Quick Answer

Index fund investing for freelancers works best as a cashflow-first system: stabilize how you get paid, then invest only from money you can safely leave invested long term. Use a low/normal/high monthly contribution rule, with pause or reduction when cash is tight. Pick the account and fund vehicle you can execute consistently, keep the setup simple, and follow written rules every cycle.

You don't need "more investing tips" - you need a cashflow-first system that survives late payments#

If you run a business-of-one, you're not here for vibes; you're here for a repeatable system you can run.

Investing success rarely comes from flashy tips or frequent trading. It comes from a disciplined approach you can repeat. Build a simple set of rules you can follow through market noise so patience and long-term holding can do the heavy lifting.

Why tips fail when you're investing for the long run#

You can do everything "right" on paper and still derail your plan when the market gets loud. Without a system, you end up reacting to short-term noise and making impulsive moves you did not plan for.

A Lemon8 creator put it plainly: "Investing success rarely comes from flashy tips or frequent trading but from a consistent, disciplined approach." They also make the long-game point: compounding returns accumulate over time, and long-term holding can be more effective than chasing immediate gains. That only works if your behavior stays steady.

Use this mental model:

| System | Goal | What "good" looks like | What to avoid |

|---|---|---|---|

| Consistent, disciplined approach | Stay steady through noise | Repeatable decisions you can stick with | Flashy tips and frequent trading |

| Patience and long-term holding | Let compounding work over time | Holding through normal market fluctuations | Chasing quick fixes and immediate gains |

Hypothetical: you get a "hot" idea during a volatile week. If you invest based on excitement or fear, you end up whipsawing yourself. If you invest based on your rules, you stay consistent and move on.

The system (safe defaults)#

Run this sequence on a regular cadence:

| Gate | Focus | What to do |

|---|---|---|

| Gate 1 | Clarity | Decide in advance what you are doing and what you are ignoring. Write it down. |

| Gate 2 | Patience first | Plan around long-term holding, not quick wins. Markets fluctuate constantly. |

| Gate 3 | Decision rules | Use simple, repeatable rules you can execute consistently instead of reinventing the plan each time. |

| Gate 4 | Confirm local rules | Taxes and account rules vary by jurisdiction and provider. If your situation is cross-border, get clarity before you "optimize". |

Gate 4 matters most if you're cross-border: get clarity before you "optimize." If that's you, start with Tax Implications for an Australian Resident Owning a US LLC.

That's the point: boring, repeatable, durable.

Index-fund investing, defined (and the mental model you'll use for every decision)#

Index investing (also called passive investing) keeps things simple and low-cost so you can participate in the long-term growth of global markets. To stop improvising, you need a shared vocabulary and a couple of checks you can repeat when decisions get noisy.

Curvo puts the spirit of index investing plainly: "It strips away unnecessary complexity, drastically reduces costs, and gives everyone access to the long-term growth of global markets." It also notes how traditional investing can feel intimidating, with complicated jargon and conflicting advice, and that the financial industry thrives on this complexity. That matters for freelancers because complexity creates decision fatigue. Decision fatigue creates mistakes: tinkering, timing, and panic-selling.

The only definitions you actually need (operator version)#

- Index investing prioritizes simplicity and cost control while aiming to participate in broad market growth, not to "outsmart" it.

- Passive investing is another name for index investing.

Use this quick verification table when you evaluate an investing option:

| What you're deciding | What an operator checks first | Safe default behavior |

|---|---|---|

| "Is this aligned with passive investing?" | Does it keep complexity low and costs transparent? | Prefer simple, broad exposure you can hold for the long term. |

| "Will I mess with it?" | How easy it feels to second-guess and constantly change course | Build friction against constant changes. Consistency beats cleverness. |

The mental model: complexity is the enemy#

If investing feels like it requires a glossary, a hot take, and a prediction, you're back in the world Curvo warns about: jargon, conflicting advice, and complexity that serves someone else.

A Quora answer goes further and claims that "19 out of 20" actively managed mutual funds underperform their relevant index over a 15-year period. Treat that as a claim, not a law of physics. The practical takeaway still holds: if you want something you can actually stick with, you're usually better served by a simple, low-cost, long-term approach than by constant attempts to outsmart the market.

If you want to tighten the cashflow side first, try the free invoice generator.

