Quick Answer

Yes. If you used foreign exchanges such as Binance or KuCoin, run FBAR and Form 8938 as separate tests using account-level records first. FBAR is filed as FinCEN Form 114, while Form 8938 is attached to your income tax return when required. Keep statements, value-tracking support, and account-status notes, then verify current IRS and FinCEN guidance before filing.

Introduction: Why Your Definition of a "Tech Stack" is Dangerously Incomplete#

If your crypto activity includes non-U.S. exchange accounts, your stack should start with compliance, not just a mix of trading, invoicing, and bookkeeping apps. You need a setup that prevents missed filings, keeps FBAR and Form 8938 analysis separate, and preserves required records throughout the year. Use this baseline:

FBAR (FinCEN Form 114)reports certain foreign financial accounts, is filed with FinCEN rather than the IRS, and is triggered when aggregate foreign account value exceeds$10,000at any point in the year.Form 8938is attached to your annual U.S. income tax return when required to report specified foreign financial assets. A commonly cited baseline threshold is$50,000for certain U.S. taxpayers, with higher thresholds for some filers.- These obligations do not replace each other, and some accounts can be reportable on both.

- For FBAR analysis, whether an account produced taxable income does not determine whether it can be a foreign financial account.

- For FBAR timing, the annual due date is

April 15, with an automatic extension toOctober 15.

Start with the facts. IRS guidance treats digital assets as property for U.S. tax purposes. IRS Publication 5569 noted that a foreign account holding only virtual currency was not FBAR-reportable at that time, while also noting FinCEN's stated intent to propose changes. So the right starting question is not, "I used Binance or KuCoin, so I already know my filing answer," but, "What account do I have, what did it hold, and what records support that conclusion?"

This article follows that order: compliance first, operations second, payments and cashflow third. Build one evidence pack from day one so reporting decisions come from records, not reconstruction.

Related: How to Choose a Tech Stack for Your SaaS Product.

Layer 1: The Compliance Fortress - Survive Before You Scale#

Treat compliance as a core operating layer, not a year-end cleanup project. Put four basics in place now, each with one owner, one review cadence, and one evidence location, so filing decisions are less likely to turn into payment friction, delayed books, or avoidable rework.

| Control area | What to track | Why it matters | Evidence to retain |

|---|---|---|---|

| Residency tracking | Dates/locations, address used, trip purpose, material changes | Helps support your filing position and reduce contradictions across records | Itineraries, passport/travel records, lease/address documents, dated log |

| Invoice compliance | Client legal entity, billing details, service period, required wording/IDs | Can reduce AP rejections, reissues, and audit-trail gaps | Final invoice, written entity confirmation, contract/SOW |

| FBAR/Form 8938 monitoring | Foreign accounts account-by-account, max values, open/close status | Supports separate filing analysis for each regime | Account register, exports, screenshots, open/close records |

| Document vault | Year-based folders across all control areas | Keeps proof usable when filing, reviewing, or escalating | Returns, extension records, account files, contracts, advisor correspondence |

Residency tracking#

The standard is not just "track travel." It is "keep a dated record that supports the filing position you take." Log where you were, when you arrived and left, which address you used, and any change that may affect filing status.

Reconcile that log to hard records on a fixed cadence so gaps get fixed while the facts are still fresh. If your records start to conflict, escalate to a qualified tax professional before filing.

Invoice compliance controls#

Use one approved invoice template and treat legal-entity accuracy as a real check, not an admin detail. Before sending an invoice, confirm the billed entity and billing contact in writing and store that confirmation with the invoice package.

If a client asks you to bill a different entity than the contract entity, send it to review instead of changing it informally. That helps avoid rework and protects your compliance trail.

