Quick Answer

E&O insurance for software developers is professional liability coverage designed for client claims that your work caused financial harm. The practical way to buy it is to map your service risks, compare policy structure and limits, pressure-test key clauses, and verify claims-made continuity before bind. This helps you avoid gaps, reduce ambiguity with brokers, and make a defensible decision you can repeat at renewal.

Build Your E&O Decision in One Sitting Without Buying the Wrong Policy#

Use a software-specific e&o insurance for developers checklist to shortlist policies fast, pressure test the terms that decide claims, and confirm bind details before you buy.

If you search for developer E&O, some high-ranking pages target real estate development risk, not client delivery risk for a software developer. That mismatch can push you toward broker marketing copy instead of a practical buying framework. This guide resets the process so you evaluate coverage through the lens of real delivery exposure.

As the CEO of a business-of-one, you need an insurance decision process that is fast, defensible, and easy to rerun at renewal.

Professional liability insurance is the same category as errors and omissions coverage. Treat it as one part of your broader risk management system. You will leave with a repeatable way to build a shortlist, challenge vague wording, and run a focused call with insurance brokers before you bind.

What you will complete in one sitting#

- Build a three-option shortlist that matches your current service model.

- Pressure test policy wording for client work, not generic tech insurance language.

- Prepare a broker question set that exposes ambiguity before purchase.

- Separate this decision from adjacent policies like General Liability Insurance.

Imagine you deliver a custom integration and a client claims your work caused financial harm. A generic quote does not tell you enough. A checklist does. You can verify fit, claims obligations, and decision ownership in one focused review.

Confidence guardrails before you decide#

This playbook gives operational guidance, not legal advice. Coverage terms vary by carrier, state, and program structure. Confirm final wording on the exact form you plan to buy.

If a quote sits in Surplus Lines markets, confirm the implications directly. Non-admitted programs may not include the same protections as admitted markets, and rules vary by state. The details that matter show up in the form language and bind documents.

| Verify before bind | Why it matters |

|---|---|

| Policy language fits software services | Prevents buying wording built for another industry |

| Professional liability vs General Liability scope is clear | Helps avoid gaps around negligence-type service claims |

| State and program differences are documented | Reduces avoidable surprises during claims |

If you want a broader baseline first, read Liability Insurance for Freelance IT Consultants: Do You Need It?, then return here to choose your setup with tighter criteria.

Who Should Use This List and How We Score Each Option#

Use this list if you sell software services and need a repeatable way to evaluate tech E&O options against real client delivery risk.

With the market noise out of the way, the next job is fit. This section covers who this framework is built for, who it is not built for, and how to score options so broker copy does not drive your decision.

Confirm fit before you compare quotes#

Use this framework when your business matches one of these profiles:

| Profile | When it fits | Key differentiator |

|---|---|---|

| Service builder | Provides software development services through scoped builds, retainers, or implementation support | Core exposure comes from client allegations of third-party financial loss tied to mistakes, failure to deliver, or negligence |

| Professional services operator | Buys professional liability coverage for service quality disputes, not broad slip-and-fall style events | Claim categories can include negligence and misrepresentation, which sit inside errors and omissions |

| Non-fit profile | Runs heavily regulated, enterprise-only programs that may require manuscript forms and specialist placement | Likely needs structuring beyond standard professional liability insurance shopping flows |

- Service builder. You provide software development services through scoped builds, retainers, or implementation support. Key differentiator: your core exposure comes from client allegations of third-party financial loss tied to mistakes, failure to deliver, or negligence.

- Professional services operator. You buy professional liability coverage for service quality disputes, not for broad slip-and-fall style events. Key differentiator: claim categories can include negligence and misrepresentation, which sit inside errors and omissions.

- Non-fit profile. You run heavily regulated, enterprise-only programs that may require manuscript forms and specialist placement. Key differentiator: you likely need structuring beyond standard professional liability insurance shopping flows.

If a quote packet highlights eligibility like $50 million in professional fees or $500 million in annual construction value, treat it as a fit warning. Those thresholds can signal a real-estate developer program, not software-first tech insurance.

