Quick Answer

GST for Australian freelancers works best as a repeatable control system, not a one-off setup. Track GST turnover monthly, run a consistent decision tree for new client patterns, and keep ABN and BAS workflows ready before pressure hits. Use platform settings to execute decisions, but treat compliance as business-wide and escalate early when facts are mixed or unclear.

Stop Guessing GST and Run a 10 Minute Compliance Playbook#

Use a simple decision system, not memory or platform prompts, to manage GST decisions with less stress and fewer mistakes. You do not need tax trivia to start. You need a repeatable rhythm you can run even when work spans countries, clients, and platforms.

Most freelancers create GST confusion by mixing three separate jobs: policy decisions, platform setup, and reporting workflow. This guide keeps them separate so you can move cleanly. Define scope first, run a decision tree second, apply safe defaults third, and escalate fast when risk rises.

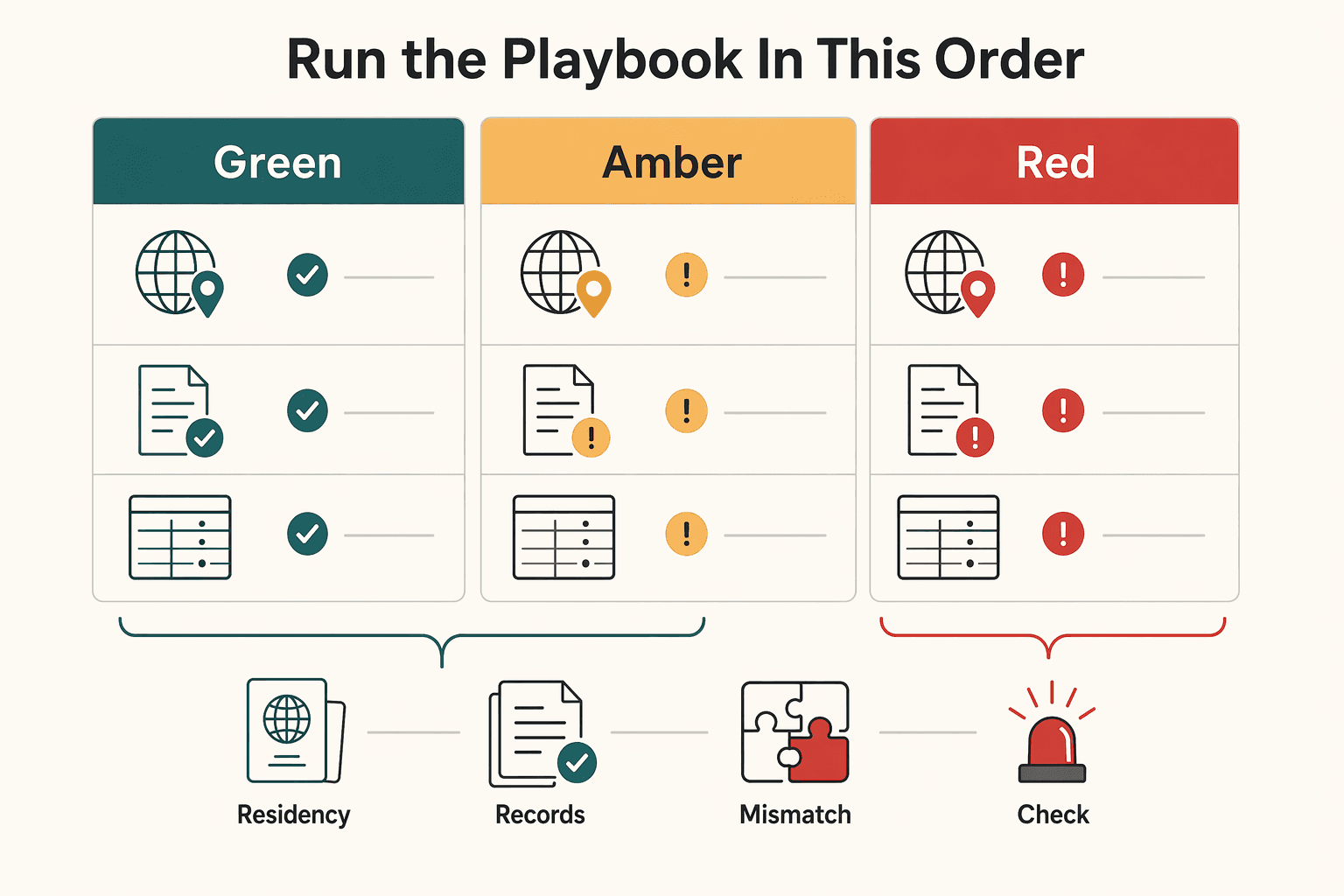

Run the playbook in this order#

- Define scope before action. Capture client location, service type, contract path, and delivery pattern in plain language.