FBAR and Form 8938 monitoring#

Organize this work by account, not by platform brand. Track each foreign account separately, then roll totals up for filing analysis. At minimum, capture the holder, platform, account type, whether the account was closed during the year, and the records that support maximum value and year-end status.

| Tracker item | What to capture | Article note |

|---|---|---|

| Holder | Account holder | Core tracker field |

| Platform | Platform | Core tracker field |

| Account type | Account type | Core tracker field |

| Closed during year | Whether the account was closed during the tax year | Form 8938 includes this checkpoint |

| Maximum value | Records that support maximum value | Used in filing analysis and Form 8938 checkpoints |

| Year-end status | Records that support year-end status | Used in filing analysis |

| Account counts | Number of accounts | Form 8938 includes this checkpoint |

Form 8938 includes account-level checkpoints such as account counts, maximum values, and whether accounts were closed during the tax year. It is filed with your annual return by that return's due date, including extensions. Filing Form 8938 does not remove a separate FBAR obligation. If no income tax return is required for the year, Form 8938 is generally not required even when asset values exceed the reporting threshold.

In your tracker, reserve fields for threshold values you verify each season: the FBAR trigger from current FinCEN guidance, and the Form 8938 cutoff, including any baseline or higher thresholds tied to filing status or residency, from current IRS guidance.

Set and document an internal review cadence tied to activity. If you close an exchange account, lose access, or move assets quickly across accounts, export records and capture screenshots immediately. If filing-status questions stay unclear, including whether you are a specified person or whether no-return rules apply, escalate to a qualified tax professional.

Document retention vault#

Make one secure, searchable vault by year, with subfolders for residency, invoices, foreign accounts, returns, extensions, and advisor correspondence. Export and store exchange records before any account closure or platform exit so your evidence does not depend on future access.

At each review point, confirm every account in your register has support on file. Also verify that you are using current Form 8938 materials and current FBAR deadline guidance from FinCEN, including any event-based extensions.

For a related example, read Professional Deep Dives: From Anxious Operator to CEO.

Before you finalize your filing workflow, run a quick self-check with the FBAR calculator so your account inventory and reporting logic stay aligned.

Layer 2: The Operations Engine - Eliminate Your "Admin Tax"#

Once the compliance layer is stable, operational drift becomes the next drag: delayed handoffs, missed approvals, and duplicated client data entry. The fix is simple but strict. Give each stage one trigger, one owner, and one proof artifact. If the proof is missing, the step is not done.

| Trigger | Owner | Manual workflow | Automated workflow (system action) | Proof artifact |

|---|---|---|---|---|

| Contract signed | You or client ops lead | Send welcome email, create folder, build task list, re-enter billing details | Status change creates kickoff tasks, client folder, and invoice handoff record | Signed contract, folder link, task record, draft invoice |

| Deliverable ready for approval | Project owner | Chase approval across email/chat, then mark complete manually | Approval logged in the designated channel updates project status and alerts billing | Approval record, dated status log, final file version |

| Project close or client offboarding | You | Remove access later, gather final docs later, archive ad hoc | Closeout checklist triggers archive, access review, final invoice, and feedback request | Access change log, archive export, final invoice, closeout checklist |

| Exchange account closed or access lost | You | Try to retrieve records after access is gone | Event triggers task to export files and save screenshots to the year vault | Exported statements, screenshots, account note |

Project tracking that survives handoffs#

Pick tools based on record quality and handoff reliability, not interface preference. IRS guidance allows flexible systems, but your setup still has to clearly show income and expenses and preserve a usable transaction record. Before you lock in your setup, check for four things:

| Check area | Confirm | Specific record or field |

|---|---|---|

| Client steps | Each client step has one owner, due date, and status | Owner; due date; status |

| Document flow | The final approved file and its history are preserved | Final approved file; history |

| Invoice handoff | Billing data carries over without retyping | Legal entity; service period; billing contact |

| Change history | History is exportable | Who changed what and when |

Keep the line clear between logs and proof. Activity logs help, but they do not replace supporting documents. You still need the underlying invoices, receipts, deposit records, paid bills, and related support for return entries.

Onboarding and offboarding without loose ends#

Run onboarding and offboarding as event-driven SOPs so execution and evidence move together. When an agreement is signed, create the folder, kickoff tasks, billing confirmation, and invoice handoff in the same motion. At closeout, confirm approval, issue the final invoice, export files, and complete access review.

Treat access lifecycle as a control, not cleanup. NIST ties account management to termination and transfer events, which maps cleanly to client closeouts and contractor roll-offs. Use a recurring checkpoint to reconcile active clients and collaborators against active folders, shared drives, and communication spaces, then fix mismatches immediately.

