Quick Answer

Start by sorting transfers into clear lanes before you file gift tax for US expats. For inbound gifts, determine donor type, separate trust distributions from non-trust gifts, and then test reporting triggers for Form 3520. For outbound transfers, run a distinct Form 709 review so giver-side facts stay separate. The article’s practical point is that classification and documentation drive compliance more than late-stage form entry.

What US Expats Need to Know First#

Keep filing season calmer by deciding early which lane each transfer belongs in: Form 3520 or not reportable under these rules. For a U.S. person living abroad, the practical order is to get the U.S. filing lane right first, then sort the cross-border details that raise risk.

The core trap is simple. A foreign gift or bequest can be excluded from gross income and still be reportable. Not taxable does not automatically mean not reportable, and that is where many expat filings go wrong.

Start with donor identity before you think about form names. A foreign person can be a nonresident alien individual, a foreign corporation, a foreign partnership, or a foreign estate. If you received a large gift or bequest from a foreign person, Part IV of Form 3520 may apply, but only if the threshold is met. When testing that threshold, aggregate gifts from related parties.

That sequence matters because most filing mistakes start as classification mistakes. If you classify correctly on day one, later choices become mechanical. If you classify late, every later step gets harder, including document collection, threshold testing, and final review. Use this pre-filing screen before software entry or preparer handoff:

- Classify each received transfer, then tag donor type.

- For received amounts from foreign persons, test threshold status after combining related-party gifts.

- Flag missing donor details, inconsistent transfer descriptions, or mixed entity and personal funding.

- Record your filing decision and the facts behind it.

Treat timing as a control, not an afterthought. Late, incomplete, or incorrect Form 3520 filings can trigger section 6039F(c) penalties if reasonable cause is not established. The filing timing is the 15th day of the fourth month after the end of your income tax year, generally April 15 for individuals.

If you only do one thing after reading this article, build your transfer list early and attach a provisional lane to each item. You can refine details later, but early lane assignment prevents last-week filing chaos.

Start with the two gift paths that drive every decision#

Put each transfer into two paths before anything else: receipt from a foreign person (the Form 3520 lane) or gifts you make (a separate lane outside this section). That first split removes most avoidable errors.

- Path 1: Receipt from a foreign person. Start with donor type: nonresident alien individual, foreign estate, foreign corporation, or foreign partnership. If you received a large gift or bequest, Part IV of Form 3520 may apply only if the applicable threshold is exceeded. Aggregate gifts from related parties before testing.

- Path 2: Gifts you make. Handle this separately from the foreign-person receipt analysis.

If both paths occur in the same tax year, run two independent analyses and make two separate filing decisions. Keep trust and non-trust receipts separate as well: foreign trust distributions go to Part III of Form 3520, not Part IV.

A common failure mode is trying to solve both paths in one combined worksheet and then carrying assumptions from one side to the other. That creates noise fast. Keep each transfer in one lane first, then reconcile totals and timing across the full return package.

When facts are incomplete, assign a temporary lane and mark the missing evidence required to confirm it. That keeps progress moving without pretending certainty. You are not delaying decisions. You are staging them in the right order.

Define the key terms before you touch a tax form#

Define the terms first, because they determine how you classify a transfer and which part of Form 3520 may apply.

- Foreign gift or bequest: an amount received from a person other than a U.S. person that you treat as a gift or bequest and exclude from gross income.

- Foreign person: a nonresident alien individual, foreign corporation, foreign partnership, or foreign estate.

- Part IV of Form 3520: the section a U.S. person may need to complete when receiving a large gift or bequest from a foreign person.

- Foreign trust distribution: reported on Part III of Form 3520, not Part IV.

Then apply threshold logic. Reporting is required only when the applicable threshold is exceeded, and gifts from related parties must be aggregated. Testing each transfer in isolation can produce the wrong result.

Not every incoming transfer is treated as a foreign gift. Qualified tuition and qualified medical payments made on behalf of the U.S. person are excluded from foreign gift treatment, so keep records showing payer, beneficiary, and payment purpose.

Treat those definitions as filing controls, not just vocabulary. If your team uses different wording for the same transfer, pause and standardize labels before anyone starts form prep. One consistent label set can reduce duplicate work and conflicting draft positions.

