Quick Answer

Yes, you can often begin from overseas, but treat onboarding as incomplete until three gates are cleared: application lodged, identity or proof review finished, and account usability confirmed for receiving funds. Keep invoices flowing through an already accepted AUD route while full setup continues. Handle GST separately: standard registration requires an ABN, while simplified registration issues a 12-digit ARN with narrower operating limits.

You don't need "a bank account." You need a reliable way to get paid from Australia.#

You may be able to get paid from Australia before full account onboarding is complete. The immediate goal is simpler: usable AUD receiving details, payer acceptance of those details, and records you can reconcile to each invoice. Define that deliverable first, and you lower the risk of cashflow delays while broader onboarding continues.

Different payers can want different things. Some may only need valid payment instructions. Others may not release funds until they see ownership evidence. Others may need a true operating account because refunds, outgoing transfers, or day-to-day treasury are part of the job.

Start with the exact deliverable#

Start with the deliverable, then choose the provider path.

| What you actually need | Decision trigger | Ready when | Red flag |

|---|---|---|---|

| AUD collection details | Your client only needs local or otherwise acceptable AUD payment instructions. | The payer confirms the details work in their AP process, and you have tested the format on a live invoice. | You assume payment details are enough, but procurement also requires ownership evidence or supplier onboarding documents. |

| Proof of banking | AP, procurement, or vendor onboarding requires evidence that the receiving account belongs to you or your business. | You have the exact document format the payer accepts, and the account-holder name matches your contract and invoice. | The document shows a different legal name, trading name, or entity than the invoice. |

| Operating account | You need incoming funds plus ongoing banking activity, including outgoing payments, treasury, or business segregation. | You can access the account, receive funds, and export records for month-end reconciliation. | You only have an application in progress or provisional approval, not a usable account. |

Keep tax identifiers in their own lane. If a client asks for ABN, GST status, or a non-resident identifier, that is separate from the payment rail decision. The ATO states you need an ABN before standard GST registration, and that simplified GST registration is for non-resident businesses that do not need an ABN and do not need GST credits. After simplified registration, the ATO issues a 12-digit ARN. Those identifiers can matter for invoicing and tax handling, but payer onboarding still depends on the payer's requirements.

Keep three lanes separate#

Most avoidable delays come from answering the right question in the wrong lane.

The immigration lane covers visa status and physical presence. Keep it separate from tax registration and provider compliance checks.

The tax lane covers ATO registration and obligations. The ATO states not every business must register for GST, but penalties may apply if registration is required and missed. Once required, registration must be completed within 21 days. The published criteria excerpt includes a $75,000 GST turnover trigger, but do not treat that as the only trigger without checking current ATO rules. If you are unsure how to answer tax-profile questions, pause and check current ATO guidance before submitting details.

The provider compliance lane covers bank or fintech onboarding: identity checks, tax self-certification, and ownership evidence. This is the lane that determines whether the provider will let you use the account or collection details.

Your GST path is one practical decision point. Standard GST registration is for non-resident businesses and requires ABN, identity proof, and BAS lodgment with GST paid monthly or quarterly. The ATO also notes you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. Simplified GST registration is also for non-resident businesses, but only where you do not need an ABN and do not need GST credits. If a payer requires ABN-linked GST functions, that points toward standard registration. If not, simplified may cover tax obligations without solving banking requirements.

Run two tracks instead of one bet#

If payment timing matters, split the work. Use the live AUD collection path your payer already accepts, and keep full account or operating setup moving in parallel.

- Use now

Invoice through the live AUD collection path the payer has already accepted. Before sending material invoices, confirm that the supplier profile name matches the invoice, the payer has approved the payment details, and remittance advice includes a reference you can match.

- Onboard in parallel

Continue full account or broader operating setup if you need stronger controls later. Do not migrate all invoices until you can receive funds there, retrieve statements or transaction exports, and meet the payer’s document standard.

This split lowers operational risk during transition.

