Quick Answer

Inflation and interest rates affect freelancers most through slower cash collection, payment fees, and shrinking purchasing power, not just through headline pricing pressure. Track days-to-cash, payment rail, and fee leakage per client, then tighten deposits, milestone billing, payment terms, acceptance criteria, and billing cadence before changing rates. Raise prices with a documented review policy after timing and process risks are clear.

Inflation isn't "macro news" - it's a hidden pay cut unless you run a cashflow playbook#

Treat delayed cash collection and payment fees as measurable cost centers, then reduce them with terms, billing cadence, and payment-rail choices. If you are the CEO of a business-of-one, cash collection is not admin. It is your core system. The real damage often shows up in the gap between delivery and settlement, plus the fees and friction that quietly reduce what you actually keep.

The receivables lag you can control (even on Net Terms)#

When you deliver work today and wait on Net Terms (Net 30/45/60), you create a receivables lag. These are days where you already did the work, but you cannot redeploy the cash.

You do not need a macro forecast to manage this. You need a tracking habit. Add these columns to your invoice tracker:

- Invoice issued date

- Paid date (when funds land)

- Days-to-cash

- Payment rail (card, bank transfer)

- Friction notes (PO missing, approver changed, "resend invoice" loop)

Do this for every client. Patterns show up fast: who says "Net 30" but pays later, and where preventable process slop keeps you waiting.

Stop treating late payment as an annoyance. Treat it as operational risk you can reduce.

Your 30-minute, risk-first system (pricing triggers, controls, rails)#

Most advice ends at "raise your rates." That helps, but it is incomplete. You also need to tighten the system that protects your earnings after you send the invoice:

| Lever | What it covers |

|---|---|

| Pricing triggers | Review when scope expands, renewals approach, or payment behavior degrades |

| Contract controls | Define acceptance criteria, sign-off steps, and "pause work on overdue balances" language |

| Invoicing cadence | Invoice at milestones, not only at the end |

| Payment rails | Pick the rail that matches the situation |

Stripe explicitly positions its Standard plan as pay as you go: "Access a complete payments platform with simple, pay-as-you-go pricing. No setup fees, monthly fees, or hidden fees." That helps you start fast, but you still have to manage fee leakage.

| Payment rail | Known processing fees (examples) | What to confirm |

|---|---|---|

| Stripe card payment (Standard) | 2.9% + 30¢ per successful transaction for domestic cards. Extra fees can apply (for example: +1.5% international cards, +1% if currency conversion is required, +0.5% manually entered cards). | Which fees apply to your customers and checkout flow. |

| Stripe Instant Bank Payments | 2.6% + 30¢ per successful transaction (as listed by Stripe). | Availability and how you will reconcile payments to invoices. |

| Bank transfer (outside Stripe) | Fees and timing vary. | Confirm fees and timing before you promise terms. |

Hypothetical: a new client insists on Net 60 and wants to pay by card. You can keep the headline rate, but tighten milestones, collect a deposit, and document acceptance. That way you keep the amount outstanding smaller while you deliver.

If you need help selecting Stripe setups for a non-US business, use this: How to Open a Stripe Account for a Non-US Business.

Your mental model: terms first, price second (define the variables before you change anything)#

Lock the terms and cash-collection mechanics first, then adjust price with clean data instead of vibes. Once you treat receivables lag as a cost center, you can turn inflation pressure into controllable operating levers. Start by defining the variables before you negotiate anything.

Start with definitions that affect real work (not headlines)#

Inflation is the gradual rise in the cost of goods and services, which means your money buys less over time. Cash Flow Frog puts it plainly: "Inflation is the gradual rise in the cost of goods and services, meaning your money doesn't go as far as it used to." For a freelancer, that shows up as shrinking purchasing power between project start, invoice, and payment. The same invoice can cover fewer necessities later.

Interest rates are part of the broader market context you and your clients operate in, but the "why" and "what happens next" varies. Instead of debating what rates "should" do, focus on the parts you can control: your process, your policies, and how consistently you enforce them.

