Quick Answer

Map your taxpayer facts before claiming relief. In a us-uk tax treaty freelancer case, confirm whether Article 4 is even needed, check Article 5 before leaning on Article 7, and match payer paperwork to income type by using Form W-8BEN for non-personal-services income or Form 8233 for personal-services income. Keep domestic filing duties active, then run a final consistency check so treaty notes, return drafts, and payor records do not conflict.

How the US-UK tax treaty applies to freelancers#

Start with your facts and filing setup before you interpret the treaty. For freelancers and consultants with US and UK income exposure, one common risk is assuming the treaty will sort everything out before your residency position, filing obligations, account status, and records are clear.

This guide follows a practical sequence. First map your situation. Then read the US-UK Tax Treaty against those facts. Then handle filing and documentation in the right order. The goal is simple: avoid filing mistakes, avoid missed filings, and know when to escalate to a qualified tax professional.

Use official documents first. The IRS United Kingdom treaty documents page provides treaty materials in PDF form. The source page used here shows a last reviewed or updated date of 12-Aug-2025. If you plan to rely on a clause later, verify it in that official treaty package first.

On the UK side, lock down Self Assessment basics early:

- HMRC says you must tell it by 5 October 2025 if you need to complete a return for the previous tax year (6 April 2024 to 5 April 2025), and late notification can lead to penalties.

- If you are a sole trader, you register by registering for Self Assessment; the cited trigger is earning more than £1,000 in a tax year (6 April to 5 April).

- If you are filing online for the first time, you must register before using the service, and you need your UTR to sign in and file.

- HMRC says your return may be delayed if you file without reactivating an existing account.

- Not everyone can use the standard online filing service in the same way, including some people who lived abroad as non-residents.

Treat this setup as risk control, not admin overhead. Keep the treaty PDFs you rely on, registration confirmations, your UTR details, and records such as bank statements and receipts so your filing position is supportable.

If your facts are mixed, pause early and document before you file. Dual-country ties, prior non-resident periods, and uncertainty about filing route can all be signs to slow down before making treaty-position decisions. For related context, see A Freelancer's Guide to the US-Canada Tax Treaty.

Start with your taxpayer profile before you touch the treaty#

Start with a one-page fact sheet, not treaty articles. Your treaty position only becomes usable after you pin down your status and payment flow.

Classify the facts that drive the answer#

Document the basics first: your taxpayer status, your claimed treaty-country residence, whether the income is from personal services, and who the payor is. Do not interpret treaty articles yet. Build a clean fact pattern you can keep consistent across payer documentation and tax filings. If those answers change by client, tax year, or payment stream, stop and sort that out before making treaty claims.

Record the payer path, not just the client name#

Who actually pays you matters because treaty withholding claims run through the payor, the withholding agent. Record whether payment comes from a direct US client, an agency, or a platform, and capture the legal name of the entity remitting funds.

Do not submit forms on autopilot. For income not earned from personal services, the relevant treaty withholding form is Form W-8BEN. For income earned from personal services, the form is Form 8233.

Build a one-page evidence sheet#

Keep it short and update it before each filing cycle. At minimum, include:

| Evidence item | Detail |

|---|---|

| Taxpayer status and treaty-country residence | Record your taxpayer status and claimed treaty-country residence |

| Payer legal name and role | Record whether payment comes from a direct US client, an agency, or a platform, and capture the legal name of the entity remitting funds |

| Form requested or provided | Form W-8BEN or Form 8233 |

| TIN status | Reduced treaty withholding on W-8BEN or W-8BEN-E generally requires a US or foreign TIN, with a limited exception |

| Certifications and Limitation on Benefits position | Whether you can certify treaty-country residence, beneficial ownership, and any applicable Limitation on Benefits position |

Before you move on, do one final checkpoint. IRS treaty tables are summaries, not a substitute for treaty text, and Table 4 highlights major Limitation on Benefits tests. If your documentation is questionable, check the actual treaty provisions. If a payor knows or has reason to know a claim is ineligible, it must not apply the treaty rate.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Build a clean mental model of what the treaty can and cannot do#

Treat the treaty as a reference point for cross-border tax questions, not as a shortcut that removes filing and record-keeping duties. That distinction prevents a lot of early mistakes.

Start with what the treaty is for#

Use the treaty documents to frame cross-border tax questions and possible double-taxation issues, then check filing duties separately under domestic rules. For this workflow, keep your notes anchored to the treaty text without over-interpreting any single clause too early.

Read the treaty as a document set, not one file#

When wording feels unclear, go back to the full UK treaty document set listed by the IRS, which says complete texts are available in PDF:

| Document | IRS listing detail |

|---|---|

| Income Tax Treaty | Income Tax Treaty PDF - 2001 |

| Technical Explanation | Technical Explanation PDF - 2001 |

| Protocol | Protocol PDF - 2001 |

| Exchange of Notes | Exchange of Notes PDF - 2001 |

The IRS page also points to the U.S. Treasury tax treaty documents page for further treaty information. In practice, note which document you relied on when you record your position.

Flag the Saving Clause early#

If you run into the Saving Clause, take it as a signal to verify your assumptions before you act. Do not assume treaty relief by itself means there are no domestic filing obligations.

Keep a separate UK filing baseline in view#

Keep UK compliance mechanics in a separate note from your treaty analysis. HMRC says you must tell HMRC by 5 October if you need to complete a return for the previous year, and late notification can lead to a penalty. HMRC also says you need records, for example bank statements or receipts, and filing can be delayed if you submit without reactivating an existing account.

| Checkpoint | Detail |

|---|---|

| Tell HMRC if you need to file | HMRC says you must tell HMRC by 5 October if you need to complete a return for the previous year, and late notification can lead to a penalty |

| Sole trader registration | GOV.UK says registration is required when earnings exceed £1,000 in a tax year |

| Records | HMRC says you need records, for example bank statements or receipts |

| Account status | Filing can be delayed if you submit without reactivating an existing account |

| Online filing route | HMRC lists cases where its online Self Assessment service cannot be used, including if you lived abroad as a non-resident |

For sole traders, GOV.UK says registration is required when earnings exceed £1,000 in a tax year. HMRC also lists cases where its online Self Assessment service cannot be used, including if you lived abroad as a non-resident.

Run the residency and permanent establishment checks in order#

Use this order to keep the analysis clean. Confirm domestic filing facts first. If a dual-residency conflict appears, flag Article 4 (Residence) for review. Then review Article 5 (Permanent Establishment) before relying on conclusions under Article 7 (Business Profits).

Treaty analysis does not replace weak underlying facts. If your HMRC status, filing route, or records are unclear, your position can become inconsistent across filings and notes.

Step 1 starts outside the treaty#

Start with UK Self Assessment mechanics and document what is known. If you need to complete a return for the previous year, HMRC says you must tell them by 5 October. In the cited guidance example, the previous tax year is 6 April 2024 to 5 April 2025, and late notification can lead to a penalty. If you are a sole trader and earn more than £1,000 in a tax year, registration is required.

Before making treaty claims, confirm the basics: whether you have a Unique Taxpayer Reference (UTR), whether an older Self Assessment account needs reactivation, and whether the online filing service fits your case.

Step 2 tests nexus before profits#

Once your filing posture is clear, use this workflow to check Article 5 (Permanent Establishment) before leaning on Article 7 (Business Profits).

From this material, PE is an open question, not a conclusion. Keep it open until the facts are documented. At minimum, keep the records HMRC expects, such as bank statements or receipts, so your return and evidence file line up.

Confirm the filing route early as well. HMRC states its online Self Assessment service is unavailable in some cases, including where you lived abroad as a non-resident. In those cases, use commercial software or other forms.

Step 3 handles older terminology carefully#

If you see Independent Personal Services in older commentary, treat it as a signal to reconcile terminology, not as a conclusion. Keep your notes explicit about what is still unresolved, and do not mix labels as if they are interchangeable until you confirm which treaty framing you are actually relying on.