Score each option with a reusable operator rubric#

Ignore brand hype. Score practical usefulness with the same four checks every time.

| Scoring item | What to verify | Why it changes your outcome |

|---|---|---|

| Scope match | Does wording match your real services and third-party financial-loss exposure? | Tech E&O is designed around client financial-loss allegations tied to professional mistakes or failure to deliver. |

| Claim type fit | Do terms clearly handle professional liability triggers such as negligence or misrepresentation? | Professional-liability claims can include these categories, not just broad general-liability events. |

| Cost structure | Score Deductible and Retention (SIR) separately, then model what cash you pay before insurer money starts. | Higher deductibles often lower premium, while retention is insured-paid before the policy responds. |

| Market fit | Check whether eligibility signals align with software services. | Some E&O programs are built for other industries, so poor fit can appear before you even compare terms. |

Example scenario: a client says your integration caused billing issues and revenue loss. Your scorecard lets you pressure-test policy response before you bind. That keeps the decision disciplined and practical.

If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

What Does E&O Actually Cover for Software Developers and Where Does General Liability Stop?#

Use e&o insurance for developers to handle client allegations tied to your professional work, and use General Liability Insurance for bodily injury, property damage, and personal or advertising injury exposure.

Once you can score options, you need a clean boundary between policy types. That boundary keeps your shortlist grounded in real service risk, not vague tech insurance labels.

For a software developer, Errors and Omissions (E&O) Insurance and Professional Liability Insurance point to the same core coverage family. This coverage targets negligent acts and omissions in professional services that harm clients, including allegations like negligence or misrepresentation. General Liability Insurance serves a different job and focuses on non-professional negligence exposures.

Know which policy should lead the review#

Most confusion starts when buyers expect one policy to solve every dispute. Use this operator map instead.

| Coverage lane | Typical trigger | Key differentiator |

|---|---|---|

| Professional liability (E&O) | Client alleges your delivery error caused financial loss | Built for service mistakes and omissions tied to your work product |

| General liability | Bodily injury, property damage, or personal and advertising injury claim | Built for non-professional negligence events, not core service performance disputes |

| Policy mechanics check | Claim lands in a gray area | Policy form, exclusions, and Defense Costs language decide practical response |

Example scenario: you ship an integration, the client claims transaction errors, and revenue drops. Route the analysis first through professional liability, then confirm whether the wording includes or limits that allegation pattern.

Pressure test wording before you bind#

Run this short checklist with your broker so the decision stays concrete:

| Test | Broker prompt |

|---|---|

| Boundary test | Which parts of my service catalog sit in E&O, and which do not? |

| Defense-cost test | How does this form handle defense costs and damages up to policy limits? |

| Exclusion test | Which exclusions could block my most likely client dispute types? |

| Jurisdiction test | If placement uses Surplus Lines, ask how wording may vary by state and program structure. |

| Decision test | Ask for written confirmation of assumptions before bind, so renewal teams can reuse the same logic. |

This prevents false confidence from broad policy names. It also forces clarity where claims decisions actually get made.

How Should You Choose Limits and Structure Without Overpaying?#

Set primary limits to the real downside of your client work, then add excess limits when your exposure can outgrow that first layer.

With the coverage boundary clear, you can choose structure with fewer assumptions. This turns e&o insurance for developers into an operating decision, not a guess based on headline premium.

Build your limit stack in the right order#

Use this sequence before you compare carriers:

| Decision item | How to apply it | Key differentiator |

|---|---|---|

| Primary Limits | Start with your largest single contract risk and client concentration. Primary cover responds first to covered loss, subject to deductible or retention mechanics. | It is your first working layer, so mistakes here create the biggest coverage gap. |

| Excess Limits | Add only when a serious claim could exhaust primary limits, or when contracts require higher liability capacity. | Excess layers respond after underlying limits are reached, so they are capacity tools, not default buys. |

| Escalation check | If governance exposure increases, including board or officer responsibilities, review whether broader Exec Risk alignment makes sense. | You avoid paying for complexity too early, but you still plan for growth triggers. |

Example scenario: you rely on one large retainer, ship a faulty release, and face a major client loss claim. A layered structure can protect you, but only if you sized primary limits first and added excess for a clear reason.