Build your cashflow model with three dials you control#

Think in dials, not slogans. You will make better decisions faster.

| Dial | What you define | What "good" looks like | Your safe default move |

|---|---|---|---|

| Price | Rate card, scope boundaries, renewal language | Price matches current costs and effort | Review rates on a schedule and at renewal |

| Timing | When you bill, how you follow up, and what "done" means | Shorter time between delivery and cash | Reduce ambiguity and tighten your follow-up loop |

| Risk | Your payment process plus enforcement and documentation habits | Fewer disputes and fewer surprises | Get approvals in writing and keep clean records |

Operational rule: treat timing as a leading indicator and price as a lagging indicator. If cash arrives late, fix the workflow before you "solve" it with a bigger number.

A useful gut-check comes from 6 Figure Creative: "If you're not tracking these seven key metrics in your business, you're leaving money on the table." You do not need their full list to act. Track a small set of metrics that tell you how fast cash turns over and where delivery gets messy.

Hypothetical: a client asks for a lower rate "because budgets tightened." Respond like an operator. Keep your rate card stable, clarify scope and sign-off, and set a clear internal trigger for when late payment changes how you proceed next time. That protects cashflow first, then preserves pricing power.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

How do inflation and interest rates actually hit your invoices (not just your budget)?#

They hit your invoices through two mechanics you can measure: time-to-cash and fee drag. If you can track what happens between "sent" and "settled," you can manage the impact without arguing about headlines.

1) Quantify the "waiting cost" hiding inside Net Terms#

Stop treating Net Terms as a contract detail and start treating them as an operational KPI.

Make this non-negotiable in your tracker:

- Invoice issued date

- Paid date (the date funds land, not the date the client "processed" it)

Then segment the same data two ways:

- By client: get true average days-to-cash per account (not just an overall average).

- By payment rail: label payments like "Stripe card," "bank transfer," "cross-border transfer," and "other."

Even without doing finance math, this shows where cash timing becomes operational. Longer gaps mean you carry costs longer. Short gaps mean you operate with less stress.

Hypothetical: a "great" client pays every invoice, but your tracker shows they pay later than everyone else and only via a rail with higher fees. Do not argue about rate first. Tighten timing and rail choices first, then revisit pricing.

2) Identify leakage competitors ignore (fees)#

Two leaks eat invoice value: fees you can price in and fees you can reduce by choosing the right rail. Use a quick comparison table as your default audit:

| Leakage type | Where it shows up | What to track (per invoice) |

|---|---|---|

| Card and method fees | Processors charge per successful payment. Stripe standard domestic card is 2.9% + 30¢ per successful transaction. Stripe also adds 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. | Gross invoice, fee amount, net received, method used |

| FX and currency conversion | International payments can stack card and conversion add-ons (including currency conversion when required). | Invoice currency, settlement currency, conversion notes, net received |

| Payout fees (platform payouts) | If you pay out to other accounts via Stripe Connect ("You handle pricing"), Stripe charges $2 per monthly active account (active in any month payouts are sent) and 0.25% + 25¢ per payout sent. | Accounts paid out, payout count, payout fees, net sent |

Operational move: shorten the gap between work and cash by tightening timing expectations and nudging clients toward lower-fee rails before you touch your rate card.

If Stripe sits in your stack and you operate outside the US, keep your setup clean so fee and currency choices stay deliberate: How to Open a Stripe Account for a Non-US Business.

Want a quick next step? Try the free invoice generator.

Diagnose your exposure in 30 minutes: the 3-part freelancer risk score (rate, timing, and client behavior)#

Build a one-page scorecard per client across rate, timing, and behavior, then tighten the right control first (price, terms, or workflow). Once you have days-to-cash and payment-method behavior in one place, you can stop treating inflation like background noise and start managing it client by client.

