the invoice and flag the payment as refundable for the first 8 weeks.

Schedule outgoing obligations from settled cash, not initiation signals. SEPA credit transfers are generally processed within one banking business day for electronic submissions, while paper submissions can take up to two banking business days.

Apply extra caution to direct debit inflows. Because payers can request a refund within 8 weeks, use a short holding period before committing non-reversible payouts against that intake.

Where supported, pair local banking activity with Gruv modules so invoice collection status and payout decisions stay traceable. Use Gruv for internal tracking, and treat confirmed bank settlement records as the trigger for payout release. For SEPA credit transfers from cross-border clients, standardize remittance data early: SEPA Extended Remittance Information supports 140 unstructured characters and up to 999 structured entries of 280 characters.

Run reconciliation on a fixed cadence and keep an evidence pack per paid invoice: invoice copy, booking entry, remittance details, payout approval, and payout confirmation. This supports GoBD-aligned electronic bookkeeping and can speed dispute handling. If booking data, invoice references, and payout records do not match, pause new payouts until records align.

When volume increases, keep the same logic instead of adding complexity. One intake path, one settlement check, and one payout release rule are often enough to reduce avoidable payout mistakes.

Related: Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe. Want a quick next step for "open bank account germany foreigner"? Try the free invoice generator.

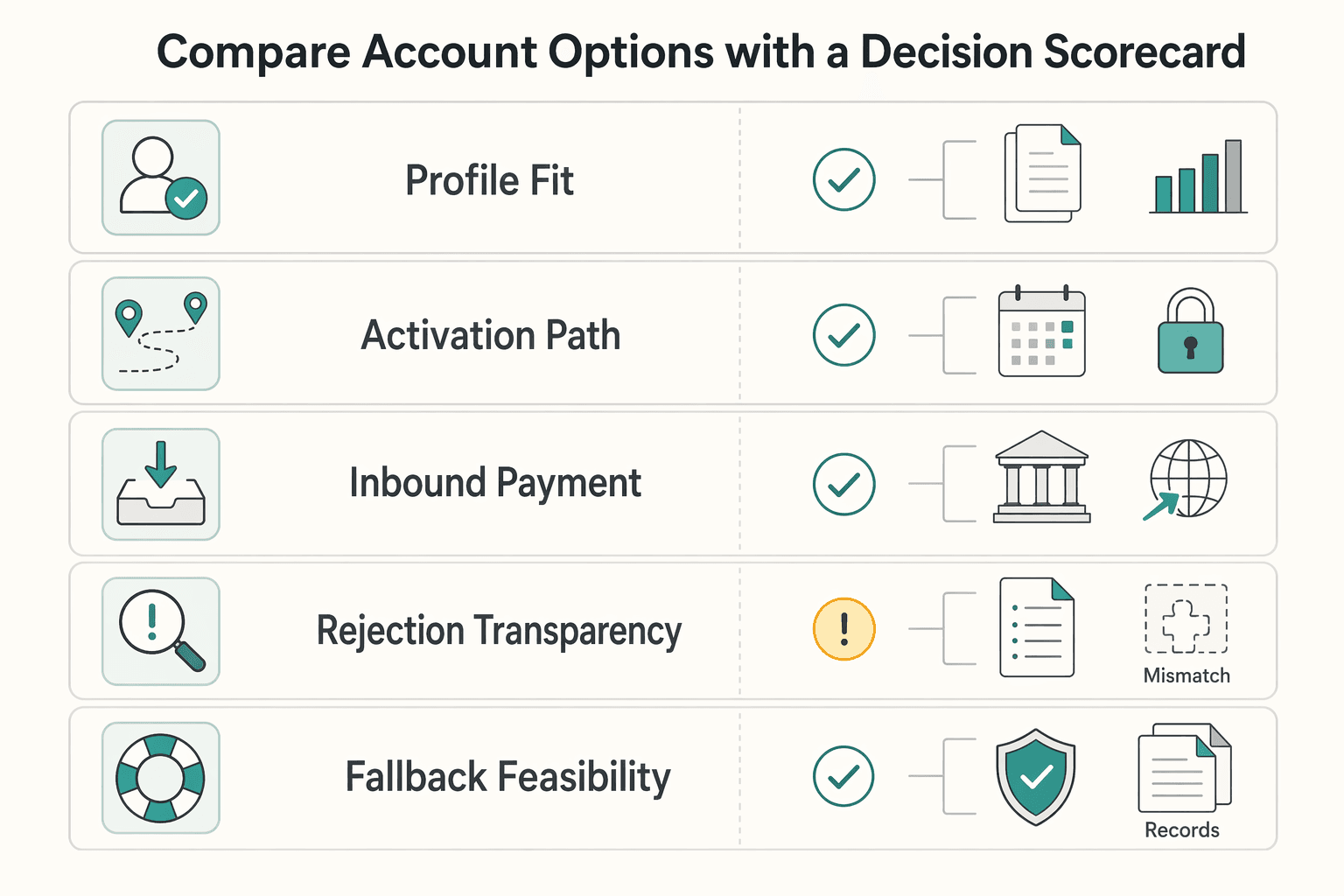

Compare Account Options With a Decision Scorecard#

Choose the account that minimizes payment interruption risk, not the one with the fastest-looking signup.

Before scoring options, separate tax-policy items from banking onboarding decisions. VAT Cross Border Rulings, OSS, and the cross-border SME scheme are VAT-planning topics, while account acceptance is a separate onboarding decision.

Use a simple 0-2 scorecard and require written evidence for every 2.

| Criterion | What to verify | Score guidance | Red flag |

|---|---|---|---|

| Profile-fit clarity | Are document and profile conditions clearly stated for your case? | 2 = explicit criteria, 1 = partial guidance, 0 = vague copy | You are guessing from ads or forum posts |

| Activation path clarity | Is the verification and activation path clear before applying? | 2 = clear upfront, 1 = appears late, 0 = unclear | You cannot identify what blocks activation |