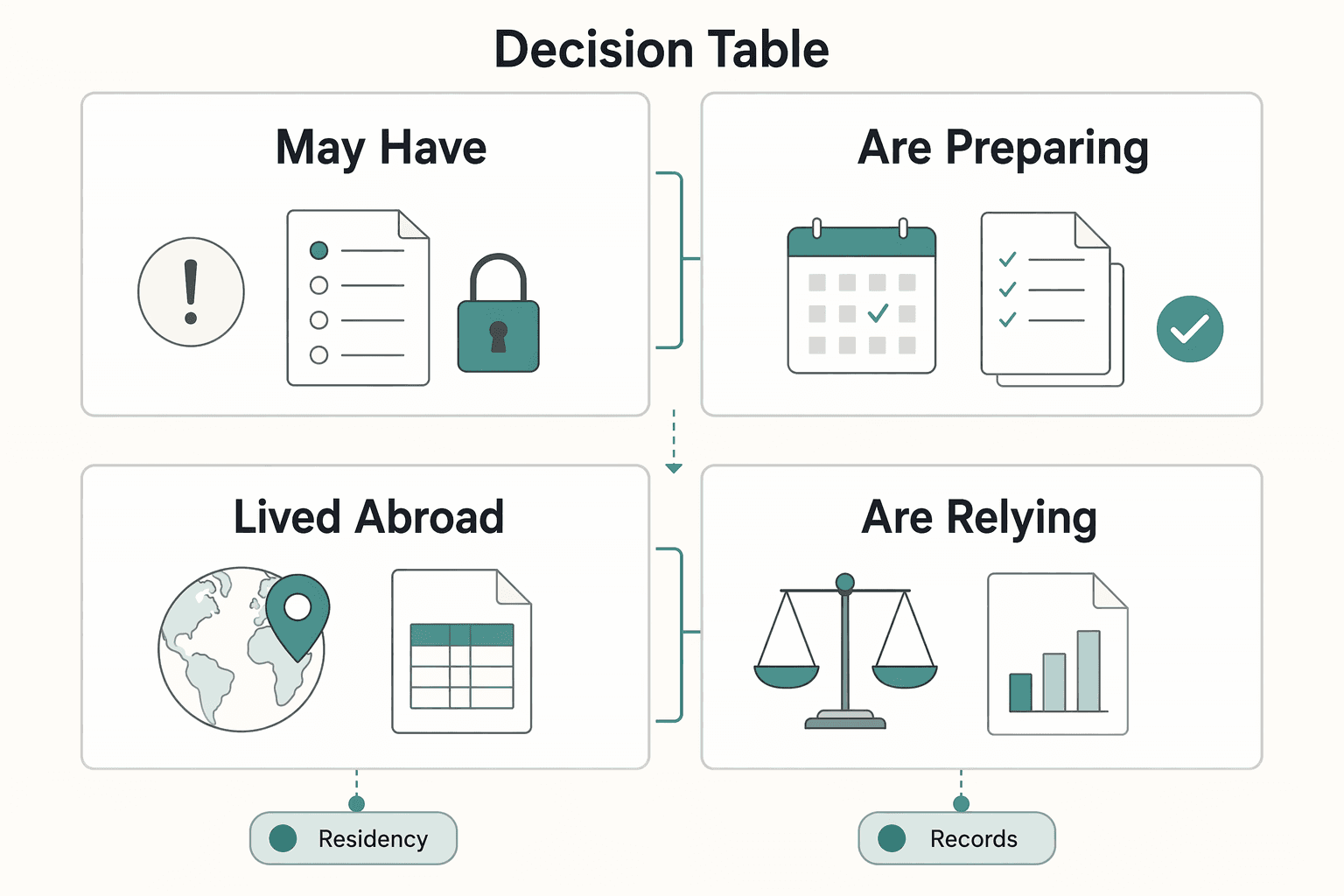

Decision table#

| Fact pattern | Likely treaty article to review first | What is still unknown | What evidence to collect |

|---|---|---|---|

| You may have tax ties in both countries | Article 4 (Residence) | Whether there is a real dual-residency conflict | HMRC registration status, UTR status, dated filing notes, bank statements or receipts |

| You are preparing to allocate business profits | In this workflow, Article 5 (Permanent Establishment), then Article 7 (Business Profits) | Whether a PE-type question exists before profit allocation | Filing records, bank statements or receipts, dated work or fact notes |

| You lived abroad as a non-resident and plan to file online | Domestic filing route first, then treaty articles if needed | Whether HMRC online filing is available for your case | HMRC route check, account reactivation status, copies of forms or software submission path |

| You are relying on older material using Independent Personal Services | Reconcile with current treaty reading before concluding | Whether the older label maps cleanly to your current treaty analysis | Source note, current treaty-reading note, explicit unresolved items |

If Step 1 is incomplete, pause. Lock down filing posture and evidence first, then move through Article 4, Article 5, and Article 7.

Apply the filing baseline even when treaty relief is available#

Treaty relief can change tax outcomes, but it does not erase routine filing duties. Treaty positions may reduce double taxation, but you still need your domestic filings to be complete and internally consistent.

If you are filing in more than one country, keep each return position explicit even when your clients are in the US. For US-connected cases, separate two decisions: filing required and tax due.

