Quick Answer

A practical guide to long-term care insurance starts with one outcome: decide whether to Go, Wait, or Skip based on risk and cashflow durability. Treat long-term care as a daily-living and supervision funding risk, not a medical-bill assumption. Then document what you verified, what is still unknown, and the trigger for your next annual review.

Long-term care is a cashflow risk - here's the 10-15 minute system to control it#

Treat long-term care insurance as a planning decision, then document a simple Go / Wait / Skip call you can re-run every year. Once the topic is on the table, the operator move is to turn "maybe someday" into a repeatable control. That cuts stress because you stop relying on vibes and start relying on a decision record.

A care need can hit your time, your choices, and your finances at once. That's why you treat long-term care as a real planning risk, not as "later-life content."

The operator frame: make one decision, not a thousand micro-decisions#

You want a risk-first workflow that produces a clear outcome you can defend later. Here's the fast structure:

- Define the risk you want to control: downtime risk, forced spending, or loss of choice (for example, needing to rely on a public program with constraints).

- Choose a default action: Go, Wait, or Skip.

- Log the decision: what you checked, what you assumed, and what would change your answer next year.

| Outcome | When it fits (operator logic) | Next action you take immediately |

|---|---|---|

| Go | You can fund premiums without destabilizing your plan, and you want to transfer long-duration care-cost risk to insurance. | Start policy comparisons and request written details you can file. |

| Wait | You need stronger reserves, cleaner cashflow, or more clarity on options before you commit. | Set a calendar reminder and define what "ready" means (in writing). |

| Skip | You plan to self-fund or rely on a fallback program, and you accept the constraints that come with that choice. | Document the rationale and the trigger that would make you revisit. |

Keep it audit-ready (and don't trust random tabs)#

Store your decision log with your finance controls, not in stray tabs. When you verify government programs or rules, use safe defaults: "A .gov website belongs to an official government organization in the United States." Also confirm you see HTTPS because "The https:// ensures that you are connecting to the official website and that any information you provide is encrypted."

Treat program and market details as changeable. HHS published a report titled "Exiting the Market: Understanding the Factors behind Carriers' Decision to Leave the Long-Term Care Insurance Market" (Publication Date: Jun 30, 2013), prepared under contract #HHSP23320100022WI, and it states the views reflect the authors. In practice, re-check critical details before you act.

If you want a deeper dive, read A Deep Dive into FinCEN's Beneficial Ownership Information (BOI) Reporting.

The mental model: Long-Term Care Insurance is for "daily living," not "doctor bills"#

Long-term care planning is mainly about funding daily living help, support, and supervision. If your Go / Wait / Skip decision is going to hold up, you need a clean definition of the risk you might transfer to coverage. Keep medical treatment in a separate mental bucket so you buy the right protection.

Long-term care shows up when someone can't reliably manage day-to-day function without help. That help can happen at home (including aging in place) or in other supportive care settings. It can also include supervision when cognitive decline changes safety, not just mobility.

Alzheimer's disease fits this pattern because it's "a progressive, neurodegenerative disease... leading to loss of mental functions such as memory and learning," which can turn "physically fine" into "not safe alone."

Define the bucket: daily living, supervision, and where costs actually land#

Use ADLs to keep the category crisp. Activities of Daily Living (ADLs) include "bathing, eating, grooming, dressing, toileting, administering medication, [and] moving around." That list matters because policies often hinge on whether someone needs extended assistance with these tasks or supervision.

In real life, medical care and long-term care can overlap in the same week. Separate them anyway. That keeps you from shopping for the wrong product or assuming one product covers everything.

| Category you're paying for | What it looks like on the ground | What to call it in your notes |

|---|---|---|

| Acute medical treatment | Diagnostics, specialist visits, procedures, recovery protocols | Medical care |

| Ongoing function support | Bathing, dressing, toileting, medication help, moving safely | Daily living assistance (ADLs) |

| Safety and oversight | Cueing, redirection, protective environment, especially with cognitive impairment | Supervision |

| Place of care | At home (aging in place), adult day services, or other supportive care settings | Care setting |

The operator risk equation: frequency + severity + duration#

Don't overcomplicate this. Run it like any other risk control:

- Frequency risk: How likely you'll need ongoing help.

- Severity risk: How expensive that help gets in your likely care setting.

- Duration risk: How long the need lasts once it starts.

For business owners, this sits inside cashflow continuity planning. You already manage risks you can't invoice your way out of. Treat long-term care the same way: define the bucket, separate it from medical costs, then decide whether you want to fund that risk with savings, insurance, or another documented plan.

Does Medicare cover long-term care?#

In general, Medicare doesn't pay for long-term care. Once you've separated "daily living and supervision" from "doctor bills," you can assign each bucket to the right payer and stop planning on a false assumption.

Medicare's own language stays blunt: "Medicare doesn't pay for long-term care." Medicare.gov also clarifies the common trap: "Medicare and most health insurance, including Medicare Supplement Insurance (Medigap), don't pay for long-term care services."

That includes long-term care in a nursing home or in the community. In practice, that covers most real-world custodial support, including help with bathing, dressing, and using the bathroom.

Don't mix up these three programs (this mistake gets expensive)#

Use this as your operator translation table:

| Program | What it primarily covers | What it does not solve for (safe default) |

|---|---|---|

| Medicare | Health coverage, primarily medical care | Most long-term care, including personal care services such as custodial care |

| Medicare Supplement Insurance (Medigap) | Helps lower your share of certain Part A and Part B costs (Original Medicare) | Long-term care services (it fills Medicare cost-sharing, it does not replace LTC planning) |

| Medicaid | A separate program with state-specific rules | Do not assume eligibility, coverage, or timing without verifying your state's rules |

Operational implication: if you assume Medicare covers ongoing home support or facility support, you underfund the duration risk. That gap often forces decisions under pressure. Family members cover supervision with unpaid time, or you liquidate assets faster than your business cashflow can replace them.

(UnitedHealthcare's Medicare Made Clear notes an estimate that approximately 63% of individuals age 65 and older will require extra care at some point, which makes "probably not me" a weak plan.)

What to verify safely (rules change, and you need receipts)#

- Confirm current boundaries on Medicare.gov.

- Verify any state-specific assumptions using your state's official resources.

- Document what you found and the date you checked in your decision log.

How is long-term care paid for if you don't have insurance?#

There is no single answer, but if you don't have coverage, you still need a written funding plan that matches your care-setting options to the dollars and rules you can actually use. The goal is not perfect forecasting. It's a model you can pressure-test.

Model it side-by-side (as a worksheet, not a vibe)#

Do not treat this like a philosophical question. Build a one-page model with three columns and force every care scenario into it:

| What to model | What you control | Operator questions that prevent surprises |

|---|---|---|

| Care scenario (the setting and intensity) | Your preferences, your willingness to move, your support network | What setting would you actually accept in a stressful week? What's your "good enough" fallback? |

| Real costs (money and time) | Savings rate, reserves, spending, business runway, delegation | Can you cover the expense without breaking your invoice-to-expense rhythm? Who coordinates care when you're slammed? |

| Verified funding sources and constraints | Your planning and documentation | What funding sources are you eligible to use, in which settings, and under what conditions? What timelines and approvals could affect access? |

If you run a business-of-one, treat coordination time as a real cost. Even if you can afford the bills, the operational load can still steal billable hours and turn care into a cashflow problem.

Build a conservative baseline scenario, then stress-test runway#

Skip hero math and keep it concrete. In your decision log, write two baseline lines and three stress-test questions:

- Baseline A: support at home (home health care or similar help).

- Baseline B: higher-support setting later (assisted living facility or nursing home).

| Test | Question to answer |

|---|---|

| Cashflow test | What breaks first, taxes, payroll (if any), rent, or your personal runway? |

| Time test | Who owns care coordination, and what work gets dropped when care needs spike? |

| Decision test | If you had to choose in a stressful week, would you pick the setting you want, or the setting you can access fastest? |

Finally, keep other programs in the right lane. Social Security and Supplemental Security Income (SSI) often come up in planning conversations, but you must verify details in your jurisdiction. If you work across borders, note that Social Security "Totalization" agreements exist to eliminate dual Social Security taxation, and the U.S.-Canada agreement explicitly does not cover SSI.

Is long-term care insurance worth it for a freelancer (or a two-person studio)?#

There is no universal "worth it" answer. The clean way to decide is to write down which risk you will carry and which risk you will transfer, then confirm your choice survives a bad year.

Reframe "worth it" as a risk trade you control#

Stop trying to predict whether you'll need care. Run a risk trade instead, and pick the downside you can tolerate.

| Risk you keep | What it looks like in real life | Your operator control |

|---|---|---|

| Premium risk | You commit to ongoing payments and you must keep them durable through income volatility. | Stress-test affordability and build a "premium budget lane" that you do not raid. |

| Care-cost risk | You self-fund care costs if it happens, and the bill hits at the same time your capacity drops. | Build reserves, simplify obligations, pre-decide what you would sell or pause. |

| Plan risk | You rely on a fallback plan you haven't pressure-tested, or you assume "something will cover it" without verifying. | Document assumptions, then verify the current rules and constraints that apply to you when you review annually (rules vary by jurisdiction and program). |

Behavioral economics is useful here. An HHS/ASPE paper defines it as: "behavioral economics focuses on human limitations, empirically testing the ways in which human behavior departs from the rational." Your limitation here usually shows up as procrastination disguised as "research."

Compare options explicitly (without guessing)#

You will see different policy designs and feature sets in the market. Do not assume they behave the same. Force a side-by-side worksheet and require each option to answer the same questions about cashflow timing, what's required to qualify for benefits, and what happens if you stop paying.

Freelancer lens: premium affordability means premium durability. A freelancer healthcare explainer put it plainly about health coverage: "Health insurance premiums, deductibles, and copays can get really expensive, especially for freelancers and consultants who don't have an employer paying for anything." Use that same mental model here. Can you still pay after a client loss, a slow quarter, and a tax bill?

"Skip" can be rational, but only if you write: (1) what you will self-fund, (2) what lifestyle or business changes you accept, and (3) what your fallback plan is. Put LTC in your protection stack alongside non-negotiables like tightening payment rails and avoiding volatility you can't invoice your way out of, including The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

The Go / Wait / Skip framework you can run in 10-15 minutes (and revisit annually)#

Make a Go / Wait / Skip call by locking your outcome first, stress-testing premium durability, and re-checking the realities you rely on each year. You are not trying to "solve long-term care." You are installing a repeatable decision you can re-run in annual planning.

A 10-15 minute run-through (copy/paste this)#

Step 1: Set your non-negotiable outcome (one sentence, date-stamped). Pick one primary goal and write it down: protect spouse or partner cashflow, protect business continuity, protect a home, or protect other assets. Keep it single-focus or you will negotiate against yourself later.

| Step | Action | Key detail |

|---|---|---|

| 1 | Set your non-negotiable outcome | Pick one primary goal and write it down in one sentence, date-stamped. |

| 2 | Run the premium durability stress test | Ask what breaks first: tax payments, operating expenses, or personal runway. |

| 3 | Decide with thresholds, not vibes | Choose Go, Wait, or Skip. |

| 4 | Verify state variability | Save the link you used and date-stamp it in your decision log. |

| 5 | If you're a federal employee, treat FLTCIP as a special branch | Check OPM guidance, note today's date, then re-check right before you apply. |

Step 2: Run the premium durability stress test (freelancer test). Treat the premium like a fixed vendor contract. Ask: if premiums rise or income dips, what breaks first: tax payments, operating expenses, or personal runway? If the honest answer is "I'd skip quarterly taxes" or "I'd float payroll or rent," you do not have durability yet. A policy you can't sustain becomes a liability.

Step 3: Decide with thresholds, not vibes.

| Decision | Use this when | Your next move |

|---|---|---|

| Go | You can sustain premiums through a bad year, and you want protection from long-term care costs. | Start a structured policy comparison and underwriting conversation. |

| Wait | You need stronger cash reserves, or you feel uncertain about underwriting odds (health history, timing, paperwork readiness). | Set a 90-day stabilization plan, then rerun this framework. |

| Skip | You do not want to prioritize premiums for this risk right now, and you are comfortable relying on other resources or a different fallback plan. | Document the choice, then set an annual review date. |

Confirm variability before you lock in (state and federal)#

Step 4: Verify state variability. Insurance products and consumer protections vary by state, so verify basics with your state regulator. Save the link you used and date-stamp it in your decision log.

Step 5: If you're a federal employee, treat FLTCIP as a special branch. If you're a federal employee, check OPM guidance on the Federal Long Term Care Insurance Program (FLTCIP) before you assume availability. OPM states: "Individuals not currently enrolled may not apply for coverage, and current enrollees may not apply to increase their coverage," and "The suspension will remain in effect for 24 months" (unless OPM issues a subsequent notice to end or extend it), with an extension "to be effective on December 19, 2024." In your log, note today's date, then re-check right before you apply.

Policy comparison playbook: what to check before you sign (so you don't buy a "maybe")#

Before you sign, confirm what the policy pays for, how claims work, and whether underwriting blocks you. Once you've run Go / Wait / Skip, you're not debating the category. You're selecting a contract that has to perform under stress.