If your notes include covered expatriate or US-situs property, flag those for separate analysis. Before filing, recheck Part III versus Part IV, related-party aggregation, and any exclusion. Then calendar Form 3520 for the 15th day of the fourth month after year-end, generally April 15 for individuals. Late, incomplete, or incorrect filing may trigger section 6039F(c) penalties if reasonable cause is not established.

A practical check at this stage is to ask whether an independent reviewer could classify each transfer using only your memo and source documents. If not, your definitions are probably too loose and need tightening before filing starts.

Decide when Form 3520 is required for gifts you receive#

Part IV of Form 3520 may be required only in specific situations, not for every transfer from abroad. Start by confirming the transfer is a foreign gift or bequest, then apply the threshold test.

| Check | What to do |

|---|---|

| Gift or bequest | Confirm the transfer is a gift or bequest from a foreign person |

| Foreign trust distributions | Separate foreign trust distributions from non-trust gifts or bequests |

| Related parties | Aggregate gifts from related parties before testing the applicable threshold |

| Qualified tuition or medical payments | Exclude qualified tuition and qualified medical payments made on behalf of the U.S. person |

| Threshold | File Part IV only if the applicable threshold is exceeded |

Confirm donor type early. A foreign person can be a nonresident alien individual, foreign estate, foreign corporation, or foreign partnership, and an applicable threshold applies. Keep foreign trust distributions out of this lane because those are reported in Part III, not Part IV. Then work through the checks in that order.

The order matters because each step narrows the decision. If you test thresholds before classifying trust status and donor type, you can waste time proving numbers that do not control the filing result. Classification first, threshold second, filing action third is the cleaner order.

For cleaner internal review, keep donor identity support, transfer evidence, and your aggregation calculation together. You want one review trail from fact to form line.

Final gate: file Form 3520 on time and with complete information. The due date is the 15th day of the fourth month after year-end, generally April 15 for individuals. Late or incomplete filing can create section 6039F(c) penalty exposure when reasonable cause is not established.

Decide when Form 709 is required for gifts you give#

Form 709 is the giver-side return for gifts you make. It does not replace recipient-side Form 3520 reporting, which may apply separately for certain foreign gifts or bequests. Use this decision sequence before deciding to file:

- Confirm the transfer is outbound from you as the giver.

- Keep each gift in its own record with recipient, relationship, date, and asset type.

- Check how the transfer is treated under applicable U.S. gift tax reporting rules.

- If you are claiming special tax treatment, collect supporting documentation before finalizing.

- Keep Form 709 analysis separate from any Form 3520 file so giver and recipient reporting do not mix.

Most confusion in this lane comes from blending giver-side and recipient-side facts in one narrative. Keep separate records for what you gave and what you received, even if the events happened in the same year. That split can make later review and any needed amendments easier.

If you are gifting while moving countries, set your U.S. filing position first, then ask local counsel to test local gift or inheritance treatment. When key facts are unresolved, document assumptions and resolve them before submission.

A useful habit is to add a short decision note for each outbound transfer. Explain why it belongs in the Form 709 lane and what evidence supports that call. Those short notes save time when questions come back months later.

Handle the covered expatriate exception before it surprises you#

Run a covered expatriate check before finalizing any gift filing position when the donor previously held U.S. citizenship or long-term green card status. If that flag appears, do not assume standard gift-reporting assumptions settle the case.

Under IRS expatriation rules, IRC sections 877 and 877A apply to certain expatriating U.S. citizens and certain long-term residents who end U.S. resident status for federal tax purposes. For expatriations on or after June 17, 2008, IRS says the newer 877A rules apply when the listed tests are met. Covered expatriate status is test-based and includes Form 8854 certification history, including whether five years of U.S. tax compliance were certified. IRS also lists a 2025 five-year average annual net income tax test of $206,000 and a net worth test of $2 million or more.

Because this issue can get mixed into routine gift classification, use a dedicated checkpoint:

- Capture donor profile: former U.S. citizen or former long-term resident, plus expatriation date.

- Gather status-testing support, including Form 8854 history where available.

- Flag 877A indicators in your notes, including the $206,000 (2025) income tax test and the $2 million net worth marker.

- Keep this review separate from ordinary gift-reporting lanes.

The legal pivot is IRC section 2801, which final regulations describe as applying tax to U.S. citizens and residents, and certain trusts, that receive covered gifts or bequests directly or indirectly. That is why this exception is often misclassified when teams rely only on standard gift-reporting assumptions.

Treat Form 708 as a professional-review trigger, not a clerical step. Public summaries can conflict on rollout timing and availability, so confirm current IRS materials and instructions before locking your next move. If facts suggest section 2801 may apply, escalate early and document assumptions and donor-status evidence in the file.

In practice, this checkpoint can pay off even when the final answer is that section 2801 does not apply. You still get a cleaner file, clearer reasoning, and a documented basis for the position you took.

When escalation is needed, frame the question tightly for the reviewer: donor status, expatriation facts, transfer facts, and the specific decision you need confirmed. Focused questions tend to get faster, better answers than broad requests for general review. If mobility planning is part of the bigger picture this year, How to Negotiate a Long-Term Stay Discount on Airbnb may help on the non-tax side.

Separate gift reporting from income and asset reporting#

Keep three lanes separate: gift classification, asset or account disclosure, and income reporting. They are related, but they are not the same filing decision. A foreign gift or bequest can be excluded from gross income when received, while later earnings from that asset may still be reportable under normal income rules.

| Topic | Article rule |

|---|---|

| Gift lane | For amounts received from a non-U.S. person, you may need Part IV of Form 3520 |

| Trust distributions | If the receipt is a foreign trust distribution, report it in Part III of Form 3520, not Part IV |

| Related-party gifts | Aggregate related-party gifts when testing whether foreign-gift reporting is required |

| Form 8938 | Form 8938 is attached to the annual income tax return when specified foreign financial assets exceed the applicable threshold |

| FBAR | Filing Form 8938 does not eliminate FBAR (FinCEN Form 114) requirements |

| No income tax return | If no income tax return is required for the year, Form 8938 is not required |

| Later earnings | Later earnings from that asset may still be reportable under normal income rules |

In practice, use the gift lane for transfer characterization and the asset or account lane for holdings disclosure. Keep those decisions separate even when the same transfer touches more than one filing.

The practical risk here is duplication or omission. If the same account appears under multiple internal labels, one reviewer may assume another reviewer already handled it. A simple lane map removes that ambiguity and clarifies where each item belongs, including when more than one filing may apply.

Run a lane map checkpoint#

Before filing, map each account or asset touched by a transfer to the correct lane(s) so nothing is omitted or duplicated.

- Identify source and legal character first (gift or bequest versus foreign trust distribution).

- Assign the applicable filing lane (

Form 3520Part IV,Form 3520Part III,FBAR, and/orForm 8938). - Note where later income from that asset will be reported.

- Verify timing, including

Form 3520by the 15th day of the fourth month after year-end, subject to extension.

Over-reporting creates noise and amendment risk. Under-reporting creates penalty risk. Keep each obligation in its lane, then connect that lane to related income reporting.

A lane map also helps during handoffs. If you switch preparers or ask for a second review, the reviewer can follow your logic without rebuilding the entire file from raw statements and emails.

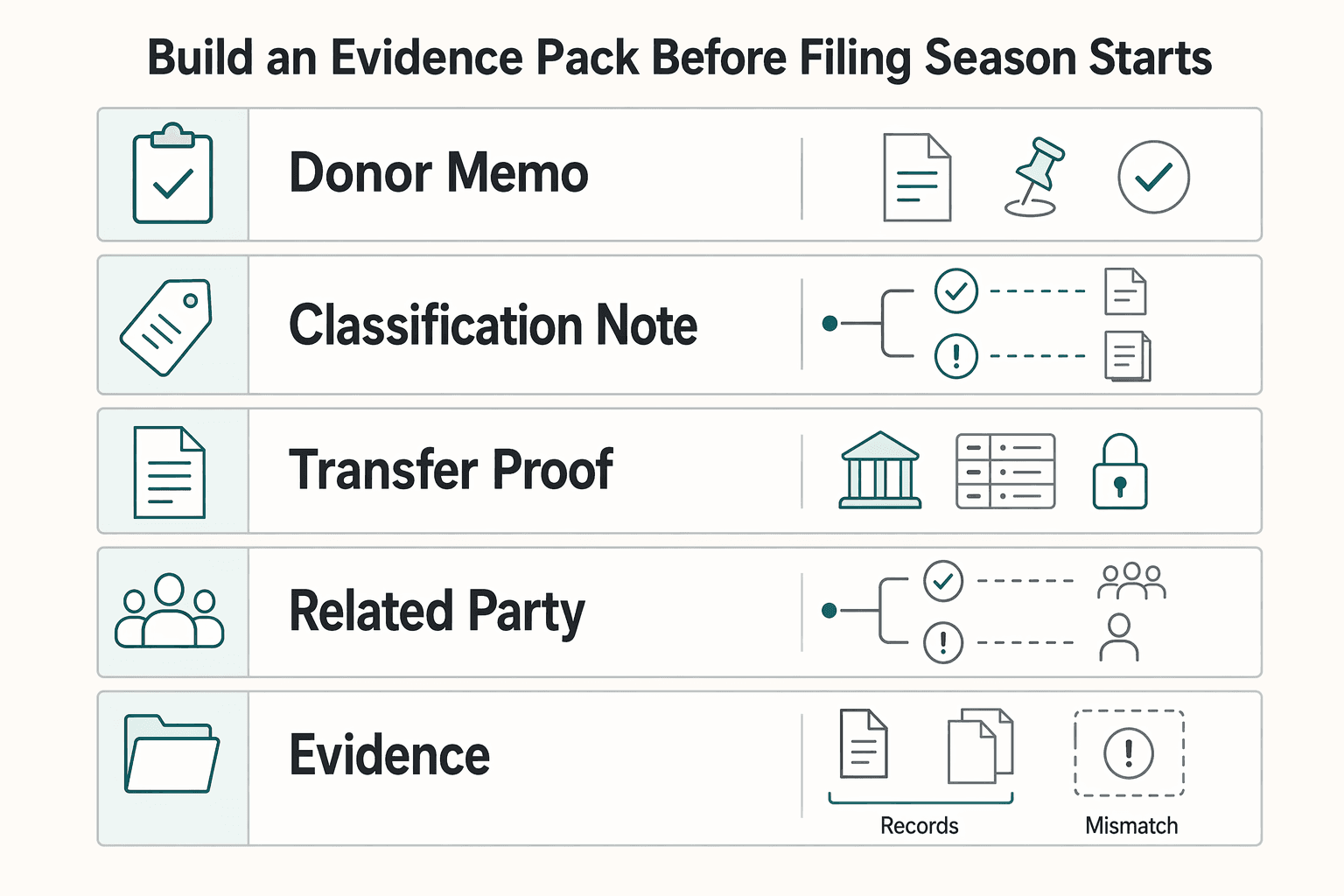

Build an evidence pack before filing season starts#

Build one evidence file per transfer before filing season starts. In practice, documentation gaps can create risk, especially when donor classification is unclear. Start with a donor memo for each transfer:

| File item | What to include |

|---|---|

| Donor memo | Legal identity and relationship; jurisdiction; source type: individual, corporation, partnership, estate, or trust-linked arrangement; a short trust-risk screen if the structure is mixed or unclear |

| Classification note | A one-line classification note tying facts to the lane reviewed, such as Part IV versus Part III of Form 3520 |

| Transfer proof | Bank confirmations; gift letters; valuation support when relevant; legal correspondence on intent or ownership; a dated index that maps each file to a specific transfer |

| Related-party aggregation log | Who is treated as related, why they are grouped, and the combined annual amounts used for the reporting decision |

| Timing record | Track Form 3520 by the 15th day of the fourth month after year-end, subject to extension |

Add a one-line classification note tying facts to the lane reviewed, such as Part IV versus Part III of Form 3520. If trust-distribution indicators appear, route to Part III analysis because foreign trust distributions are reported there, not in Part IV.

Keep transfer proof in the same file set so reviewers can trace each transfer quickly, and maintain a dated index that maps each file to a specific transfer.

Maintain a related-party aggregation log for the tax year aligned with IRS instructions. Record who is treated as related, why they are grouped, and the combined annual amounts used for the reporting decision.

Track timing in the same file: Form 3520 is generally due by the 15th day of the fourth month after year-end, subject to extension. If donor classification is uncertain, document your conservative assumption and escalate early. Late, incomplete, or incorrect Form 3520 filings can trigger section 6039F(c) penalties when reasonable cause is not established.

The evidence file should answer three questions without extra calls: what happened, why it was classified this way, and what was filed. If any of those answers is hard to find, tighten the file before submission.

A useful operating habit is to date-stamp decision notes and keep older notes instead of deleting them. That creates a clear history when facts change during review.

Also confirm consistency between your donor memo and your aggregation log. If names, relationships, or source types differ across documents, reviewers can challenge your threshold analysis even when your math is correct.

Use a filing calendar that prevents late and incomplete returns#

Use one filing calendar with enforced internal checkpoints so filings are complete before deadlines. Put Form 3520 on the schedule, set internal dates ahead of the filing date, and require a documented extension decision point instead of a last-minute call. If another related return may apply, confirm current IRS instructions before locking assumptions.

For Form 3520, anchor timing to the known rule: file by the 15th day of the fourth month after year-end, generally April 15 for individuals, subject to extension.

The calendar works best when each date has a clear output. Do not use calendar entries that only say review. Tie each checkpoint to a specific artifact such as updated aggregation math, completed donor memo, or signed classification note.

Pre-filing QA gate#

Run this checklist before signing or transmitting:

- Confirm donor type and transfer character.

- Recompute related-party aggregation and retain the math.

- Select the correct

Form 3520lane:Part IV of Form 3520for reportable foreign gifts or bequests,Part III of Form 3520for foreign trust distributions. - Confirm threshold testing was performed without assuming unsupported dollar amounts.

- Check whether qualified tuition or medical payments made on behalf of the U.S. person are excluded from foreign gift treatment.

- Verify attachment completeness: donor memo, transfer proof, aggregation log, and classification support.

If donor classification is still uncertain at this gate, document a conservative assumption and escalate immediately.

This pre-filing gate helps catch avoidable defects. It is usually better to hold the file briefly than to file incomplete information and respond to follow-up issues later.

Post-filing checkpoint#

After filing, confirm filing status, save a locked copy of what was filed, and archive it under the same tax-year index as the evidence file. Include the final QA checklist, extension records, and decision notes so the position can be defended later.

This control is worth the effort. Late, incomplete, or incorrect Form 3520 filings can create section 6039F(c) penalty exposure when reasonable cause is not established.

Post-filing review is also where you improve next year. Note which documents were hardest to obtain, where classification changed late, and which assumptions required escalation. Those notes shorten the next cycle and reduce deadline pressure.

Red flags that mean stop DIY and talk to a pro#

Stop DIY if a transfer may involve a covered expatriate or the facts are too complex to classify with confidence. A filing calendar helps with timing, but it does not resolve narrow, fact-sensitive rules like IRC section 2801.

IRC section 2801 applies to U.S. citizens and residents, including trusts, that receive covered gifts or covered bequests from covered expatriates, directly or indirectly. If your file shows expatriation signals and you cannot resolve donor status from documentation, treat that as a professional-review trigger before finalizing.

Escalate when these facts appear#

- Possible covered expatriate donor, or any pattern suggesting

IRC section 2801may apply. - Transfers with unresolved donor facts or conflicting documentation that affect whether a transfer is a covered gift or covered bequest.

- Entity or trust involvement that makes application of

IRC section 2801unclear. - Cross-border facts that leave U.S. classification uncertain.

Use a hard checkpoint: if classification is uncertain, pause and escalate. Keep the handoff focused with a donor timeline, the conflicting facts, and the exact determination you need. If legal interpretation is central to the decision, verify against current official editions before locking positions.

Escalation is not a failure. It is a control to prevent you from filing with unresolved legal classification risk. Early escalation can help avoid post-filing correction. For another risk-screening lens, see 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Practical checklist for globally mobile freelancers and consultants#

Use this as a final filing gate. Separate documentation, Form 8938/FATCA checks, and FinCEN Form 114 (FBAR) checks before submission.

Five-step filing check#

- Confirm whether

Form 8938is in scope. Verify you are a specified person; if no income tax return is required for the year,Form 8938is not required. - Build a minimum evidence file. Keep account and transfer records, valuation support when relevant, and a short facts memo for each reporting decision.

- Run non-gift checks in parallel. Review

FATCAreporting throughForm 8938and separately check whetherFinCEN Form 114 (FBAR)is required. FilingForm 8938does not replace FBAR filing when FBAR otherwise applies. - Confirm current-year

Form 8938instructions before filing and attach the form to your tax return when required. Thresholds are not one-size-fits-all, and higher thresholds can apply for joint filers or taxpayers residing abroad. - Set a stop-and-escalate checkpoint before signature. If facts conflict, records are incomplete, or classification is uncertain, pause and get professional review before submission.

A simple tracking sheet helps: transfer, filing lane, evidence status, non-gift check status, and escalation decision. It keeps open items visible and makes handoffs cleaner when another preparer reviews the file.

To make this checklist useful in real life, assign an owner and a completion date to each step for each transfer. Unassigned checklist items tend to stay open until the filing deadline, when mistakes can be hardest to fix.

Also store the checklist with the evidence file, not in a separate task app only one person can access. If someone else must step in, they should be able to see status and reasoning in one place.

Conclusion#

The practical path is straightforward: classify the transfer correctly, choose the right reporting lane, and document facts before deadlines.

Costly errors often come from unclear donor classification, covered expatriate risk, or weak records, not difficult calculations. Separate recipient-side reporting from giver-side analysis first, then map each transfer to one lane.

For recipient reporting, use this facts-first check before you finalize any filing lane:

- If you received gifts or bequests from a nonresident alien or foreign estate, test the annual aggregate. Once it exceeds

$100,000,Part IV of Form 3520may be required, and each gift above$5,000must be separately identified. - If the transfer is a foreign trust distribution, report it in

Part III of Form 3520, not the foreign-gift lane. - Aggregate gifts from related parties when testing thresholds.

For execution, timing and filing mechanics matter as much as classification:

Form 3520is filed separately from the income tax return.- The due date is tied to the 15th day of the fourth month after year-end, generally April 15 for individuals, subject to extension.

- If facts are incomplete, use a conservative filing position and document that assumption.

Escalate early on these two edge cases:

- Purported gifts from foreign corporations or partnerships: if the annual amount exceeds the applicable reporting threshold, separately identify each gift and donor, and account for recharacterization risk.

- Any donor who may be a

covered expatriate, becauseIRC section 2801can impose transfer tax on U.S. recipients, including trusts, for covered gifts and bequests.

Keep a compact evidence file: donor classification memo, transfer proof, related-party aggregation log, and filing records, including extensions and confirmations. That documentation is what keeps positions defensible if an incomplete or incorrect filing is questioned.

If you want a practical next step, run one pass through your current-year transfer list. Assign a provisional lane, missing evidence, and escalation status to each item. That single pass turns a vague filing burden into a manageable set of decisions. If you want confirmation on what is supported for your specific country or program, Talk to Gruv.

Frequently Asked Questions

Do U.S. expats owe tax when they receive foreign gifts?

Treat whether a received foreign gift is taxable income as a facts-and-instructions question for the specific filing year, not a one-size-fits-all rule. If key donor or transfer facts are unclear, get professional review before filing. Start with classification and documentation before debating outcome, because if donor type or transfer character is uncertain, a taxability conclusion may be premature.

When does `Form 3520` become required for a foreign gift?

This section does not include the trigger rules or thresholds for Form 3520. Check current IRS instructions for your filing year and match them to your documented facts. Do not rely on prior-year assumptions. Use your records during this check so instructions are applied to your actual facts, not memory of prior returns.

What is the practical difference between `Form 3520` and `Form 709`?

Use current IRS form instructions to confirm the mechanics and scope difference between Form 3520 and Form 709, and to determine which filing lane applies to the transfer you are documenting. If classification is ambiguous, escalate before submission. One practical safeguard is to keep recipient-side and giver-side records separate until each lane decision is final.

Can gifts from a `covered expatriate` be taxed under `IRC section 2801`?

Treat covered expatriate scenarios under IRC section 2801 as issues that need current authoritative guidance. Escalate instead of making a DIY determination. If section 2801 may be relevant, include donor-status facts and the specific unresolved question when you escalate.

If the gift itself is not taxable income, what can still be taxed later?

Separate gift characterization from foreign-asset reporting obligations. Form 8938 is used to report specified foreign financial assets above the applicable threshold and is attached to your tax return. Filing Form 8938 does not remove an otherwise required FBAR filing. The key distinction is filing lane: gift-related classification questions are separate from foreign-asset and account-reporting obligations.

How do `FBAR` and `Form 8938` relate to gift-tax reporting?

FBAR and Form 8938 are separate reporting obligations and are not substitutes for each other. Form 8938 is attached to your income tax return, and filing it does not relieve an otherwise required FinCEN Form 114 (FBAR). If you are not required to file an income tax return for the year, you do not need to file Form 8938 for that year. Treat gift reporting and account reporting as connected but separate checks so one filing decision does not accidentally overwrite another.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

How to Negotiate a Long-Term Stay Discount on Airbnb

Your first job is not to squeeze out a discount. It is to secure a workable place on the right dates without turning your move into a waiting game. If you want to negotiate Airbnb long-term stay pricing, treat it like a housing decision with deadlines, not a casual back-and-forth.