Separate filing duty from liability outcome#

If you claim the Foreign Earned Income Exclusion (FEIE), the IRS position is clear: you still file a return and report the income. A common mistake is treating excluded income as if it does not need to be reported.

FEIE also requires qualification, not assumptions:

- Under the physical presence test, you need 330 full days in a 12-month period.

- Those days count only if your tax home is in a foreign country.

- If you miss 330 full days, you do not meet that test.

- Bona fide residence is not automatic just because you lived abroad for one year.

Relief methods still create paperwork#

Foreign Tax Credits can change liability, but they still sit inside the filing baseline. The key filing mechanic is Form 1116:

- Use a separate Form 1116 for each income category.

- Check only one income-category box on each form.

If your books do not map cleanly to those categories, credit calculations can become a weak point.

Run one consistency check before you file#

Before filing, confirm your treaty position, domestic return disclosures, and payer-facing paperwork all tell the same story.

- Residency facts and dates are consistent across notes and return drafts.

- Income classification matches invoices, bookkeeping, and any Form 1116 workpapers.

- Your relief path, whether FEIE, Foreign Tax Credits, or a treaty position, does not conflict with prior disclosures.

If those items do not align, fix that first. In cross-border compliance, conflicting paperwork can be a bigger risk than the underlying tax amount. For a step-by-step walkthrough, see A Freelancer's Guide to the US-Australia Tax Treaty.

Handle Form W-8BEN correctly with US clients and platforms#

For onboarding, send Form W-8BEN to the US payor acting as the withholding agent, for example a client or platform, not directly to the IRS in that intake step. Treat it as payer-facing withholding documentation, not a generic admin upload.

Send the right form for the income type#

Use the form that matches how the income is being treated. For income that is not earned from personal services, use Form W-8BEN. For income earned from personal services, use Form 8233.

If a payer requests W-8BEN for personal-services income, pause and confirm how they are classifying the payment before you submit anything.

Use a simple if-then workflow#

Keep the process simple and documented:

- If a US client or platform requests withholding documentation, submit the form that matches the income type through their intake process, and keep your own record of what you sent and when.

- If they cannot intake your form, document the escalation in writing and ask for their manual review path for foreign payee tax documentation.

A platform's intake limits can affect operations, but they do not by themselves determine treaty eligibility under the US-UK Tax Treaty.

Do not send it blindly#

A W-8BEN is a certification. Your treaty claim should line up with the facts you are certifying, including treaty-country residence, beneficial ownership, and, when relevant, limitation-on-benefits conditions. If you are claiming a reduced treaty withholding rate, a U.S. or foreign TIN is generally required, with limited exceptions for certain marketable securities.

If your treaty article or rate is unclear, use the IRS treaty tables to identify the likely claim, then confirm it against the actual UK treaty documents. The tables are directional, not a complete substitute for treaty text.

Choose FEIE or Foreign Tax Credits with a defensible rationale#

Choose the method that fits your facts this year, not the one you used last year. FEIE and Foreign Tax Credits both address double-tax pressure, but they depend on different qualification and documentation paths.

Start with eligibility before you compare outcomes:

- FEIE applies only if you are a qualifying individual with foreign earned income.

- Under the physical presence test, you need 330 full days in foreign countries during a 12-consecutive-month period, and a full day is 24 consecutive hours.

- Those 330 days do not need to be consecutive, but if you miss the threshold, you do not pass that test.

- Under the bona fide residence test, you need bona fide residence for an uninterrupted period that includes an entire tax year. Living abroad for one year is not automatically enough.

- Foreign Tax Credits require their own filing support on Form 1116, with one income-category box per form and separate country lines or columns where required.

| Relief method | Typical use case | Interaction risks | Records needed |

|---|---|---|---|

| FEIE (physical presence) | You can document 330 full days abroad in a 12-month window | Day-count mistakes; incomplete full-day support | Day-count records, FEIE workpapers, income records |

| FEIE (bona fide residence) | You can support bona fide residence covering an entire tax year | Treating one year abroad as automatic qualification; weak residence support | Residence-period records, income records, FEIE workpapers |

| Foreign Tax Credits | You can support Form 1116 treatment by income category and country | Wrong income category; weak country-by-country tracking | Form 1116 workpapers and country-level tracking records |

One FEIE interaction to watch: if you claim a foreign housing exclusion, it reduces the income available for FEIE. The FEIE maximum is $130,000 (2025) and $132,900 (2026) per qualifying person, but the exclusion is limited to foreign earned income minus any housing exclusion claimed.

Before filing, keep a clear evidence set:

- side-by-side FEIE vs FTC computations

- FEIE and/or Form 1116 workpapers used in the return

- records supporting the physical presence or bona fide residence position you claimed

Before you lock your filing position, document your residency facts and ties in the Tax Residency Tracker so your relief choice is backed by a clean evidence trail.

Read the high-impact treaty articles without overclaiming#

If you freelance across the US and UK, use the treaty as a control point, not a shortcut. Flag Article 4 (Residence), Article 5 (Permanent Establishment), Article 7 (Business Profits), Article 23 (Limitation on Benefits), and Article 26 (Mutual Agreement Procedure). Then verify what you can actually support in your file, and treat these article labels as prompts rather than enough detail for substantive treaty conclusions.

| Article | Use | Caution |

|---|---|---|

| Article 4 (Residence) | Review if a dual-residency conflict appears | Treat article labels as prompts rather than enough detail for substantive treaty conclusions |

| Article 5 (Permanent Establishment) | Review before Article 7 | PE is an open question, not a conclusion |

| Article 7 (Business Profits) | Review after Article 5 when preparing to allocate business profits | Do not rely on it before checking Article 5 |

| Article 23 (Limitation on Benefits) | Flag for review | Do not claim specific Article 23 status tests from this section |

| Article 26 (Mutual Agreement Procedure) | Flag for review | Do not claim when Article 26 should be started or what result it should produce |

This is where discipline matters most. Keep your claims tight:

- Do not treat article titles alone as proof of your filing position.

- Do not claim specific Article 23 status tests from this section.

- Do not claim when Article 26 should be started or what result it should produce.

- Do not claim how a Technical Explanation or Protocol changes treaty application from this section.

A good default before filing is a one-page note listing each article, the exact question you are trying to answer, and the document that supports your facts. If your records do not support the claim, generalize or pause instead of overcommitting.

Keep that discipline tied to UK filing basics. First-time filers must register for Self Assessment before using the online service. You need a UTR. Existing accounts may need reactivation to avoid delays, and you need records, for example bank statements or receipts. If you lived abroad as a non-resident, HMRC says the online service is not available and directs you to commercial software or other forms.

Keep an audit-ready evidence pack from day one#

Build one indexed evidence pack early so your positions stay consistent and supportable across filings. Keep the core records together: your residency timeline, contracts, invoices, payment records, payer correspondence, and workpapers for any U.S. relief claim.

If you are using Foreign Earned Income Exclusion (FEIE), document the qualification method, not just the income amount:

- For the physical presence test, track the exact 12-month window and confirm 330 full days abroad.

- Count each full day as 24 consecutive hours, midnight to midnight.

- Missing the day count fails this test even for illness, family problems, vacation, or employer orders.

- If you are using bona fide residence, keep a short facts memo plus supporting records, because living abroad for one year alone does not automatically establish bona fide residence.

If you are claiming Foreign Tax Credits, keep a full Form 1116 calculation file:

- Use a separate Form 1116 for each income category.

- Check only one category box on each form.

- Use separate country lines or columns when taxes were paid to multiple foreign countries or territories.

- Report amounts in U.S. dollars except where Part II says otherwise.

For other U.S. information-reporting items outside FEIE/FTC, keep your analysis and supporting documents together while you confirm what applies.

Avoid the mistakes that cause rework, penalties, and stress#

Rework usually starts when your documents tell different stories. Treat the US-UK treaty as a document set, not a blanket exemption, and keep your filings aligned before you submit.

A safer default is to avoid these mistakes:

- Treating treaty relief as automatic instead of checking your position carefully against the full treaty materials.

- Letting your UK and U.S. filings and U.S. relief workpapers, including Form 1116, conflict.

- Filing FTC positions as if they are automatic. The IRS says eligibility requires 4 tests, and some foreign taxes are still non-creditable even when those tests are met.

- Missing Form 1116 mechanics: use a separate Form 1116 by income category, and check only one category box on each form.

- Claiming Foreign Earned Income Exclusion (FEIE) and Foreign Tax Credits on the same excluded income stream.

Red flags that should trigger immediate review#

If any of these show up, stop and review before filing:

- treaty relief is being treated as automatic without checking the full treaty document set

- FTC is claimed without confirming the IRS qualifying tests

- potentially non-creditable foreign taxes are included in the FTC calculation

- FTC is claimed without a clean Form 1116 category split

- FEIE and FTC touch the same income stream

If even one red flag appears, pause and resolve it before filing so the final package stays consistent. Related reading: A Deep Dive into the US-Japan Tax Treaty for Remote Workers.

Conclusion#

The sequence that usually works is simple: confirm your residency facts, complete baseline filings, and keep matching records. Treaty outcomes and payer-form handling depend on your specific facts and are not established here.

Treat UK Self Assessment as an operational checkpoint, not an afterthought. If you are filing for the first time, register before using HMRC's online filing service. To file online, you need your Unique Taxpayer Reference (UTR), and if your old account is inactive, reactivate it first to avoid delays.

Before filing, run one quick consistency check:

- filing route matches your situation

- account status is active

- records support the same story

- submitted details do not conflict across forms

If you lived abroad as a non-resident, HMRC says you cannot use that online filing service and should use commercial software or other forms instead.

Keep key UK dates visible. In the cited guidance snapshot, HMRC says you must notify them by 5 October 2025 if you needed to file for the previous tax year (6 April 2024 to 5 April 2025). Online filing is on or after 6 April following tax year end, tax is due by 31 January, and missing the filing deadline can trigger a penalty. For sole traders, the cited registration trigger is earning more than £1,000 in a tax year.

Keep your evidence pack plain and complete. HMRC expects records, for example bank statements or receipts, so you can complete the return correctly. If your facts, paperwork, and filing path point in different directions, pause and resolve the mismatch before filing.

To turn this checklist into a repeatable workflow, use the Gruv tools hub for tax-document and compliance helpers aligned to freelancer operations.

Frequently Asked Questions

Do I pay UK tax first or US tax first when I freelance in the UK for a US client?

These materials do not establish a UK-first or US-first ordering rule. Use a safer default: keep a clean record of what tax was paid, to which country, on which income, and for which period. If you plan to claim U.S. relief on Form 1116, keep your country details and income-category split organized before filing.

Does the US-UK Tax Treaty automatically prevent double taxation for freelancers?

No automatic treaty outcome is supported by these IRS excerpts. Do not treat the treaty as a blanket shield without a separate treaty analysis. Keep your treaty position consistent across your return filings, relief calculations, and payer paperwork.

Do I still need to file in the US if I live and work in the UK?

Yes, if you are using FEIE, you still file a U.S. return reporting that income. FEIE is an exclusion for qualifying individuals, not a filing waiver. Also, living abroad for one year alone does not automatically establish bona fide residence for FEIE.

Do I send Form W-8BEN to the IRS or to my US client or platform?

These materials do not say where Form W-8BEN is submitted. Follow your payer or platform process and keep proof of submission.

How do I decide between FEIE and Foreign Tax Credits for the same tax year?

There is no universal winner in these materials. Start with eligibility and mechanics. FEIE requires qualifying status, often through the physical presence test (330 full days in any 12 consecutive months, with a full day as 24 consecutive hours from midnight to midnight) or bona fide residence for an uninterrupted period that includes an entire tax year. For FTC claims, Form 1116 must be split by income category, with only one category box checked per form. If taxes were paid to multiple countries or territories, Form 1116 also requires separate country lines and columns.

What records should I keep in case HMRC or IRS asks for proof?

Keep documents that directly support the position you filed. For FEIE, keep a detailed travel log and day-count support, because missing the minimum presence requirement is a hard failure regardless of the reason. For FTC, keep foreign-tax payment proof, Form 1116 workpapers by category and country, filed returns, and matching invoice or payer records for the same income stream.

When should I escalate to a cross-border tax professional instead of self-filing?

Escalate when your result depends on a close call rather than clear facts. Common examples are day counts near the 330-day threshold, a weak bona fide residence position, or inconsistent drafts across FEIE, Form 1116, and payer documentation. If you cannot explain your filing position clearly from your records, escalate before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/forms/2023/2023-1031-publication.pdftrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- gov.uk/log-in-file-self-assessment-tax-returnexternal

- gov.uk/self-assessment-tax-returns/registeringexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How to Find the Best Deals on Flights

If you are planning a move or a long stay, the right way to find cheap flights is to choose the fare that supports the trip you are actually taking, not just the one with the lowest headline price. A cheap fare can still be the smart choice, but only if it gets you there on a schedule you can use, leaves you functional when you land, and gives you booking records you can work with later.