Quick Answer

Yes, some foreigners, including some non-residents, can open a bank account in Cyprus, but approval depends on the bank and your documents. The least painful route is to choose the right setup for your payment rail, prepare an audit-ready KYC and AML pack, and keep invoices, payer names, and transfer references consistent. Plan for online onboarding to sometimes end with a meeting or branch follow-up.

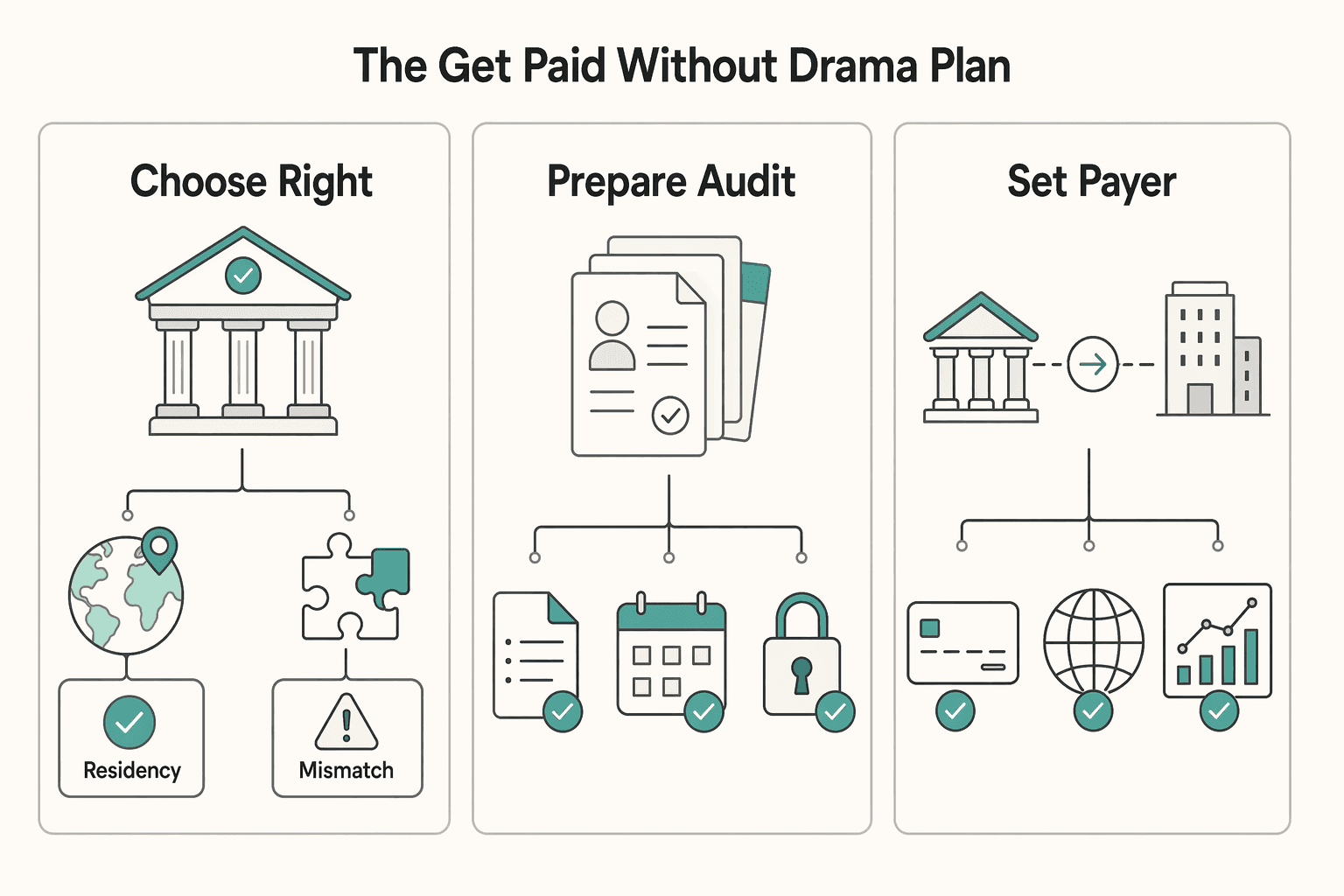

Opening a Bank Account in Cyprus as a Foreigner: the "Get Paid Without Drama" Plan#

