Quick Answer

Yes, a U.S. freelancer living in Australia can still owe U.S. tax, and the us-australia tax treaty freelancer question is resolved by facts, not slogans. Start with residency and income classification, then test treaty treatment, Foreign Tax Credit mechanics, and FEIE eligibility. The article’s sequence uses IRS treaty documents, Form 1116 category separation, and a written evidence pack before filing. It also flags early escalation when Saving Clause or Permanent Establishment interpretation could change the result.

Introduction for freelancers who want a defensible tax position#

If you freelance across borders, a defensible tax position is usually the fastest route to a clean filing. The order matters: lock down the facts, test the treaty treatment, then map the filings and relief choices. If you reverse that order, it is easy to optimize for an answer that falls apart once someone asks for support.

Start with primary documents, not forum summaries or recycled templates. For Australia, the IRS treaty index points you to the Income Tax Treaty, the Protocol, and the Technical Explanation, and it routes you to Treasury treaty documents for added context. Treat that set as the baseline reference for your file.

Use the document timeline as a quality check, not as the filing answer. The index reflects 1982 treaty materials and 2001 protocol materials and shows a last reviewed date of 08-Aug-2025. That does not decide your return, but it does help confirm that you are working from the currently listed set.

If your facts are mixed, pause before you claim anything. Build a short fact log and tag each item as confirmed, assumed, or unknown. That one-page habit prevents quiet assumptions from spreading into every later worksheet.

A simple way to keep the work clean is to split it into two passes. Pass one is fact integrity: timeline, contracts, invoices, and payment evidence. Pass two is tax treatment: treaty position, credits, exclusions, and filing forms. Keeping those passes separate helps you avoid shaping the facts around a preferred outcome.

By the end of this guide, you should have three concrete outputs:

- A decision sequence you can follow before filing.

- A records checklist tied to the claims you may need to defend.

- Clear escalation triggers for issues that should not be handled solo.

That thread runs through the rest of the article. The goal is not a clever interpretation. It is a filing position that is coherent, documented, and hard to dispute.

Define the terms before you decide anything#

Most cross-border filing mistakes start as language mistakes, not math mistakes. If the labels shift halfway through the analysis, the same facts can produce different answers on different worksheets. Define the terms once, then use those same labels everywhere.

Use document authority in this order:

- Income Tax Treaty PDF as base text.

- Protocol PDF as additional treaty text.

- Technical Explanation PDF for interpretation support.

- IRS Australia treaty index, then Treasury treaty documents for supplemental context.

Keep these working definitions stable in your file:

- Tax Residency: determined by facts and circumstances under the guidance used here.

- Permanent Establishment: a practical check on whether activity may create a taxable business presence.

- Source-of-Income Rules: a practical check on where each income stream arises.

- Residency Tie-Breaker Rules: treaty analysis used when both countries can plausibly treat the same person as resident.

Add one control before you run numbers: if a key term cannot be grounded in records, tag that line as unknown and stop that calculation branch. That keeps uncertainty visible and avoids fake precision later.

A one-page definitions sheet in your annual folder is usually enough. Use the same labels in your memo, your Form 1116 workpapers, and your advisor notes. Most avoidable confusion comes from relabeling the same facts, not from lack of effort.

Do not skip the self-employment branch while you define the file. IRS guidance defines self-employment tax as Social Security and Medicare tax on net self-employment earnings. It also says the rules are generally the same for a self-employed U.S. citizen or resident whether in the United States or abroad. Net earnings of at least $400 can trigger self-employment tax. The same guidance says self-employment income still counts in net earnings even when part of gross income is excluded under FEIE.

If residency or income character is still unclear after this setup, stop there and resolve it. Treaty relief built on unstable definitions is hard to defend later.

Known vs Unknown box

| Item | Known now | Unknown needs fact-specific review |

|---|---|---|

| Authority docs | Treaty, Protocol, and Technical Explanation are in hand | Which provisions control your exact facts |

| Tax Residency | Facts and circumstances drive the analysis in this guidance | Whether treaty tie-breaker analysis is required |

| Source-of-Income Rules | Income streams and client locations can be listed now | Final sourcing result for each stream |

| Self-employment tax | U.S. status and the $400 trigger are known checkpoints | Whether final treatment changes tax due, reporting duty, or both |

Start with your residency facts before touching treaty claims#

Do not draft treaty conclusions until your residency file is stable. Build one timeline that both countries could read and test. If you cannot support a timeline entry, mark it clearly instead of filling the gap with assumptions.