The freelancer sequencing rule: protect "Get Paid" before you automate investing#

Protect cashflow reliability first, then automate index fund investing only from money you are confident you will not need for near-term bills. This sequencing helps you avoid selling an investment at the exact wrong moment when a payment comes in late.

People love to call index funds "passive," but real life still needs maintenance. The source puts it bluntly: "Let's be real: truly passive income doesn't exist." It also notes that "almost every income stream requires time, effort, and ongoing attention to maintain." Treat your "get paid" workflow as part of that ongoing attention. You earn the right to automate later.

Keep investing automation downstream of cashflow reality#

You do not need fancy software. You need a boring habit: only automate buys from money that's actually available after you cover near-term obligations and keep a buffer.

Hypothetical: a client promises payment "next week," but the deposit does not clear. If your investing automation is downstream of confirmed cashflow, you can pause without panic and avoid touching your index fund position.

Where Gruv fits (context, not a promise)#

Gruv is modular financial infrastructure for money movement. Where supported and enabled, it can help you collect funds, hold and track balances, convert when needed, and pay out with compliance gates and audit-ready records through modules like Virtual Accounts and Payouts.

How should freelancers invest in index funds with irregular income?#

Use a simple low/normal/high contribution ladder, and only invest when your emergency fund is intact. Once you have a safe-to-invest gate, you still need a repeatable way to size contributions when income swings. That's the difference between long-term investing that compounds and a plan that breaks the first time a client pays late.

Freelance finance has a structural problem. As HDFC Fund notes, "the income of freelancers tends to be erratic," so you cannot run this like payroll-deducted employees do. Sidepocket also flags the operational gap: "With no employer-sponsored retirement plans, health insurance, or automatic payroll deductions," you carry the full responsibility for consistency.

Use a three-tier contribution ladder (operator rule, not vibes)#

Treat this as a practical operator rule for investing with irregular income. Keep the instrument consistent if that's your plan, but vary the amount based on the month you actually lived.

| Month type | Contribution rule | What you protect |

|---|---|---|

| Low month | Contribute $0 or a small minimum. Skip the buy if it competes with essentials. | Liquidity and bill safety |

| Normal month | Contribute your baseline amount. | Consistency without strain |

| High month | Contribute baseline plus a predefined "surplus sweep." | Progress without lifestyle creep |

Baseline is a percentage of money you can invest after you fund essentials and reserves. Start conservative. Add a hard floor: if you have not built your emergency fund, do not force purchases. Proshield Invest puts it plainly: "Before you invest a rupee, build an emergency fund of at least 6 months of living expenses."

Hypothetical: you land a great project, then the next month comes in quiet. Your ladder lets you sweep extra in the strong month, then drop to $0 in the quiet one without breaking the plan.

Trigger points and "automation that won't betray you"#

Use trigger points to stay disciplined:

| Trigger | Action | Note |

|---|---|---|

| Emergency fund falls below the minimum you're trying to maintain | Pause or reduce investing | The section cites Proshield Invest's recommendation of at least six months of living expenses before investing. |

| Last few months show reliable inflows and you consistently maintain your reserve | Raise your baseline in small steps | Only raise your baseline after stability. |

| Recurring calendar checkpoint on your money day | Verify reserves, classify the month, then place the buy | Automate the habit, not just the transfer. |

These triggers are simple on purpose. Put a recurring calendar checkpoint on your money day: verify reserves, classify the month as low, normal, or high, then place the buy. Automate the habit, not just the transfer. This mirrors the discipline of investing a portion regularly through a Systematic Investment Plan (SIP), which HDFC Fund describes as a way "investors use Systematic Investment Plan (SIP) to handle through the market volatility," while still respecting irregular income.

ETF or index mutual fund - which is the safer default for uneven cashflow?#

Choose the ETF or index mutual fund option that lets you invest consistently in low, normal, and high months with minimal friction. Once you have a contribution ladder, you need an instrument you can use cleanly when contributions shrink, pause, or restart. Choose based on minimums, purchase flexibility, and account constraints, not "best fund" debates.

Choose based on constraints, not labels#

For freelancers with uneven cashflow, the real question is not "ETF vs index mutual fund." It is whether you can invest the exact dollar amount your ladder calls for on the day you run your money workflow, without friction.