One source of truth for decisions#

Keep one official record for approvals, scope changes, deadlines, and billing changes. Conversations can happen anywhere, but final decisions should be written back to the same place so a third party can reconstruct what was approved, delivered, and billable.

That discipline helps both compliance and operations. You get cleaner records for reporting and clearer support when you need year-end files, foreign account exports, or filing analysis. Well-organized records also make it easier to provide the right answers if the IRS contacts you. Recordkeeping saves the most time at tax time when proof is captured during the work, not after it.

For a step-by-step walkthrough, see A Deep Dive into Thailand's Long-Term Resident (LTR) Visa for Tech Professionals.

Layer 3: The Finance Hub - Get Paid Without Penalties#

After approvals and handoffs are under control, cash movement becomes the next failure point. Use four separate rails, each with one job: client intake, currency conversion, reserves, and operating spend. That can keep funds usable, reduce payout friction, and leave a cleaner trail for year-end reporting.

Separate rails by job, not by provider#

Do not force one account to do everything. Keep intake for receiving client payments, conversion for FX decisions, reserves for protected cash, and operating spend for daily outflows.

| Rail | Primary job | Speed to usable funds | Fee transparency check | FX handling rule | Payout timing control | Reconciliation quality |

|---|---|---|---|---|---|---|

| Client intake | Receive invoices and client payments | Usable after settlement into an account you control | Gross amount, net amount, and deductions are exportable | Avoid forced conversion at receipt when you bill in multiple currencies | Use payout settings you can verify | Strong when invoice ID and payment reference follow the deposit |

| Conversion | Exchange currency when needed | Fast after funds arrive | Keep quote, settled amount, and timestamp | Convert only for planned reserve or spend needs | You decide when to convert | Strong when each conversion maps to a source deposit |

| Reserve | Hold tax and buffer cash | Slow by design | Low activity is expected | Keep FX activity minimal | Movement should be deliberate | Strong when statements support period-end and maximum-value tracking |

| Operating spend | Pay vendors, payroll, and local expenses | Fast for day-to-day use | Outgoing payments must map to ledger categories | Spend in the owed currency where possible | High control for recurring outflows | Strong when each payment includes vendor and purpose detail |

Treat "withdrawal penalties" as a flow-control check#

Value leakage can come from hidden conversion, delayed settlement, or weak traceability. Each month, check four fields together: invoiced amount, settled amount, converted amount, and posted ledger amount. If they do not tie, fix the flow before assuming pricing is the real problem. Use these checks:

| Failure point | Check | Response |

|---|---|---|

| Hidden conversion | Compare invoice currency to settlement currency | Disable automatic conversion where possible |

| Settlement delay | Compare payment date to usable-funds date | Review payout schedule and destination rail settings |

| Traceability loss | Verify every deposit and payout keeps a stable reference | Reference reaches your ledger and month-end exports |

Build a finance-to-compliance blueprint#

Your finance process should feed compliance records automatically, not force you into year-end reconstruction.

| Workflow step | Required record | Why it matters for compliance |

|---|---|---|

| Invoice issued and paid | Invoice ID, gross amount, net amount, payment reference | Preserves the source-to-settlement trail |

| Settlement received | Account/platform, date, currency, amount, destination account | Supports account-level tracking across rails |

| Conversion posted (if used) | Quote, timestamp, source amount, converted amount | Explains value movement between currencies |

| Ledger posting | Category, counterparty, purpose, linked payment reference | Keeps reconciliations audit-ready |

| Monthly compliance pack | Statement exports/screenshots, year-end balance, maximum value, open/close status, acquired/sold notes | Supports Form 8938 checkpoints and related recordkeeping |

For Form 8938, file by attaching it to your annual return by that return's due date, including extensions. Filing Form 8938 does not replace FinCEN Form 114 (FBAR). Form 8938 also includes checkpoints on maximum value, whether foreign deposit or custodial accounts were closed during the year, and whether foreign assets were acquired or sold. Verify scope before tagging an account for Form 8938, since some accounts maintained by a U.S. payer are excluded.

If you file through an entity, confirm whether specified domestic entity rules apply. The Form 8938 instructions cite a threshold of $50,000 on the last day of the tax year or $75,000 at any time during the tax year for certain specified domestic entities.