Track these items in one date sequence:

- Days physically present in each country, including arrival and departure dates.

- Home-base evidence such as lease periods and occupancy records.

- Family and economic ties.

- Tax-home indicators tied to where work activity was centered.

Use one date format and one location format throughout. In practice, mixed date styles and inconsistent place labels create avoidable review disputes, even when the underlying facts are sound.

Before you model credits or exclusions, apply this decision rule: if both countries could plausibly treat you as resident, pause and review tie-breaker language before you finalize calculations.

Then run a consistency check across the whole file:

- Keep one residency timeline across every worksheet.

- Align the home-base and ties narrative with documentary evidence.

- Refer to the same treaty set each time you cite treaty language.

A small control here saves a lot of rework later: every timeline line should point to a document, or to a note explaining why evidence is unavailable. That stops silent assumptions from drifting into treaty analysis and then reappearing as if they were established facts.

A common failure mode is claiming a treaty-sensitive position while residency facts are still moving. Timeline errors can change treatment, including U.S. self-employment outcomes tied to when income was received and whether you were a U.S. resident at receipt. Once residency is stable, the next hinge issue is income classification.

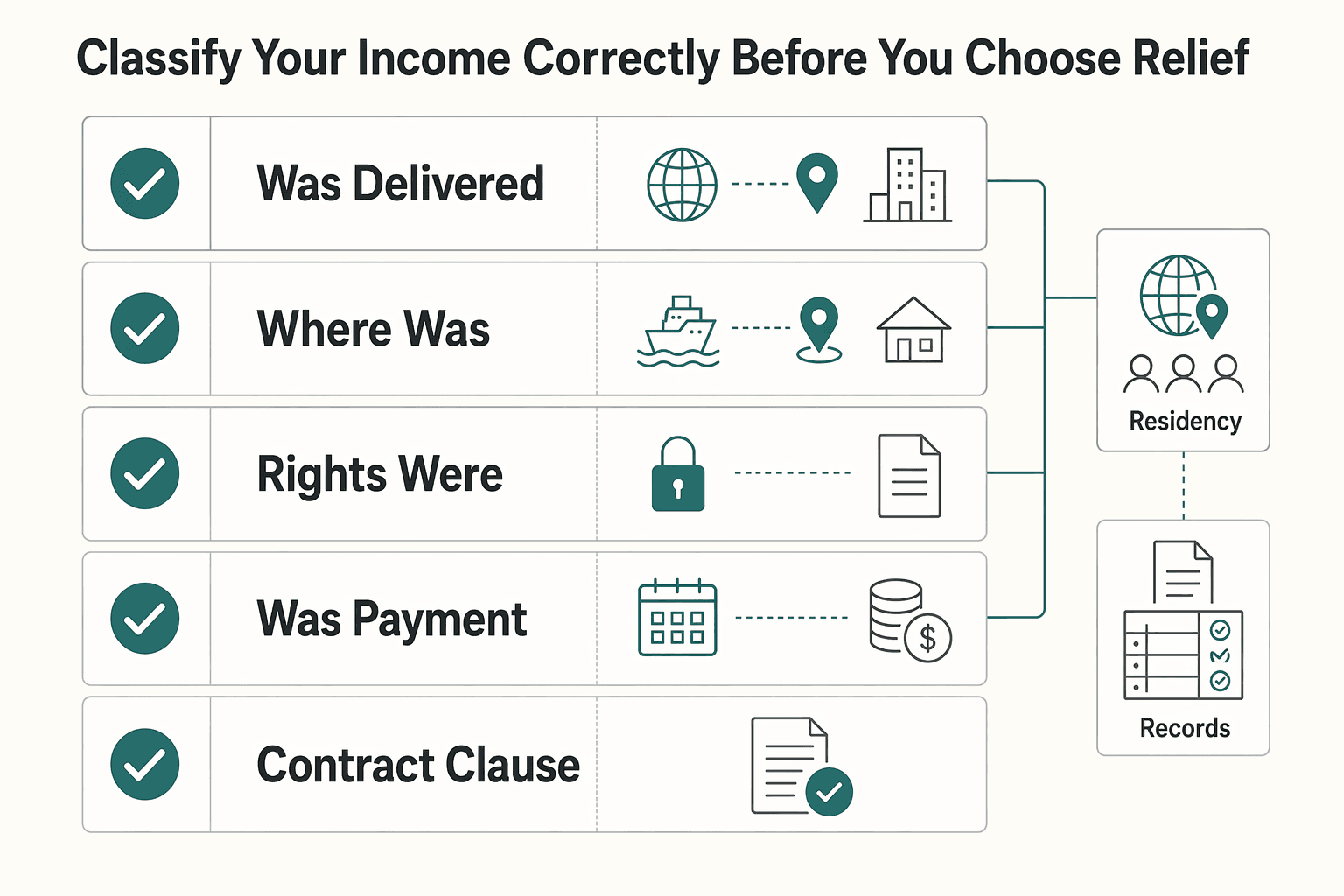

Classify your income correctly before you choose relief#

Income classification is the hinge decision in this file. If the classification is weak, the treaty position, the credit modeling, and the forms can all drift out of sync.

Separate service income and royalty-type income at the contract and invoice level. When one engagement includes both services and IP rights, split the language and the billing lines so each item has a clear character, date, and business purpose. You are not changing the economics. You are making the tax character visible and testable.

Run source analysis by stream, not as one annual assumption. A useful invoice-level check asks four direct questions:

- What was delivered?

- Where was the work performed?

- What rights were licensed, if any?

- When was payment received?

When contracts blend deliverables, force clarity through invoice structure. Keep service work and licensed-rights items on separate lines and map each line to the matching contract clause.

For U.S. exposure, test each stream for U.S. trade or business and ECI risk. IRS guidance says a foreign person generally must be engaged in a U.S. trade or business during the tax year for income to be treated as ECI. For personal services, it points to activity that is considerable, continuous, and regular.

Run self-employment timing and status checks at the same time. IRS guidance states that individuals who are neither U.S. citizens nor U.S. residents are not subject to U.S. self-employment tax. It also states that self-employment tax can apply when net self-employment earnings are at least $400, income received while you are a U.S. resident can be included even if services were performed while nonresident, and FEIE alone does not remove self-employment income from net-earnings calculations.