To open a bank account in Cyprus without cashflow chaos, treat it as a payments system build, not a one-off admin task. You're the CEO of a business-of-one, and this is one of those unsexy systems that decides whether your month runs smoothly or turns into a support-ticket grind. The plan is simple: optimize for getting paid predictably, then pick the account setup that matches your risk profile and paperwork reality.

If you're a freelancer, creator, or small team, the real issue usually isn't "can I get a Cyprus bank account?" It's whether you can receive client funds reliably without avoidable delays, unclear fees, or compliance back-and-forth that stalls your month. Banks and fintech providers run on compliance, and they do not reward improvisation.

This guide uses a risk-first system built on three ideas:

- Choose the right rail for the job (bank vs EMI vs a workflow that uses both).

- Prepare an audit-ready KYC/AML pack so you answer questions once, not 12 times.

- Set payer and invoice rules that keep your incoming payments clean and easy to reconcile.

The compliance reality (and how to use it)#

KYC (Know Your Customer) is the process of verifying customer identity and assessing risk as part of compliance. AML (anti-money laundering) covers laws and procedures designed to prevent criminals from concealing illegal funds. In practice, expect questions about who you are, what you do, and where money comes from. Banks also use a risk-based approach, where customer relationship risk depends on the facts and circumstances of that relationship.

Your operator move: write a reusable source of funds narrative you can paste into forms and emails. Keep it boring and verifiable (example: "I provide UX design services to B2B SaaS companies. Clients pay against invoices. Typical invoice size: EUR X to EUR Y. Main client geographies: EU/UK/US. I can provide signed contracts and invoice history.")

Pick your setup: bank, EMI (Wise), or both#

Use this as a safe default for expat and non-resident banking decisions, then refine it based on your clients and rails:

| Setup | Best for | Tradeoffs | What you must control |

|---|---|---|---|

| Cyprus bank account | Local banking needs and traditional banking workflows | Typically more documentation and compliance questions | Clean incoming flows, consistent payer names, clear business activity |

| EMI (Wise) | E-money accounts and online-first payment workflows (provider-dependent) | Not a bank; regulated differently and can have different processes | Matching legal name, consistent invoice references, disciplined reconciliation |

| Bank + EMI workflow | Resilience and optional separation of "receive" vs "hold" funds | More moving parts | A written rule for which clients pay where, and why |

One concrete example of a bank-led route: Bank of Cyprus states you can open a QuickAccount through Internet Banking or the BoC Mobile app (for eligible 1bank subscribers, aged 18 and over). For an EMI example: Wise states the UK FCA has licensed Wise Payments Limited as an electronic money institution for issuing e-money. Different rails, different rules.

What you do next: pick one primary "get paid" endpoint, build your document pack around it, then set invoice rules so every client payment looks the same on arrival. That's how you reduce drama. Need a practical next step? Try the free invoice generator.

The Mental Model: Rails + Risk (Define These Terms Before You Choose Anything)#

To do this without surprises, separate "payment rails" (how money moves) from "risk/compliance" (why providers ask questions). If you do that upfront, you stop guessing, answer KYC cleanly, and choose the right transfer method for each client.

Rails: IBAN, SEPA, SCT, SWIFT (what moves money, and how)#

IBAN is an account identifier defined by the ISO IBAN standard (ISO 13616-1). In practice, it is the account number format many European payers expect on invoices and bank forms. If your Cyprus bank account or EMI gives you an IBAN, you will use it as the destination identifier for EUR bank transfers.

SEPA (Single Euro Payments Area) is a framework of tools and standards designed to make cross-border euro payments as easy as national payments. The SEPA region consists of 41 European countries (status: 22 May 2025). Inside SEPA, SEPA Credit Transfer (SCT) is the interbank scheme for euro credit transfers with a common set of rules and processes.

