Quick Answer

A digital will for online assets should be an operational handoff system, not just a list of accounts. Build it in one session by classifying accounts by risk, documenting access and authority for each one, assigning a trusted executor, and defining actions such as continue, transfer, archive, or close. Then maintain it on a quarterly cadence so payment and client workflows stay resilient.

Your cashflow is digital so your estate plan must be operational too#

Treat your digital assets and online accounts like a business continuity control, because losing access can stall operations when timing matters. Digital assets can include social accounts, messages, and cloud-stored documents, and even basic questions like "What will happen to your Facebook account when you die?" are not always operationally clear in the moment.

| Deliverable | What to capture |

|---|---|

| Critical accounts | List revenue-critical and security-critical accounts first, then legacy-only assets |

| Access location | Record where access lives, including your password manager and recovery paths |

| Decision-makers | Assign a primary and backup decision-maker for each action |

| Account handling | Define what each account needs on incapacity or death: continue, transfer (where supported), archive, or close |

| Review date | Set a review date so the system stays usable |

If you cannot reach billing, banking, client-portal, or other platform accounts, payments and client work can get delayed while people scramble to verify control. Build a reusable Digital Will system in one focused session, then keep it current with a maintenance rhythm you will actually follow.

As the CEO of a business-of-one, you need a handoff plan that keeps the work moving even when you are not available. This is not sentimental legacy planning. This is operator discipline for a business that runs through online accounts and tool-based workflows (including things like secure client portals and payment processing).

You are writing instructions a trusted person can execute under pressure, without guesswork, and without exposing sensitive data. Your Digital Will sits inside a broader Digital Estate Plan, which may pair legal documents with the operating steps across account types (details and authority can depend on jurisdiction and the accounts involved).

This is only getting harder as the volume of digital data grows. Synovus notes that in the two-year period from 2012 to 2014, humans produced more data than in all of human civilization before that. If you become unavailable at the wrong time, small access failures can stack fast: a client cannot confirm where to pay, communication breaks, and work pauses because nobody can verify account control. An operational handoff plan stops that chain reaction.

Build your first version in one session with five deliverables, then treat it like a system you maintain:

- List revenue-critical and security-critical accounts first, then legacy-only assets.

- Record where access lives, including your password manager and recovery paths.

- Assign a primary and backup decision-maker for each action.

- Define what each account needs on incapacity or death: continue, transfer (where supported), archive, or close.

- Set a review date so the system stays usable.

Use this trust standard for every step, so someone else can execute cleanly without creating risk:

| Standard | What you document | Why it protects operations |

|---|---|---|

| Traceable | Owner, account purpose, and last update | Your team can verify facts quickly during a handoff |

| Permissioned | Who can act, at what level, and in what order | You reduce overreach and avoid ad hoc access sharing |

| Safe for sensitive data | Retrieval procedure instead of raw secrets in documents | You keep credentials controlled while preserving continuity |

Do this well and you do not just store account notes. You build a repeatable system that protects operational continuity, preserves trust, and keeps your digital estate practical when timing matters most.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program. Want a quick next step for "digital will for online assets"? Try the free invoice generator.

Build the mental model before you touch a checklist#

Build a mental model before you build your checklist. Mental models are the internal representations you form from past experience and understanding, and they shape how you expect systems and interfaces to behave. Get the model right first, and your plan stays usable under pressure instead of turning into a pile of notes.

| Layer | What it covers |

|---|---|

| Instructions | what you want done |

| Authority | what validates the action (legal or otherwise, depending on the situation) |

| Access | how someone can actually get in (credentials, recovery flows, and handoffs) |

| Platform control | what the system will and will not let them do after they get in |

A good mental model reduces bad assumptions, especially because people tend to expect new systems to work like the ones they already know (Jakob's Law). So if your checklist depends on "someone else will be able to do X," make sure you are not relying on vague familiarity or wishful thinking.

One practical way to frame it is to separate the layers that often get mixed together:

- Instructions: what you want done.

- Authority: what validates the action (legal or otherwise, depending on the situation).

- Access: how someone can actually get in (credentials, recovery flows, and handoffs).

- Platform control: what the system will and will not let them do after they get in.

This distinction protects execution quality because you need to name the layer that matters for the action, not just the outcome you hope for.

As you build, use a simple decision rule and record it in plain language before you move to implementation:

- Assign one owner of record for each account.

- Assign one actor who executes the step.

- Assign one authority path that validates the action.

- Assign one platform action that completes the task.

- Record all four in plain language before you move to implementation.

Related: A Guide to Superannuation for Australian Freelancers.