- Run one decision tree for every new pattern. If facts match a pattern you already logged, reuse the prior decision. If facts differ, treat it as a new case.

- Apply safe defaults. When facts feel unclear, pause irreversible steps, mark the case for review, and collect missing documents.

- Separate tools from obligations. Platform settings help you execute inside one channel. They do not replace your broader tax workflow.

- Keep audit notes live. Record what changed, what you decided, and what you still need to confirm so reporting stays controlled, not rushed.

| Risk tier | What it looks like | Action |

|---|---|---|

| Green | Repeating work pattern with consistent client and delivery facts | Follow your checklist and log the decision |

| Amber | Mixed client locations, mixed channels, or unclear service classification | Escalate early and hold assumptions lightly |

| Red | Conflicting interpretations, missing records, or major business model change | Talk to a pro now before you proceed |

If you invoice an overseas client through a platform and a local client directly in the same week, do not debate from scratch. Run the same checklist, assign a risk tier, and escalate amber or red cases immediately. That is practical compliance for a business of one.

If location and residency status are part of what drives uncertainty, pair this with A Guide to Tax Residency in Australia for Digital Nomads. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Build the Core Mental Model Before You Touch Any Forms#

Build your GST model around three decisions, then run every client or platform change through that same model. The playbook only works if the logic stays consistent. Get this clear once, and GST becomes a repeatable process instead of a guess.

Treat GST as something you actively manage, not a one-time setup task. Decision quality comes from clean inputs, especially how you track income and reporting readiness. Keep your workflow simple, but keep it disciplined.

Lock in the three core terms#

| Term | What it means for operations | What to do now |

|---|---|---|

| GST turnover | Total gross income from business activities before expenses | Track it monthly in one sheet so registration decisions come from records, not memory |

| Registration trigger | For most businesses, a cited trigger is $75,000 in annual turnover; some industries, like rideshare, are described as registering from the first dollar earned | Use this as an early warning gate and verify how your activity is treated before acting |

| Business Activity Statement (BAS) | Your regular financial check-in with the ATO and the form used to report and pay several business taxes, not a separate tax | Build records in a way that feeds BAS prep continuously |

Keep decisions consistent as work changes#

When a new client arrangement does not match your usual work, run the three-term check. Classify risk. Pause any irreversible setup until your notes are clear. That pause protects cash flow and reduces cleanup later.

Use this quick control list each month:

- Update GST turnover from your gross-income ledger.

- Check whether your work pattern changed in a way that may affect registration treatment.

- Prepare BAS inputs as you go, not at deadline.

Related: The Best Tools for Creating Professional Presentations.

Do You Need to Register for GST Yet#

Register for GST when your sole trader GST turnover reaches $75,000 or more in any 12-month period, and prepare early when you approach that line. This is not a once-a-year decision. It is a control loop: monitor, decide, document, then act.

Use a turnover gate, not a profit guess. If your turnover crosses the threshold, treat registration as required and move quickly.

Run the threshold gate first#

| Operating state | Decision rule | Immediate action |

|---|---|---|

| Below $75,000 GST turnover (sole trader context) | Registration can be optional | Keep monthly tracking and keep evidence current |

| At or above $75,000 in any 12-month period | Registration is required | Start registration steps immediately and log what triggered the change |

| Close to threshold with uneven income | Treat as amber risk | Prepare ABN and BAS workflows now so you can switch fast |

Set safe defaults before you cross#

| Safe default | Details |

|---|---|

| Track GST turnover monthly in one ledger | So memory never drives tax compliance. |

| Treat this guidance as directional | Confirm final decisions against current primary guidance. |

| Use community commentary for context only | Not as your final authority. |

| Keep ABN details consistent | Across invoicing and platform profiles. |

| Build your BAS process early | With a quarterly rhythm and records ready ahead of time. |

| Once registered, invoice and keep records | In a way that supports charging GST on taxable supplies and retaining records for the required period. |

If a new project mix pushes your revenue pattern up fast, do not debate it in chat threads. Run the same gate, log your evidence, and move to registration prep before pressure hits.

How Should You Treat Overseas Client Work Without Guesswork#

Classify overseas work stream by stream, keep turnover tracking active, and escalate early when facts conflict so your GST decisions stay defensible. You already set your registration gate. Now apply the same discipline to cross-border work, because this is where freelancers drift into guesswork.

Keep turnover tracking clean. The GST turnover trigger still matters, so overseas revenue still belongs in your tracking rhythm, especially as you track progress toward the $75,000 per year registration point. Then run a classification pass for each engagement before you issue invoices.