Use this monthly run list to keep finance and compliance aligned:

- Confirm each rail still has one job only: intake, conversion, reserve, or operating spend.

- Reconcile invoiced, settled, converted, and posted ledger amounts for foreign-currency flows.

- Export statements or screenshots for each foreign account or platform and store them in the year vault.

- Update maximum-value tracking for foreign deposit and custodial accounts.

- Log account openings and closures and whether foreign assets were acquired or sold.

- Current Form 8938 threshold for your filing status and residency: pending verification against official IRS materials.

- If filing through an entity, verify whether specified domestic entity rules apply.

- Check current FBAR timing and any event-based extension notices before filing.

For a related topic, see A Deep Dive into Form 3520 (Annual Return To Report Transactions With Foreign Trusts).

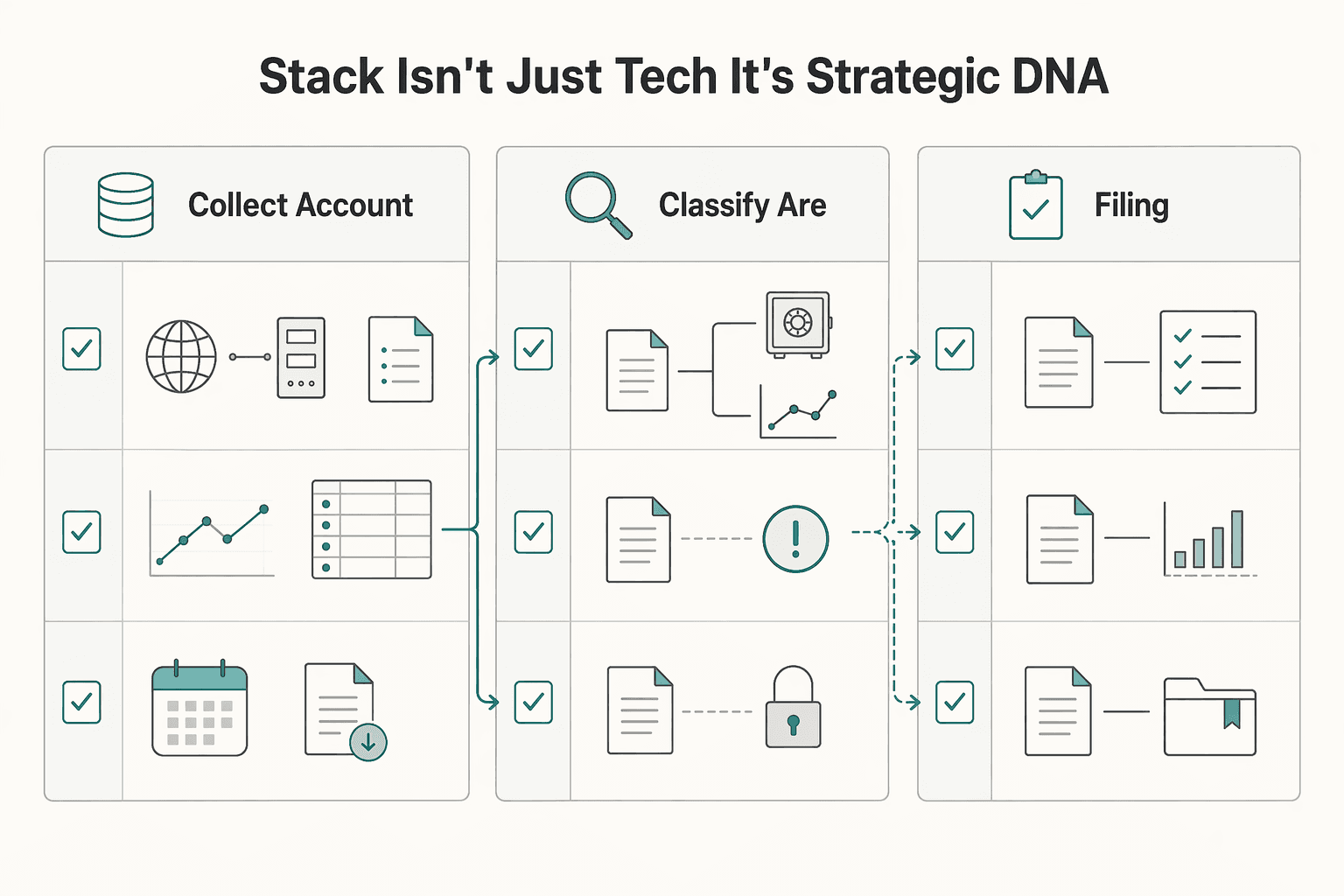

Your Stack Isn't Just Tech - It's Your Strategic DNA#

Your stack is not a tool list. It is the repeatable process you run each filing cycle: collect foreign-account records, review FinCEN Form 114 and Form 8938 separately, and keep the evidence behind your decisions.

The practical shift is simple. You are not just choosing tools. You are building a process that captures the right facts when foreign platforms are involved, and still makes sense if you revisit the file later or hand it to a preparer:

- Collect account data for each foreign financial account.

- Classify what you are testing as accounts, assets, or both.

- Review FBAR and Form 8938 as separate filing decisions.

- Store documentation that supports your filing position.

The key checkpoint is whether your file supports the form-level questions. For Form 8938, that includes the applicable calendar year or tax year. It also includes account-inventory items such as the number of foreign deposit accounts, the maximum value of those accounts, and whether foreign assets were acquired or sold during the year. If your records do not support those points, the file is not ready for review.

A common failure mode is treating one decision as if it answers both forms. It does not. Filing Form 8938 does not remove a separate FBAR obligation. And if you do not have to file an income tax return for the year, Form 8938 is not required, but you still need a separate FBAR determination.

A compliance-first stack can give you outcomes you can verify: fewer missed reporting steps, a cleaner handoff to your preparer, and more consistent decisions year to year. Before the next cycle, document where your current process breaks, then turn those gaps into one compliance-first checklist and one tool map.

We covered this in detail in A Deep Dive into the US-Ireland Tax Treaty for Tech Consultants.