Which assets are mission critical versus legacy only?#

Classify assets by operational impact first, because a digital will for online assets only works when your team knows what to protect in what order. With your model in place, turn it into triage. In one focused pass, decide what your Digital Will and Digital Estate Plan must keep accessible, what they must defend, and what can wait.

Digital assets can span financial accounts, investments, social profiles, photos, and cryptocurrency. When planning is missing, people can lose access to important accounts, face financial loss, and end up in disputes that could have been avoided. This is continuity across online accounts, not just legacy planning.

| Tier | Examples to consider placing here | Why this tier comes first | First action |

|---|---|---|---|

| Revenue-critical | Online banking accounts, cryptocurrency wallets | Losing access can disrupt time-sensitive financial actions and create immediate operational risk | Document who executes your payment and access-continuity steps immediately |

| Security-critical | Email accounts, domain names | A compromised account can be used to disrupt, disable, or maliciously control related systems and recovery paths | Lock down recovery paths and define incident actions |

| Legacy-only | Cloud storage services, social media accounts, personal archives | These matter, but they are often less time-sensitive than core access and security dependencies | Set archive, transfer, or memorialize instructions |

Do a quick sort now and keep it strict. Each account goes in one tier only, and you prioritize access and security dependencies before everything else:

- Put every account into one tier only.

- Mark the accounts that create immediate operational or financial risk if access is delayed, then mark security choke points.

- Record credential and recovery locations, including your password manager path.

- Assign one action per account: continue, transfer, archive, or close.

- Flag Reward Points and Loyalty Program Benefits for provider rule checks, since transfer rights can vary.

If you operate across regions, pair this with A Guide to Estate Planning for Digital Nomads. That helps your classification model and authority plan stay aligned.

What should your one-session digital will build include?#

Build your digital will for online assets as an execution pack, not a note dump, so someone you trust can act safely when you cannot. You already ranked accounts by mission impact. Now convert that ranking into instructions your executor can actually follow inside your broader digital estate process.

Start with an asset register. Digital assets can include online banking and investment accounts, crypto wallets, email and cloud accounts, and social profiles. Assume real access friction, including device access, security questions, and two-factor prompts.

One way to structure an asset register is to capture fields like these:

| Field | What to record | Why it matters |

|---|---|---|

| Platform | Provider and account type | Prevents account confusion during handoff |

| Owner | Who owns or controls the account | Clarifies responsibility and authority path |

| Credential location | Where access lives (in a secure location) | Speeds retrieval without exposing secrets |

| Recovery method | Backup email, device, or recovery steps | Helps handle lockouts and verification |

| Required action | What you want done if you are incapacitated or die | Removes guesswork under pressure |

Next, define action types per account. For Facebook, X (Twitter), and LinkedIn, state whether you want the profile memorialized or deleted, and include any handling notes that matter to your situation. Some assets may not be legally transferable, so include a fallback instruction if transfer or takeover is not possible.

Use a minimum implementation checklist that creates clear instructions, controlled access, and continuity for the workflows that keep revenue moving:

- Inventory all active online accounts.

- Assign account owner and backup contact (where applicable).

- Document the access path, including any device or email dependencies.

- Note two-factor and security-question dependencies.

- Define memorialize or delete choices for social profiles, plus any other account-specific handling instructions.

- Mark a review date and trigger events.

This is the core of practical legacy planning when your business runs on accounts: clear instructions, controlled access, and continuity for revenue-critical workflows.

Who should get access and what authority must be explicit?#

Give access only to a Digital Executor you trust to execute your plan, and define authority in writing before any emergency starts. Without planning, loved ones can be locked out of important accounts, so spell out who can act and what they're allowed to do.

| Filter | What to confirm |

|---|---|

| Trust | this person protects confidentiality and follows your instructions exactly |

| Technical competence | this person can handle account recovery, two-factor prompts, and your password manager process without shortcuts |

| Availability | this person can act quickly when client communication or cashflow routes break |

| Conflict screening | this person has no incentive to delay, block, or redirect outcomes |

Pick your Digital Executor using four practical filters, and be honest about whether they will still perform when things are messy:

- Trust: this person protects confidentiality and follows your instructions exactly.

- Technical competence: this person can handle account recovery, two-factor prompts, and your password manager process without shortcuts.

- Availability: this person can act quickly when client communication or cashflow routes break.

- Conflict screening: this person has no incentive to delay, block, or redirect outcomes.

Separate roles clearly. Your executor runs the operations. A Fiduciary holds legal authority where the law requires it. In some jurisdictions, that legal layer can shape what gets reviewed when someone requests access.