SWIFT is different. SWIFT acts as a messaging carrier between financial institutions. It transports payment messages, but it does not hold funds or manage accounts. You will see SWIFT referenced in bank-transfer instructions where banks use SWIFT messages to communicate payment details.

Use this operator table when a client asks, "How should we pay you?"

| Need | Best-fit rail label you'll see | What you give the client | What can slow you down |

|---|---|---|---|

| EUR transfer within SEPA rules | IBAN + SCT | IBAN, account name, bank details, invoice reference | Missing reference, mismatch between invoice name and account holder |

| International transfer messaging | SWIFT | IBAN or account number plus SWIFT code and bank info | Extra information requests, missing or incorrect banking details |

Risk: KYC, AML, source of funds, source of wealth (why they question you)#

KYC (Know Your Customer) means the provider verifies your identity and assesses risk. AML rules aim to detect and report suspicious activity linked to money laundering and terrorist financing. This is why expat and non-resident banking can feel personal. The institution must understand the transaction context.

Two terms you must keep straight:

- Source of funds: the origin of the money used in a particular transaction (example: "Client A pays invoice #1042 for design services.")

- Source of wealth: how you accrued your overall wealth (example: "Income from employment and my registered freelance business over the last X years.")

Operator move: write both statements in plain language and keep them consistent across applications, onboarding calls, and every "please explain this incoming transfer" email. That consistency can reduce friction when you open the account and when payment volume grows later.

What's the Least Painful Path for Your Profile (Bank vs EMI vs Hybrid)?#

The least painful path matches your dominant payment rail (SEPA vs SWIFT) and your compliance narrative (KYC, source of funds, source of wealth) with the fewest moving parts. Use this decision tree to pick a setup you can defend on every onboarding call and every "please explain this transfer" email.

A 10-minute decision tree (pick the path with the cleanest rails)#

Start with how clients pay you, not with whichever provider looks easiest.

- Most invoices are EUR and your clients sit in SEPA: prioritize IBAN + SEPA Credit Transfer (SCT). SCT runs in euros between accounts located in SEPA, and Cyprus sits in SEPA as an EU member state. In practice, a Cyprus bank account often fits cleanly for EU client invoicing if you want a local EU banking setup and straightforward reconciliation.

- You need multi-currency receiving and a single account you can use across countries/currencies: consider Wise (and add a Cyprus bank account later if your volume, counterparties, or operational needs push you there). Wise positions its multi-currency IBAN account as one account that can provide local banking details across multiple countries and currencies, and it states Wise Payments Limited holds authorization as an Electronic Money Institution (EMI) by the UK FCA (registration number 900507).

- You need status visibility and audit-ready collection-to-payout workflows: add a platform layer (for example, Gruv Virtual Accounts, where enabled) so you can assign dedicated receiving details per client, keep deposits traceable, and make invoice matching routine instead of detective work.

Use this quick comparison to decide without overthinking:

| What you optimize for | Bank (Cyprus bank account) | EMI (example: Wise) | Hybrid (EMI + bank + platform layer) |

|---|---|---|---|

| Best when | Clean EUR SEPA billing | Multi-currency workflows | You want clean traceability end-to-end |

| Typical tradeoff | May involve deeper KYC / documentation (including source-of-funds) | Some payers may prefer "traditional bank" setups | More components to maintain |

| Your job | Keep documents consistent | Keep account usage consistent | Define rules (what lands where) |

Personal vs business, and the non-resident reality check#

Choose "personal vs business" based on risk containment. If you invoice like a business, it's often simplest to open as a business. You want the account profile to match reality, supported by contracts and invoices, so your source of funds answers stay simple and repeatable.

Non-resident banking may come with heavier KYC asks. Plan for identity documents and proof of address, and expect requests for source of funds details. Banks may also ask non-residents for a bank reference, so build slack into your timeline and keep a single, consistent story across every institution.