1) Start with coverage reality (not the brochure)#

A policy aims to help cover long-term care services that regular health insurance or Medicare typically do not. Your first job is to confirm the eligible care settings you actually want covered.

| Item to confirm | What to look for in the policy | Question to ask |

|---|---|---|

| At home | Whether it pays for care at home | Ask the carrier or broker to show you, in the policy, whether it pays for care at home. |

| In a community setting | Whether it pays for care in a community setting | Ask the carrier or broker to show you, in the policy, whether it pays for care in a community setting. |

| In a nursing home | Whether it pays for care in a nursing home | Ask the carrier or broker to show you, in the policy, whether it pays for care in a nursing home. |

| Cognitive impairment | Where the policy defines cognitive impairment benefits, and whether it changes eligibility, documentation, or payment rules compared to physical limitations | Ask: "Where does the policy define cognitive impairment benefits, and does it change eligibility, documentation, or payment rules compared to physical limitations?" |

Ask the carrier or broker to show you the actual policy language for each setting: at home, in a community setting, and in a nursing home.

Then push on cognitive impairment specifically. Do not assume anything about Alzheimer's disease or other cognitive conditions. Ask: "Where does the policy define cognitive impairment benefits, and does it change eligibility, documentation, or payment rules compared to physical limitations?"

Why this matters operationally: one long-term care event can flip your retirement planning into a cashflow problem fast. One industry article cites the average cost of a private room in a nursing home at over $100,000 per year, so "mostly covered" can still leave meaningful downside if the setting you need sits outside the contract.