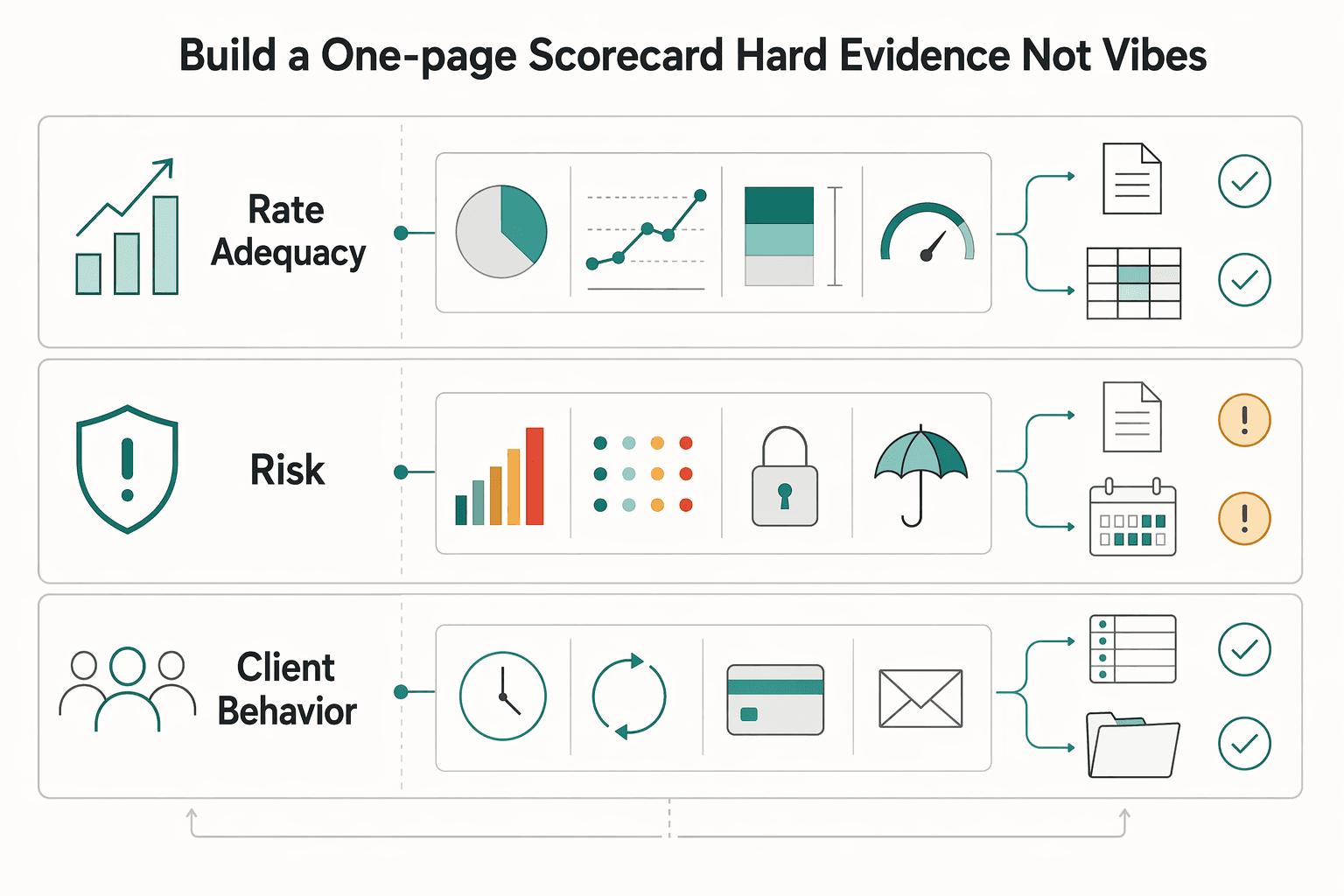

Build a one-page scorecard (hard evidence, not vibes)#

Open a sheet, list your active clients, and fill one row per client. Keep it boring and factual. You do not need a perfect scoring formula. You need consistent inputs you can compare.

| Risk area | What you record (per client) | Evidence to pull (fast) | What "good" looks like (your definition) |

|---|---|---|---|

| Rate adequacy | Last rate review date, current rate, margin notes | Your proposal/SOW, last increase email, current scope notes | You can explain why today's rate still fits today's cost reality (inflation, tools, subcontractors) without guessing a universal % |

| Timing risk | Stated payment terms, actual days-to-cash, late frequency | Invoice issued date vs paid date from your tracker | Actual payment behavior matches what the contract says, with minimal chasing |

| Client behavior | Change-request pattern, acceptance clarity, payment method exposure | Your change logs, approval emails, payment method used | Clear "done" criteria and a payment path you can reconcile without surprises |

For payment method exposure, track the economics you can verify. If a client pays by card via Stripe, Stripe's standard pricing lists 2.9% + 30¢ per successful domestic card transaction, with additional fees shown for cases like 0.5% (manually entered cards), 1.5% (international cards), and 1% (currency conversion when required). That is not a moral judgment. It is planning.

Hypothetical: you review a client and realize the rate feels fine, but the scope changes weekly and nobody signs off. Do not lead with "rate increase." Lead with acceptance criteria and milestone checkpoints.

Turn the scorecard into actions (controls, not drama)#

Attach one default action to each risk area so you move fast:

- If rate adequacy looks weak, schedule a rate review tied to scope options (keep scope, adjust rate, or reduce scope).

- If timing risk looks weak, tighten billing cadence (more frequent invoicing) and consider Milestone Billing or Advance Deposits for new work.

- If behavior looks weak, require written acceptance criteria, keep a delivery log, and standardize change requests before you expand scope.

Also capture friction points you personally observe in how invoices get approved and paid. Treat each one like a system bug. Write the fix into your invoice checklist so the process is easier to follow and reconcile.

Should you raise rates, tighten terms, or change billing cadence first? (use this decision tree)#

When budgets tighten, start by adjusting cadence and payment timing so the work stays sustainable, then revisit price. You do not need more debate. You need a default move per situation that you can enforce cleanly.

The decision rule: address timing and cadence when timing causes the pain#

Use what your invoices already show you: when cash actually arrives, and whether clients are asking to space out work. If money shows up late, a rate increase can still leave you feeling broke because the constraint is timing, not pricing. If money shows up on schedule but your costs climbed, pricing (or scope) is usually the cleaner lever.

Here's a practical decision tree you can run client by client:

| Situation you observe | Your first move | Your "operator" implementation detail |

|---|---|---|

| Stable client, pays late | Tighten payment expectations and billing cadence | Put the updated expectations in writing before the next cycle. Invoice on a schedule you can actually follow. |

| Stable client, pays on time, margins shrinking | Adjust rate or re-scope | Offer two options: keep scope at a new rate, or keep price by reducing scope. |

| Client signals budget pressure | Offer a lighter cadence instead of forcing the same frequency | Make the new cadence explicit (what changes, what stays, and when you revisit). |

Hypothetical: a "great" client pays reliably, just late. Stop trying to win with a bigger invoice. Tighten the workflow: scheduled invoices and clear due dates.

Avoid the competitor trap: bigger invoices with the same delays#

Rate increases help, but they can also amplify friction if you leave timing unchanged. A higher invoice with the same delays raises the stakes of every follow-up.

Watch real-world cadence shifts in client behavior. A Money Nuts & Bolts podcast host described budget pressure showing up as cadence changes, with some people moving from weekly sessions (cited as about $800 a month) to every other week. The same pattern can show up in your business: when clients tighten their cash flow, consider mirroring the operator move by adjusting cadence and payment timing, then pushing price only where it actually fixes the constraint.

How to adjust your rates during inflation (without making up a random percentage)#

Adjust rates using a documented review trigger plus a consistent "options" message, and let payment timing and fees (not vibes) set the floor. Once you know whether timing, price, or process friction is causing the pain, you can update price without guessing.

Build a rate-review policy you can repeat (and defend)#

Pick two triggers and treat them like systems, not moods:

- Calendar trigger: choose a review cadence you will actually follow. You do not need a perfect interval. You need a consistent one.

- Contract trigger: run a review at renewal, any scope increase, or expanded deliverables.

In each client file, keep a one-page "rate decision record" next to Net Terms and payment history:

- Last rate change date

- Current scope and what changed (tools, subcontractors, turnaround expectations)

- Actual days-to-cash vs stated terms

- Payment method and direct costs you pay to collect

This ties a rate change to operating reality, not a headline.

Communicate increases like an operator (date, reason, options)#

Send a simple notice that includes (1) effective date, (2) reason tied to cost and scope reality, (3) two paths:

- Option A: keep scope, move to the new rate.

- Option B: keep the old rate, reduce scope into a smaller package.

For existing clients, earn goodwill with operational improvements you control: clearer milestones, tighter invoicing, faster turnaround, fewer revision loops. You stop sounding like a negotiator and start sounding like someone who runs a clean process.

Use different defaults for different risk profiles:

| Client type | Price move | Terms move |

|---|---|---|

| Existing, pays on time | Smaller, predictable adjustments | Keep terms stable, tighten only if timing slips |

| New or late-pay pattern | Rate may stay similar | Add Advance Deposits and Milestone Billing early |

Hypothetical: a client wants "the same deliverables" but adds extra review rounds and slower approvals. Offer the new rate starting next cycle, or reduce rounds and lock milestones so both sides stop bleeding time.

Finally, account for method effects. Stripe describes Standard pricing as pay-as-you-go with "No setup fees, monthly fees, or hidden fees," but you still pay per-transaction fees. For example, Stripe lists 2.9% + 30¢ per successful transaction for domestic cards, and notes additional fees like 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. Price so collection costs do not silently erase your margin, and tighten acceptance criteria so payment expectations are clear across any rail.

If you need help setting up Stripe outside the US, use How to Open a Stripe Account for a Non-US Business.

When procurement or industry rules constrain pricing mechanics (like automatic escalators), ask the client for their policy and confirm what your contract jurisdiction allows before you promise anything.

What payment-term safeguards protect cashflow when inflation is high?#

Treat payment terms as your cashflow firewall: tighten time-to-cash with deposits, shorter payment terms, and clear invoicing rules before you rely on another rate increase. A new rate does not help if it lands late. Collection mechanics are where inflation can hurt most.

Set safer default terms (timing beats opinions)#

Inflation means prices rise over time, so buying power shrinks. When your client pays late, your invoice effectively buys less when it arrives. That is economic basics, not drama.

| Term move | How it is described |

|---|---|

| Advance deposit | Collect a portion upfront to cover startup costs and protect your calendar |

| Shorter payment terms (by default) | Shorten your standard terms compared to what you used historically, then offer longer terms only after a client proves reliability |

| More frequent billing (when it fits the work) | Invoice as work is delivered instead of waiting until the very end, so cashflow is less back-loaded |

Build your default terms to reduce waiting time and stabilize income. As Giggle Finance puts it, "Asking for deposits and shorter payment terms reduces waiting time and creates a more stable monthly income." In practice, that looks like:

- Advance deposit: collect a portion upfront to cover startup costs and protect your calendar.

- Shorter payment terms (by default): shorten your standard terms compared to what you used historically, then offer longer terms only after a client proves reliability.

- More frequent billing (when it fits the work): invoice as work is delivered instead of waiting until the very end, so cashflow is less back-loaded.

Hypothetical: a client insists they "only do Net Terms" but they also require multiple stakeholders to approve work. Keep the rate, but break delivery into smaller, clearly defined steps and invoice as each step is accepted, so you are not waiting on one giant approval bottleneck.

Put enforcement and invoicing into a workflow (not a debate)#

Write your contract in plain language, then back it up operationally:

- Late charges: consider a late-fee clause only where your jurisdiction allows it, and treat it as a boundary setter, not your main plan.

- Overdue handling: if you want consequences for overdue invoices, define them clearly and confirm the approach with local counsel for your contract and client type (rules and enforceability vary).

- Invoice workflow that prevents "AP ping-pong":

- Invoice immediately when a deliverable (or agreed step) completes. * Include the billing contact, PO number (if required), and payment instructions every time. * Send an "invoice pack" attachment bundle: relevant SOW excerpt, written sign-off (if you use it), and the invoice.

Finally, run an escalation ladder based on missed commitments (not arbitrary dates). Start with a reminder and re-send. Then confirm payment method and AP status. If it continues, move to whatever formal notice and next steps your agreement supports, and consider outside help if needed.

Long payment terms plus repeated delays signals client quality. Inflation does not create bad clients. It reveals them.

Cross-border invoices and FX: how to stop losing money between currencies, rails, and holds#

Treat currency and payment rail as part of your pricing system, because cross-border mechanics change what you keep after fees. Once terms are tighter, protect the "between" layer: conversion, processing fees, and operational friction that quietly taxes what you keep.

Make currency a deliberate choice (and document it)#

Cross-Border Invoice is any invoice where client payment and your operating costs may sit in different countries or currencies. Pick the invoice currency per client, then lock it into the SOW and every invoice header so nobody renegotiates midstream.

Use this safe default decision rule:

- If you pay expenses in your home currency, invoice in that currency unless the client's procurement requires otherwise.

- If the client insists on paying in their currency, treat FX as a line item you manage (timing, conversion method, and fee visibility). Do not "hope it nets out."

Hypothetical: you work locally, but a client pays you in a foreign currency. Your headline rate stays the same, but the amount you retain changes when conversion happens. Solve it by (1) choosing one invoice currency, (2) stating who pays conversion costs, and (3) reconciling every deposit against the invoice total.

Choose rails based on fee visibility and reconciliation (not vibes)#

Stripe gives you published pricing for card rails, which makes fee leakage easier to model:

- Stripe Standard pricing: "No setup fees, monthly fees, or hidden fees."

- Domestic cards: 2.9% + 30¢ per successful transaction.

- Additional fees: + 1.5% for international cards, + 1% if currency conversion is required, and + 0.5% for manually entered cards.

Compare rails like an operator:

| Decision factor | Card (Stripe) | Bank transfer |

|---|---|---|

| Fee transparency | Published fees (including international and conversion add-ons) | Varies by bank and corridor, confirm in advance |

| Reconciliation workload | Strong if you standardize invoice IDs and receipts | Can increase if references arrive inconsistent |

| Dispute readiness | Keep proof-of-delivery and signed milestones for any rail | Keep the same documentation discipline |

Operational checklist (copy/paste):

- Write "Invoice currency" and "Accepted payment methods" into the SOW.

- Track gross invoice, fees, and net received per payment (your investment strategy starts with knowing net).

- For Stripe, decide up front who absorbs international and conversion fees, then price accordingly.

- Confirm account and onboarding constraints before promising a method to an overseas client (use: How to Open a Stripe Account for a Non-US Business).

Your monthly operating loop + the "get paid" checklist (copy/paste into your process)#

Build a monthly cash-collection loop that spots leakage early and forces consistent actions. This is where your playbook becomes repeatable: one review, a few triggers, and a checklist you actually use.

The monthly review: one report, two leaks, one decision#

Start with your invoices and payment dates: pull issued date vs paid date and group by client, stated Net Terms, and payment method (card processor vs transfer). Then identify your top two leak sources:

- FX costs on Cross-Border Invoices: you cannot manage what you do not log. Track each conversion's timing and settlement amounts so you can explain variance later and choose better defaults next month.

- Late payers creating cash gaps: separate "slow rail" from "slow client." If a transfer method is slow to reconcile, fix the process. If a client pays late, change the terms.

Use a simple grouping table so the decision stays objective:

| What to group by | What you look for | What you change next |

|---|---|---|

| Net Terms | Clients who pay later than their terms | Tighten terms, add deposits, change billing cadence |

| Payment method | Rails that increase delays or disputes | Switch rails, improve invoice references, add documentation |

| Cross-border vs local | Patterns in FX variance | Standardize invoice currency and conversion timing |

Hypothetical: a solid client pays and suddenly disputes a deliverable. Do not argue about intent. Check your acceptance criteria, your proof-of-delivery, and your milestone sign-off trail, then tighten the workflow for the next milestone.

Hard triggers (so you do not renegotiate emotionally)#

Write triggers into your internal policy and apply them consistently:

| Trigger | Default response |

|---|---|

| Client pays late repeatedly | Move them to Advance Deposits + Milestone Billing for future work, or shorten Net Terms |

| Client disputes deliverables | Tighten acceptance criteria, require written approvals at each milestone, and store proof-of-delivery |

| Same payment method keeps slowing things down | Consider switching rails and tightening your invoicing details so payments reconcile cleanly |

Keep your files audit-ready. Store SOW, milestone approvals, invoice PDFs, and delivery evidence together. Also define time windows clearly in your own docs. For example, one contract defines calendar days as any day on the calendar (including weekends and holidays), while business days exclude Saturdays, Sundays, and State of Oregon recognized holidays.

What should I do first this month? (copy/paste)

- Review top 5 clients by revenue and slowest days-to-cash.

- Tighten Net Terms on any client with repeat delays.

- Add Advance Deposits + Milestone Billing to new contracts by default.

- Update your rate card when your scope, costs, or positioning changes (add an effective date and scope options).

- Choose an FX and collection method for every Cross-Border Invoice.

The bottom line: protect purchasing power by shrinking time-to-cash and locking in clean terms#

Inflation can raise the cost of supplies, rent, and services, shrinking purchasing power and profit margins if your revenue does not rise accordingly. Treat it like a system: track CPI-driven cost pressure, then adjust pricing, budgeting, and vendor relationships on a schedule instead of reacting emotionally.

Inflation means prices for goods and services rise across the board and keep rising over time. The U.S. government measures inflation using the Consumer Price Index (CPI), which tracks prices of common items people buy (like food, gas, and clothing). Simply Business also notes the Fed has been raising interest rates to cool the economy.

Your inflation system (diagnose, control, review)#

Treat this as a monthly 30-minute financial planning block:

| Step | What you look at | What you decide | Output you document |

|---|---|---|---|

| Diagnose exposure | Costs that moved (tools, rent, contractors), invoice aging, client friction | Which lever matters most (price, timing, behavior) | A 1-page client note: terms, pay history, scope risk |

| Apply controls | Rate card, budget cuts, vendor renegotiations | What changes now vs at renewal | Updated rate card, updated budget, vendor plan |

| Operationalize | Review cadence + triggers | "If X, do Y" rules | A checklist you reuse every month |

One useful reality check: Nav reports that more than 70% of small business owners think prices will continue to rise. If you wait for "certainty," you will wait forever.

Practical term hygiene (clean terms, clean proof, fewer surprises)#

These are common contract and invoicing moves, but the excerpts above do not support claims that any of them reliably "protect purchasing power" during inflation or reduce dispute/chargeback/hold risk. Use them as general term hygiene, then evaluate what actually works for your clients.

- Shorten payment terms where appropriate, especially for new or inconsistent payers. Put the actual due date on the invoice.

- Use advance deposits and milestone billing when it fits the project and relationship. Treat it as clarity and risk allocation.

- Document acceptance in writing (email counts). Tie each invoice to a named deliverable and a clear sign-off moment so expectations are explicit.

If you work cross-border, be explicit up front about currency and payment method, and confirm what your bank, processor, or platform supports in your country and your client's country before you promise a method.

Hypothetical: you notice a client pays reliably but approvals drag. Keep the rate steady for now, tighten the billing cadence, and require written acceptance at each milestone so your cash planning stops hinging on one internal stakeholder.

If you want to evaluate tooling for collections and payouts, you can review platforms like Gruv (Virtual Accounts, Payouts, MoR workflows) and confirm availability for your market and client base before you standardize your process.

Frequently Asked Questions

How should freelancers adjust rates over time?

Use a repeatable rate-review policy instead of changing prices on instinct. Review costs, scope, payment timing, and collection costs on a consistent cadence and at renewal or scope increases. Then set an effective date and offer either the same scope at the new rate or reduced scope at the old rate.

How much can I raise rates with existing clients?

There is no universal percentage. The ceiling depends on your contract, renewal window, scope, timelines, and payment terms. Frame the conversation as a choice between updated pricing for the same scope or a smaller scope at the current rate.

What matters more than raising rates right away?

Protecting net revenue and reducing leakage matters first. Track what you actually keep per invoice after payment fees and delays. If timing is the real problem, fix terms, cadence, or workflow before relying on a bigger headline rate.

How do payment gateway fees affect cashflow?

They reduce the net amount that reaches your bank on each successful payment. Over time, those per-transaction charges can materially change your effective take-home. Track gross invoice, fee amount, method used, and net received per invoice.

Should I change payment terms or billing structure first?

Start with the lever that matches the bottleneck. If cash arrives late, tighten payment terms and invoicing cadence. If work runs over a long timeline, use smaller billable checkpoints so delivery and cash stay aligned.

What Stripe fees should freelancers know about (cards, international, and Connect)?

Stripe's Standard pricing is pay-as-you-go, but per-transaction fees still apply. The article lists 2.9% + 30 cents for successful domestic card transactions, plus 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. For Stripe Connect when you handle pricing, it lists $2 per monthly active account and 0.25% + 25 cents per payout sent.

What should freelancers do first this month to protect cashflow?

Review invoice aging by client and payment method first. Confirm payment rail costs and your real net per invoice, then tighten terms or add advance deposits and milestone billing where delays repeat. For cross-border work, choose an FX and collection method for each invoice and keep approvals, invoices, and delivery evidence together.

Try a related tool

Yuki writes about banking setups, FX strategy, and payment rails for global freelancers—reducing fees while keeping compliance and cashflow predictable.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

How to Open a Stripe Account for a Non-US Business

**Treat your Stripe setup as a system for cashflow, not a quick signup, so your first payouts are more predictable.** If you run a small business, this is one of those setup decisions where "close enough" gets expensive later. If you are a nonresident operator, the pain usually shows up in a few places: payout delays, avoidable verification loops, and uncertainty about which path actually fits your business. If you guess early, you usually create rework later, especially when invoices are already waiting.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.