Safe default for cashflow protection: pick one primary receiving endpoint (usually a SEPA-based account for EUR billing), document it in your invoicing template, and add complexity only when you can explain it cleanly.

Your Audit-Ready Document Pack (KYC/AML) - Built for Freelancers and Creators#

To get through onboarding without endless back-and-forth, you need an "audit-ready" document pack that tells one consistent story across identity, address, and money flow. Once you've picked your bank vs EMI vs hybrid path, the job is operational: give compliance what they need to clear KYC and AML without guesswork.

Think "single PDF folder," not "upload whatever they ask for." KYC in Cyprus focuses on verifying identity and assessing risk profile to prevent money laundering and related financial crime. You win by making your narrative obvious on page one.

The core pack (personal or non-resident banking)#

Start with table-stakes documents, then layer in money-flow evidence.

| Pack component | What to include | Operator notes (avoid KYC loops) |

|---|---|---|

| Identity | Valid passport or national ID. | Some app flows require an original passport/ID to proceed. Do not start onboarding until you can meet that requirement. |

| Proof of address | Utility bill or bank statement showing your name and address. | Treat recency as a hard constraint. Enter the exact same address in the form as the document shows (same spelling, same unit number). |

| Source of funds support | Bank statements showing inbound payments. Contracts, client invoices, and other supporting documents that explain the flow of funds. | Organize evidence so it "clearly and transparently shows the flow of funds." Lead with a one-page index: payer, amount range, and why you get paid. |

Non-residents can open accounts, but expect extra checks. Don't argue. Reduce ambiguity by aligning your submitted proof with your onboarding data and your invoice header.

Income evidence that works for freelancers and creators#

Banks often ask for income and source-of-wealth context. Give them a clean sample:

- Recent invoices that match real inbound payments on your bank statement.

- Contracts or SOWs for those clients.

- A short "what I do" summary (one paragraph) describing your services and typical client/counterparty locations.

Business-account specifics: UBO + activity summary

If you apply as a company (even a tiny one), expect Ultimate Beneficial Owner (UBO) identification. Cyprus-focused guidance calls UBO identification a non-negotiable AML requirement. Prepare a simple ownership chart (even "you: 100%") and keep it consistent with your formation documents.

Also plan for "additional information and documentation" requests. That can be part of account opening and AML due diligence. Your goal stays the same: one story, backed by paper.

Tax declarations you'll likely sign: many applicants complete FATCA and CRS self-certifications (tax residence and TIN), collected on a self-certification form, with reportable accounts reported annually. If you are a U.S. person, check whether FBAR (FinCEN Form 114) applies. The cited trigger uses an aggregate foreign account value over $10,000 at any time during the year. Confirm edge cases with a qualified tax advisor.

Finally, treat translation and notarization as bank-specific. In some cases, notarized copies and translation into English or Greek are required. Confirm first, pay second.

Related: Tax Residency in Ireland for Digital Nomads and Tech Contractors.

Can You Open a Cyprus Bank Account Online, or Will It Turn Into "Branch Finish"?#

You can sometimes start the process online, but plan for a human step that may include an in-person meeting. With your KYC/AML document pack ready, the next job is execution: choose an onboarding path that matches your reality, not the marketing headline.

A concrete anchor: Bank of Cyprus promotes digital onboarding for individuals. On its QuickAccount page, the bank states: "You can open an account in your name through the Internet Banking or BOC Mobile app." It also describes app-based verification: "You can open an online account through the BoC Mobile App by completing your digital verification (ID/passport scan and selfie)." That is the practical meaning of "online" here. You get a streamlined start, with identity verification built into the app flow.

Bank of Cyprus also describes a traditional route for account opening. Its international account opening page states: "To open an account, you will need to personally visit of our an International Business Units" and adds that "During the meeting you will be required to present a duly completed Account-opening Questionnaire." Operator translation: even if you hope to open the account online, keep your calendar flexible in case you're routed into a meeting before everything is fully active.

A practical "what it looks like" path (BoC Mobile App)#

Do not over-script the steps. Different customers see different prompts. But you can safely expect the building blocks:

| Action | What to expect |

|---|---|

| Digital verification | ID or passport scan plus selfie in the BoC Mobile App |

| Customer identification changes | Scan the document and take a selfie |

| Address changes | Attach proof of address |

| Meeting follow-up | Present a duly completed Account-opening Questionnaire if you are asked to attend a meeting |

In practice, that usually means digital verification first, document uploads when the app asks for them, and a questionnaire or meeting follow-up if the bank routes you there.

Prep for the interview so you do not contradict yourself#

Your goal in expat and non-resident banking is consistency. Walk in with numbers you can defend, and make sure they match your invoices and portfolio.

Have ready (and keep it identical across forms):

- One-paragraph business description (what you sell, how you deliver).

- Client countries.

- Typical invoice range and expected monthly inbound volume.

- Why you need the account in Cyprus (for receiving client payments and clean reconciliation).

What to say (copy, paste, adapt): "I provide [service] to clients in [countries]. Typical invoices are €[x] to €[y], paid by bank transfer. I can provide contracts, invoices, and proof of delivery as source of funds evidence."

Operator move: Ask the bank, in writing if possible, whether your specific profile can complete onboarding digitally or whether they require a meeting. Also ask for any account fees and minimum balance expectations attached to your customer profile, so the account does not surprise you after approval.

SEPA vs SWIFT in Cyprus: Fees, Timelines, and the Cashflow Gotchas#

When you open an account in Cyprus, you're not just getting an IBAN. You are choosing payment rails, and rails quietly shape your fees, predictability, and support workload. Once onboarding is moving, the next operator move is to route invoices on purpose so cashflow stops "mysteriously" leaking.

Choose rails intentionally (define the job first)#

SEPA (Single Euro Payments Area) lets consumers and companies make and receive payments in euro across borders under the same basic conditions, including within the European Union. SEPA Credit Transfer (SCT) specifically requires the payment to run in euros and both accounts to sit in the SEPA area. If you invoice EU clients in EUR to a Cyprus IBAN, SCT often fits the job cleanly because it stays inside a dedicated euro scheme.

SWIFT is a system banks use to communicate for international payments. Wise notes that when sending money to a bank account outside its originating currency, it usually goes through the Swift network - "a network of banks that help process the payment until it gets to your destination country." That network can create more places for deductions and extra processing steps.

Here is the practical decision frame:

| Your invoice scenario | Default rail to request | What to confirm before you send it |

|---|---|---|

| EUR invoice, both banks in SEPA | SEPA Credit Transfer (SCT) | Sender uses EUR, correct beneficiary details |

| Invoice needs to move outside its originating currency | SWIFT | Whether intermediaries can deduct fees mid-flight, and what the recipient should expect to land |

The three fee buckets to audit (in writing)#

Do not guess. Ask your provider to spell out:

| Cost area | Ask for in writing |

|---|---|

| Account fees | Monthly maintenance, dormancy, and any conditions tied to your account |

| Incoming transfer fees | Receiving fees for SEPA and/or SWIFT, plus whether correspondent fees can reduce the credited amount |

| FX economics | The bank's conversion method and markup if you invoice in USD and land funds in EUR |

- Account fees: monthly maintenance, dormancy, and any conditions tied to your account. Get the schedule, not vibes.

- Incoming transfer fees: receiving fees for SEPA and/or SWIFT, plus whether correspondent fees can reduce the credited amount. ZEN notes that with SWIFT transfers, "correspondent fees and other processing charges may already have been deducted while the transfer was in progress."

- FX economics: if you invoice in USD and land funds in EUR, ask for the bank's conversion method and markup. Do not accept "free transfer" as a complete cost explanation.

Operator tip: Build a "fees and rails" checklist into your client onboarding, right next to KYC. That is how expat banking stops feeling random.

Reduce "pending transfer" anxiety (and card chaos)

Two controls cut stress fast:

- Cutoffs and value dates: ask your bank how postings behave around non-business days, and what timestamp they use for "received."