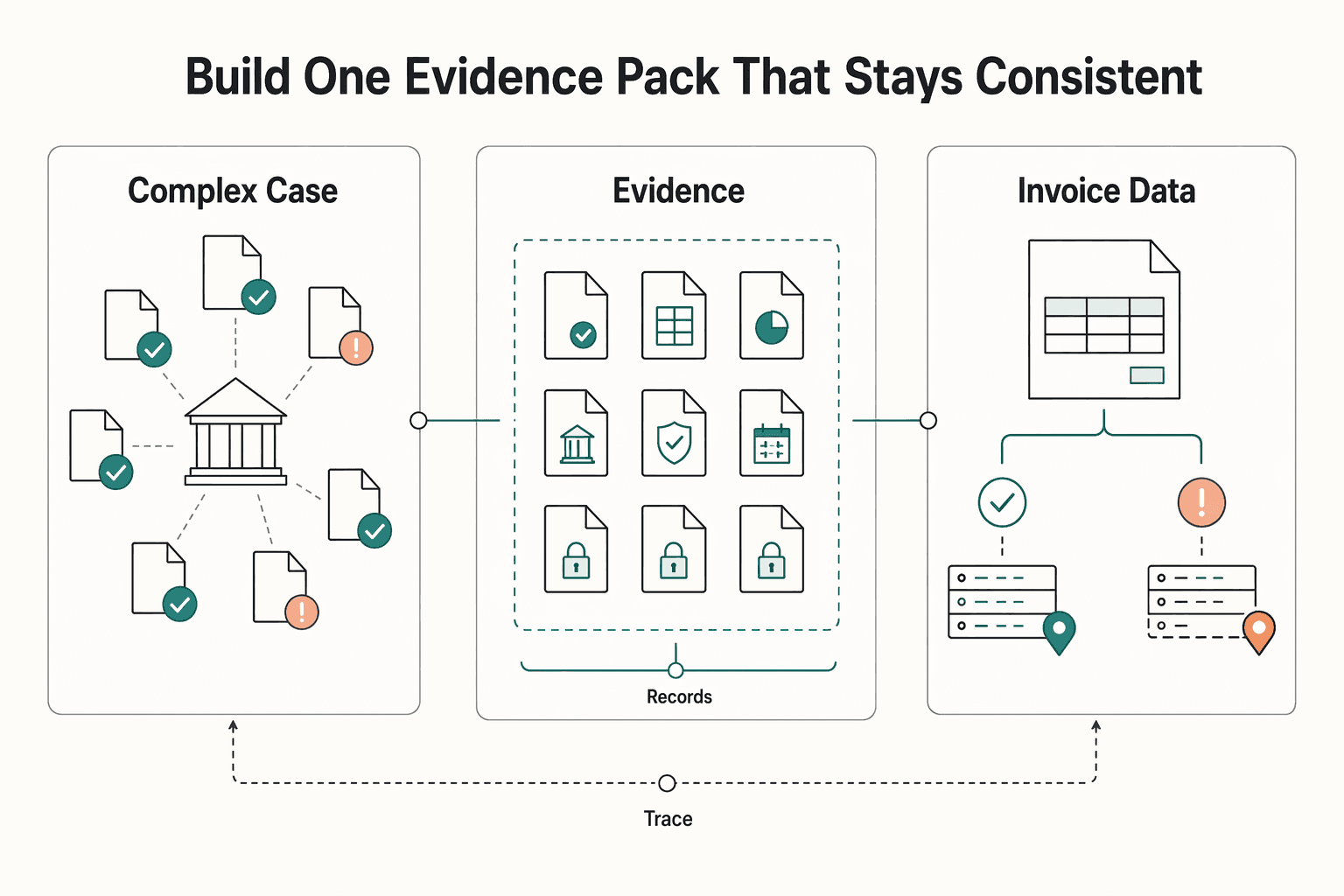

Build one evidence pack that stays consistent#

One compact evidence pack will save you repeated cleanup later. The key is internal consistency.

| Evidence item | What to keep aligned | Checkpoint |

|---|---|---|

| Name and entity details | Legal name, business name, entity name, and identifier (ABN or ARN, where relevant) | The same name and identifier appear on the contract, invoice, tax registration, and provider profile. |

| Registration evidence | ABN record where relevant, or ARN and ATO registration confirmation where relevant | For standard GST with an existing ABN, keep ATO written confirmation showing the effective registration date. Keep a separate slot for any ownership proof the provider asks for during onboarding. |

| Invoice data | Seller identity, issue date, invoice number, GST treatment, and receiving details | Use one invoice format. If details change, version the template and keep written payer acknowledgement. |

| Reconciliation records | Invoice PDF, remittance advice, payout confirmation, receipt date, and internal notes on fees or FX where relevant | You can trace each receipt back to one invoice without guesswork. |

The core control is simple: keep the name on your money path aligned with the name on your invoice path. That one habit reduces onboarding friction and month-end cleanup. It also sets up the mental model for the rest of this guide: treat getting paid as a sequence of checks, not a single application.

For a step-by-step walkthrough, see Opening a Bank Account in Cyprus as a Foreigner.

The 2026 mental model: "Get paid" is a pipeline (not a bank)#

Treat this as a payment pipeline, not a branding choice. Your setup works when you choose the right GST lane early, complete the required registration steps, and keep evidence of what was submitted and when. For non-residents, ABN-related identity checks can add processing time, so judge progress by stage-level pass or fail checks and stored evidence, not by the fact that you submitted an application.

Run a lane check before every form#

Before you answer any registration field, label the lane first.

GST requirement: not every business needs GST registration, but penalties may apply if you fail to register when required, and once required you must register within 21 days.

Standard GST registration: this non-resident lane includes ABN-linked setup, additional identity proof, and BAS lodgment plus GST payment obligations, monthly or quarterly. If you are outside Australia, you cannot lodge electronically and may need an Australian registered tax agent.

Simplified GST registration: this is a limited non-resident lane. You are not entitled to an ABN, cannot claim GST credits, cannot issue tax invoices, must lodge and pay quarterly, and receive an ARN after registration.

Use this rule: do not assume both GST lanes support the same operating capabilities.

Use the pipeline as an operator checklist#

If you need to keep this process under control, track it like an operator would: one stage, one pass condition, one stored record.

| Stage | Pass when | Fail when | Evidence to store |

|---|---|---|---|

| Decide lane | You have confirmed whether GST registration is required and selected standard or simplified registration. | You start forms without confirming requirement or lane. | Decision note with lane and date. |

| Register | Required registration is submitted on time. | You are required to register but miss the 21-day window. | Submission confirmation and timestamp. |

| Confirm activation | Standard lane: written GST registration details and effective date received. Simplified lane: ARN received. | You cannot produce active registration details for your lane. | Registration notice and effective-date or ARN record. |

| Operate | Standard lane reporting and payment cadence is set, with BAS lodgment and GST payment monthly or quarterly, and simplified lane limits are respected. | You run processes your lane does not allow or miss required lodgments or payments. | Reporting calendar, lodged return or BAS records, payment records. |

If you need payment this week, the practical move is still a two-track path: complete the required GST lane actions now, and run broader onboarding tasks in parallel until they are fully usable.

You might also find this useful: How to Set Up a Business Bank Account in the UK as a Non-Resident.

Related: Opening a Business Bank Account for a UAE Free Zone Company.

Do you actually need an Australian business bank account?#

Not always. In the sources for this section, the key legal decision is whether you need GST registration and, if so, which non-resident pathway applies. Those sources do not state that a full Australian business bank account is always required.

Decide by the outcome, not the logo#

Judge this by the operating outcome you need, not by whether the provider looks like a traditional bank.

| Use case | Decision criteria | Do you need a full Australian business bank account? | Best first move |

|---|---|---|---|

| GST may not be required yet | Not every business needs GST registration, but if registration becomes required you must register within 21 days. | No automatic requirement shown here. | Confirm whether your activities currently trigger GST registration. |

| Standard GST registration (non-resident) | This pathway requires ABN registration, identity proof, BAS lodgment, and GST payment, monthly or quarterly. | No automatic requirement shown here. | Use this path when you need standard GST features and can meet the ongoing obligations. |

| Simplified GST registration (non-resident) | This pathway is for non-resident businesses that don't need an ABN, including some low value imported goods sales (A$1,000 or less), but you can't issue tax invoices or claim GST credits. | No automatic requirement shown here. | Use this path only if the simplified limits fit your model. |

Three definitions clear up most of the confusion.

ABN (Australian business number) is a business identifier. Individuals carrying on an enterprise can be entitled to one.

Standard GST registration is the non-resident path with ABN, identity, BAS, and GST reporting and payment requirements.

Simplified GST registration is the non-resident path for businesses that do not need an ABN. After approval, you receive a unique 12-digit ARN used to identify you in ATO systems.

Run this gate before any application#

Before you submit forms, answer these four checks.

- Do your business activities mean you need GST registration now?

- If yes, can you register within the required 21-day window?

- Does the standard path fit, including ABN, identity proof, BAS, and GST lodgment and payment obligations?

- Or does the simplified path fit better, knowing you cannot issue tax invoices or claim GST credits?

Take one of these two tracks#

If you know which GST path fits, commit to it and stop mixing the two.

Standard-GST track: proceed when you need the standard system and can meet ABN, identity, BAS, and payment obligations. Note that offshore operators cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

Simplified-GST track: proceed when you do not need an ABN and can operate within simplified limits. Use the 12-digit ARN for ATO identification after registration.

Related: Opening a Bank Account in Europe as a Non-Resident.

Related: Opening a UAE Bank Account as a Non-Resident Freelancer.

If your immediate priority is AUD collection while onboarding is still pending, compare whether Virtual Accounts fit your fallback path.

Can you open an Australian bank account from overseas in 2026? (What "start online" really means)#

Possibly, but confirm with your chosen bank whether a non-resident can fully activate and use an Australian account entirely from overseas. Treat "start online" as progress, not completion. Use three gates: application submitted, identity and proof requirements cleared, then confirmation that setup is effective and usable. If a client payment is due before gate three, onboarding risk is still live.

This follows the same pattern as ATO registration: submission is not completion. For standard GST registration, non-residents may need extra identity proof when applying for an ABN, and the ATO confirms registration details in writing with an effective date.

The three gates that matter#

The useful question is not whether you applied. It is which gate you have actually cleared.

| Stage | One practical action | Proof to keep |

|---|---|---|

| Application submitted | Submit the provider form with your legal entity details exactly as used on registrations | Provider receipt, reference number, or confirmation email |

| Identity or proof requirements cleared | Complete all requested identity and business-proof steps, then confirm whether anything is still outstanding | Explicit confirmation that review is complete |

| Account usable | Confirm the account can perform the core functions you need, for example receiving funds | Provider confirmation or live account details showing the account is active and usable |

A screen that says "application received" is gate one, not gate three. If a payer requires final account details or provider-issued ownership evidence, you need proof from the last row.

Policy varies by provider#

Provider policy can change, so treat public onboarding pages as a starting point, not a guarantee. Use provider pages such as CommBank, NAB, and ANZ as references, then confirm current requirements directly before you apply.

Keep tax setup and bank onboarding in separate lanes. Standard GST registration is for non-resident businesses entitled to or holding an ABN, and may require extra identity proof for ABN applications. The standard path also has operating constraints for remote teams: you cannot lodge electronically from outside Australia and may need an Australian registered tax agent; GST is paid monthly or quarterly. Simplified GST registration is for eligible non-resident businesses that do not need an ABN, do not have to prove identity, and receive an ARN after registration, but cannot issue tax invoices or claim GST credits. These are tax pathways, not bank-approval guarantees.

Onboarding readiness checks#

Use these checks before you submit.

| Control | Verify before you submit | Why it matters |

|---|---|---|

| Path choice | Confirm whether standard or simplified GST applies to your case | The two pathways have different requirements and outcomes |

| ABN readiness (standard path) | If using standard GST, confirm ABN entitlement/details and prepare extra identity proof for the ABN application | You need an ABN before GST registration, and extra proof can increase processing time |

| Completion evidence | Keep ATO written registration confirmation with effective date (standard) or ARN details (simplified) | Submission alone is not completion |

| Capability limits | Confirm whether your chosen GST path supports what you need next | Standard and simplified pathways do not provide the same capabilities |

If you need standard GST registration, you need an ABN first. If GST registration becomes required, the ATO says you must register within 21 days, and penalties may apply if you fail to register when required.

So decide by payment-deadline risk:

- Pause if you have not confirmed your GST path, required identifiers, or completion evidence.

- Proceed only when review is confirmed complete and you have proof the account is active and can receive funds.

- Switch tracks if your timeline conflicts with outstanding verification or with the limits of your chosen GST pathway.

If tax-residency concepts are getting mixed into provider onboarding, separate them first with A Guide to Tax Residency in Australia for Digital Nomads.

You might also find this useful: How to Open a Bank Account in Uruguay as a Foreigner.

Choose-your-path matrix: the lowest-risk setup for your situation#

A lower-risk default is a two-track setup: keep your live AUD collection path active now, and run fuller onboarding in parallel until the account is verifiably usable. Use this as an operational fallback while provider checks are still in motion, not as a provider-policy guarantee.

Route the decision with four inputs:

- how soon you can complete any required identity steps

- whether the provider currently requires local contact details, confirmed against the provider's current onboarding materials

- whether you need an individual or entity account path

- what your payer requires to release funds, whether that is receiving details only or ownership proof

Pre-application checks that prevent avoidable holds#

Before submitting anything, confirm the current rules on the provider’s onboarding page:

- eligibility and identity flow, including any in-country or branch step the provider currently requires

- supported customer type, individual or entity, and exact legal-name match across invoices and registrations

- required evidence artifacts for your path, including identity, ownership, registration, and any provider-requested proofs

If GST setup is relevant, keep tax and banking as separate lanes. If you are a non-resident, whether you need to register for GST depends on your business activities. Standard GST registration is for non-resident businesses entitled to or holding an ABN, and ABN is required before GST registration. Once GST registration is required, registration is due within 21 days, and penalties may apply for failing to register when required. Simplified GST registration is for non-residents that do not need an ABN; it does not require identity proof and issues a 12-digit ARN, but it does not allow issuing tax invoices or claiming GST credits.

| Your situation | Route now or parallel | Verify before cutover | If activation is delayed |

|---|---|---|---|

| Overseas, payment due soon, no confirmed local onboarding path | Go now on your live AUD collection route; keep onboarding parallel | Payer accepts your current receiving details and remittance trail | Keep collecting on the live route and retain payment references for matching |

| Overseas, arrival soon, provider allows early application | Parallel onboarding | Remaining identity step, review status, and whether payer requires provider-issued ownership proof | Do not commit to bank-proof delivery until review is complete |

| In Australia, identity can be completed now | Go now only after verification and receipt testing succeed | Login access works, account can receive funds, payer accepts your proof document | Keep the existing route active until payer acceptance is confirmed |

| Company, partnership, or trust | Parallel unless the entity account is already active | Entity support, ownership disclosures, and identifier consistency across records | Continue collections on the live route while entity review completes |

After you choose a route, map invoice, payout, and reconciliation handoffs in Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe. If you need AUD collection continuity while onboarding is still pending, use Gruv Virtual Accounts as the continuity lane.

When should I switch from parallel onboarding to full cutover?#

Switch only after this is true in practice: the account is active, you can access it, and it can receive funds. Application submission or "approved" status alone is not enough when the payer requires ownership evidence or final account details. Keep the live collection route until those checks are complete.

When is proof of banking required instead of tax registration proof?#

Use the payer’s request as the rule. ABN, ARN, or ATO registration documentation can support tax workflows, but they do not by themselves prove an active, usable account owned by your business. If the payer asks for banking ownership evidence, hold cutover until that document standard is met.

If you want a deeper dive, read How to Host a Webinar to Generate Freelance Leads.

If your route depends on provider eligibility, onboarding gates, or market-specific coverage, use contact Gruv to validate your setup before switching payment rails.

Frequently Asked Questions

When should I switch from parallel onboarding to full cutover?

Switch only after this is true in practice: the account is active, you can access it, and it can receive funds. Application submission or "approved" status alone is not enough when the payer requires ownership evidence or final account details. Keep the live collection route until those checks are complete.

When is proof of banking required instead of tax registration proof?

Use the payer’s request as the rule. ABN, ARN, or ATO registration documentation can support tax workflows, but they do not by themselves prove an active, usable account owned by your business. If the payer asks for banking ownership evidence, hold cutover until that document standard is met. If you want a deeper dive, read How to Host a Webinar to Generate Freelance Leads. If your route depends on provider eligibility, onboarding gates, or market-specific coverage, use contact Gruv to validate your setup before switching payment rails.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

How to Host a Webinar to Generate Freelance Leads

**Treat your webinar as a repeatable pipeline system (capture, qualify, route, follow up), not a one-off event you hope generates leads.** If you run a business-of-one, you're the CEO. Your webinar should behave like an asset you can operate, not a performance you have to reinvent.