Before you choose a relief path, keep one evidence sheet for each income stream:

- Contract clause supporting character.

- Invoice lines mapped to services versus licensed rights.

- Source notes for that stream.

- Payment date and residency status at receipt.

- U.S. connection note showing ECI testing.

The tradeoff is simple. This takes more time now, but it cuts amendment risk later. If a payment cannot be supported cleanly from the records, that is the point to escalate, not the point to improvise.

Decide where tax is owed first using a simple decision table#

Set a first-taxing hypothesis before you pick relief elections. Use this table as a control for disciplined thinking, not as a substitute for full treaty interpretation.

Anchor each row to the treaty document set and mark incomplete facts as unknown instead of guessing.

| Residency status | Client location | Income type | Possible Permanent Establishment facts | Likely first-taxing jurisdiction | Likely relief path under the US-Australia Tax Treaty | Risk level |

|---|---|---|---|---|---|---|

| United States clearly supported by residency file | Mostly United States clients | Service income | No clear PE facts in Australia | Confirm with a qualified adviser | Do not finalize relief sequencing without full treaty text review | Medium |

| Australia clearly supported by residency file | Mostly United States clients | Service income | No clear PE facts in the United States | Confirm with a qualified adviser | Do not finalize relief sequencing without full treaty text review | Medium |

| Single-country residency appears likely, but contracts mix services and licensed IP | Cross-border client base | Services and royalty streams split by line | PE facts unclear | Confirm with a qualified adviser | Treaty analysis is required before any relief decision | High |

| Dual residency is plausible | Cross-border client base | Mixed service and royalty streams | PE facts uncertain | Undetermined until residency facts are fully resolved | Treaty position first, then relief sequencing after full treaty review | High |

If the facts are borderline, use the more conservative position and document why. Conservative here means easier to defend, not necessarily lower tax.

Before you rely on the table, run five checks:

- Reconcile each row to invoice-level source notes, not just annual totals.

- Confirm residency using facts and circumstances rather than one shortcut.

- Check whether any service was physically performed in California, because California guidance treats services performed in California as California-source for nonresidents.

- Use California residency and source checks only for California analysis, not as a substitute for Australian residency conclusions.

- If any row shows a conflict, mark it high risk and escalate before filing.

Treat each row as a mini case file. Keep the row result, the key evidence, and the open issues together so the review trail matches the filing logic. This table tells you where to start. The next section is about sequencing the actual relief tools once that starting point is clear.

Apply treaty relief, credits, and exclusions in the right order#

Use one repeatable order each year: document the treaty position, model the Foreign Tax Credit, then test FEIE. Use it as a filing discipline for consistency. It is not a claim that one rule always overrides every case.

Lock your facts before calculations: residency support, income character, service location, and foreign taxes paid or accrued. For FTC work, Form 1116 is category-specific. Use a separate Form 1116 for each income category and check only one category box per form.

FEIE should be tested on its own requirements, not on preference. You still file a U.S. return reporting the income. Eligibility depends on the qualification rules, including minimum time requirements under bona fide residence or physical presence tests, subject to limited exceptions. For 2026, the stated FEIE maximum is $132,900 per person.

If you are also claiming a foreign housing exclusion or deduction, compute housing first because it reduces the FEIE limit base. The general housing limit is 30 percent of the FEIE maximum, and IRS materials list a 2026 housing amount of $39,870.

Before you lock any election, reconcile three branches on one page: the treaty position, the Form 1116 category results, and the FEIE qualification facts. If those branches do not line up, the risk is procedural even before you get to interpretation.

Do not assume FEIE is automatically better than FTC. Choose the path your facts support and write down why. A short year-specific election memo can do most of the work:

- What you claimed this year.

- What changed from last year.

- Why the change is supported by records.

If nothing changed, say that directly. If the facts changed, tie each change to documents and show where the treatment changed.

The common failure modes here are familiar:

- Switching between FTC and FEIE across years without a written, fact-based reason.

- Trying to credit tax on income that was also excluded.

- Filing Form 1116 without clean category separation.

Have this review file ready before you submit:

- Dated treaty-position memo for the tax year.

- Form 1116 copies by income category.

- FEIE qualification records, including day counts.

- Workpapers showing foreign earned income was reported before exclusion.

- Housing calculations with ordering and cap checks.

- Proof of foreign tax paid or accrued tied to return lines.

If any of that is missing, close the gap before filing. Good mechanics help, but they do not solve interpretation risk by themselves. That is where Saving Clause and Permanent Establishment issues usually come to the surface.

Handle Saving Clause and Permanent Establishment without guessing#

Do not guess on Saving Clause or Permanent Establishment issues. If the answer turns on ambiguous treaty language or disputed facts, that is a professional review point.

For U.S. citizens, worldwide U.S. taxation remains the baseline even while living abroad. That is why treaty analysis, FEIE, and FTC can all matter in the same file. Clean mechanics make the issue visible, but they do not remove interpretation risk.

Keep these profiles separate from the start:

- A U.S. citizen freelancer in Australia usually starts from worldwide U.S. taxation, then applies treaty and relief analysis. FEIE may reduce taxable foreign earned income when qualification is met, but it does not remove the need for consistent classification and documentation.

- A non-U.S. freelancer with U.S. clients may start from a different baseline, so residency facts, treaty position, entity classification, and local law can drive more of the outcome.

A common mistake is copying conclusions from one profile to another because the client mix looks similar.

Before you file a Saving Clause or PE-sensitive position, keep a short evidence set:

- One-page fact memo covering citizenship, residency, client location, and service location by stream.

- Year-specific treaty-position statement noting what changed or did not change.

- Contract and invoice excerpts supporting classification.

- Notes separating clear interpretation points from ambiguous points.

- Escalation note for any issue that depends on unresolved treaty language.

If two reasonable readings produce different filing positions, escalate early. Delay is cheaper than defending an avoidable interpretation error.

Build your evidence pack before filing season starts#

Build the evidence pack before deadline pressure arrives. The objective is simple: one clean line from source documents to filing positions.

Start with transaction records, then add the legal support in the same tax-year folder:

- Signed contracts.

- Invoices.

- Payment confirmations.

- Income map linked to residency analysis.

For each line item, track the same core fields:

- Client location.

- Service delivery location.

- Income type.

Keep treaty and Technical Explanation excerpts in the folder you actually use to file, not only in bookmarks. When review starts, you should not need to rebuild the legal basis from memory.

Residency is still fact-based and circumstance-driven. If the facts changed during the year, split the records by period and align each period with the position taken.

Run one pre-filing coherence check before anything gets submitted:

- Residency facts match the narrative in your return workpapers.

- Every invoice maps to client location, service location, and income type.

- Each mapped line ties to contract, invoice, and payment proof.

- Treaty excerpts in the file match the claims in your memo.

Add a short change log to the same folder. Record what changed, when it changed, and which position was updated. That small step prevents repeated analysis and makes the next year faster.

File the forms freelancers commonly miss#

Treat tax due and reporting duty as separate decisions. A better tax result does not automatically remove information filing obligations.

Start with Form 8938 if it is applicable. It is attached to the income tax return. IRS materials note a commonly cited $50,000 figure for certain filers and also say higher thresholds can apply for joint filers and taxpayers residing abroad.

Use one hard guardrail: if you are not required to file an income tax return for the year, Form 8938 is not required for that year.

Run FBAR as a separate branch. Filing Form 8938 does not replace a FinCEN Form 114 requirement when FBAR rules otherwise apply. For FBAR value reporting, record amounts in U.S. dollars and round up to the next whole dollar.

The common failure mode here is simple: people equate no tax due with no filing requirement.

Keep one filing matrix with one line per form: required, not required, or pending review. Tie each line to the supporting memo or worksheet in your annual folder so the conclusion is traceable.

Use that matrix as a consistency tool, not just a checklist. If one line says not required, your memo should explain why in facts-based terms. If one line is pending, assign an owner and a date so the issue does not roll into deadline week unnoticed.

Minimum records to keep:

- Form 8938 applicability worksheet with filing status and residency context.

- Filed Form 8938 copy, if required, attached to return records.

- Separate FBAR decision memo explaining why FinCEN Form 114 was or was not required.

- FBAR valuation workpapers in U.S. dollars with rounding notes.

Keeping these branches separate reduces contradictions across the return, FBAR filings, and year-over-year positions.

Compare three freelancer scenarios and the safer default in each#

When the facts are mixed, the safer default is full reporting first and relief second. Report the income completely, then claim relief only where eligibility is documented.

| Scenario | Likely first filing actions | Likely relief path | Escalation trigger |

|---|---|---|---|

| Australia-based consultant, mostly United States clients, with cross-border facts still unclear | File U.S. return with income reported. Build a fact file from contracts, invoices, and delivery records before taking a facts-sensitive position. Prepare Form 1116 by income category if claiming credits. | Start with FTC modeling. Test FEIE only if qualifying status and foreign earned income treatment are supportable. If FEIE is used, apply the 2026 annual limit of $132,900, adjust for qualifying days for part-year qualification, and compute housing first because it limits FEIE. | Key facts remain unclear and could change filing position. |

| Conflicting residency indicators that could change filing treatment | Keep return reporting complete while eligibility evidence is reconciled. Treat relief calculations as provisional until facts are coherent. | Do not lock final FTC versus FEIE treatment until eligibility facts are stable. If FEIE is tested, confirm minimum time requirements are met or an exception is documented. | Two supportable fact patterns produce different filing outcomes. |

| Contracts that mix multiple income categories | Split records into distinct streams before computing relief. Keep separate workpapers so one stream does not distort another. | Use separate Form 1116 filings by income category. Test FEIE only on amounts that clearly meet FEIE requirements and are still reported on the return. | Income characterization remains disputed or changes year to year without documented facts. |

Across all three scenarios, avoid one repeated error: lower tax due does not mean fewer filing duties. FEIE does not let you omit income from a U.S. return, and Form 1116 category mechanics still matter when credits are claimed.

Before filing, run this three-point check:

- Amounts excluded under FEIE are still reported on the return.

- Each Form 1116 has one category and one checked category box.

- Scenario memo conclusions match the underlying records.

If any one of those fails, pause and escalate.

Red flags that mean you should bring in a pro now#

If even one of these red flags is still unresolved, bring in a cross-border advisor. Any single issue here can change the filing position and increase amendment risk.

1) You cannot clearly separate services income from IP income#

Do not finalize treatment when contracts mix delivery work and licensing terms without clean mapping. Contract clauses and invoice lines should point to separate income types. If they do not, your character analysis is unstable.

2) Your residency facts support more than one defensible answer#

Escalate when the outcome changes depending on which residency narrative you use. If additional residency analysis could reverse the result, treat the current position as provisional until the facts are reconciled.

3) Your result depends on disputed interpretation#

If the filing result depends on debatable treaty language or unclear cross-border facts, this is no longer a routine self-prep decision. Escalation is a control, not a failure.

4) Prior-year filings conflict with this year's assumptions#

Escalate when this year's narrative does not align with prior-year returns, FBAR filings, or Form 8938 treatment. Year-over-year inconsistency without documentation is a review risk.

For Form 8938 and FBAR in particular, pause for review if any core duty point is unclear.

Core filing duty checks:

- Form 8938 is attached to an income tax return.

- If no income tax return is required for the year, Form 8938 is not required for that year.

- Filing Form 8938 does not replace separate FBAR duty when FBAR is otherwise required.

Threshold and valuation checks:

- The commonly cited $50,000 Form 8938 figure is not universal. Higher thresholds can apply for joint filers or taxpayers residing abroad.

- FBAR maximum account value is a reasonable approximation of the year's highest value, reported in U.S. dollars, rounded up to the next whole dollar, using the Treasury rate for the last day of the calendar year when conversion is needed.

Bring this packet to the first advisor call:

- Contract excerpts that separate services and licensing terms.

- Invoice and payment mapping by income type and country.

- Residency timeline with supporting facts.

- Prior-year filings plus current-year Form 8938 and FBAR workpapers.

What to do this week to stay compliant and low stress#

The next step is execution, not more theory. Every number should trace to a document, and every election should have a short written reason.

- Finish the fact sheet before tax modeling. Build one sheet covering residency facts and income classification. Record where you lived, where services were performed, who paid you, and how each payment is characterized. Keep unresolved points visible in a dedicated column.

- Assemble the file you will actually submit from. Gather FTC records, then draft Form 1116 workpapers while details are fresh. Keep category separation and country separation where required, and report Form 1116 amounts in U.S. dollars. Reconcile totals to source records before you move on.

- Use conservative treatment when facts remain uncertain. Do not claim FTC on income excluded under FEIE, and do not force unclear items into a credit position. Some foreign taxes are non-creditable even when four qualifying tests appear met, so compare credit versus deduction before locking treatment.

- Set escalation triggers now, not in deadline week. Escalate early when the outcome depends on unresolved treaty interpretation or residency judgment calls. Add one Australia-side trigger: if activity looks like employee work, ABN entitlement may not apply for that activity.

Use a weekly closeout rhythm: update facts, reconcile forms, resolve unknowns, and log what changed. Small weekly updates are easier than rebuilding the full file near filing deadlines.

This lowers stress because it removes last-minute guessing. If stronger facts appear later, individuals generally have up to 10 years to file a refund claim for additional creditable foreign taxes. Use that window for true corrections, not as a substitute for clean records now.

If you decide to bring in outside support, confirm country coverage and tax-document outputs before enrolling so your records can move straight into filing.

Frequently Asked Questions

Does the US-Australia Tax Treaty eliminate US tax for freelancers?

No blanket result is established here. This section does not show zero U.S. tax for every freelancer. If you claim FEIE, the income is still reported on the U.S. return.

Can a US citizen freelancer living in Australia still owe US tax?

Yes. FEIE applies only when qualification rules are met and the income is reported on a U.S. return. For 2026, the maximum exclusion is $132,900 per qualifying person, and part-year qualification requires a qualifying-days adjustment.

When does Permanent Establishment matter for a solo consultant with US clients?

This section does not provide a bright-line PE test for every fact pattern. If your result depends on PE interpretation, treat that as an escalation trigger.

Which comes first in practice: treaty position, Foreign Tax Credit, or Foreign Earned Income Exclusion?

This guide uses a practical sequence for consistency, but does not claim a universal legal ordering rule for all cases. Two hard mechanics do apply: use separate Form 1116 filings by income category and check one category box per form. If you claim a foreign housing exclusion, compute housing first because it limits FEIE.

What records should I keep before claiming treaty relief?

Keep records that support qualification timing, especially when the year includes qualifying and non-qualifying periods. Keep workpapers showing how foreign earned income and any housing exclusion were calculated. If you claim FTC, keep Form 1116 workpapers by income category.

Do I still need FBAR, FATCA, or Form 8938 if treaty relief reduces tax?

A reduced tax result does not resolve those filing questions by itself. The provided excerpts do not include FBAR, FATCA, or Form 8938 thresholds or filing tests, so confirm those requirements separately before submission.

When should I file Schedule SE in a US-Australia freelancer setup?

The provided excerpts do not include Schedule SE trigger rules. Treat Schedule SE as a separate analysis from FEIE and Form 1116 mechanics, and review that branch separately before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: