Quick Answer

Start with a go/no-go call: if you can document eligibility, keep records consistently, and explain your right-to-work status, the france micro-entrepreneur guide points to filing in sequence and operating with monthly controls. Build one evidence folder with your decision note, registration confirmations, and early declarations. Set up invoicing with stable business details, keep your livre des recettes current, and pause for professional review when residency facts, visa status, or VAT treatment are unclear.

Start Here if You Want Low-Stress Compliance in France#

Low-stress compliance starts with one question: does the Micro-entrepreneur regime match your real setup right now? It is often presented as a simplified option for lower-revenue activity, so use it as a fit test, not a shortcut.

If you are freelancing or consulting, the practical target is simple: make a clear go or no-go call, register in the right sequence, and keep records clean from the start so you can explain your filing path if asked.

Before registration, write a one-page decision note:

- What you do

- Where you expect to work

- Whether your current status supports legal self-employment in France

Keep this note dated and editable. If your client mix, work location, or immigration status changes, update the same page instead of creating scattered versions. That gives you one reference point when you need to explain why you filed the way you did.

For non-EU applicants, this is a hard checkpoint. If your right-to-work path is not clear, pause and get professional advice before filing.

Treat launch as a sequence, not one form. Use this cadence:

- Step 1: make the go or no-go decision

- Step 2: set the order, with structure first, then visa or permit path if relevant, then registration

- Step 3: organize core records in one place

- Step 4: run a monthly review so documents and filings stay aligned

A calm first quarter usually comes down to one habit: each step should leave a trace you can find quickly later. Save your decision note, registration confirmations, and early declarations in one location from the start. Fast retrieval matters as much as technical correctness when someone asks for proof.

Talk to a professional now if any of these apply.

- You cannot clearly explain your legal right-to-work position in France

- You are non-EU and still deciding between visa or permit routes

- Your records are fragmented and you cannot quickly produce a clean evidence trail

If none of these red flags apply, move forward with discipline. You do not need perfect paperwork on day one. You need a setup you can run calmly and defend later.

The Core Terms You Need Before Any Decision#

Treat terminology as a control point before you file. In this context, auto-entrepreneur and micro-entrepreneur refer to the same regime, and it helps to keep this terminology work separate from tax-residency analysis.

| Term | Meaning | Detail |

|---|---|---|

| Auto-entrepreneur | Used here as the same regime as micro-entrepreneur | Keep terminology consistent in your records |

| Micro-entreprise | Simplified form for an individual entrepreneur, with no legal distinction between you and the business | Keep it separate from tax-residency analysis |

| Activity label | Pick the category that matches your real work | Commercial, artisanal, or liberal |

| Declarations | Choose monthly or quarterly reporting during registration | Selected during registration |

| Revenue book | Keep it from the start and record all income received | Required record; may be requested in an audit |

Why this matters in practice: terminology drift creates avoidable friction. If your registration text uses one term and your own notes use another without context, later checks can become slower and harder to reconcile. Keep a short definitions page in your records and use those same terms in your templates.

Keep tax residency analysis on its own track. It connects to how you operate, but terminology choices alone do not resolve residency questions.

When you review your file each month, ask two separate questions:

- Is my business activity still described correctly in my registration records?

- Do I need a separate residency check?

Separating those questions avoids a common mistake: treating one completed admin step as proof that every related compliance topic is solved. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

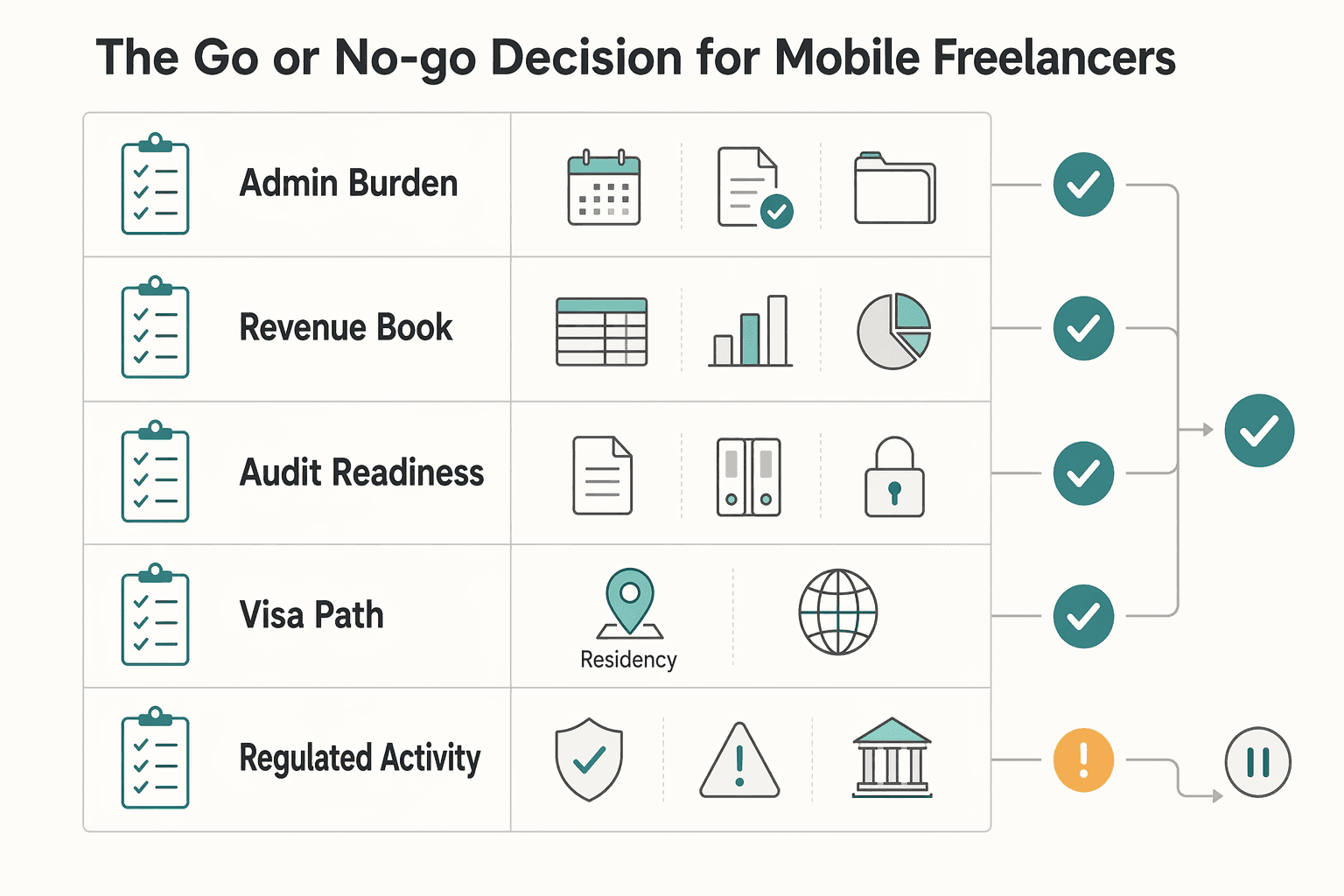

The Go or No-Go Decision for Mobile Freelancers#

Go only if you can execute the basics from day one. If not, pause and compare options before registering. Micro-entrepreneur status is simpler, not consequence-free, and it is easier to manage when your records are consistent and review-ready.

Use this one-page scorecard.

| Decision lens | Go now | Pause and review first |

|---|---|---|

| Admin burden | You can keep ongoing records consistently | You are already likely to fall behind on core admin |

| Revenue book readiness | Your revenue book process is ready from day one | You do not yet have a reliable way to record all income |

| Audit readiness | You can provide required records if requested | You would be backfilling evidence under pressure |

| Visa path (non-European) | Your business visa path is clear before filing | Your visa path is still unclear |

| Regulated activity checks | You have the required qualification or proof of experience | You still need qualification or proof, which can block registration |

Do not use the scorecard as a vague reflection tool. Use it to set a decision date and an action path. If most of your signals sit in the pause column, your next move is to resolve blockers before filing, not to register and fix problems later.

Keep one hard gate: if you cannot clearly explain your right-to-work and registration documents, pause and get professional review first.

Before filing, confirm these checkpoints:

- Your revenue book is ready and includes all income received from day one.

- If you are non-European, confirm your business visa path before filing.

- If your activity is regulated, confirm the required qualification or proof of experience first.

The practical contrast is simple. If your records are clean and your right-to-work facts are settled, filing is likely to be more straightforward. If your documents conflict or your status is unclear, pause for targeted fixes before filing.

A key risk is missing required evidence when registration or review asks for it. One reported case describes a founder stuck at registration for 9 months. Treat that as a cautionary example, not a standard timeline.

Eligibility and Immigration Checks Before Registration#

Do not file until your legal work basis and activity description are both documented and internally consistent.

| Topic | Article says | Before filing |

|---|---|---|

| Work-right and residence status | Confirm France-specific criteria for EU versus non-EU work rights, Profession Libérale eligibility, and self-employment residence-permit eligibility with the relevant authority | Treat these as unresolved until confirmed with the competent French authority and matching documents are held |

| Activity description | Use one declared activity description across registration, invoicing, and compliance records | Fix wording before submission if documents describe different activities |

| Cross-border SME scheme | VAT mechanism with a EUR 100 000 condition, prior notification flow, and 35-working-day process target | Do not use it as a proxy for work-right checks |

| OSS rules | VAT mechanics in the EUR 10 000 threshold context | Do not use them as a proxy for work-right checks |

Run two checks separately before you register: immigration and work authorization on one side, tax and VAT setup on the other. VAT schemes do not establish immigration eligibility.

For immigration, confirm France-specific criteria for EU versus non-EU work rights, Profession Libérale eligibility, and self-employment residence-permit eligibility with the competent French authority. Treat these as unresolved until you confirm them and hold matching documents.

For activity setup, use one declared activity description and keep it consistent across registration, invoicing, and compliance records. If your documents describe different activities, fix the wording before submission.

Do not use EU VAT process rules as a proxy for work-right checks. The cross-border SME scheme, including the EUR 100 000 condition, prior notification flow, and 35-working-day process target, is a VAT mechanism. OSS rules in the EUR 10 000 threshold context are also VAT mechanics, not immigration clearance.

Before filing, keep a dated verification packet with your core eligibility and filing documents, and archive the EU guidance you rely on. If anything conflicts with your declared activity or residency narrative, pause and resolve it first.

Make the packet operational, not decorative. Include short notes that explain what each document supports, for example work authorization, activity description, or VAT treatment context. That extra line can save time when you revisit the file after a gap.

If you find a conflict, handle it in this order:

- Stop new submissions until wording is aligned.

- Identify which document reflects your real current activity and status.

- Update other records to match that source before filing anything else.

This sequence helps keep one mismatch from spreading into invoices, declarations, and correspondence.

Picking the Right Activity Category Without Creating Future Rework#

Choose your activity category before you file, then keep that wording consistent across your registration records, invoices, and filings.

Start from what you actually sell now. In France, a professional activity can be carried out in your own name or through a company form. The micro-enterprise regime can cover artisanal, commercial, or liberal activities as a main or side activity. That flexibility helps, but vague wording creates rework later.

| Real work pattern | Usually cleaner starting label | Practical reporting effect |

|---|---|---|

| You mainly sell expertise, advisory, or execution time | Liberal professions | Service wording on invoices and declarations can be easier to keep aligned |

| You sell services plus products, bundles, or resale elements | Commercial activity | You may need tighter invoice wording so sales lines and filings describe one consistent core activity |

The main red flag is mixed or overly broad activity descriptions. When registration text, invoice language, and filing language drift apart, routine checks can become harder and cleanup work increases.

If your model is mixed, use one primary-activity rule and review it regularly before filing:

- Write a one-sentence primary activity statement based on your main revenue source.

- Check recent invoices against that statement for wording drift.

- If drift is recurring, update your internal description and get advice before the next filing cycle.

Another practical control is to maintain a short approved wording list for invoices. Keep one version for your core service description and one for any secondary line items that still fit your declared activity. Consistent wording lowers the chance that client-specific phrasing creates contradictions later.

Keep a simple checkpoint in your compliance folder: final registration activity text, invoice template language, and a dated review note. Also confirm category fit before you file, because exclusions to the micro-enterprise regime exist.

Registration Sequence and the Evidence Pack to Keep#

Sequence matters. Registering before your wording and core records are controlled creates avoidable cleanup.

| File item | Article detail | Use |

|---|---|---|

| Confirmation receipts | Save each confirmation receipt | Keep them in one registration evidence pack |

| Final activity declaration text | Keep your final activity declaration text | Reuse the exact wording across records |

| Tax and social registration confirmations | Store those confirmations with your main record | Keep them with the registration file |

| Master record | Single source for copy-paste fields | Use it for final activity wording and stable business details |

A practical order is this: confirm eligibility and business structure, complete registration, register for taxes and social security, then set up accounting. The micro-enterprise format is lighter on accounting, but tax and social obligations still apply and thresholds still matter.

Use this checklist:

- Confirm you are eligible for the regime you plan to use.

- Finalize one activity description and reuse that exact wording across registration and bookkeeping labels.

- Complete registration and save each confirmation receipt.

- Complete tax and social security registration and store those confirmations with your main record.

- Set up your accounting system and align recurring business details across your tools before routine invoicing.

Treat the master record as your single source for copy-paste fields. That includes your final activity wording and any stable business details used across documents. A single source sharply reduces keyboard mistakes in early invoices.

Build one registration evidence pack in a single place: confirmation receipts, your final activity declaration text, and tax/social registration confirmations. Use clear file names with date and purpose so checks are fast under pressure.

You can keep naming simple and durable, for example date plus document purpose. The point is not aesthetics. The point is that you can find the right proof in under a minute when a client, accountant, or authority asks for it.

A common failure mode is inconsistency. Before you send early invoices, verify recurring business details match your master record and accounting setup. If something is off, fix it before issuing.

The First 30 Days Setup That Prevents Most Mistakes#

The first 30 days set the tone for the rest of the year. Put simple controls in place now so you do not spend later months repairing avoidable drift.

Use this checklist:

- Start a simple income log in week one and record payments consistently as they come in.

- If your activity involves purchases, start tracking them early instead of waiting until volume rises.

- Use one invoice template with stable service descriptions and identifier fields copied from your master record.

- Run a monthly close routine: reconcile payments and invoices, archive invoices, and prepare totals you can use for tax and social declarations.

- Save month-end outputs together, including reconciliation notes, invoice archive, and any corrections, so checks are fast later.

Keep this distinction clear: tax and social obligations apply, but this checklist is an internal control routine for cleaner execution, not a claim about specific statutory monthly-close deadlines.

A practical month-one cadence helps:

- Early month: capture each payment and archive each invoice as it is issued.

- Mid-month: check whether invoice wording and identifier fields still match your master record.

- End of month: reconcile cash received, open invoices, and declaration totals.

This rhythm can reduce cleanup burden by avoiding reconstruction work months later from partial records.

Run an early eligibility check if your activity may be regulated. Missing qualification proof can block registration. For some manual regulated activities, a diploma or about 3 years of experience can be one qualification path. There are cases where founders were delayed for 9 months at the registration stage. If you are non-European, include the business-visa path in your first-month setup plan.

Turnover and VAT Monitoring Rules You Should Not Wing#

Track turnover every month and prepare regime-change operations early. Waiting for filing season is how small gaps become expensive cleanup.

Use this planning anchor carefully. One advisory source states that if turnover exceeds EUR 77,700 or EUR 188,700 for two consecutive years, you must move to another tax regime from January 1 after those two years. Use that for regime-change planning only, not as a VAT-threshold rule.

| Monitor area | Monthly check | Why it matters |

|---|---|---|

| Turnover trend | Current month, year-to-date, and rolling trend | Flags sustained growth early |

| Threshold exposure | Distance to EUR 77,700 or EUR 188,700 and second-year risk | Reduces last-minute regime-switch pressure |

| Regime-change readiness | Draft status for accounting workflow updates and client communication plan | Prevents rushed process and communication changes |

Predefine trigger actions so decisions stay consistent under pressure:

- If your forecast shows a real chance of a second consecutive excess year, open a regime-change readiness plan with an owner and deadline.

- If growth stays above plan across repeated monthly reviews, draft and internally test your updated billing and admin workflow.

- If process changes are likely next quarter, prepare client-facing communication before the switch window.

Make trigger actions concrete. Decide who updates billing templates, who reviews declaration impact, and who approves client-facing wording. Even in a solo activity, naming the role clarifies what must happen first and what can wait.

The tradeoff is straightforward: micro keeps administration lighter while it still fits, but delayed regime-change readiness creates avoidable coordination work across billing, client communications, and filings.

A short monthly checkpoint keeps this manageable:

- Confirm current turnover figures are complete and reconciled.

- Note whether your risk of consecutive excess years has changed.

- Update your regime-change readiness status and next action date.

Bookkeeping and Invoicing Standards That Survive a Tax Audit#

Audit durability comes from current records tied to money actually received. Treat the livre des recettes as a core accounting record, and use a livre des achats only when your activity requires purchase tracking.

For a micro-entrepreneur, the revenue book is a core accounting obligation. Keep it accurate and current, and record each payment with collection date, amount received, client identity, and nature of the transaction. In an audit, tax authorities can request this record to verify declared sales.

Do not let invoicing timing distort your books. Invoiced sales and cash receipt often happen on different dates, so your revenue book should follow receipt dates, not invoice issue dates. Reconcile invoices against payments regularly so unpaid invoices stay visible without being treated as collected income.

Use a regular spot-check on a small sample of invoices:

- Confirm each sampled payment appears in the

livre des recetteswith the correct receipt date and amount. - Verify client identity and transaction nature are consistent between invoice and book entry.

- Make sure payment evidence and invoice records can be matched quickly.

- Fix any mismatch quickly so drift does not carry into future declarations.

Add one more safeguard: keep a short unresolved-items list after each review. If an invoice is unpaid, partially paid, or unclear, log it with an owner and next action. This keeps open issues visible until they are closed, rather than disappearing between reporting cycles.

When corrections are required, keep clear traceability. Note what changed, when it changed, and why, so differences in declared figures are easier to explain during review.

Red Flags That Mean You Should Talk to a Professional#

When key facts are unclear, escalate before your next filing or status step. Clean books help, but they do not resolve visa or status uncertainty by themselves.

- Your status facts are no longer clear across countries, especially after a material mid-year change in where you lived or worked.

- You are unsure whether your current visa path still fits your situation.

- Your activity description shifted, but registrations, invoice wording, or declarations were not updated consistently.

- You received an official notice and cannot confidently interpret what is being asked.

- You cannot quickly assemble a coherent evidence trail for your planned stay, activity, invoices, and declarations.

If your case depends on the entrepreneur or profession libérale route, treat visa uncertainty as a hard trigger to escalate. This route is described as a long-stay visa (visa long séjour valant titre de séjour entrepreneur/profession libérale) with an initial one-year stay and an extension process before expiry for two to four years. One public refusal example cited supporting information judged incomplete or not reliable, which is a practical warning that document quality can affect outcomes.

Targeted advice works best when you bring a clean packet. Include your one-page situation narrative, activity description, recent invoices, declaration history, and any authority messages. Advisors can give clearer direction when they can see the full chain rather than isolated documents.

If you receive advice, translate it into concrete file updates quickly. Update wording, templates, and checklists in the same week so old language does not keep circulating in future invoices or declarations.

Building a Cross-Border Payment Trail That Supports Compliance#

A compliant cross-border payment trail is one chain you can follow from invoice to payout to declaration entry without gaps. When that chain breaks, reconciliation slows down and review risk rises.

Use one reference key across each related record set so matching is mechanical, not memory-based. Keep that key on client invoices, payout records, bank receipts, and your declaration worksheet. Map records back to core business identity records for consistency.

France is moving to structured electronic invoicing in a 2026 rollout, with staggered deadlines that include a September 2026 milestone for large companies. Under that model, structured formats such as Factur-X or XML are expected, while plain PDF alone is described as non-compliant. Where transmission applies, retain proof that invoice and transaction data were sent through the public invoicing portal or a certified service provider.

For cross-border payouts, choose tools with clear status history and exportable logs so your reconciliation stays evidence-based. This matters most across regions, where payment regulation can be fragmented and matching records can become more costly and uncertain.

Run a monthly checkpoint to catch drift early:

- Trace a sample of paid invoices from invoice to payout to declaration line.

- Reconcile gross amount, fees, conversion outcome, and net receipt, then log variances.

- Export provider transaction logs and store them with that month's invoice batch.

- Flag and resolve unmatched payments before filing.

To make this repeatable, decide where each document lives before volume grows. Keep invoice exports, payout logs, and reconciliation notes in monthly folders with the same naming pattern. Consistent storage is a practical control, not clerical overhead.

Provider features can help, but they do not transfer your legal obligations. Coverage claims, for example payouts to many countries, and consolidation features, such as campaign payouts grouped into one invoice, are product-specific and can vary by market or program. Treat them as operational aids, and keep your own invoice-level mapping so audit responses do not depend on a single vendor view.

When a mismatch appears, triage in order. First confirm invoice and payout references match. Next verify fee and conversion treatment. Then check declaration entry logic. That sequence usually finds the root cause faster than editing declaration lines first.

The Bottom Line for a Compliant Business of One#

Compliance stays manageable when your registration choices and daily records stay consistent. A practical sequence is to clarify your residency and operating facts, confirm eligibility, define your activity clearly, complete registration, then maintain regular controls.

The micro-entrepreneur regime is simplified, not documentation-free. Issue an invoice for each transaction, and make sure the required information is present, including your SIRET number. Keep registration documents and invoicing records aligned so your file remains coherent over time.

Keep recordkeeping strict and simple:

- Maintain a

livre des recetteswith all income received during the year, including date of collection and customer identity. - Keep a purchase register if your activity includes sales of goods or supplies.

- Treat these records as audit-facing documents, since authorities may request the revenue book during a tax audit.

If VAT treatment is unclear, pause and get targeted expert input before issuing or filing.

Use this checklist to stay on track (adapt the timing to your workflow):

- This week: confirm regime fit and whether your residency and eligibility facts are clear.

- This month: confirm registration evidence is organized, validate invoice fields, and update your

livre des recettes. - Ongoing: review records regularly, watch for VAT complexity, and correct drift early.

- Any time facts are ambiguous: stop and get expert input before filing.

If you keep one operating rule, keep this one: do not let unresolved ambiguity compound. When facts are unclear, pause, verify, and document the decision before the next invoice or declaration. That single habit protects both compliance quality and your workload.

Frequently Asked Questions

Is Auto-entrepreneur status the same as the Micro-entrepreneur regime in France, and does the distinction matter in practice?

Use the exact terminology shown in your registration records and tax accounts, and if your documents mix terms, get written confirmation before your next declaration.

Can a non-EU freelancer register without a Profession Libérale visa or Residence permit for self-employment?

There is no clear immigration-eligibility rule here for non-EU applicants. Resolve work-right status before locking in business filings or client billing plans. If visa or permit status is unclear, consider pausing registration and getting targeted advice before making client-facing commitments.

How do I decide between Liberal professions and Commercial activity if my work is mixed?

Keep your activity description, invoices, and declarations aligned, and seek official or professional guidance if your revenue mix changes or classification is unclear.

When does VAT (TVA) become a practical issue, and when should I request a VAT number?

VAT becomes a live issue when your cross-border sales fall into EU scopes where scheme choice changes filing. For certain cross-border B2C e-commerce supplies, the EU-wide threshold cited is EUR 10,000. The cross-border SME scheme separately cites a Union turnover cap of EUR 100,000, requires prior notification, and indicates registration should not take longer than 35 working days after receipt. Keep these VAT mechanics separate from immigration checks.

What records are legally essential between livre des recettes, livre des achats, and invoices with SIREN/SIRET?

Verify bookkeeping obligations for those books and specific SIREN and SIRET invoice fields directly before assuming your template is complete. As a practical control, keep a traceable chain from invoice to payout to declaration and keep identifiers, dates, and activity wording consistent.

Can I stay in micro-entreprise if I need meaningful expense deductions, or is régime réel a better fit?

Make this choice using your own numbers, including cross-border VAT exposure and admin capacity, and revisit the choice periodically as volume changes.

What are the top signals that my French tax residency or filing setup needs professional review now?

Escalate when VAT treatment for a complex cross-border deal is unclear, since France participates in VAT Cross-border Rulings and requests are made where you are VAT-registered. Escalate when you cannot confirm whether OSS or cross-border SME-scheme conditions apply to your case. If your filings and records are inconsistent, get professional review before submitting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- etf.europa.eu/sites/default/files/2023-05/Micro-Credential...trusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

The Best SEO Tools for Freelancers

Before you buy anything, decide how you will defend it to yourself and to a client. For a solo operator, tool selection is not a taste question. It is an operations decision about whether you can produce the same monthly report on time, explain the numbers, and keep working if a tool changes or disappears.