Tune cost and continuity without hidden tradeoffs#

| Term | What it means | Key differentiator |

|---|---|---|

| Deductible | What you pay before insurance starts paying, and larger deductibles usually reduce premium | Changes upfront cash pain, not just annual price |

| Retention | Insured-paid loss before policy response on forms that use it | Do not treat retention and deductible as interchangeable |

| Defense Costs | Language can place defense spending and damages within policy limits | Ask directly whether defense erodes available limits |

| Claims-Made Policy | Structure often requires coverage in force when the event happened and when the claim is made | Renewal continuity controls claim viability |

| Tail planning | Matters during carrier changes or shutdown planning, since some forms offer extended reporting periods | Transitions can break protection if you ignore timing |

Use this rule: set limits by exposure, tune cost levers second, and document continuity decisions every renewal.

The 5 Best E&O Policy Setups for Software Developers#

Start with the setup that matches your service model and claim pattern, then tune price. In practice, fit can matter more than headline premium when comparing e&o insurance for developers.

With structure in mind, map it to real buying options. Use this shortlist to compare errors and omissions and professional liability setups by practical usefulness for a software developer, not by brand hype.

This is a working operator list, not a universal market ranking. Confirm exact form language with your broker before binding.

| Setup | Best for | Brief description | Key differentiator | Pros | Watchouts |

|---|---|---|---|---|---|

| Lean freelancer setup | Solo consultants with small scoped projects | Uses a straightforward Claims-Made Policy, where coverage hinges on a claim first made during the active policy period | Keeps operations simple for a one-person delivery model | Simple structure to manage for solo work | Lower limits can leave less room in a larger client dispute |

| Agency growth setup | Small teams running multiple retainers | Keeps E&O language explicit for covered Third-Party Financial Loss allegations tied to errors, omissions, or negligence, which traditional liability may not address | Clearer boundary between professional-service allegations and generic liability language | Better clarity on the claim type the policy is designed to address | Coverage wording varies by carrier and form |

| Integration-heavy setup | API and systems integrators | Targets covered Third-Party Financial Loss allegations tied to errors, omissions, negligence, or downtime events | Aligns coverage intent to dependency-heavy delivery risk | Better fit for integration failure allegations | Claim outcomes still depend on policy language and case facts |

| Contract-heavy setup | Developers signing enterprise MSAs and procurement terms | Centers clause review, especially Consent-to-Settle Clause language that can require insurer approval flow through you before settlement | Gives you stronger control over high-stakes dispute decisions | Clearer settlement-approval expectations in disputed cases | Consent-to-settle wording is not identical across carriers/forms |

| Leadership-risk aware setup | Incorporated firms with investors or board exposure | Separates client delivery risk from leadership liability by coordinating E&O with Directors and Officers (D&O) Insurance | Draws a cleaner boundary between company service claims and director or officer wrongful-act exposure | Supports leadership-risk planning as the business matures | Requires coordination across separate policies and roles |

Example scenario: your studio signs a larger enterprise deal and adds board oversight in the same quarter. Keep the risk map clean by running E&O for delivery-related client financial-loss allegations. Then evaluate a separate D&O track for leadership wrongful-act allegations, instead of forcing one policy to do both jobs.

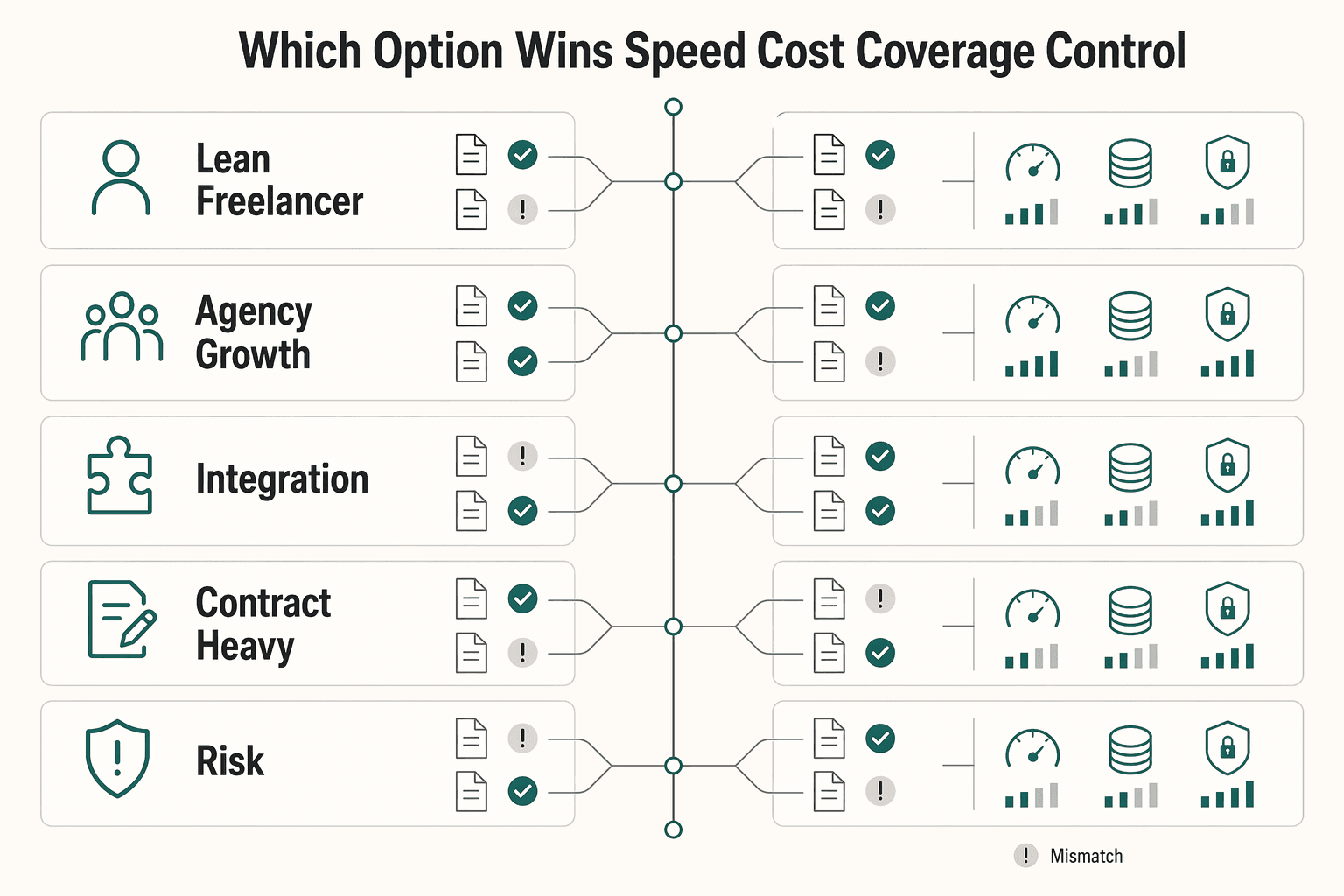

Which Option Wins on Speed Cost and Coverage Control#

Choose the option that protects your real client exposure first, then tune cost, because policy wording and limits can matter more than premium alone in E&O insurance for developers.

You now have five possible setups. This step helps you shortlist before you speak with retail insurance agents or insurance brokers. Use this matrix to compare errors and omissions options by operational fit, and force clear tradeoffs across Primary Limits, Excess Limits, and Retention.

| Setup | Best for | Coverage control | Cost pressure | Operational complexity | Verify before bind |

|---|---|---|---|---|---|

| Lean freelancer | Solo devs | Medium | Low to medium | Low | Defense Costs treatment, Retention funding timing |

| Agency growth | Small teams | Medium to high | Medium | Medium | Retroactive Date continuity, Retention funding timing |

| Integration-heavy | API/integration firms | High | Medium to high | Medium | Primary vs Excess attachment, follow-form endorsements/exclusions |

| Contract-heavy | Enterprise-facing devs | High | Medium to high | High | Primary Limits adequacy, narrowing endorsements/exclusions |

| Leadership-risk aware | Funded/incorporated firms | High | High | High | Defense Costs treatment, Retroactive Date continuity |

Read the winners correctly#

If you need speed and low admin load, the lean freelancer row can be a faster path to bind in some markets. If you need stronger control over claim outcomes, contract-heavy and integration-heavy setups usually score higher because they force deeper wording review. If you run a growing company with more internal stakeholders, leadership-risk aware can add process and cost.

Do not treat these ratings as universal facts. Carriers, endorsements, and exclusions can narrow what looks like broad protection. Use price as an input, not as your decision logic.

Verify before you bind#

Use this short script to cut false confidence:

- Confirm whether Defense Costs reduce available limits.

- Confirm the exact Retroactive Date and how renewals preserve continuity.

- Confirm how Retention works in cash-flow terms before policy response.

- Confirm whether excess layers follow form or introduce narrowing endorsements.

Example scenario: you run a small productized studio, add one large enterprise client, and sign tighter indemnity language. You might shortlist agency growth and contract-heavy. Then choose the one that gives clearer professional liability wording after verification.

Which Clauses Are Non-Negotiable Before You Bind?#

Lock Retroactive Date continuity, Prior Acts Coverage, consent mechanics, and defense-cost treatment before price, because these clauses decide whether your policy actually responds when a claim hits.

Once you have the right setup, the clause review decides whether your policy responds to real disputes. This matters most when errors and omissions exposure connects to prior client work. Use this red-flag checklist before you bind:

| Clause | What to confirm now | Key differentiator |

|---|---|---|

| Retroactive Date | Confirm the exact date and require the same date at renewal or carrier switch. | Claims-made forms only respond to acts on or after this date, so a mismatch can create an uninsured gap. |

| Prior Acts Coverage | Ask whether the form includes full prior acts or limits prior work through a retroactive date. | Some claims-made policies with no retroactive date provide full prior acts coverage. |

| Consent-to-Settle Clause | Require clear language on when the insurer needs your approval and what happens if you refuse settlement. | Some clauses add a hammer mechanism that can shift later damages or claims expense. |

| Defense Costs | Confirm whether defense sits inside limits or outside limits. | In defense-inside-limits structures, every dollar spent on defense reduces available settlement or judgment funds by one dollar. |

| Claims-Made obligations | Confirm reporting duties and timing triggers in writing. | Coverage usually requires the policy in force when the act occurred and when the claim or lawsuit gets filed. |

Retroactive-date risk is straightforward: insurers can limit coverage for wrongful acts before the retroactive date, and mismatches at renewal or carrier switch can create gaps. Treat Prior Acts Coverage and Retroactive Date as non-negotiable in professional liability review.

Questions to ask Insurance Brokers#

- "State the Retroactive Date you propose and confirm you will preserve it unchanged at renewal."

- "Does this policy grant full Prior Acts Coverage, or do you restrict prior work by date or endorsement?"

- "Show the exact Consent-to-Settle Clause wording and explain any hammer provision in plain language."

- "Do Defense Costs erode limits, and if yes, where will that pressure hit first in a live claim?"

- "List every claims-made reporting obligation that could block coverage if my team misses a step."

If you switch carriers after a heavy delivery cycle, one missed retroactive-date detail can leave yesterday's work outside today's policy response.

Run an Audit-Ready Buying Workflow Like a Business Operator#

Run a four-step buying workflow that maps real exposure, normalizes policy structure, preserves continuity, and records decisions for renewal discipline.

Clause review only helps if you can rerun it. This section turns your work into a system you can repeat each year. That way, e&o insurance for developers supports real client delivery risk instead of becoming a one-time paperwork exercise.

Four steps to run before bind and at every renewal#

| Step | What to do | Key differentiator |

|---|---|---|

| 1. Map your service catalog to claim patterns | List each service you sell, then tag likely Third-Party Financial Loss allegations such as inadequate work, negligent actions, or failure to deliver expected service levels. | You anchor errors and omissions decisions to actual client harm patterns, not generic coverage labels. |

| 2. Normalize comparable options | Gather comparable quotes, then align the same fields across each option: Deductible, Retention (SIR), Primary Limits, each-claim limit, aggregate limit, coinsurance terms, and exclusion wording. | You compare like for like. Deductible and SIR are not interchangeable, and structure changes can reduce real risk transfer. |

| 3. Lock continuity controls in writing | Document your Retroactive Date, prior acts position, claims reporting duties, and the owner for renewal tasks in one bind checklist. Start renewal prep at least three months before renewal. | Continuity breaks fast. A gap or a retroactive-date change can expose legacy work. |

| 4. Build an audit-ready record trail | Store submissions, quoted options, broker Q and A, endorsements, and bind decisions in one controlled folder, then run an annual review. Keep relevant E&O records as long as possible. | You create defensible operations for professional liability decisions and cleaner claims response when pressure hits. |

Example scenario: you expand from build-only work into ongoing integrations. Your workflow flags a higher financial-loss profile in Step 1. It forces tighter limit and retention comparison in Step 2. It also reduces the chance of a retroactive continuity miss in Step 3. That sequence protects downside better than premium-first shopping.

Choose a Safe Default Then Improve Annually#

Choose one fit-for-purpose policy setup now, verify it with your agent or broker, and run a yearly review cycle instead of waiting for perfect certainty.

You now have the framework, clause checks, and workflow. The move is simple: bind a defensible setup that matches your current delivery risk, then improve it as your business changes.

Use this safe default operating loop#

| Control | What to do now | Key differentiator |

|---|---|---|

| Fit first | Start with coverage aligned to your real service exposure and current delivery model. | You choose based on present risk, then refine as your work evolves. |

| Verify before bind | Speak with an agent or broker, confirm market availability for your profile, then compare terms and prices before you choose. | You reduce blind spots because independent agents can represent multiple insurers, and some programs run through retail agent or broker channels. |

| Improve annually | Put a recurring annual review on your calendar and update limits, exclusions, and workflow controls as your client mix changes. | Annual review is a strong default for financial stability, and it is especially important for small businesses that evolve quickly. |

This loop keeps your risk management grounded in how insurance actually works across jurisdictions. State-based frameworks differ, policy details can vary, and program access can vary. You protect yourself by rechecking assumptions each year.

Example scenario: you move from short project work to larger retainers with higher client dependency. Keep your current policy in force, run your annual review, and tighten key wording with your advisor. Then decide whether your limits and terms still fit the risk you are carrying.

Use this light-touch next step today:

- Pick one setup from your shortlist.

- Run the clause checklist and renewal controls.

- Ask your broker to confirm market-specific availability and final wording before bind.

If you want a freelancer baseline before that call, review Liability Insurance for Freelance IT Consultants: Do You Need It?.

Frequently Asked Questions

What is E&O insurance for software developers in plain English?

Errors and omissions insurance is specialized liability coverage for client claims that your professional work caused financial harm. For a software developer, that usually means disputes about negligence, advice, or delivery quality, not physical injury. Use e&o insurance for developers for service-performance risk.

Is E&O the same as professional liability insurance?

In most business insurance language, yes. Professional liability insurance and E&O usually describe the same coverage category. Still, confirm the exact policy wording, exclusions, and reporting duties before you treat two quotes as equivalent.

Does general liability cover coding mistakes or missed deliverables?

Usually no. General liability insurance focuses on physical risks like bodily injury or property damage. Coding errors, missed specs, and missed deliverables usually sit in professional liability territory.

What does E&O usually cover and exclude for freelance developers?

E&O often responds to allegations of negligent work, misrepresentation, or failure to deliver the expected service level. A missed deadline can still turn into a negligence claim, and technology professional liability can help with claim costs. Coverage still turns on exclusions and policy conditions, so review those lines closely with your broker.

How much E&O coverage should an independent developer buy?

No universal dollar amount fits every business. Set limits based on your contract obligations, client concentration, and the largest financial-loss scenario your work could trigger. Then stress-test your deductible, retention, and each-claim versus aggregate limits so your risk management plan matches your cash flow.

What is the difference between a claims-made policy and an occurrence policy?

A claims-made policy ties coverage to when the claim gets filed during the policy period. An occurrence policy ties coverage to when the incident happened, even if someone files later. This trigger difference affects how you handle renewals, reporting discipline, and continuity planning.

When should a developer business add D&O or Exec Risk coverage?

Consider Directors and Officers (D&O) Insurance when directors or officers could face personal liability from suits tied to their leadership role. D&O protects directors and officers from personal loss in those cases. It is a separate decision from E&O and does not replace coverage for client service errors.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- oregon.gov/das/Risk/Pages/InsTermlgy.aspxtrusted

- sba.gov/business-guide/launch-your-business/get-busi...trusted

- iii.org/publications/insuring-your-business-small-bu...external

- thehartford.com/professional-liability-insurance/errors-omis...external

- thehartford.com/professional-liability-insurance/errors-omis...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Liability Insurance for Freelance IT Consultants: Do You Need It?

**Treat your insurance decision like risk management, not online shopping.** As an independent IT consultant, you can face a negligence allegation, a client financial-loss claim, and legal defense costs even when you delivered in good faith. One bad dispute can drain time, focus, and cash before anyone proves fault. If you run solo, you are the CEO of a business-of-one, and risk decisions are part of the job.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.