| Inbound payment readiness | Can you confirm a small live inbound transfer after opening? | 2 = tested and recorded, 1 = planned only, 0 = no test plan | First client invoice goes out before a live test |

| Rejection transparency | Are likely rejection categories and next steps explained? | 2 = clear reason categories, 1 = generic responses, 0 = no clarity | Reapplying with unchanged documents |

| Fallback feasibility | Is a second receiving route active until the first live payout clears? | 2 = ready and tested, 1 = exists but untested, 0 = no fallback | One onboarding failure stops collections |

Keep a short decision file per option: criteria snapshot, verification-path notes, rejection-handling response, and inbound test result. Score all options in one sitting using the same evidence standard so the comparison stays fair.

Final rule: if a faster option has unclear rejection handling or no tested fallback, choose the one with clearer criteria and a verified intake path.

Plan Your Fallback Path Before You Need It#

Set your fallback path before you apply, so a rejection or delay is less likely to interrupt collections.

If onboarding is declined or paused, work from records, not memory:

- Request the reason in writing.

- Log exactly what you submitted and when.

- Fix one documented issue at a time.

- Avoid parallel retries with unchanged documents.

- Reapply once with a clear note of what changed.

Use a temporary Wise route as a continuity bridge while you repair the primary setup. Wise says pricing is pay-as-you-use with no subscriptions, account registration is free, and receiving account details in 24 currencies is free. Treat this as a continuity bridge, not a guaranteed acceptance path for German onboarding.

Price that bridge before routing volume. Wise says fees can start from 0.57% and that it uses the mid-market rate. It also shows ATM terms with a 100 USD monthly allowance and 2 or less withdrawals in that tier. After that, it applies +1.50 USD per withdrawal and a 2% component where applicable. Check your exact corridor before sending invoices.

Keep verification hygiene tight. For U.S. government guidance, confirm https:// and domain markers like .gov or .mil. If you use eCFR text, note that it is authoritative but unofficial in your decision file.

Final rule: fix one blocker, submit one clean reapplication, and keep the temporary route active until your primary account flow is stable. This helps protect revenue while you repair the main path instead of hoping a second identical submission will be treated differently.