Ontario and Canada also treat digital assets as part of an estate, and you can address them in a will. Keep your digital estate language precise, then confirm local enforceability with counsel.

Run an access-and-transfer checkpoint for every critical account. Some digital assets may not be legally transferable, which can limit what anyone can do even when your estate documents name an authorized person. Document both the preferred action and the fallback action when access is denied. Safe default: align legal language, platform settings, and role permissions before you rely on any handoff plan.

| Account type | Suggested starting executor access (keep it tight) | Why this reduces unnecessary exposure | Fallback if blocked |

|---|---|---|---|

| Email Accounts | Start with recovery channels and billing communications, where possible | Limits exposure of sensitive personal content while keeping the lights on | Route client replies to a backup mailbox and preserve records |

| Cloud Storage Services | Limit access to continuity folders and client deliverables | Keeps personal archives out of scope | Share a pre-approved backup folder and log every action |

How do you hand off access without creating a security mess?#

Hand off access by making your executor's authority clear and your digital estate information organized, so your loved ones can act without guesswork or unnecessary privacy risk. Without a will, your property may not go to the people you want, and courts will usually decide who acts as your personal representative or executor, so don't leave this to chance.

Gaps create chaos. Aim to leave your digital footprint clear and unencumbered, both to save loved ones time and headaches and to protect their privacy. Without planning and oversight, digital assets can become hard to interpret and add stress right when people are already under pressure.

| Focus area | What to document now | Why it lowers risk |

|---|---|---|

| Authority | Who is authorized to act (your executor or personal representative) and what they're responsible for | Reduces confusion and prevents delays or improvising |

| Digital inventory | A clear list of key online accounts and digital assets you want handled | Keeps things from becoming undecipherable later |

| Where information lives | Where the executor can find the information they'll need to carry out your plan | Saves time and reduces avoidable headaches |

| Privacy boundaries | What should stay private, what should be shared, and what should be closed or removed | Helps protect your and your loved ones' privacy |

| Maintenance | A simple habit for keeping this information current when accounts change | Prevents stale info from creating extra stress |

Before you finalize, run a tight handoff checklist that forces clarity:

- Confirm you've named who can act, and that their authority is clear.

- Confirm you've listed the critical accounts and digital assets you want handled.

- Confirm your instructions are understandable enough that your executor won't have to guess.

- Confirm your privacy preferences are written down, not assumed.

- Confirm you revisit and update your digital estate information after account changes.

Where do rules vary and how do you confirm safely across jurisdictions?#

Treat your digital will for online assets as jurisdiction-specific legal operations, not a universal template. You have a secure handoff routine. Now confirm your legal language and account instructions hold up everywhere they need to. This is what turns a solid plan into a dependable system your Digital Executor can execute under pressure.

Rules vary, starting with will formalities. Many Wills Act regimes require testamentary instruments to be signed by the testator and by two witnesses. Some places recognize alternative will formats (for example, holographic wills in about half of American states, which must be in the testator's handwriting rather than attested), and some do not. Even where statutes do not expressly allow electronic wills, judicial approval may still be possible. Do not copy a template across markets and assume it will perform when tested.

Also avoid treating state names like shorthand for rules. If your plan references fiduciary access to digital assets concepts, review the rules that apply where you operate and where your estate will be handled. Then have counsel validate your fiduciary and executor language before you rely on it.

Run a four-step confirmation loop#

| Checkpoint | What you confirm | Why it protects continuity |

|---|---|---|

| Governing law | Your Digital Will and broader Digital Estate Plan point to the correct governing law | Prevents authority gaps when your executor acts |

| Provider Terms of Service | Each critical account category states current rules for transfer, closure, or memorialization (where available) | Stops bad assumptions about what platforms allow for online accounts |

| Local counsel review | Executor authority language matches local practice and court expectations | Reduces disputes when a fiduciary requests access |

| Policy-change trigger | You re-check after major platform policy updates | Keeps legacy planning operational as rules shift |

If you work across borders, pair this section with A Guide to Estate Planning for Digital Nomads. Coverage and enforceability vary by jurisdiction, so treat this as a recurring verification process, not a one-time setup.

Run a quarterly audit-ready review so the plan stays usable#

Run an audit-ready review on a fixed cadence so your digital asset management plan still works before it gets stress-tested. Now move from setup to operating rhythm. Your DAM program stays reliable only when you regularly audit your existing assets and workflows and keep governance, measurement, and optimization in the loop.

Treat auditing as a repeatable control, not a one-time project. Set a cadence, measure drift, and fix gaps quickly. (The idea of "audit cadence" shows up explicitly in digital-audit guidance, and Frontify frames DAM work as a six-step checklist that includes "Audit your existing assets and workflows" plus an ongoing "Govern, audit, measure, and optimize" step. Those pages also show update dates in 2025, which is a useful signal to revisit your own checklist.)