- Investigation readiness: for SWIFT, keep whatever payment confirmation/reference the sender can provide accessible so you can escalate with specifics.

On cards, remember the asymmetry: a chargeback is a reversal that happens when a customer disputes a card transaction with their bank or card company. NetSuite notes a merchant may have as few as 20 to 45 days to prove a charge was legitimate or accept the loss.

If you accept cards, isolate that flow (separate reconciliation and refund logic) so it does not contaminate your IBAN-based collections. If you need automation help on the card side, use Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Where Gruv fits: if you want tighter traceability, Gruv can help you track deposit statuses (credited, held, returned) for Virtual Accounts (where enabled) and preserve an audit trail that keeps EU banking reconciliation clean when clients pay across multiple rails.

Why Transfers Get Stuck (and How to Clear Holds Fast Without Begging)#

Transfers get stuck because the bank cannot map the money to a clean, documented story (who paid, why they paid, and why it matches your stated activity). Once you've chosen the right rail (SEPA vs SWIFT), the job is to remove ambiguity so compliance does not need to "investigate" you mid-cashflow.

Design around the hold triggers you can control#

A lot of "pending" situations start with preventable mismatches in your metadata and documentation:

- Weak source-of-funds narrative: Banks may ask for information and documents on source or value of wealth during Cyprus account-opening, and they may request additional documentation after initial review. If inbound funds hit your account but you cannot tie them to invoices, contracts, and delivery, you create work for their AML process.

- Payer or beneficiary mismatch: If the payer name (or entity) doesn't match what your invoice and contract say, you can trigger review. In wire contexts, a beneficiary name mismatch can even result in the bank rejecting and returning the wire: "When the beneficiary name doesn't match the account number, the receiving bank should reject the wire and return it automatically."

- Unexpected changes: If your activity changes in a way the bank doesn't understand from your existing file, they may ask questions. You do not control bank risk models, but you can control how well you explain the change.

The review-clearance pack (send it once, send it clean)#

Do not drip documents out for a week. Build a single PDF pack that lets the analyst close the loop fast. Use this as your default whenever a transfer to your IBAN gets held (SEPA Credit Transfer or otherwise):

| Document or note | What to include |

|---|---|

| Contract or SOW | Signed, with scope and dates visible |

| Invoice | The exact payer legal entity name |

| Proof of delivery or acceptance | Email acceptance, final deliverable link, or platform completion screenshot |

| Client entity details | Legal name, address, and website |

| Source-of-funds tie-out | The clearest proof you have that shows the source and movement of funds |

| Short explanation | Transfer amount, payment reference, invoice number, and service period in 5 to 8 lines |

That source-of-funds row matters. bunq's guidance stays practical here: provide "the clearest proof you have that shows the source and movement of funds." Invoices and contracts qualify as common examples.

Include a short explanation (5 to 8 lines) that ties together:

- transfer amount

- payment reference

- invoice number

- service period

Prevention: run a remittance reference system

Payment reference is the note attached to a transfer that tells the recipient what the payment is for. Use it. As NEC Money puts it: "This remittance information tells the payee the purpose of the payment, such as an invoice number."

Practical defaults for cross-border banking workflows:

- Standardize invoice numbers (example:

GRUV-INV-ACME-01). - Ask clients to paste the invoice number into the transfer reference for SEPA Credit Transfer.

- Avoid third-party payments ("my friend will pay you"). Many firms refuse them to comply with AML requirements, and they can complicate reviews.

When the bank asks for "more information," reply with one consolidated PDF plus a bullet summary. Then ask one direct question: "What exactly are you trying to verify, and which document would close it?" That keeps your reply tight, professional, and fast.

The Freelancer "Get Paid" Playbook: Invoices, Payer Rules, and Reconciliation That Survives KYC#

An account stays easy to pay only when every invoice, payment reference, and deposit tells one consistent story that a bank can verify under KYC and AML. Once you understand how holds happen, you prevent them upstream by tightening the inputs clients use when they pay your IBAN.

Invoice terms that reduce delays and disputes (copy, paste, enforce)#

Put these lines on every invoice you send once the account is live (and keep the wording consistent across invoices, contracts, and email threads):

- Payment method line: "Payment via bank transfer to IBAN preferred."

- Beneficiary name line: "Beneficiary name must match the account legal name exactly." This matters because payment failures often come from name mismatches. Mercury's support guidance stays blunt: "Make sure the name on the payment matches the legal name on the account before trying again."

- Terms that create certainty: include a due date (for example, "Due within 7 days"), a late fee clause if you use one, and for new clients a deposit milestone (example: "50% upfront, 50% on delivery"). You reduce disputes by setting expectations before money moves.

Also keep your invoice fields clean. Cyprus VAT invoice requirements include basics like date of issuance, a unique sequential number, VAT number of the supplier, and full name and address of supplier and customer. Even if VAT does not apply to your specific situation, these fields create a stronger paper trail.

Payer rules + a reconciliation system you can defend in 60 seconds#

You do not hope clients pay correctly. You give them a checklist and head off sloppy payments before they happen.

| Control | What you require from the client | Why it helps when you need to explain deposits |

|---|---|---|

| Payer identity | Legal entity name and address (as registered) | Helps you match deposits to the contracting party if you're asked in a KYC follow-up |

| Payment reference | A consistent reference that includes the invoice number | The reference tells you what the payment is for. NEC Money: "This remittance information tells the payee the purpose of the payment, such as an invoice number." |

| Proof bundle | Contract/SOW + invoice + acceptance proof stored together | You answer "why this money" without scrambling |

Reconciliation system (simple, non-negotiable): maintain a ledger with invoice number, bank transfer reference, expected amount, received amount, and received date. Razorpay explicitly calls out the practice of matching the payment reference number and the bank reference number with the corresponding invoice for accurate record keeping. If you collect via more than one transfer type, track them separately so you do not mislabel a normal delay as non-payment.

Source-of-funds narrative template: one paragraph that states your services, typical clients, client geographies, expected monthly volume range, and typical invoice size. Attach a few key contracts, recent invoices, and bank statements that show matching deposits. Wise notes it may ask for invoices from the last 6 months along with bank statements in some cases, so build your filing system to produce that fast.

If you want less ops drag, use tooling that gives you audit-ready records and reconciliation exports. If you already automate parts of your workflow, plug your finance stack into a repeatable system like Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Finally, watch for name confusion in search results: "Cyprus Credit Union" results often refer to a U.S. institution. It even states its savings accounts get insured up to $250,000 by the NCUA. That has nothing to do with opening a Cyprus (EU banking) account, so validate jurisdiction before you follow any eligibility rules.

If you want a deeper dive, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Conclusion: Your Safe Default Setup (and the Checklist to Execute This Week)#

Your safest way to set this up in Cyprus - and actually use it to get paid reliably - is to build the system in a risk-first order: lock your payment rail, get KYC/AML-ready, then tighten invoicing discipline. You now know where applications fail (holds, mismatched stories, incomplete packs). The win is to pick a default you can run without improvising every month.

Start with the rail. If you invoice in EUR, default to SEPA for euro bank transfers. SEPA exists to let customers make cashless euro payments across the EU in a fast, safe, efficient way, which makes it a clean "get paid" setup for EU banking. If SEPA isn't the right fit for a given payment, use another bank transfer method your bank supports for that currency/corridor. This decision determines what your client needs from you (beneficiary details, references, and any extra routing fields) and what questions compliance will ask later.

Next, treat KYC/AML like a project, not paperwork. Banks will ask for identity and address (for example, Bank of Cyprus signals you should have a copy of ID/passport plus proof of residential address). Build a source of funds bundle once, then reuse it: contracts or SOWs, matching invoices, proof of delivery (screenshots, acceptance emails, statements of work completion), and a one-page narrative that explains who pays you and why.

Finally, pre-empt the tax reporting layer. FATCA is a U.S. law that requires certain U.S. taxpayers with financial assets outside the U.S. to report those assets to the IRS. CRS is an OECD automatic exchange of information standard. Banks commonly collect tax residency and TIN via a self-certification form, and Bank of Cyprus states it collects country of tax residence and tax identification number and reports reportable accounts annually. Do not wing it here. Confirm exactly which forms they need for your profile (especially in expat banking and non-resident banking).

Use onboarding as a process (not a hope)#

Operate like this:

- Expect follow-ups. Reply with a single consolidated PDF bundle, not scattered attachments.

- Keep names, addresses, and business descriptions identical across forms, invoices, and your narrative.

- When rules vary by nationality, residency, or bank program, confirm in writing: non-resident eligibility, online vs branch completion (Bank of Cyprus states you need an original passport/ID for mobile app opening), translation/notarization expectations, and any fees or minimum balance requirements they will apply to you.

Short execution checklist (print this)#

- Choose your primary receiving rail: SEPA (EUR) vs another bank transfer method when SEPA isn't applicable.

- Prepare your document pack: passport/ID, address proof, contracts, invoices, proof of delivery, source of funds narrative.

- Define invoice rules: beneficiary name match, mandatory reference format, deposit milestone for new clients.

- Ask the bank for 4 confirmations: onboarding channel, fees, minimum balance, translation/notarization expectations.

- If you need status visibility and reconciliation exports, consider a modular infrastructure layer (e.g., Gruv Virtual Accounts/Payouts, where enabled). Request access or talk to sales to confirm coverage.

Frequently Asked Questions

Can a non-resident open a bank account in Cyprus?

Yes, some non-residents can open a Cyprus bank account, but eligibility is decided by the bank case by case. Expect heavier KYC checks and be ready to show identity, address, and a clear source-of-funds story.

Can I open a Cyprus bank account online as a foreigner?

Sometimes. Bank of Cyprus says some applicants can start digitally in its mobile app, but if you do not have an original passport or identity card you cannot open the account through the app. A safe default is digital start, branch finish if manual review is triggered.

Do I need a Cyprus address to open a bank account?

Do not assume you need a Cyprus address. Banks commonly ask for proof of your residential address, and Bank of Cyprus gives a utility bill not older than 6 months as an example. That is about verification, not necessarily living in Cyprus.

What documents do I need for KYC in Cyprus (and what counts as source of funds)?

Expect KYC to cover identity, address, and your money story. The article lists ID or passport, proof of residential address, and a bank reference as common asks. Source of funds means documents that explain where your money comes from and match your expected account activity, such as invoices, contracts, and supporting statements.

Do documents need translation, notarization, or an apostille?

Some banks ask for translation, notarization, or both, and others do not. Requirements vary by bank and document type, so ask for the exact checklist before you pay. Send scans first and certify only what they reject.

How long does it take to open a bank account in Cyprus - and what causes rejections?

Timelines vary, so plan your cashflow as if onboarding will take longer than you want. Delays and rejections usually come from mismatched names, stale address proofs, missing bank references, or a source-of-funds story that does not match your inflows.

Is SEPA available with Cyprus bank accounts, and when do I need SWIFT?

Yes. Cyprus participates in SEPA, and SEPA covers euro payments when both accounts are within SEPA. Use SWIFT when the transfer does not fit a SEPA euro credit transfer, and remember SWIFT carries the instructions banks use to process the payment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cftc.gov/IndustryOversight/AntiMoneyLaundering/dsio_a...trusted

- federalreserve.gov/frrs/regulations/joint-statement-on-the-risk...trusted

- irs.gov/businesses/corporations/foreign-account-tax-...trusted

- oecd.org/en/publications/consolidated-text-of-the-com...trusted

- bankofcyprus.com/en-gb/Personal/Digital_Channels/campaign/new...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

Tax Residency in Ireland for Digital Nomads and Tech Contractors

Pick one status for the current year in Ireland, then document it so you can defend it. The goal is a position built on records you can prove now, not a perfect answer to every edge case.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.