Start with the only safe default: verify how your brokerage account actually handles dollar-based buying. Some platforms support fractional shares, which lets you place a precise buy even when share prices feel out of reach. As one investing commenter put it, "Most of them allow you to buy fractions of shares and not just full shares." This matters when your "low month" rule calls for a small purchase. It also matters when you want to restart gently after a pause.

Also watch for platform lock-in. Vanguard's advisory brochure states: "All options will require your accounts to be with Vanguard." It also notes those programs "vary in cost, account minimums, features." Translation: if you rely on an advisory program, you accept their minimums and where you hold the account.

That might feel stable, or it might feel restrictive if you relocate or change setups. If location changes sit on your roadmap, sanity-check broker access early (see Japan Digital Nomad Visa: A Guide to the New 2025 Program).

Here's the operator checklist to run before you commit, especially if your cashflow is uneven:

| Constraint to verify | Why it matters with uneven cashflow | What to confirm for an ETF | What to confirm for an index mutual fund |

|---|---|---|---|

| Minimum to start or add | Your ladder includes small or zero months | Can you buy fractional shares for the ETF, or only whole shares? | Does the fund, or any program you're using, enforce minimums to start or add? |

| Automation support | You need consistency without constant decisions | Does your platform support recurring buys, and can you change amounts month-to-month? | Does your platform support recurring buys, and can you adjust quickly when income dips? |

| Cash access workflow | You will have occasional "cash pinch" weeks | What's your broker's process for moving cash in and out of the brokerage cash position? | Same question, plus any fund or program constraints your broker discloses |

Hypothetical: you run your money day, classify the month as "low," and want to invest a small amount. If your platform will not let you place small buys, you either skip investing or force a larger buy than your cashflow supports.

Decision rule you can trust: if you cannot reliably meet minimums or you want maximum flexibility in contribution size, lean toward an ETF setup when your broker supports fractional shares for it. If you can meet any minimums consistently and your platform makes it easy to invest a fixed dollar amount into an index mutual fund, that can work, but only if you confirm the minimums and account constraints in writing.

Brokerage account or IRA - what account should a freelancer use for index funds?#

To buy shares of index funds, you generally use a brokerage account (for more general investing) or an individual retirement account (IRA). Choose between them based on the rules, access, and reporting you can actually manage, not as a test of whether you're "serious" about investing.

NerdWallet puts the core choice plainly: to buy shares of index funds, you generally use a brokerage account (for more general investing) or an individual retirement account (IRA). Either account type can be used to hold index funds, and ETFs can also be used to get similar broad-market exposure where supported by your provider.

The operator comparison (what changes when you change the account)#

| Dimension | Brokerage account | IRA |

|---|---|---|

| Primary purpose | More general investing | Retirement-focused investing with account-specific rules |

| Access and use | How you add or take out money depends on your provider's policies and the rules that apply to you | You follow IRA-specific rules set by your jurisdiction and provider |

| What you can buy | What's available depends on the broker/platform | What's available depends on the broker/platform and IRA program |

| Complexity to manage | You still need to handle whatever records and reporting apply to you | Can add another layer of program rules and eligibility checks to get right |

A practical detail: some platforms attach incentives to specific IRA programs. For example, Public.com advertises a 1% match on annual contributions for Traditional and Roth IRAs. Treat offers like this as a bonus, not the reason you choose the account. Verify the program rules in writing.

The IRA fork you must name (Traditional vs Roth)#

You will see Traditional IRA and Roth IRA as two common branches. They come with different rule sets, and the details can affect eligibility and reporting. Do not guess. Confirm what applies to you with your broker's disclosures and a qualified tax professional.

Hypothetical: you take on an overseas client, spend part of the year traveling, and your tax residency changes. That shift can change what rules apply to you and what you need to report. Use this as your cue to pause, confirm the rules, then continue.

Cross-border warning you should treat as non-negotiable: residency rules can get detailed, and outcomes vary by jurisdiction. Even the IRS publishes guidance with sections like "Dual-resident taxpayers who are Canadian residents under a tie-breaker rule," which signals how detailed these questions can get. If you live or work across borders, start with a local pro and a broker that supports your residency profile. You may also want to review: Tax Implications for an Australian Resident Owning a US LLC.

Picking your funds like an operator: costs, coverage, and "don't-sabotage-yourself" guardrails#

Keep it simple on purpose: pick one broad, diversified fund (or ETF) you can hold through boring months, and add another only when you can explain the "why" in one sentence. After you choose an account container, brokerage account vs IRA, the next risk sits inside the container: scattered holdings, unclear fees, and avoidable admin work.

Start with one core holding you actually understand#

Here, simplicity protects consistency. The goal is not to collect funds. The goal is to keep buying the same thing on schedule when clients pay late.

A safe operating rule: start with a single broad-market fund you can describe without Googling. What "broad-market" means depends on what's available where you live and what your broker actually offers, so focus on the fund's stated exposure, the index it tracks or the market it targets, not the hype.

Treat "diversify by buying a bunch of stuff" as a trap unless you verify what you own. A random internet answer even advises, "Divest your $ into several programs, one being mutual funds." That kind of guidance nudges you toward spreading money around. It does not tell you what the funds hold, what they cost, or what paperwork they create.

Hypothetical: you add eight niche ETFs because each sounds smart. Three months later you cannot explain your exposure, you stop contributing, and you "wait for a better time." That is self-sabotage disguised as strategy.

The operator checklist: costs, overlap, and tax friction#

Run this checklist before you buy, and again before you add a second fund:

- Fees you can see: Find the fund's expense ratio in the official fund documents. If you're comparing providers, compare the same fund type and exposure, not just the brand name.

- Fees you forget: Confirm trading commissions, transaction fees, and minimums inside your specific brokerage account. Brokers change policies, and your residency can change access.

- Diversification you can prove: Pull the top holdings list for each fund and check how similar they are. Do not assume "more tickers" automatically equals more diversification.

- Tax and distributions you can predict: Mutual funds and ETFs can distribute income, like dividends, and sometimes other payouts. Tax treatment varies by jurisdiction and account type, so verify how it works where you live before you commit.

| Guardrail | What to check | "Green light" signal |

|---|---|---|

| Costs | Expense ratio, broker fees, minimums | You can explain total ongoing costs in plain language |

| Coverage | Index tracked, geography, market cap focus | You can name the exposure you want and why |

| Overlap | Top holdings, sector weightings | Each additional fund adds a clear new exposure |

| Tax friction | Distribution policy, local tax handling | You understand what paperwork and tax implications might apply |

The monthly freelancer investing workflow (with a reusable checklist you can run every pay cycle)#

Each cycle, reconcile cleared cash, label what kind of month it is, follow your written plan, and stop if your buffer slips. This is the execution layer that keeps late payments from turning long-term investing into a stressful weekly debate.

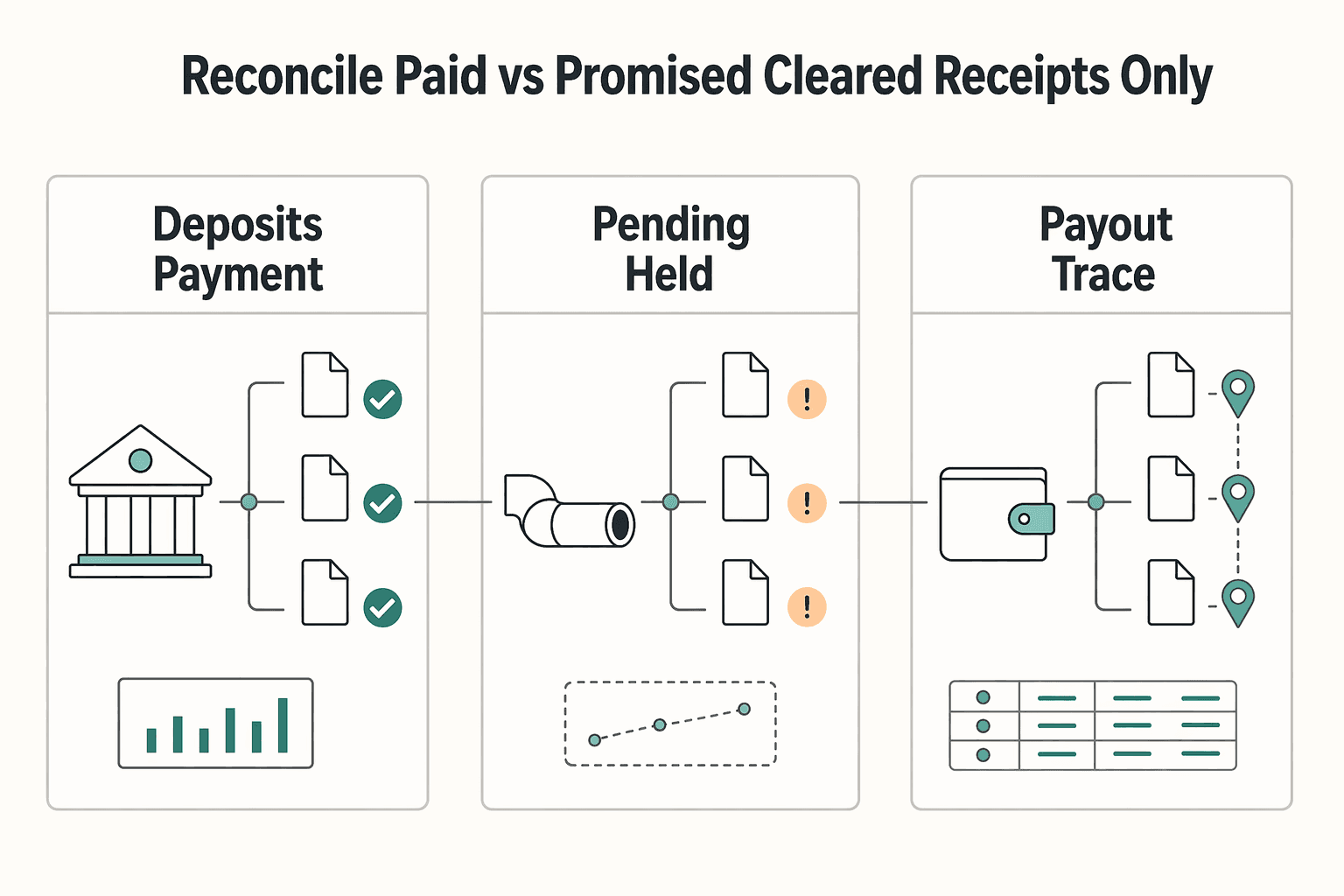

Step 1: Reconcile "paid vs promised" (cleared receipts only)#

Your investing amount should come from cleared money you can prove, not invoices you sent or money that "should land any day." Treat receivables like a pipeline, not cash.

| Check | Action | Why |

|---|---|---|

| Deposits and payment processor payouts | Match them to invoices or projects | Your investing amount should come from cleared money you can prove. |

| Pending, held, disputed, or reversed items | Separate them from received money | Treat receivables like a pipeline, not cash. |

| Ledger or audit trail | Review the underlying transactions | Keep your number defensible. |

Operator moves:

- Review deposits and payment processor payouts, then match them to invoices or projects.

- Separate "received" from "pending," "held," "disputed," or "reversed."

- If you use tooling with a ledger or audit trail, for example Gruv's ledger-derived balances where enabled, review the underlying transactions so your number stays defensible.

Hypothetical: a client says "paid," but a payout hold delays the deposit. If you act on the promise, you can create a liquidity problem. If you act on cleared receipts, you keep control.

Step 2 to 5: Decide, execute, guardrail, document#

Use a simple month-type rule so you make the decision once, then repeat it.

| Month type | What it signals | What you do (pre-written) | Primary goal |

|---|---|---|---|

| Low | Cash feels tight or uncertain | Pause or reduce contributions | Avoid forced selling |

| Normal | Cash feels stable | Follow your usual contribution | Consistency |

| High | You have real surplus after essentials and buffer | Add extra only if it's truly surplus | Capture upside without lifestyle creep |

Then execute cleanly:

- Execute in the right place: use the account and setup you already chose. Do not improvise mid-month because you "feel good."

- Add one guardrail: adopt a hard rule like "no investing until buffer restored." This matters more than perfect optimization when income fluctuates.

- Document once, reuse forever: keep a one-page note with what you buy, where you buy it, and the rules you follow. This prevents decision fatigue and strategy drift.

Mini checklist (copy/paste):

- Cash buffer above my minimum?

- Any overdue invoices past agreed terms?

- Any payout holds, chargebacks, disputes open?

- Month type: Low / Normal / High

- Planned contribution per my written rule: ___

- Execute in: the account/vehicle I already chose (no improvising)

- Same plan as last cycle (no strategy-switching): Yes/No

The bottom line: a freelancer index-fund plan that won't break when clients pay late#

You do not need a complex portfolio to do this well. A simple plan you can stick with matters more than a fancy one you keep rewriting.

Keep two principles front and center:

- Simplicity beats cleverness. For many people, one broad-market index fund plus a written contribution rule is easier to maintain than a complicated setup.

- Start earlier, but not recklessly. As one investor put it, "the earlier you invest, the greater the potential value that savings has." Use that as motivation to start, then set rules you can live with.

If you implement only one thing#

Write your contribution rules down and follow them using conservative inputs. Do not let optimism run the numbers. If you cannot defend the number without squinting, lower it.

Next step: a one-page setup you can run on autopilot#

Make these four decisions once, then execute without negotiation for a while before you "optimize" anything:

| Decision | Safe default | Your operator rule |

|---|---|---|

| Baseline contribution | Small enough that you can repeat it | If you feel forced to "catch up," your baseline is too high |

| Core fund | One broad index fund | No fund-hopping, no overlapping duplicates |

| Account path | Pick an account you can manage consistently | Do not switch accounts on impulse |

| Execution cadence | A regular cadence you can maintain | Calendar reminder beats vibes |

Copy/paste checklist (run on your cadence):

- Contribution amount: baseline (and only add more if your written rule says so)

- Buy the same core index fund again: Yes/No

- Anything changed that should update my written rules: Yes/No

Frequently Asked Questions

How should freelancers invest in index funds with irregular income?

Treat index fund investing for freelancers like an ops process. Base contributions on cleared receipts, then apply your Low, Normal, High rule. When cash is uncertain, downshift or pause. When cash clears, resume your baseline.

ETF or index mutual fund for freelancers with variable cashflow?

Pick the vehicle that creates the fewest failure points when cashflow swings. ETFs can achieve the same broad index exposure and often have lower investment minimums, which can help when your contribution amount varies. Some index mutual funds have large investment minimums, which can make variable contributions harder. If your contribution size changes month to month, leaning ETF can reduce minimum-related friction. | Decision factor | ETF | Index mutual fund | |---|---|---| | Contribution flexibility | Strong (often lower minimums) | Can constrain you (some large minimums) | | Practical fit when cashflow swings | Often easier to keep consistent | Can be tougher if minimums are high | | Best fit | Variable cashflow | Steadier contributions (when minimums are workable) |

Can I invest before stabilizing client payment risk?

Yes, but only behind a “safe-to-invest” gate that prevents forced selling. Client payment risk (holds, disputes, delays) hits you before market risk does because it can turn an investing plan into a liquidity crisis. If you cannot confidently separate “promised” from “cleared,” invest smaller or pause until your buffer and receipts stabilize.

What account should a freelancer use for index funds: brokerage account or IRA?

You generally need a brokerage account or an individual retirement account (IRA) to buy shares of index funds. Choose based on flexibility versus retirement intent, not vibes. If payment timing surprises are still common, brokerage account flexibility can matter. Do not guess on IRA rules for your situation.

What are the biggest risks of index-fund investing for freelancers?

The biggest operator risk is selling at the wrong time because cashflow broke, not picking the “wrong” S&P 500 fund. Also watch behavior drift (tinkering, fund-hopping) and complexity creep (too many overlapping funds). Keep the setup simple so you stay passive in practice, not just in theory.

How much should a freelancer keep in cash before buying an S&P 500 index fund?

Set a cash buffer you can defend, then invest only what sits above it. I cannot give a universal weeks or months number here, because it varies and a specific threshold is not something to rely on from this guide. Use a decision rule instead: if your buffer dips below your pre-set minimum, treat the month as Low and pause or reduce purchases.

Do index funds create tax liabilities from distributions, and how does that vary by country?

Tax treatment can vary widely by country, account type, and tax residency, so do not assume your friend’s outcome applies to you, especially if you move countries or hold cross-border accounts. Confirm the rules locally for your specific setup. If cross-border tax applies, start with this: Tax Implications for an Australian Resident Owning a US LLC.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Tax Implications for an Australian Resident Owning a US LLC

There is no one-size-fits-all shortcut for US LLC tax decisions across Australia and the United States. Setting up a US Limited Liability Company (LLC) is one step; getting the tax treatment right in both systems is where risk starts. If you are handling **australian owning us llc tax** decisions, treat this as a classification and documentation problem first, not a shortcut hunt. If you run a business of one, your job is to pick the defensible path and keep the paperwork tight.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.