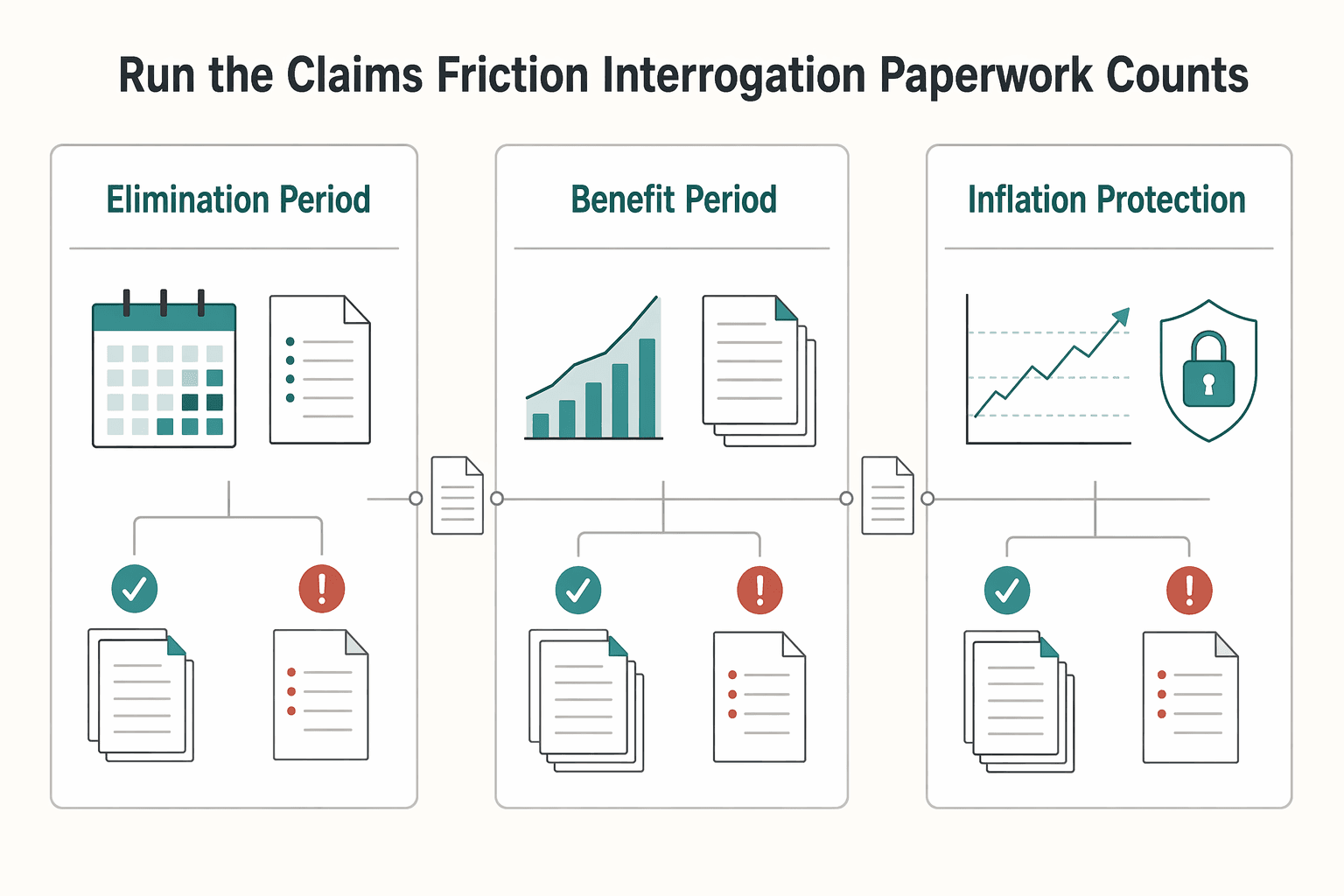

2) Run the "claims friction" interrogation (paperwork counts)#

Treat claims like accounts receivable. You can't bank benefits you can't collect. Use this checklist on every carrier, and write the answers into your decision log:

- Eligibility trigger: "Which daily activities trigger eligibility, and where do you define them?"

- Documentation: "Who must certify eligibility (doctor, nurse, care coordinator), and what documents do you require?"

- Timing: "After I submit a complete claim, what timeline do you target for approval and reimbursement?"

- Payment mechanics: "Do you reimburse me, pay the provider, or offer both?"

Now compare the policy mechanics that drive outcomes, side by side:

| Policy lever | The operator question to ask | The risk you control |

|---|---|---|

| Elimination period | "What waiting period applies before benefits start, and what counts toward it?" | How long you must self-fund care costs |

| Benefit period / pool of money | "What is the maximum available benefit, and how does the policy track usage?" | How far coverage stretches in a long event |

| Inflation protection | "How can benefits increase over time, and when can that change?" | Erosion risk vs rising care costs |

Finally, underwriting and exclusions decide whether this policy exists for you at all. Ask for the underwriting outline up front, then document what would trigger denial or higher premiums, especially around cognitive history. If you evaluate employer or government options, confirm current availability and plan details on the relevant .gov pages as of your decision date.

Make it audit-ready: your "known vs unknown" table + annual review triggers + mini checklist#

Create a one-page decision record that separates documented facts from assumptions, then review it annually. Once you've compared policies and pressure-tested claims friction, lock the work into an operator artifact you can defend later. Think of it like storing a major client contract: clear rationale, attached evidence, and an explicit plan to verify what you could not confirm today.

Build the one-page decision record (store it with your financial ops docs)#

Keep it to one page, then attach supporting PDFs or screenshots in a folder.

- Decision: Go / Wait / Skip

- Date + rationale: One paragraph. Include the threshold you used (for example, "premium stays payable in a bad-year scenario").

- What you checked (evidence): Links plus saved PDFs or screenshots (policy pages, underwriting outline, rider language, emails).

- What you still don't know: List unknowns and write exactly how you will verify (who, where, and when).

Hypothetical scenario: you choose "Wait" because your cashflow looks solid today, but you plan to relocate. You write, "Re-check how this policy would be treated after relocation, then re-run quotes," so you do not treat an old jurisdiction as current.

Known vs Unknown table + annual review triggers (as a recurring control)#

Use the table to kill false certainty. "Known" means you can point to a document you saved.

| Category | Known (documented) | Unknown (verify before you rely on it) |

|---|---|---|

| Federal option context | OPM administers the Federal Long Term Care Insurance Program (FLTCIP). An OPM contractor operates the FLTCIP system, including enrollment and claims administration. Interested persons must apply individually. FLTCIP runs on an enrollee-pay-all basis. The contractor operates LTCFEDS.gov. | Current FLTCIP availability, plan options, underwriting, premiums, and benefits (confirm as of your check date). |

| Your private policy | Your signed policy form, riders, and any carrier-provided underwriting outline you saved. | Eligibility triggers, exclusions, reimbursement mechanics, and inflation rider terms if you did not verify them in the contract itself. |

| Jurisdiction variability | Any written materials you saved that describe how your insurer treats your coverage if you move or change residency. | Any jurisdiction-specific differences that could affect your policy in practice (confirm directly with your insurer and your own advisors). |

Annual review triggers (practical, not "required"): for example, meaningful changes in income, health, where you live, premium notices, or a shift in caregiving responsibilities. Re-check any government program references (OPM, FLTCIP) as of the day you review.

Treat this like reconciliation: document assumptions, reconcile annually, keep records exportable. If you already reconcile monthly, fold this into your yearly close using the same discipline as How to Reconcile Bank Statements in Xero.

Mini checklist (copy/paste)

- Define goal (asset protection vs independence vs business continuity)

- Run premium durability stress test (bad-year scenario)

- Choose Go/Wait/Skip + write the threshold you used

- Confirm any jurisdiction-specific differences with your insurer and your own advisors

- If applicable, verify OPM and FLTCIP status as of today

- Store your Known vs Unknown table + set an annual review date

The bottom line: treat LTC like a controllable system, not a scary mystery#

Treat long-term care insurance as one option inside a documented risk-control system. Run it with the same discipline you use to protect cashflow in your business.

At this point, you have the pieces that matter. The win is not perfect foresight. It's a repeatable decision you can defend.

Long-term care planning starts when you define the problem in plain language. Decide what "long-term care" means in your life, what you expect your health coverage to handle versus what it might not, and what resources you would use if you need ongoing help.

You might cover that need through assets, insurance, and other programs that depend on eligibility (rules vary and change). Do not guess. Keep a brief record of what you verified, where you verified it, and when.

Your operator kit: a simple decision record you can revisit#

Keep it simple and readable. A one-page note is often enough:

- What you're protecting against (in your words)

- The options you considered and why you chose what you chose

- The assumptions you're relying on

- What would make you revisit the decision

Make it reviewable, then check it periodically#

Keep your notes tidy and easy to find, and set a recurring reminder to revisit them. If you already run regular finance hygiene, anchor this to it: How to Reconcile Bank Statements in Xero. Consistency beats intensity here.

Frequently Asked Questions

Does Medicare cover long-term care?

Coverage rules vary, so verify what applies to your situation on Medicare’s official resources and write down the date you checked. That single step prevents expensive planning assumptions.

Who should buy long-term care insurance?

Buy long-term care insurance when you want to protect cashflow and assets from a loss of independence you do not want to self-fund. AMF’s practical test fits operators: ask, “Do I have the cash required to pay the costs related to a loss of independence?” and “Does the cost align with my budget?” If either answer makes you uncomfortable, you have a real decision to model and document.

How is long-term care paid for if you don’t have insurance?

You typically combine (1) personal cashflow and assets, (2) unpaid family caregiving time, and (3) whatever public programs you qualify for (rules vary by jurisdiction). If you run a business-of-one, model the second-order cost too: time spent coordinating care can reduce your ability to invoice.

Is long-term care insurance worth it?

“Worth it” means you choose which risk you keep: premium risk or care-cost risk. Make it mechanical. If you can fund premiums inside your bad-year budget, long-term care insurance can reduce the chance you must liquidate assets quickly during a care event. If premiums strain cash reserves, choose “Wait” or “Skip” and document the trigger that would change your decision.

What does long-term care insurance usually cover?

Long-term care insurance provides financial coverage if you become unable to take care of yourself due to illness or accident. Depending on the policy, it may pay an annuity for certain long-term care situations (including in-home care or stays in specialized care centres), or it may reimburse expenses, which requires you to submit invoices. Read the policy form so you know which benefit style you buy.

Can federal employees still enroll in FLTCIP?

OPM extended the FLTCIP application suspension effective December 19, 2024, and it remains in effect for 24 months unless OPM changes it by notice. During the suspension, individuals not currently enrolled cannot apply, and current enrollees cannot apply to increase coverage. If you already enrolled or you sit in the application process, BENEFEDS says your FLTCIP premium information should appear in your My BENEFEDS dashboard within one business day after you create the account (and your application gets approved). If it does not, call 1-877-888-FEDS (1-877-888-3337) (TTY 711).

What’s the difference between a traditional long-term care policy and a hybrid long-term care policy?

The labels are not a reliable shortcut. Treat this as a documentation exercise: request the policy form and confirm (1) how the policy pays benefits (annuity versus expense reimbursement), and (2) what proof you must submit. If you hate paperwork and want predictable ops, you might favor a structure that does not require you to chase and submit invoices, but only after the contract confirms it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

How to Reconcile Bank Statements in Xero

**To reconcile in Xero safely, run a weekly or daily system on the Reconcile tab that clears statement lines, isolates exceptions quickly, and closes each period with documented completion.**