Run the two-step test in your notes#

| Step | What you record | Decision use |

|---|---|---|

| Income stream facts | What you were paid for, by whom, and the engagement context | Sets the factual base for GST treatment |

| Turnover status | Your running annual business turnover | Keeps registration checks current |

| Escalation flag | Where facts are mixed or treatment is unclear | Triggers early review with a tax professional |

Keep one caution in view: income streams can differ. Do not copy one treatment across your whole business by default. Classify each stream, document why, and escalate unclear cases before lodgement pressure builds.

Keep BAS-ready evidence from day one#

| Evidence step | Details |

|---|---|

| Invoice and payment tags | Tag every invoice and payment with client location and service type when you create it. |

| Decision note storage | Store your decision note beside the transaction so later review stays fast. |

| BAS workflow mapping | Map tags to your Business Activity Statement (BAS) workflow so BAS prep does not become end-period cleanup. |

| If registered | Keep BAS lodgement, GST treatment checks, and eligible expense tracking in view so GST credits are easier to support. |

| Mixed cases | Move cases from green to amber when location facts or treatment logic conflict, then escalate to your tax adviser early. |

If you deliver strategy work to an overseas client while also running a local campaign project, apply the same checklist to both, log the differences immediately, and escalate the mixed case before lodgement pressure builds.

Why Platform Setup Is Not a Full Compliance Strategy#

Use platform settings to execute decisions, not make them. GST obligations apply across your whole business. You now have a decision workflow. Protect it from drift, because risk rises when platform screens or forum posts replace your operating rules.

In Australian GST practice, platform setup is only one layer. Goods and Services Tax (GST) applies to most goods and services sold in Australia, including digital products and online services. Your logic has to cover all income channels, not one app. If your annual turnover reaches or is expected to reach $75,000, registration becomes a business-level decision, not a platform toggle.

Build an authority stack in your SOP#

| Authority level | What it should decide | What it should not decide |

|---|---|---|

| Australian Taxation Office (ATO) | Registration timing, GST turnover monitoring, and reporting obligations | Interface-specific data entry steps |

| ATO community and secondary guidance | Directional context and practical interpretation cues | Final rule decisions |

| Platform docs and commercial explainers | How to configure fields and workflows after you decide policy | Whether your policy is legally correct |

| Forums | Edge-case prompts to investigate further | Binding compliance instructions |

This stack keeps your process stable under pressure. ATO guidance says businesses should monitor earnings for timely registration. After registration, you still need to collect GST on taxable sales and remit it through regular Business Activity Statements (BAS). No platform field can do that governance for you.

Keep execution and governance separate#

- Treat GST and ABN fields in any platform as implementation details.

- Track GST turnover in one master ledger across all channels.

- Map every invoice and payment record to your BAS workflow.

- Escalate if forum advice conflicts with your ATO-based reading.

If you update one marketplace profile and assume the job is done, while direct client invoices continue outside that setup, your data diverges fast. Keep one decision framework, then push that framework into every platform so compliance stays consistent.

Run a Weekly and Monthly GST Control Checklist#

Run a weekly reconciliation and a monthly BAS readiness review to keep GST work predictable and audit-ready. You separated platform setup from compliance. Now make that real with a cadence that covers every invoice stream, so one platform update never hides a business-wide risk.

The point of the checklist is simple: keep your ledger aligned with reality, keep your classifications consistent, and keep BAS inputs continuously ready.

Run the two control loops#

| Control loop | What you check | What you produce |

|---|---|---|

| Weekly | Match invoice records to payment receipts, confirm GST treatment tags, and note GST turnover movement across all channels. | A reconciled ledger, a short exception list, and clear follow-up owners. |

| Monthly | Verify business profile details stay consistent across invoicing tools, marketplace profiles, and accounting software. Build BAS inputs from already reconciled data. | A BAS input pack that is ready before lodgment pressure appears. |

This cadence keeps surprises small, and it turns GST compliance into a system you run, not a deadline you survive.

Lock risk down with logs and gates#

Keep a dated decision log for every material change. Include:

- What changed in process, coding, or client classification.

- Which relevant tax guidance you checked.

- What action you took, who owns it, and when you will review it again.

If you use accounting software, test exports before you need them. Confirm exports preserve invoice IDs, payment references, tax labels, and timestamps so your audit trail stays intact end to end.

If you onboard a new overseas client while a local retainer renews, your weekly check should flag the classification question early. Your log captures the guidance check. Your monthly pack stays clean enough to lodge BAS on time without heroic cleanup.

When Should You Talk to a Pro Instead of Pushing Ahead#

Talk to a tax professional as soon as facts conflict, compliance obligations feel unclear, or a filing decision could materially change your cash position. You already have a routine for record-keeping and deadlines. This is the escalation layer that keeps you safe when the facts stop being clean.

The Australian tax system is layered, and deadlines can pressure even experienced operators. As a sole trader, you and the business are the same legal entity, so tax compliance risk lands on you personally. Escalation is not failure. It is a control.

Use a simple risk tier playbook#

| Tier | Typical signal | Decision |

|---|---|---|

| Green | One clear treatment path, stable operating pattern, and no unresolved interpretation issues. | Self-manage, document your reasoning, and continue your controls. |

| Amber | More than one treatment seems plausible, or compliance obligations and deadlines are becoming hard to manage. | Escalate for professional review before you finalize your filing position. |

| Red | Rule interpretation stays unresolved after your review, or different guidance you reviewed points in different directions. | Stop pushing ahead and get formal advice before lodgment or classification decisions. |

Escalate with an operator brief#

When you escalate, send a tight brief so the adviser can decide fast:

| Brief item | What to send |

|---|---|

| Transaction pattern | The exact transaction pattern that created uncertainty. |

| Planned filing position | The filing position you planned to use. |

| Guidance checked | The guidance you checked and where confidence dropped. |

| Deadline and decision needed | The deadline that matters and the decision you need. |

If your treatment notes start to diverge on similar transactions and you cannot reconcile the interpretation cleanly, that is an amber signal. Move early, get a clear decision path, and then update your SOP so the same edge case does not slow you down twice.

Turn This Into Your Default Operating System#

Use a documented decision framework with safe defaults and escalation gates so your GST process runs like an operating process, not a memory test. You have the pieces. The win is turning them into one system you can run every week, even when client mix and platforms change.

GST turnover is your control metric, meaning gross business income before expenses. Track it on a rolling 12-month view, not by feel. Keep one simple rule visible in your SOP: when you hit or are likely to hit the applicable threshold, registration becomes a priority and you move quickly. Set an ABN gate as well, because you cannot register for Goods and Services Tax (GST) without an Australian Business Number (ABN).

Build one decision system you can run under pressure#

| Control point | Safe default | Why it protects tax compliance |

|---|---|---|

| Decision anchor | Validate rule decisions against current ATO guidance first. | Stops platform or forum drift from rewriting your policy. |

| Threshold gate | Monitor GST turnover weekly and review monthly against your entity type. | Prevents late registration surprises in freelance tax Australia. |

| ABN readiness | Keep ABN details current and confirm ABN readiness before GST registration steps. | You cannot register for GST without an ABN. |

| Platform recordkeeping | If you use freelancer platforms, reconcile platform records with your own invoices and income tracking. | Keeps turnover evidence organized when threshold risk changes. |

Use your playbook baseline as an operating starting point, including the commonly cited $75,000 threshold for most businesses. Then confirm current guidance for your exact facts before you file or change treatment.

Escalate before risk compounds#

If your fact pattern changes, run this sequence immediately:

- Document the assumption that changed.

- Check the latest ATO guidance for that exact fact pattern.

- Escalate before filing if interpretation still feels ambiguous.

If your client mix shifts while your income accelerates, your system should flag the threshold check, record the assumption change, and trigger review early. That is how you keep control and keep compliance repeatable.

For broader context that can affect compliance inputs, use A Guide to Tax Residency in Australia for Digital Nomads.

Frequently Asked Questions

Do Australian freelancers need to register for GST before or after crossing the GST turnover trigger?

The provided guidance here does not set a specific turnover threshold or a before/after timing rule. Do not run this as a last-minute decision: track turnover continuously and keep your records ready so you can act quickly when your status changes.

Is GST always 10% for every freelance service scenario in Australia?

In the provided guidance, GST is described as 10% for most goods and services in Australia (2025 context). If you are GST-registered, it also says you add GST to the prices you charge, but do not treat that 10% figure as a universal shortcut for every invoice.

How does GST treatment change when my clients are overseas?

Overseas-client GST treatment is fact-sensitive. Document your facts clearly, and get professional review when the pattern is mixed or unclear.

Does entering my ABN on Upwork cover all of my GST obligations?

Use Upwork guidance for Upwork workflow only: it explains GST on Upwork, how to add your ABN, what to do if your information changes, and includes guidance for users without an ABN or GST registration. Treat that as platform-specific setup, not a full compliance answer for every channel.

What should I do first if I think I am close to the GST turnover trigger?

First, reconcile your records and maintain one accurate turnover view so you can act quickly once you confirm your status with qualified advice.

When should I stop self-managing and talk to a tax professional?

Talk to a tax professional as soon as your facts are unclear or your records are incomplete. Early review is usually easier than cleaning up decisions later.

Which source should I trust first when ATO, platform docs, and forum advice seem inconsistent?

Trust primary official tax guidance for rule decisions, and use platform docs like Upwork for platform execution details. Treat forum commentary as a prompt to verify, not a final authority.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

The Best Tools for Creating Professional Presentations

Use a 2025-2026 validation sweep each quarter: confirm one monthly software baseline ($15/month), one collaboration baseline ($30/month), and one premium workflow baseline ($60/month) before changing client-facing tool commitments.