If you want a compliance-first setup for getting paid across borders with clearer operational controls, contact Gruv to confirm fit for your workflow.

Frequently Asked Questions

What should you review first if you used Binance, KuCoin, or another foreign exchange?

Review evidence before classification. Gather platform statements or screenshots, year-end balance support, value-tracking support, and notes on whether foreign deposit or custodial accounts were closed and whether foreign assets were acquired or sold during the year. Then separate what you are testing for each form, apply the two sets of rules independently, and archive the support file you relied on.

Do FBAR and Form 8938 ever both apply?

Yes, they can. Form 8938 instructions state that filing Form 8938 does not relieve a FinCEN Form 114 filing requirement. Treat them as parallel checks, not substitutes.

What gets misclassified most often?

One error is treating one exchange export as if it answers both forms. Another is skipping Form 8938 prompts on closed foreign deposit or custodial accounts and foreign assets acquired or sold during the year. Keep account-level and asset-level analysis separate in your notes.

How do you handle thresholds without overclaiming?

For Form 8938, confirm your filing category in current IRS guidance before using any threshold. IRS materials reference $50,000 for certain taxpayers and $50,000 year-end / $75,000 anytime for certain specified domestic entities, but category-specific thresholds must be verified before filing. For FBAR, verify the current threshold directly from current FinCEN guidance.

What documents should you keep if you want a defensible file?

Keep the records that support your classification, not just final totals. Save statements or screenshots, transaction exports, year-end balance support, value-tracking workpapers, closed-account and acquired or sold notes, plus filed-form copies and confirmations.

What if you do not have to file an income tax return?

Then Form 8938 is not required for that tax year. That does not answer FBAR by itself, so run the FBAR check separately.

How often should you verify guidance in 2026?

Verify before filing and again when your facts change. The IRS About Form 8938 page shows a 23-Jan-2026 review date, but you should still confirm the latest instructions before filing.

What is one next step you can complete right now?

Create one folder per foreign exchange account and save four items today: latest statement or screenshot, year-end balance support, value-tracking note, and closed, acquired, or sold notes. That gives you a usable evidence base before you decide final FBAR and Form 8938 treatment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- csrc.nist.gov/pubs/sp/800/92/r1/ipdtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: