Quick Answer

Build your freelance financial safety net by setting one must-pay monthly baseline, then allocating every cleared payment the same day to tax, operating, reserve, and discretionary buckets. Require written terms before kickoff, including scope, billing trigger, due-date language such as Net 30, and a named approver. Track each invoice by billed, due, paid, and cleared status, then use a fixed overdue escalation path. Close the month only after payment proof and exception ownership are documented.

Build a Financial Safety Net That Protects Income and Payments#

Your freelance financial safety net is more than a savings balance. It is the set of controls that lets you cover fixed obligations on time when receipts are uneven, and it keeps invoiced revenue separate from cash you can actually spend. The goal is not to predict every slow month. The goal is to reduce the chance that one late client payment turns into missed bills, tax pressure, or borrowing.

Step 1#

Start with the bills that must clear even if no client pays this week. Include housing, utilities, insurance, debt minimums, committed payroll or contractor costs, critical software, and tax obligations.

If you are in the US, self-employed people generally need estimated tax payments, and the year is split into four payment periods: April 15, June 15, Sept. 15, and Jan. 15 of the following year.

Use one checkpoint first: can cash already received cover the next 30 days of must-pay items without depending on open invoices? If not, you have expected revenue, not a cash buffer. That distinction matters because an invoice can be valid and approved and still not become spendable cash in time. If you need the invoice to clear before rent, payroll, minimum debt, or tax cash can be covered, your position is tighter than your revenue report suggests.

Step 2#

Allocate each cleared payment the day it arrives. Cover current obligations, set aside tax cash, fund near-term operating needs, and move the rest to reserve cash for shocks or slow-pay gaps. Do not wait for month-end.

Under the cash method, income is generally reported when payment is received. Treat that as your operating reality too. Money is usable when it clears, not when it is invoiced.

The practical test is simple. If a payment lands today, you should be able to say what portion is already committed, what portion belongs to tax, and what portion is truly free to hold or spend. If that answer depends on memory, your month-end close will be slower and riskier than it needs to be. Small delays in allocation can blend tax money into ordinary spending and let strong invoice totals create a false sense of room.

| Check | Strong-month illusion | Cash-safe position | Triggered action |

|---|---|---|---|

| Invoices vs cash | You track only billed amounts | You track billed, due, paid, and cleared cash | Pause optional spend if cash trails receivables |

| Next 30 days | Covered by expected payments | Covered by cash already received | Tighten spend or accelerate collections |

| Tax readiness | Tax is a rough estimate | Tax cash is separated before spending | Move tax funds after each receipt |

| Late-payment risk | Delays are handled ad hoc | Aging by client is visible early | Follow up before invoices become overdue |

Step 3#

Set payment controls before work starts. Put terms in writing, invoice on time, confirm receipt, and identify the actual approver on the client side.

Use one recordkeeping system that shows income, expenses, billed date, due date, paid date, and status. Good records help you monitor business progress, and they make overdue invoices visible before they create serious cashflow pressure.

This sequence carries through the rest of the guide: define your baseline, split cleared cash fast, control payment timing, then review weekly and monthly. If you skip the order and start with reserve goals or debt goals first, you can end up optimizing around numbers that are not yet grounded in current cash, documented obligations, or actual receivable status.

Gather the Inputs Before You Touch Your Budget#

Clean records come first. If your inputs are messy, your reserve and debt decisions can rest on cash that is not actually available.

Step 1#

Pull everything into one working view: what has been billed, what has cleared, what still needs to be paid, plus the bills and receipts that support those entries. Paper is fine if that is what you have now, but move to a spreadsheet or app once manual tracking starts slowing updates.

The tool matters less than the view. One working view should let you answer four questions quickly: what is due to you, what has actually arrived, what you still owe this month, and what evidence supports each line. If you have to check email for one answer, a bank feed for another, and a notes app for a third, your cash picture is more fragile than it looks.

Step 2#

Before you analyze anything, separate income by cash state in a way that fits your workflow, such as invoiced, received, and expected. Keeping those labels distinct helps you avoid treating projected cash as usable cash.

Use one tracker format throughout. Common fields include client, reference, amount, billed date, due date, status, and an evidence link or note. You can also add a cleared date for received payments and a likely month for expected items.

This is a common failure mode in small-business admin. A month can look healthy because several invoices were sent, but sent invoices are not the same as cash in hand. A good tracker makes that visible without drama. You should be able to filter open items, scan overdue items, and see which expected receipts are still too uncertain to support a spending decision.

| Raw records | Decision-ready inputs |

|---|---|

| Mixed naming and reference styles | One client naming pattern and one reference per item |

| Bills, receipts, and account activity in separate places | Each entry tied to stored evidence |

| Inconsistent notes like "sent" or "waiting" | One shared status set across all records |

| No clear cash-state separation | Distinct labels for cash received vs not yet received (and expected items, if useful) |

Step 3#

Validate status and assign ownership. Each invoice should have one current status, and if more than one person touches the tracker, one person should own updates when status changes.

Before moving on, run two checks: flag invoices that are overdue or missing status, and flag any month where expected income sits below your essentials baseline. Once those are clean, you can plan reserves with more confidence.

If you work alone, ownership still matters. It just means you decide where the update happens and when. The point is to avoid half-updated records where the invoice was sent, but no one marked receipt confirmation, or where payment arrived, but the tracker still shows the invoice as open. Those small breaks can create bad decisions later, especially when you are choosing between reserve use, debt payments, and follow-up priority.

You might also find this useful: How to Set Financial Goals for Your Freelance Business.

Calculate Your Survival Number First#

Your survival number is the minimum cash you need for one month if payments arrive late. It is not a revenue target. It is your must-pay baseline so you can keep operating without missing obligations that protect your life, work, and tax position.

Step 1#

Classify recurring expenses before you total anything. Use only must-pay, can-delay, and optional.

Reserve must-pay for costs that create immediate risk if skipped this month: housing, core utilities, groceries and household supplies, work-critical transportation, insurance, minimum debt payments, and critical business tools. Include taxes here. If you are self-employed, IRS guidance says you generally need estimated tax payments if you expect to owe $1,000 or more, and late estimated payments may trigger penalties.

Use can-delay for real bills you can move without immediate damage. Use optional for costs you can pause now with no material consequence beyond convenience. If you are unsure where something belongs, ask one practical question: if this line does not get paid this month, what fails first? The answer usually reveals the right category faster than looking at the dollar amount alone.

| Expense example | Treat as | Decision criteria | Common misclassification |

|---|---|---|---|

| Rent, basic utilities, minimum loan payment | Essential | Missing payment creates immediate housing, service, or credit risk | Counting only the minimum and missing required bill-related fees |

| Groceries and household supplies | Essential | Needed for normal living and work continuity | Treating all food spend as essential, including convenience-heavy spend |

| Health insurance, business insurance, estimated taxes | Essential | Missing payment can create coverage gaps, penalties, or catch-up pressure | Labeling taxes or premiums as "irregular" and excluding them |

| Streaming, entertainment, noncritical apps, convenience services | Discretionary | Can be paused this month without breaking operations or compliance | Keeping small subscriptions in essentials because each one looks minor |

Step 2#

Total one month of must-pay costs and save that as your baseline. Convert quarterly, annual, or uneven required bills into monthly placeholders so timing does not hide the real obligation.

Then verify it against records. Check recent bank activity and bill evidence, and confirm each must-pay line is supported by a statement, invoice, premium notice, tax reminder, or other bill notice. Remove unsupported lines and add any missing required obligations.

This verification step is what turns a rough budget into an operating control. If a line belongs in the baseline, you should be able to show why it exists and when it recurs. That matters later when cash tightens, because a verified list is easier to defend than a vague memory of what "usually" gets paid. It also exposes hidden required costs, such as annual tools or periodic premiums, before they hit in the same month as a late receivable.

Step 3#

Stress-test this baseline for timing shocks, not just lower sales. Payments may arrive late, a planned project may pause before payment clears, expected income may be delayed, or a new urgent expense may land in the same month.

For each scenario, ask what still gets paid and what tightens first. If cleared cash drops below your verified threshold in your tracker, start your tighten sequence immediately: pause optional, delay can-delay, and protect must-pay.

If your income is irregular, use last year's income divided by 12 as a rough monthly comparison instead of leaning on one strong month.

Before you move on, keep three items together: your survival number, your ranked cut list, and your prewritten tighten sequence. You will use all three when you split cleared cash and set payment controls. The ranked cut list matters because a slow-pay month is not the time to debate every line from scratch. A short, pre-decided order helps you act faster and keeps essentials protected while you verify incoming payments and follow up on what is due.

Need the full breakdown? Read How to Create a 5-Year Financial Plan.

Split Your Cash So Gross Receipts Do Not Mislead You#

Treat every payment as unallocated until you split it. Gross receipts are not fully spendable cash because they can still include tax obligations, ordinary business costs, and money you may want to hold as a buffer.

Step 1#

When a payment clears, use one fixed allocation order consistently, such as tax, operating, reserve, then discretionary. Record each split promptly, ideally the same day.

Use separate accounts or clearly named categories in a spreadsheet or accounting tool. Record the received date, client, invoice number, gross amount, and each bucket transfer. If you cannot explain the last payment split in under a minute, the process is too loose.

A fixed order does more than organize money. It reduces re-deciding what to do with each receipt and helps protect tax and core operating needs before other spending.

Step 2#

Label cash before you spend any of it. Put tax first, since freelancer income is typically paid without automatic withholding and may require estimated payments during the year.

Use a tax review trigger in your tracker, with the current threshold pending tax-record or advisor verification, so you revisit allocations when income shifts. Then fund operating using your survival-number floor, move money to reserve, and treat only the remainder as discretionary.

The key discipline here is timing and records. Detailed tracking makes it easier to confirm what is truly available to spend. When the split is delayed, it becomes easier to cover routine expenses with funds that were meant for taxes or your buffer.

| Cash state | Practical signals | Main risk | Next action |

|---|---|---|---|

| Unallocated cash | One balance, no bucket labels, new receipt not logged | You spend tax or reserve money as if it were free cash | Split and label the payment promptly |

| Partly allocated cash | Some transfers done, but no clean invoice or tracker link | Month-end review breaks because payment purpose is unclear | Update the tracker with date, client, invoice, and bucket amounts |

| Allocated cash | Every receipt has labeled transfers and matching records | Lower confusion and faster reconciliation | Reconcile to bank activity and near-term obligations |

Step 3#

Keep this as simple as you can reconcile every month. Use only the number of accounts or categories you can actually maintain.

The common failure mode is too many buckets with weak records behind them. If that starts happening, reduce categories, keep the same allocation order, and preserve the same monthly evidence set: bank activity, invoice record, and transfer confirmation.

Simple and repeatable beats precise but fragile. A smaller set of clean buckets will protect you better than an elaborate system that stops being updated when work gets busy. The real standard is whether you can trace a receipt from invoice to cleared cash to allocation without guessing.

Set Payment Terms Before Work Starts#

Set the rule before kickoff: no work starts until payment terms are in writing and agreed. This is where you prevent avoidable slow-pay and scope disputes.

| Term element | What to define | Timing note |

|---|---|---|

| Scope definition | What is included, what is excluded, and revision limits | Before work begins |

| Billing trigger | Prepayment, funded milestone, recurring invoice, or completion trigger | For fixed-price milestone work, start only when the first milestone is funded |

| Due-date language | State the term explicitly | Net 30 means payment due 30 days after invoice receipt |

| Change-order approval path | No added work moves forward until both sides approve the change in writing | Before added work moves forward |

| Overdue escalation path | Reminder timing, pause point, and who receives overdue notices | Before kickoff |

Step 1#

Build a simple written terms stack before any work begins:

- Scope definition: what is included, what is excluded, and revision limits.

- Billing trigger: prepayment, funded milestone, recurring invoice, or completion trigger. For fixed-price milestone work, start only when the first milestone is funded.

- Due-date language: state the term explicitly, for example, Net 30 means payment due 30 days after invoice receipt.

- Change-order approval path: no added work moves forward until both sides approve the change in writing.

- Overdue escalation path: reminder timing, pause point, and who receives overdue notices.

Before kickoff, confirm you have one written record and one named approver. If details live across several messages, pull them into one usable record before work begins. The easier it is for both sides to identify the approved scope and the payment trigger, the harder it is for confusion to turn into a payment delay later.

| Billing structure | Cashflow effect | Dispute exposure | Best-fit client profile |

|---|---|---|---|

| Upfront deposit | Front-loads some payment before delivery | Lower when scope and delivery terms are clear | New clients, custom scopes, higher-risk projects |

| Milestone-based | Stages payment across funded milestones | Lower when milestones and approval criteria are specific | Fixed-price work with defined stages |

| Recurring retainer | Uses recurring invoices on a set cadence | Depends on how monthly scope and overages are defined | Ongoing support with reserved monthly time |

| Completion-based | Back-loads payment until delivery/acceptance | Higher when acceptance and payment timing are vague | Established clients, small tightly scoped work |

Step 2#

Treat pre-kickoff friction as a risk signal. Resistance to written terms, no clear internal approver, or pushback on written change approvals does not prove bad faith, but it does mean you should tighten protections before you say yes.

If you operate in New York, written terms matter even more. NYC requires a written contract for freelance work worth $800 or more, including agreements totaling $800 within a 120-day period. Under NY GBS §1411, if payment timing is not specified, the fallback is payment within 30 days after completion.

In practice, this is where you decide whether the project deserves standard terms or tighter ones. If the client is organized, approvals are clear, and billing references are known, a normal cadence may be enough. If billing details are vague before kickoff, they rarely become clearer once work is in motion.

Step 3#

Make a pre-kickoff decision based on what is actually documented:

- Proceed as scoped when terms are documented, billing triggers are objective, and an approver is named.

- Proceed with tighter protections when risk is manageable: require prepayment or funded milestones, narrow scope, or shorten invoice cycles.

- Decline when payment timing, change approvals, or overdue handling cannot be documented clearly.

The habit that matters is deciding before delivery starts, not after exposure has already grown. A clean no at the start is usually cheaper than trying to recover payment from unclear terms later.

We covered this in detail in How to Conduct a Yearly Financial Review for Your Freelance Business.

Standardize scope, deposit language, and late-payment terms before kickoff with a reusable template: Generate a freelance contract.

Choose Payment Methods by Risk, Not Convenience#

Choose your payment method before kickoff, and prefer the one you can collect reliably and document clearly if something goes wrong. Late payment and non-payment are common freelancer risks, so convenience is not enough.

Step 1#

Compare payment rails by operational risk before you send the first invoice: fees, processing speed, security, and professional fit. Fee structure alone can materially change your net. For example, on $100,000 revenue, 3% vs 0.5% is a $2,500 gap.

| Payment rail | Settlement predictability | Fee visibility | Dispute burden | Currency exposure | Record quality |

|---|---|---|---|---|---|

| Card via payment processor | Depends on processor payout settings | Usually disclosed in processor pricing | Dispute flow follows processor rules | Varies by provider and currency setup | Can be strong when invoice and payment records stay linked |

| Bank transfer (ACH/wire) | Common for higher-value business payments, but often slower than newer options | Typically visible in transfer details | Follow-up depends on bank process and documentation | Varies by bank and transfer corridor | Can be strong when invoice and transfer references are retained |

| Platform wallet / processor balance | Depends on platform payout options | Fees can vary by payout route and conversion settings | Dispute and support options vary by platform | Conversion handling varies by platform | Good when platform history and payout records are preserved |

| P2P app | Built for person-to-person transfers; business fit varies | Terms and fees vary by app | Escalation paths vary by app | Cross-border support varies by app | May require extra documentation for business records |

If you work cross-border, review fee terms, currency handling, and recordkeeping before kickoff. Speed matters, but a method that is hard to reconcile later can create avoidable follow-up work.

Step 2#

Pair the rail with payment controls at the same time. The method does not protect you by itself. The method, billing cadence, and acceptance checkpoints work together.

| Project shape | Use these controls |

|---|---|

| Lower risk, clear scope, clear acceptance point | Set an upfront commitment or staged invoices, and tie payment to defined deliverables |

| Higher risk, changing scope, or multi-approver client | Increase upfront commitment, shorten milestone cadence, and require written acceptance at each checkpoint |

| Vague or likely-to-expand work | Avoid informal rails; use a business-focused method and smaller billing stages to limit unpaid exposure |

A safe rail with loose controls can still lead to slow pay. A stronger combination makes the client's path clear: how to pay, when to pay, and what event triggers payment. It also leaves you able to show the chain from scope to delivery to invoice to receipt later if needed.

Step 3#

Keep a traceable evidence trail for every project so you can prove the payment chain without relying on memory:

- Invoice issuance proof, such as a sent record or timestamped email

- A clear client approval owner, where possible

- Dated delivery acceptance notes for each milestone or completion trigger

- Written scope-change signoff before extra work proceeds, when practical

- Payment confirmation, such as a processor receipt, remittance email, or bank reference

When a payment question comes up, these records can matter more than recollection alone. If you can gather the full file in minutes, you are usually in a better position to resolve confusion before it becomes a stale dispute.

Step 4#

Use one decision rule: if a payment method weakens traceability or makes it harder to connect invoice, approval, delivery, and receipt, default to the safer method even if it is less convenient.

That rule helps when the tempting option is simply the one the client already uses casually. For business work, your standard should be proof and process, not ease alone.

Related reading: How to Create a Financial Plan for a Sabbatical.

Send Invoices in a Way That Prevents Excuses#

Many invoice delays trace back to process failures. Treat invoicing as a controlled sequence, not a one-time send. Late-payment excuses are common and predictable.

A 2019 CPA article on small-business late payments described excuses as "numerous and well used" and reported that over half of invoices from Xero small-business subscribers were paid late. Use that as a risk signal, not a 2026 benchmark. You can reduce delays by removing avoidable friction before you send.

| Common excuse | What it usually means | Prevention control |

|---|---|---|

| "We never received it" | Routing failure or wrong contact | Send to the confirmed billing inbox, copy the project owner, and request written receipt confirmation |

| "We need the PO or reference" | Missing internal processing field | Include the required PO, vendor ID, project code, or reference on the invoice and, if needed, in the email subject |

| "We are waiting on approval" | No clear approver or vague milestone label | Confirm the approver before sending and match milestone wording to the signed agreement |

| "We were not sure how to pay" | Payment instructions were incomplete or scattered | Include one clear payment-instruction block and share sensitive details only through official, secure websites |

Step 1 Validate billing identity#

Confirm who can route and approve your invoice before you send it. Get the exact billing entity name, billing email, portal requirements, and required references up front.

Tie your pre-send check to the signed agreement. The contracting-party name, line-item wording, and milestone labels should match what was agreed. If an approver who was not part of delivery cannot map each line item to the agreement quickly, revise before sending.

This step is easy to rush once the work is done, but it helps prevent avoidable rejection. A correct invoice sent to the wrong entity or missing the required reference can sit untouched while you assume the client is deciding whether to pay.

Step 2 Align invoice terms to contract terms#

Your invoice should reflect agreed terms, not renegotiate them. Keep bill date, due date, milestone trigger, currency, and payment method aligned with the contract.

Before sending, check three fields side by side: contract milestone label, invoice line-item wording, and required client reference. When those match, approval friction can drop and follow-up stays anchored to a clear record.

A useful habit is to run this check before you draft the email body, not after. That keeps the invoice itself clean and reduces the chance that a clarifying explanation in email ends up carrying information that should have appeared on the invoice.

Step 3 Run a fixed send and confirm sequence#

Use one send sequence every cycle. Send to the confirmed billing contact, copy the project owner, state the due date and payment instructions, then get written confirmation that the invoice was received and routed correctly.

Keep one traceable thread with send proof, receipt confirmation, approver details if shared, reminders, and payment-status updates. If sensitive payment details are needed, direct clients to your established secure channel or official secure websites instead of scattering details across messages.

This kind of consistent thread also makes follow-up easier. You are not rebuilding history from separate messages when the due date passes. Every reminder can point back to the same invoice, the same terms, and the same confirmation trail.

Step 4 Close only when funds are posted#

Do not close an invoice on verbal confirmation alone. Mark it paid only when funds are posted and matched to invoice amount, date, and reference.

Store a simple evidence pack for each invoice: sent record, confirmations, reminders, and posted-payment proof in one place. If full payment cannot clear immediately, consider moving to a written installment plan with dated amounts and due dates in the same thread.

The operational point is to separate reassurance from finality. A client saying payment is in process may be useful, but it does not change your cash position until the money arrives and can be matched.

Build Reserves While You Still Reduce Debt#

Even with good invoicing, timing gaps can still happen. The practical rule is simple: build cash resilience first, then accelerate debt payoff only after your must-pay baseline is covered.

Without savings, even a small shock can turn into debt with longer effects. Reserve-first sequencing can reduce the risk of missed essentials, minimum debt payments, and tax obligations when client payments slow down.

Step 1 Set a must-pay baseline before you chase payoff speed#

Start with minimum monthly obligations, not your full lifestyle budget. Include only what must be paid to keep your household and work running: personal essentials, core business costs required to deliver and invoice, minimum debt payments, and tax cash needed for upcoming estimated payments.

If your income is irregular, estimate monthly income from last year, then set the baseline around current required bills.

Verification point: if you cannot name one baseline number and the bills inside it, do not speed up debt payoff yet. Extra debt payments feel productive, but they are not protective if next month's essentials still depend on a client paying exactly on time.

Step 2 Build liquidity in two stages#

Build a quick-access buffer first, then a broader emergency reserve. The first layer is meant to absorb late payments or short billing months without missed obligations.

Keep this first buffer in cash that is easy to access, but not so easy that you spend it casually. A separate savings account can work. At higher balances, account protection may matter: FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category, and NCUA share insurance generally covers individual accounts up to $250,000 at federally insured credit unions.

After the quick-access layer is stable, keep building toward a larger emergency reserve. A common benchmark is 3-6 months of essential expenses, used as a planning range, not a legal rule.

The distinction between the two layers helps in practice. The first layer is about timing. The broader reserve is about resilience. Mixing the purpose of both can lead to either underfunding near-term protection or treating long-term reserves as if they are available for routine monthly drift.

Step 3 Match surplus allocation to current cash conditions#

After minimums and your first liquid buffer are intact, decide each month whether surplus should lean toward reserves or debt.

| Current state | Recommended emphasis | Risk this controls |

|---|---|---|

| Income stable, receivables current | Payoff-heavy | Cuts long-run borrowing cost, especially on higher-interest debt |

| Income volatile, obligations still covered | Balanced | Keeps debt moving while preserving flexibility if next month is weaker |

| Receivables delayed or uncertain | Reserve-heavy | Lowers risk of missed minimums, tax shortfalls, and new revolving debt |

When you do accelerate debt reduction, both highest-interest-first and snowball are valid methods. Highest-interest-first is usually cheaper over time. Snowball can improve momentum but may cost more overall.

Use the table as a monthly decision filter, not a one-time personality choice. The same person may need a payoff-heavy month after a stable period and a reserve-heavy month when invoices age or expected work slips.

Step 4 Run a monthly pass/fail control loop before anything discretionary#

At month-end, mark the month as a pass only if all of the following are true:

- minimum debt payments were made on time

- reserve cash increased or held at target

- no essentials were funded with new revolving debt

- next month's must-pay list includes the next tax due date when applicable

If any item fails, fix that first. Freeze discretionary spend, pause accelerated payoff, and direct the next surplus to the failed item until restored. Keep a short monthly note with reserve balance, debt minimum status, next estimated-tax date, and overdue invoices so the tradeoffs stay explicit.

That short note matters because it keeps the reason for your decision visible. Without it, it is easy to remember only that you "couldn't make extra progress" and forget whether the actual cause was slow pay, reserve weakness, or missed tax preparation.

Handle Slow-Pay and No-Pay Months With a Fixed Escalation Sequence#

When an invoice goes overdue, follow one prewritten escalation path so you do not improvise while cash is tightening.

Slow pay is common, but patterns are not uniform. Recent reporting says most freelancers wait more than 30 days to get paid, with an average delay of 37-42 days after invoice submission, and about one-third report delays beyond 60 days. The same reporting says timelines vary by region, industry, platform, and client type. Keep one fixed sequence, and verify jurisdiction-specific terms and protections before each escalation step.

Step 1 Verify the file before you escalate#

Before you send an escalation message, make sure the file is complete: signed agreement or SOW, invoice, delivery or approval record, and current ledger status.

Treat this as a gate. Verify the exact amount due, due date, late-payment or pause-work language, and any jurisdiction-specific constraints that apply. If any of those are unclear or inconsistent, fix that first.

Verification point: you can show, in one place, the agreement, invoice number, delivery or approval proof, prior reminders, and current balance due.

This gate helps avoid two failure modes: escalating too early on an invoice that was not routed correctly, and escalating on a file with missing proof. In both cases, the problem can get harder to solve once emotions rise and the record is unclear.

Step 2 Send the next message that matches the trigger#

Every outreach should include five things:

- amount due

- due status

- required next step

- verified deadline or deadline pending source-record verification

- stated consequence if unresolved

Keep the tone neutral and specific. Do not send vague check-ins, and do not threaten actions you have not verified.

| Trigger condition | Your action | Message objective | Evidence to retain |

|---|---|---|---|

| Invoice is due or just past due with no payment confirmation | Send a concise reminder | Confirm invoice receipt and request payment or a status update | Sent message, invoice copy, delivery or approval proof, receipt confirmation if available |

| Payment still not confirmed after reminder, or client is nonresponsive | Send a formal overdue notice tied to contract terms | Get a written payment date, payment confirmation, or documented dispute | Notice sent, contract clause, prior reminder, ledger status |

| Invoice remains unresolved while work is active | Pause new scope or future deliverables if your agreement allows it | Stop adding unpaid exposure and force a decision point | Pause notice, scope status, outstanding deliverables list |

| No resolution after pause and you have verified the next valid route | Move to the next formal step allowed by your agreement and jurisdiction | Formalize recovery or dispute handling | Full evidence pack, outreach timeline, approvals, delivery proof |

Operator rule: each new stage should reference the prior stage so the trail stays auditable. That way, every message reads as part of one controlled sequence rather than a fresh argument.

Step 3 Freeze exposure while receivables are unstable#

If a client is late, stop adding unsecured work. Pause new scope, shorten billing intervals, and tighten payment checkpoints before the next deliverable.

Where timing risk is the issue, the payment method can affect delay. The cited comparison reports direct bank transfer with pre-agreed terms as the fastest method, at 7-10 days. It reports platform escrow with dispute periods as the slowest, at 30-60+ days, with platform-mediated payments averaging 23-28 days longer than direct payments. Use that as a risk signal, not a guarantee.

Freezing exposure can be the hardest step, especially with clients you want to keep. But the risk is not only non-payment on the current invoice. It is the growth of unpaid work attached to the same unresolved process.

Step 4 Use a prewritten bridge rule only against confirmed receivables#

If a slow-pay month starts to pressure essentials, use a prewritten bridge rule instead of deciding under stress.

A practical rule is to use short-term bridge debt only for must-pay baseline expenses. Use it only when a receivable is confirmed, and only when the client has acknowledged the invoice without an active scope dispute. If those checks are missing, treat the receivable as uncertain and cut exposure first.

The value of a bridge rule is discipline. It prevents you from using debt to preserve optional spending or to extend unclear projects. If borrowing enters the picture at all, it should be tied to a documented receivable and a narrow must-pay purpose.

Run a Monthly Cashflow Audit and Evidence Pack#

Run one repeatable month-end close so you know what is true before you make next-month decisions. Use a hard rule: if a number cannot be matched to records, or a mismatch is not logged with a clear owner and follow-up date, the month is not closed.

Loose records hide risk. A small-business study found that inadequate record-keeping strategies were associated with businesses that struggle, so treat your close as evidence-based, not memory-based.

Step 1 Reconcile every invoice and payment record#

Use the same fields every month, for example: invoice number, client entity, invoice amount and currency, payment receipt date and amount, ledger posting date, ledger account, agreed payment terms, and payment method category.

Apply a strict exception rule. Any mismatch goes into the exception log before you move on, with a clear owner and follow-up date. By the end, every invoice is either fully matched or tied to one logged exception.

Do not rely on bank balance alone. Cash can look fine while the ledger is wrong, a payment is misapplied, or an overdue invoice is still marked current. Reconciliation is the step that catches those quiet breaks before they distort your next budget or reserve decision.

Step 2 Assess trend signals and attach a response#

The close should drive action, not just reporting. Pair each trend with a response so next month starts from an explicit decision.

| Metric you track monthly | Trend you see | What you do next |

|---|---|---|

| Overdue amount | Flat or falling | Hold course and keep your current follow-up cadence |

| Overdue amount | Rising | Tighten terms for new work and escalate collections on open invoices |

| Average days past payment terms | Flat or improving | Hold course if exceptions are being resolved |

| Average days past payment terms | Worsening | Shorten billing intervals and confirm approver details earlier |

| Reserve coverage vs your target | Stable or improving | Hold discretionary spend and continue reserve building |

| Reserve coverage vs your target | Falling | Reduce discretionary spend and postpone optional outflows |

If overdue amounts rise while reserve coverage falls in the same month, take both actions immediately: escalate collections and reduce discretionary spend. That combination can be a warning sign that timing stress is moving from receivables into your cash buffer.

Step 3 Store one audit-ready evidence pack#

Keep one folder per month with a consistent structure, for example:

| Folder | What it holds |

|---|---|

| 01_Signed-Terms | Signed terms |

| 02_Invoices-and-Delivery | Invoice trail and delivery records |

| 03_Payment-Proof | Payment proof |

| 04_Exception-Log | Mismatches with owner and follow-up date |

| 05_Disputes-and-Concessions | Disputes and concessions |

| 06_Close-Summary | Close summary and action note |

Use one naming convention across files, such as YYYY-MM_Client_InvoiceNumber_DocType, so you can move quickly from signed terms to invoice trail to payment proof to dispute notes.

You can apply the same completeness discipline used in formal reporting. The 2025 Form 5500 instructions emphasize complete filings with required schedules and attachments, and entries that pass screening to be received. For your close, that means complete, internally consistent records before you treat the month as final. The folder structure is there to reduce search time and make future review possible without rebuilding context.

Step 4 Close the month only after a verified stress note and action#

Run stress review only after reconciliation is complete. In your close summary, keep the stress scenario pending finance-record verification until the records support it.

Then log one concrete corrective action before closing the month, with owner and timing. The month stays open until that action note is recorded.

This last step is what turns a close into a control loop. Instead of ending with "everything seems mostly fine," you end with one verified concern and one next action grounded in the records you just checked.

For a step-by-step walkthrough, see Freelance Financial Management That Protects Cashflow First.

Common Mistakes That Break Freelancer Safety Nets#

Most safety nets fail through drift, not one dramatic event. The good news is that drift usually shows up early if you know what to watch for.

| Mistake | What it causes | What to do this week |

|---|---|---|

| Not segregating tax cash | Spendable cash looks higher than it is, and estimated-tax pressure shows up late | Create a tax transfer rule with the allocation range pending advisor or finance-record verification, and log each transfer when client money arrives |

| Mixing business and personal money | You cannot tell whether shortfalls come from slow pay, business costs, or personal spending | Route all client receipts and business expenses through a dedicated business account |

| Letting bookkeeping slip | Late invoices, unclear aging, and weak month-end decisions | Set one recurring bookkeeping block and do not close the month until exceptions are logged |

| Planning as if income is smooth | You overcommit in strong months and react too late in weak months | Map expected income timing and irregular expenses across the next 12 months |

| Skipping annual tax and deadline planning | Missed payment dates, rushed filings, and avoidable penalties | Put IRS Publication 509 dates and your own filing or renewal dates on one calendar |

Step 1 Segregate tax cash early#

Treating gross receipts as fully usable cash is a fast way to create surprise pressure. The IRS says taxes are pay-as-you-go, and individuals generally need estimated payments if they expect to owe $1,000 or more.

The early signal is simple: client money lands, but there is no matching tax transfer or log entry. Fix it now by moving each receipt into a separate tax bucket and recording the transfer. If your allocation is not verified yet, mark the allocation range as pending advisor or finance-record verification before using it to size transfers. Also note that an estimated-tax penalty can still apply even if you expect a refund when you file.

What breaks people here is usually not ignorance that taxes exist. It is the assumption that one strong month leaves enough room to deal with taxes later. A transfer rule removes that guesswork.

Step 2 Separate business and personal accounts#

If you mix business and personal transactions, your cash picture stops being reliable. The SBA says to open a business bank account as soon as you start accepting or spending money as a business, and that separation supports compliance and protection.

The early signal is that you cannot explain a low balance without digging through mixed charges. This week, route new client receipts and business bills through a dedicated business account, and label owner draws clearly instead of blending personal spending into operations.

That separation also improves your month-end close. When the account itself reflects the business flow, it is easier to identify slow-pay pressure, unusual costs, or missing transfers without untangling personal purchases first.

Step 3 Restore bookkeeping cadence before month-end#

Bookkeeping breaks when records lag reality, not because tools are imperfect. SBA guidance calls for proper bookkeeping, and IRS recordkeeping guidance ties good records to monitoring business progress and preparing financial statements.

Watch for uncategorized transactions piling up, unclear invoice status, or the same exceptions rolling forward month after month. A practical fix is one recurring bookkeeping block (weekly for many freelancers) for categorization, invoice updates, and paid, due, and overdue status. By month-end, you should be able to trace each open invoice to terms, delivery evidence, and payment status.

For many freelancers, a weekly cadence helps because month-end cleanup is harder when the whole month stayed fuzzy. Short, regular maintenance reduces the number of judgment calls you have to make later.

Step 4 Plan for variable income, not steady-paycheck assumptions#

Planning from your best month is a common mistake. When weaker months arrive, routine timing gaps turn into cashflow stress. The CFPB annual planning tool notes that variable income and expenses make budgeting harder.

The early signal is that normal slow-pay timing creates pressure even without unusual costs. Fix it with a 12-month plan that maps income timing and irregular expenses, then check whether fixed obligations still hold if an expected payment moves later.

This does not require a perfect forecast. It requires a more honest one. When you place irregular bills and uneven receipts on the same timeline, you can see whether the plan depends on everything arriving on schedule.

Step 5 Put annual deadlines on one calendar#

Deadline misses often come from fragmented planning, not lack of effort. IRS Publication 509 describes a tax calendar as a 12-month calendar divided into quarters and frames it as a way to file or pay on time and avoid penalties.

| Estimated-tax period | Due date | Note |

|---|---|---|

| Jan. 1-March 31 | April 15 | Verify current dates against Publication 509 and your own facts before relying on them |

| April 1-May 31 | June 15 | Verify current dates against Publication 509 and your own facts before relying on them |

| June 1-Aug. 31 | Sept. 15 | Verify current dates against Publication 509 and your own facts before relying on them |

| Sept. 1-Dec. 31 | Jan. 15 of the following year | Verify current dates against Publication 509 and your own facts before relying on them |

For many individual taxpayers, IRS FAQ estimated-tax periods are listed that way. Verify current dates against Publication 509 and your own facts before relying on them.

Put business renewals, insurance reviews, and any filing-related dates in the same view you use for tax planning if those obligations affect your cash timing. The real win is not the calendar itself. It is fewer surprises landing in the same month.

Monthly prevention checklist. Use the same review each month so the small breaks show up before they turn into cash stress.

- Confirm every client receipt has a matching tax transfer or a logged reason it does not.

- Review your business account for mixed personal charges and clear or relabel them.

- Update invoice status, overdue days, and exception owners.

- Compare the next 30-60 days of fixed outflows against expected payment timing.

- Check your tax calendar and annual planning sheet for any deadline inside the next 45 days.

Related: How to Build a Freelance Financial Model That Protects Cash Flow.

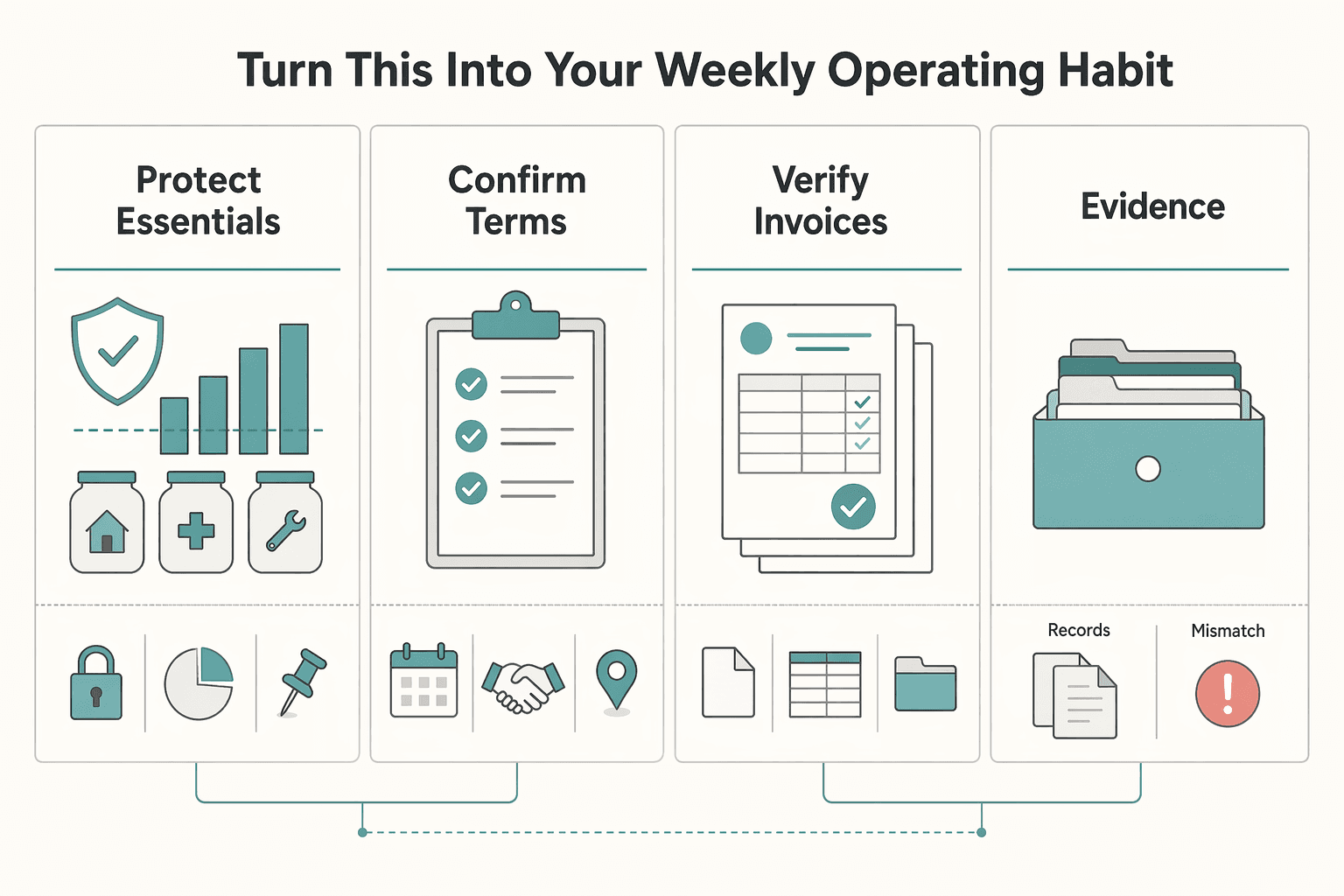

Turn This Into Your Weekly Operating Habit#

Run this on two rhythms: a short weekly control check, then a separate month-end close. That keeps timing risk visible before it turns into a cash problem.

Keep one working view with your survival number, cash buckets, open invoices, and next tax obligations. When those items sit in one place, your weekly review becomes a control check rather than a scavenger hunt.

| Habit | When | Failure signal | Immediate action |

|---|---|---|---|

| Protect essentials floor and buckets | Weekly | Cash is nearing your survival number, or tax funds were used for other spending | Pause optional spend and route new receipts to tax and operating buckets first |

| Confirm terms before kickoff | Each new engagement; review weekly for new work | Work started with unclear scope, due date, deposit, or payment trigger | Treat it as active risk until terms are documented and stored with the client record |

| Verify invoices and run follow-up sequence | Weekly | Missing approver or receipt confirmation, invoice errors, or overdue invoices with no next step | Correct, resend if needed, confirm receipt, identify approver, then move through your escalation sequence |

| Reconcile records and evidence pack | Month-end | Payments do not match invoices, documents are missing, or account activity is unexplained | Match payments to invoices, collect supporting records, and investigate unmatched or suspicious entries |

Weekly cadence#

Pick the same day each week and run a short control check: essentials first, then terms, then receivables.

Compare available cash to your survival number, and confirm that your tax bucket is intact. If you are self-employed, estimated tax generally applies and taxes are due as income is earned. Underpaying a period can trigger a penalty for that period.

For new work, get terms in writing before kickoff whenever possible, and store them with billing records. For every open invoice, keep billed date, due date, status, and next action filled in. If any field is blank, treat it as active risk.

The weekly check should end with a short decision list, not just observations. If cash is tight, note what gets paused. If an invoice is overdue, note the next outreach. If a new project is missing terms, note whether it proceeds, tightens, or waits.

Month-end close#

Run monthly close separately from weekly checks. Match payments to invoices, compare actual spending to your essentials floor, and update reserve progress. If your emergency fund is still small, keep contributing. Even small amounts improve resilience.

Then clean up the evidence pack. Invoices, receipts, deposit records, and account activity should support your books and tax reporting. If something is unexplained or undocumented, resolve it now instead of carrying it into next month.

Once this cadence is stable, you can optimize payment controls further, including card-policy decisions in Should Your Freelance Business Accept Credit Cards?.

When you are ready to tighten cashflow operations, evaluate dedicated receiving details and status tracking for inbound bank transfers where supported: Explore Virtual Accounts.

Frequently Asked Questions

How much emergency fund should a freelancer build first if income is irregular?

Build in phases, and size phase one from your survival number rather than a universal month target. That first layer is there to protect must-pay costs from timing shocks when invoices land late. Review recent bank activity, then list non-negotiable costs, including health insurance premiums, self-employment taxes, and business expenses, before you set the first reserve target.

What makes freelancer finances riskier than salaried finances with tax withholding?

The core risk is timing plus self-allocation. Salaried pay is usually predictable, while freelance receipts arrive without automatic withholding, so it is easy to overspend if taxes, insurance, and reserves are not moved into cash buckets first. Transfer each client receipt into your cash buckets as it lands, with the current allocation range pending advisor or finance-record verification before use.

Is a financial safety net just savings, or also better payment terms and invoice controls?

It is both. Savings absorb shocks, and basic invoice controls can help you catch delays earlier. Pair each reserve contribution with one receivables check, such as confirming invoice status, sending on the agreed trigger, or tightening terms before work starts.

What should I do first in a slow-pay month to avoid debt spirals on credit card or personal loan?

Protect essentials first, verify receivables second, and borrow last. Timing pressure builds fast when taxes and insurance stay regular but client payments move later. Compare available cash to your survival number, pause lower-priority spending, and review each open invoice for sent date, due date, and current status before moving through your escalation sequence.

When should I prioritize debt payoff over expanding my emergency fund?

Choose the option that best protects your next required obligations. If payment timing is unstable, aggressive payoff may raise short-term financial risk even if balances decline. Decide during monthly close using real due dates, open invoices, cash buckets, and upcoming required costs, not a fixed rule.

How do deposit requirement and late-payment clause terms reduce cashflow risk in practice?

They do not guarantee payment, but they can clarify expectations and support earlier follow-up in your escalation sequence. Keep terms, invoice dates, due dates, delivery proof, and receipt confirmation in your evidence pack, and verify enforceability from jurisdiction-specific source records before relying on fee or remedy language.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumer.gov/your-money/making-budgettrusted

- consumer.gov/system/files/consumer_gov/pdf/1041A_BudgetWo...trusted

- consumerfinance.gov/an-essential-guide-to-building-an-emergency-...trusted

- consumerfinance.gov/consumer-tools/educator-tools/youth-financia...trusted

- dol.gov/sites/dolgov/files/ebsa/employers-and-advise...trusted

- federalreserve.gov/publications/2025-economic-well-being-of-us-...trusted

- files.consumerfinance.gov/f/documents/cfpb_building_block_activities_c...trusted

- irs.gov/payments/underpayment-of-estimated-tax-by-in...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

Portugal NHR Tax Regime Decisions for 2026 Freelancers

---

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.