Define what "good" looks like and run the review queue#

| Review check for each critical area | What you're confirming | Evidence to log |

|---|---|---|

| Asset and workflow audit | Your inventory and the way work moves through it still match reality | What changed, what's missing, what's duplicated |

| Ownership and responsibility | Someone is accountable for the assets and the workflow, and that responsibility is documented | Owner notes and handoff notes |

| Governance controls | The rules you operate under are still the rules people follow | Current guidance and any exceptions |

| Measurement and optimization | You are not just governing, you are improving based on what you observe | Metrics or observations, plus the next fixes |

| Follow-up actions | Gaps have a clear next step and a clear person to do it | Action list with owners and dates |

On each cycle, run a repeatable queue so nothing quietly drifts out of scope:

- Audit existing assets and workflows across your priority areas.

- Review governance: what's enforced, what's optional, and what's being ignored in practice.

- Measure what changed since the last cycle, then capture the fixes you will run next.

Close every cycle with a short, plain-language update log. Record what changed, what still fails, who owns the fix, and what triggers an out-of-band review (for example, a new workflow, a reorg, or a tooling change).

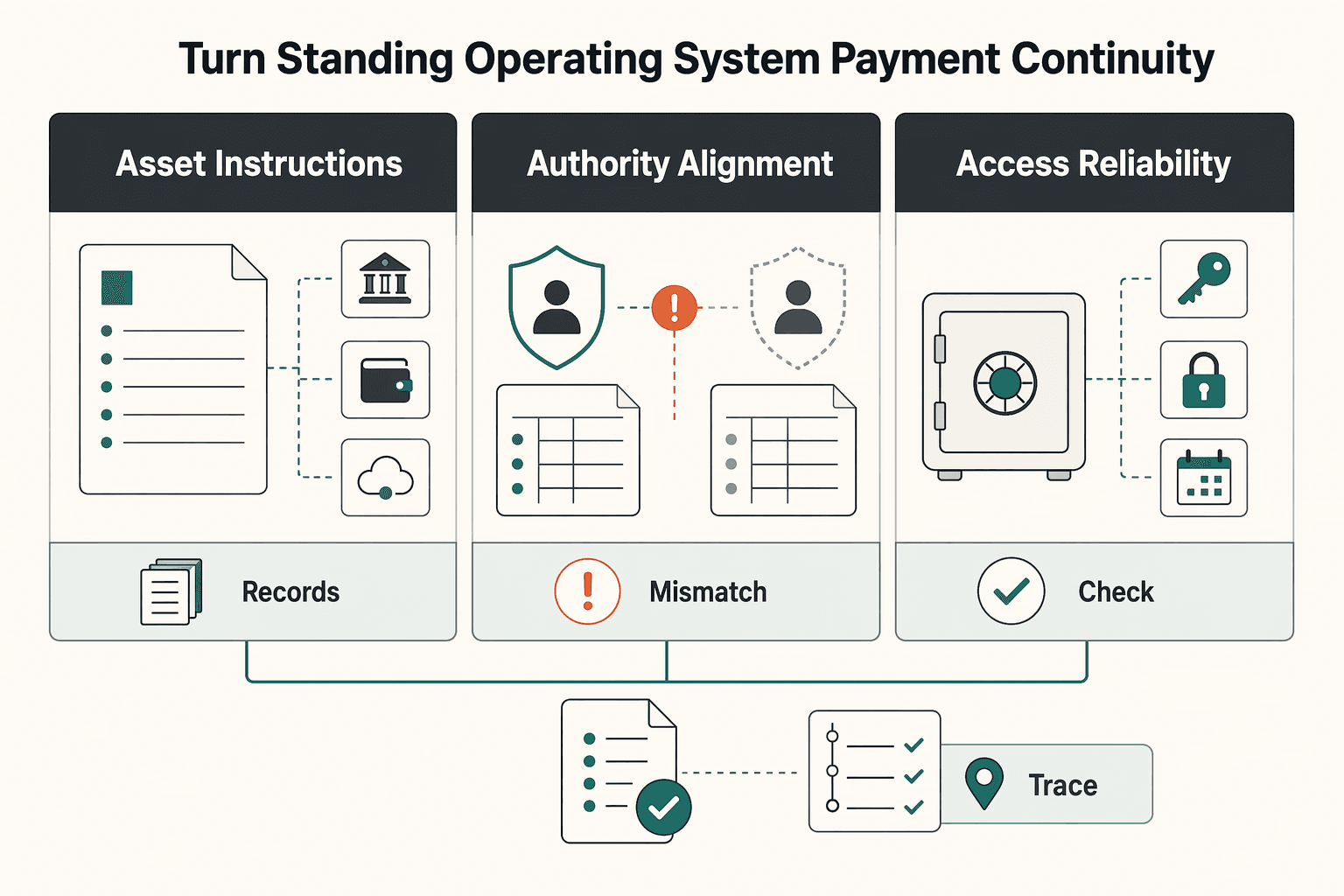

Turn this into your standing operating system for payment continuity#

A Digital Will should run like a system that protects cashflow, not a static document that only lists accounts. Turn the decisions above into one repeatable workflow. Keep your critical online accounts usable, keep authority clear, and keep actions traceable.

Treat your Digital Will as one control layer inside a broader digital estate plan. The will defines what should happen to each account. The estate plan is where you align legal authority and how the plan stays current. Your Digital Executor then runs a documented playbook instead of making judgment calls in real time.

| Control lane | What good looks like | Why it protects payment continuity |

|---|---|---|

| Asset instructions | Each priority account has owner, action, and recovery notes | Removes ambiguity when access issues interrupt billing workflows |

| Authority alignment | Legal review helps confirm your instructions fit the wider estate plan | Reduces delays when someone needs to act quickly |

| Access reliability | Recovery steps stay current in your access-management workflow | Prevents lockouts from freezing key online accounts |

Run this sequence now, then run it on your standing cadence:

- Classify assets by operational risk so you protect revenue and communication paths first.

- Assign decision authority and backup responsibility for every critical account.

- Secure access handoff with documented retrieval procedures and least-privilege controls.

- Confirm legal validity with counsel, and align wording with your broader plan.

- Review, test, and log changes so your executor can follow an up-to-date script.

Use an 80/20 rollout. Implement the highest-impact controls first, then expand coverage as your stack grows. No baseline checklist covers every provider or risk profile, so refine this system as your business changes.

Adopt the checklist, document policy gates and change logs, and request professional legal confirmation where jurisdiction rules differ. Then map your payment stack to this audit-ready routine and treat it as core operations, not admin cleanup.

Frequently Asked Questions

What should a digital will include for freelancers with client payments and online accounts?

It should include an inventory of critical online accounts and clear action instructions for incapacity or death. Add who should handle each account (where allowed), the authority path they must use, and where to find recovery info, including your password manager workflow. Without that, loved ones can get locked out of important accounts or information, which can lead to financial loss and avoidable disputes.

What is the difference between a digital will and a digital estate plan?

People often use “digital will” to mean the instruction layer for your online assets. A digital estate plan is the broader approach of including those assets in your estate planning so family and executors can manage them during estate administration. Think of the “digital will” as the execution page and the estate plan as the operating manual.

Who should be my digital executor and what permissions do they need?

Pick a Digital Executor who is trustworthy, process-driven under pressure, and realistically available when needed. Give only the access needed to complete the specific tasks you assign, and document it so they can act without guessing or overreaching.

How do Terms of Service affect heirs or fiduciary access to accounts?

Platform rules and account terms can shape what others can do after death or incapacity, and the access process is not the same across all providers. Some digital assets may also have transferability limits, depending on the applicable rules. Your job is to confirm what matters most for priority accounts and align your planning with what the provider will actually honor.

Are crypto wallets, online banking logins, domain names, and reward points handled the same way?

No. Different digital assets can come with different access controls and different transfer limits, and some may not be legally transferable at all. Do not assume one rule covers every asset class. Classify and document each type separately in your legacy planning workflow.

What is the minimum checklist to set this up in one afternoon?

Do one pass through your active accounts and sort them by revenue-critical, security-critical, and legacy-only. For each item, record owner, action type, authority path, and recovery location, then assign a backup contact. Finish with a short handoff note your executor can run without interpretation.

How often should I review and test my digital will system?

Set a recurring cadence and keep it consistent. Add trigger-based checks after major changes like platform policy updates, account ownership changes, or workflow updates. End each cycle with a short continuity drill and a dated update log so the plan stays usable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/sites/default/files/2023-12/ESF_SECURING_THE...trusted

- digitalpreservation.gov/multimedia/documents/ndiipp_appendix.pdftrusted

- nvlpubs.nist.gov/nistpubs/CSWP/NIST.CSWP.29.pdftrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12575626trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12575626trusted

- purduegloballawschool.edu/blog/news/digital-estate-planningtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.

A Guide to Superannuation for Australian Freelancers

**Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure.** As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.