The Practical Next Step for a Low-Risk Start#

Pick your profile lane first, then choose one primary bank path and one fallback before you submit anything. This is a lower-risk way to manage a process where requirements can vary by bank and applicant profile.

Start with profile fit, not signup convenience. EU and non-EU applicants can face different requirements, residence may be mandatory in some cases but not all, and online opening is not guaranteed across banks.

| Decision point | Primary path | Fallback path |

|---|---|---|

| Profile lane | Bank path aligned to your applicant profile | Path with clearer handling of extra document review |

| Residence evidence | Works with your current residence proof | Works after additional local proof is issued |

| Onboarding channel | Online when requirements are explicit | Non-online or mixed channel when online completion is unclear |

Build one complete evidence pack before first submission. For individual applications, a common baseline is valid ID (usually a passport) plus a certificate of residency that can be obtained from the local Residence Registration Office (Einwohnermeldeamt). Some account types may also require a payment statement and a work permit. For company accounts, include proof of company registration.

Use a practical execution sequence:

- Keep legal name and address consistent across all documents and form fields.

- Submit the primary application with the full pack.

- Respond to verification requests in one complete update.

- Activate the fallback path only after a documented blocker or clear stall.

Treat account opening as part of cashflow continuity, not a one-off admin task. Keep your current receiving route active until the new account is usable. Planning figures like approximately 3 working days or monthly fees starting around 3€ can help you budget, but they are estimates, not guarantees.

If you need one final filter, use this: choose the path with the clearest activation requirements and the safest payment continuity plan. That can produce fewer surprises than choosing purely on speed or headline cost.

Frequently Asked Questions

Can a foreigner open a bank account in Germany, or only residents with local paperwork?

A foreigner can often open an account in Germany, but there is no single rule that applies across all banks. A German account is not always essential, yet it can make local bill payments and getting paid for work easier. Treat eligibility as bank-specific and profile-specific.

Can I open a German account before moving, or do I need to wait for Anmeldung?

Opening from abroad can be possible, but it is often harder before arrival. A common blocker is proof of residence, including a local German address and often a registration certificate such as Anmeldung. Plan for extra checks instead of assuming pre-arrival approval.

Do I always need Meldebescheinigung, or can some banks proceed without it?

Do not assume one universal document rule. Banks commonly ask for residence proof, but the exact document they accept can vary by provider and applicant profile. Confirm the required residence document names with your bank before you apply.

Which documents are typically required besides a Passport?

A common additional requirement is proof of residence with a local German address. Some banks may also ask for a registration certificate, and digital onboarding can include document upload plus ID verification.

Is fully online opening realistic with N26 or DKB Bank, or should I expect branch steps?

Fully online onboarding can be realistic for some applicants, but it is not guaranteed for everyone. Digital banks such as DKB are described as offering app-based opening, document upload, and ID verification, while availability for foreign nationals should be checked first. N26 also markets opening from abroad with minimal paperwork, so confirm your exact path in advance.

Can I use a foreign account long-term instead of getting a German IBAN?

In some cases, yes, because a German account is not always essential. In practice, a local account can reduce friction for paying local bills and receiving payments in Germany.

What should I do first if my application is rejected or delayed?

Rejections and delays are bank-specific. First, confirm whether the account option is available for foreign nationals and which residence documents are required for your profile. Then update those items and reapply based on the bank's instructions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- ecfr.govtrusted

- europa.eutrusted

- home.wvlegislature.gov/committee/house-judiciarytrusted

- oag.maryland.gov/resources-info/Documents/pdfs/Opinions/1932/...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- wise.comtrusted

- commenda.io/germany/opening-a-business-bank-account-as-a...external

- deutscheskonto.org/en/account/open-online-current-account-germanyexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

How to Use a Letter of Intent (LOI) in a Freelance Engagement

**Use an LOI to align on preliminary terms now, while clearly separating "intent" from anything that binds immediately.** If you came here looking for freelance LOI guidance, start with the safe baseline: keep the document genuinely preliminary, and do not let it quietly become the contract you meant to negotiate later.