Quick Answer

Start by mapping one recent client engagement across decision location, contract approval, delivery direction, and record storage, then pause structural changes if any line lacks dated proof. For economic substance for solopreneurs, this article’s defensible baseline is a monthly decision log plus an evidence file that keeps contracts, invoices, activity records, and approval notes aligned. Keep U.S. reporting separate but synchronized by feeding both FBAR (FinCEN Form 114) and Form 8938 from the same account records.

What Economic Substance Looks Like in a Solo Business#

If you run a one-person business through a Single-Member LLC or an offshore company, start with a simple question: which compliance and reporting obligations may apply now, and what is the smallest structure you can defend with records. Make that call before you change entities, move banking, or submit filings that lock in a story you cannot support later.

You are likely handling delivery, contracts, banking, and compliance at once. The practical target is not perfect paperwork in week one. The target is alignment, so your decisions, daily activity, and records describe the same reality when a reviewer reads them in sequence.

Scope is the first constraint. Jurisdictions are not interchangeable, and local rules can change. Use this as a decision aid, not legal or accounting advice. Then verify jurisdiction-specific obligations before filing deadlines.

Plan structure and reporting together. For U.S. taxpayers, offshore activity can trigger FBAR and FATCA reporting, and those duties can differ by account values, filing status, and residency. Treat common thresholds as prompts to verify your exact profile, not as universal rules that fit everyone.

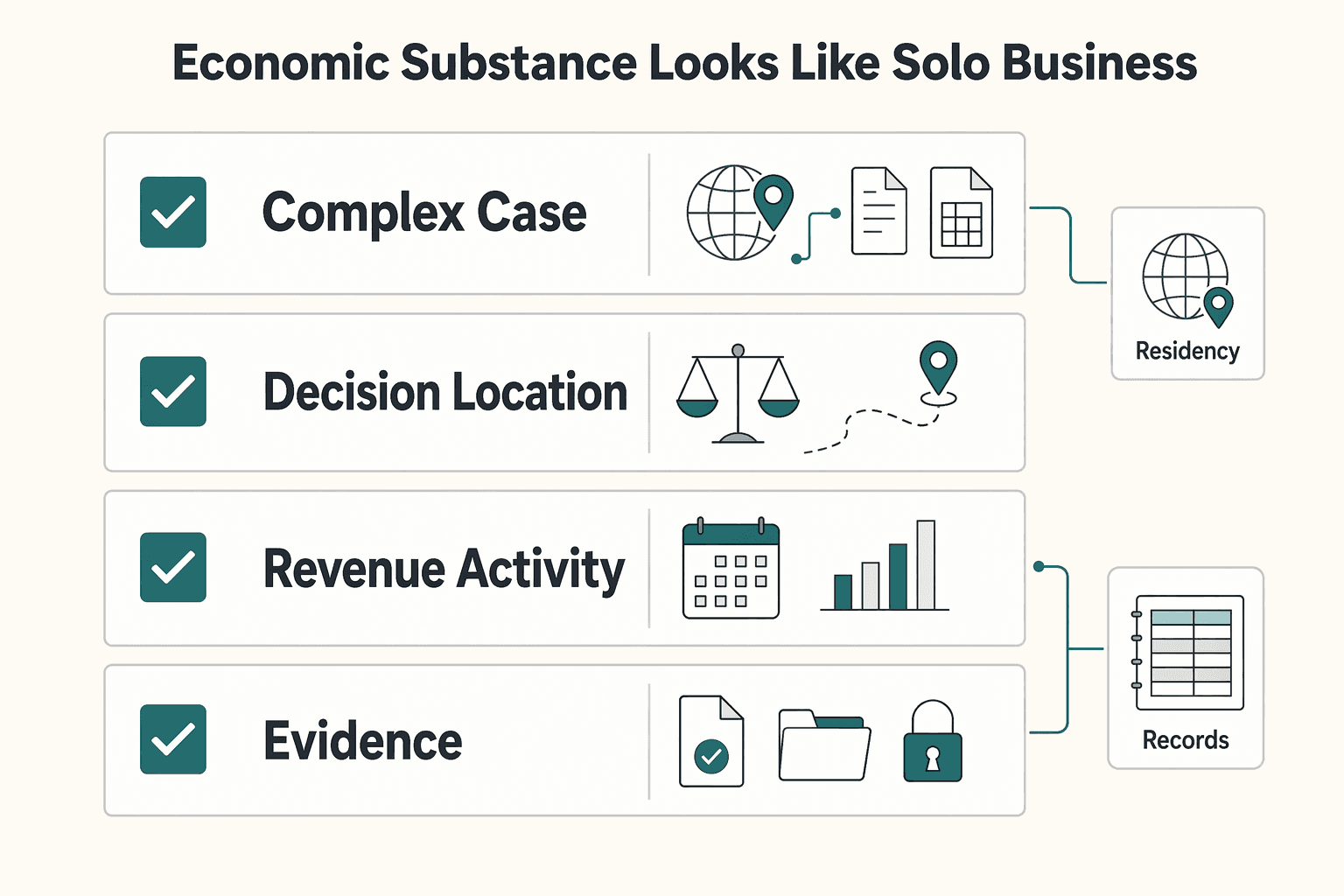

Use this four-point checkpoint before changing entities or opening foreign accounts:

- Entity location: Where is the company legally registered?

- Decision location: Where are material business decisions actually made?

- Revenue activity: Where are services negotiated, sold, and delivered?

- Record location: Where can you produce contracts, invoices, and decision notes on request?

After you answer, pressure-test each line against a recent client engagement. If you cannot point to dated records for person, place, and action, treat that line as unproven. The goal is not to win an argument with wording. The goal is to make your position easy to verify with documents you already control. If any answer is vague, pause major structural changes and get legal or accounting review tied to your facts.

For related contract language context, see What is an 'Evergreen' Clause in a Retainer Agreement?. For a concrete next step, Browse Gruv tools.

Economic Substance in Plain English#

Start with a simple rule: your filings, decisions, and records should tell one consistent story. If your documents say one thing but your day-to-day activity shows another, resolve that mismatch before you file.

Separate setup tasks from substance checks. Forming an entity or choosing tax treatment can be valid on paper while still leaving questions about where business activity and judgment occurred. Those issues are related, but they are not the same thing.

Use this quick verification routine:

- Trace one recent engagement from decision to delivery to payment.

- Match that timeline to records such as contracts, approvals, invoices, and notes.

- Check official pages first when verifying public guidance. A

.govdomain signals a U.S. government organization, and HTTPS confirms a secure connection. - If records point in different directions, pause structural changes and clean up the trail.

Add one practical habit: write short decision notes as events happen, not weeks later. Reconstructing later can create date gaps and vague language, which can lead to contradictions. A concise note with date, decision, location, and supporting file link is a practical baseline.

For solo founders, keep claims narrow, statements specific, and evidence close to each claim. When facts are unclear, do not fill gaps with assumptions. Mark the gap, then fix it.

Why Solo Founders Get This Wrong#

A common mistake is treating two different jobs as one file: filing U.S. self-employment tax forms and documenting where business activity was directed and managed. Both matter, but they answer different questions and are reviewed through different lenses.

Schedule SE is used to calculate tax due on net self-employment earnings. IRS guidance states that self-employment tax covers Social Security and Medicare taxes and can apply regardless of age or current benefit status. The Social Security Administration also uses Schedule SE information to calculate benefits. None of that, by itself, proves economic substance.

Cross-border Social Security rules add another layer. Totalization agreements are designed to reduce dual Social Security taxation by assigning coverage to one country and exempting taxes in the other. That still does not answer where your core income-generating activities took place.

Before you file, run this separation check:

- Keep Schedule SE support together: net-earnings workpapers, tax inputs, and filed forms.

- Keep substance support separate: decision records, approval trails, and delivery records tied to where work was directed.

- If cross-border Social Security coverage may apply, start Certificate of Coverage checks early.

- If the same activity is described differently across files, reconcile it before submission.

A useful internal control is a two-folder test. Folder one supports tax calculations. Folder two supports jurisdiction and activity narrative. If a document belongs in both, duplicate it with a clear note on why it matters in each context. That keeps reviewers from inferring claims you did not mean to make. Treat this as parallel discipline, not something that happens automatically just because you file taxes.

Do You Actually Need to Act on ESR Right Now?#

Treat this stage as triage, not a final legal determination. General guidance is broad, can change without notice, and is not a substitute for legal or accounting advice. If your facts are unclear, move professional review to the top of your list. If your situation appears straightforward and domestic, complete core compliance tasks first and set a timed review checkpoint.

| Checkpoint | What to verify |

|---|---|

| Entity map | List every legal entity you control and where each is registered |

| Contract path | Note where deals are negotiated, approved, and signed in practice |

| Delivery trail | Document where client work happens and who directs it |

| Decision trail | Identify where major pricing and scope decisions are made |

| Record readiness | Confirm you can quickly produce contracts, invoices, and decision notes |

Use a simple two-lane rule:

- Higher urgency: you are uncertain about your facts, obligations, or how your structure operates in practice.

- Lower urgency: your setup is straightforward, your records are clear, and you have a scheduled review checkpoint.

Use the checkpoint table before you change entities, banking, or filing posture. If even one critical line is unclear, pause and get jurisdiction-specific legal or accounting advice.

Choose a Jurisdiction by Operating Burden, Not Marketing Claims#

Choose the jurisdiction you can operate and document consistently, not the one with the best headline promise. If you cannot maintain real decision-making and clean records in-jurisdiction, do not choose it. Treat this as general guidance, not legal or accounting advice. Information can change, and if you are unsure how to proceed, seek professional review.

Use the same due-diligence questions for BVI, Cayman Islands, UAE, Estonia, and Singapore before committing:

| Jurisdiction | Setup friction | Ongoing compliance tasks | Advisory scope and cost questions | Failure consequences |

|---|---|---|---|---|

| BVI | What local setup steps must you complete in practice? | What records and actions must you maintain continuously? | What recurring support is required after setup? | What happens if records and filings do not align? |

| Cayman Islands | What local setup steps must you complete in practice? | What records and actions must you maintain continuously? | What recurring support is required after setup? | What happens if records and filings do not align? |

| UAE | What local setup steps must you complete in practice? | What records and actions must you maintain continuously? | What recurring support is required after setup? | What happens if records and filings do not align? |

| Estonia | What local setup steps must you complete in practice? | What records and actions must you maintain continuously? | What recurring support is required after setup? | What happens if records and filings do not align? |

| Singapore | What local setup steps must you complete in practice? | What records and actions must you maintain continuously? | What recurring support is required after setup? | What happens if records and filings do not align? |

Before paying formation fees, ask each advisor for written scope with an as-of date. Then compare that scope to how you run the business now, not how you hope to run it after expansion. This gap check can stop you from buying a structure that works only on paper.

For each advisor conversation, use a short comparison grid:

- What must happen locally each month.

- What records must exist before filing.

- What the advisor will do.

- What remains your responsibility.

- What the cleanup path looks like if assumptions are wrong.

That makes jurisdiction selection an execution decision. Marketing copy can make each option sound simple. Your records and calendar are the practical test of whether an option is sustainable.

Define Your Core Income-Generating Activities Before You File Anything#

Before you file anything, define the short list of actions that actually create revenue and map each action to who did it, where it happened, and what document proves it. That mapping turns planning into verifiable execution.

Build the map from real weeks, not ideal weeks. Solo revenue can move quickly, and one founder account reports swings from $0 for over three months to over $27,000 in under 30 days. Capture proof while details are fresh and timelines are still easy to verify. You can do this with simple, low-cost tools; expensive systems are not a requirement to start.

Start with actions tied directly to agreements, delivery, client outcomes, and cash movement:

- Commercial decisions: setting scope and pricing before work starts.

- Agreement decisions: confirming terms and paid change requests.

- Delivery direction: making key decisions that shape the paid result.

- Client management: handling review calls, renegotiations, and retention actions.

- Revenue handling: issuing invoices and resolving payment issues.

Then build a claim-versus-proof matrix so each material statement has a traceable path:

| Claim | Person | Place | Proof |

|---|---|---|---|

| Scope and pricing were approved by the founder | Founder | Usual location used for the approval call | Dated call notes, proposal history, approval email |

| Contract changes were approved by the founder | Founder | Same location described in your narrative | Redlined agreement, signed amendment, timestamped approval |

| Delivery decisions were directed by the founder | Founder | Primary work location during delivery period | Project log, deliverable history, client acceptance message |

| Revenue adjustments were approved by the founder | Founder | Location where billing decisions were made | Invoice trail, reconciliation notes, credit memo approvals |

Separate strategic decisions from admin tasks before you finalize your narrative. Strategic decisions change money, scope, timing, or delivery outcomes. Admin tasks support execution but are weaker proof of where key judgment happened.

A practical way to avoid drift is a monthly rewrite test. Read your narrative line by line and ask: can you point to proof for this exact statement quickly? If not, narrow the statement or improve the record. Keep claims tight enough that the evidence does the work without interpretation. If weekly capture is slipping, How to Manage Your Time Effectively as a Freelancer can help you keep a steady documentation cadence.

Build a Minimum Viable Substance Operating Model#

Keep this light and repeatable. Turn your core activities list into a monthly habit you can maintain while structure decisions are still open. Use this as an operating routine, not a jurisdiction-specific legal standard.

Set three stable rules first:

- Focus rule: define what you want to be known for, and apply it consistently to pricing, scope, renewals, and major client changes.

- Work evidence rule: for each engagement, note key outputs, who directed delivery, and when key judgment calls were made.

- Record control rule: keep contracts, approvals, invoices, and decision notes in one controlled location with date stamps and version history.

Add recurring actions that stay small but non-negotiable:

- Update the decision log as decisions happen.

- Create a short note for material decisions when formal approvals apply.

- Maintain a contract approval register that links each signed agreement to the related pricing or scope entry.

Run one monthly verification pass: pick recent claims and trace each one to real outputs and interactions. If a trace fails, fix the record before you reuse the claim.

Define advisor ownership early so accountability is clear before deadlines:

| Role | Primary owner task | Monthly check | Pre-deadline task |

|---|---|---|---|

| Legal advisor | Validate language for major approvals | Review one new decision note or contract change | Confirm key claims match signed records |

| Tax advisor | Review consistency between records and business claims | Flag missing decision or supporting record | Review final claim set for internal consistency |

| Admin support | Maintain folder order and timestamps | Reconcile log entries against contracts and invoices | Produce a complete packet for advisor review |

Keep the model intentionally small. One page of repeatable controls beats a thick process document you never maintain. The month-to-month goal is simple: no important claim should depend on memory alone.

Create an Evidence Pack You Can Defend in an Audit#

Use a fixed cadence so your evidence stays easy to review: monthly capture, quarterly review, annual lock. This is an internal discipline, not an official ESR filing format.

Apply one rule across the full pack: every claim in your filing story must link to proof. Pull decision notes, contracts, invoices, banking support, and activity logs into one set, then rewrite or remove any claim you cannot verify quickly.

Create a front index page that assigns each claim a unique ID and links it to supporting records:

| Cadence | What to include | Checkpoint |

|---|---|---|

| Monthly pack | Decision notes, client contracts, invoices, banking support, and activity logs mapped to core income-generating activities | Verify sample claim IDs against underlying files |

| Quarterly pack | Reconciliations, compliance snapshot, open gaps list, and filing-prep notes tied to offshore compliance tasks | Confirm each open gap has an owner and target date |

| Annual pack | Final assertions, supporting exhibits, and a retention checklist aligned to your reporting requirements | Run a full claim-to-proof walkthrough before submission |

If you run an offshore entity with U.S. reporting exposure, keep FBAR and FATCA support notes in the same evidence set so filing narratives stay aligned. FBAR can apply when foreign accounts exceed $10,000, and FATCA reporting can begin at $50,000 depending on filing status and residency.

Keep core setup records easy to retrieve, including identification, proof of address, and financial references. Track open gaps in the quarterly snapshot so missing files are visible before filing.

Pause filing and fix gaps if any of these appear:

- A claim has no primary document.

- Contract and invoice dates conflict with the decision timeline.

- Banking support exists, but no activity log ties revenue to a claim ID.

Add an escalation rule for unresolved gaps. If a gap survives one monthly cycle, assign an owner and a target date. Add a temporary narrative adjustment so the filing story stays accurate while cleanup is in progress.

Prefer a lean pack with regular updates over a once-a-year catch-up when your goal is faster, clearer claim-to-proof review.

Keep ESR and U.S. Reporting in Sync#

Keep ESR and U.S. reporting aligned by using one shared evidence set and one compliance calendar, while still treating U.S. filings as separate duties. For U.S. reporting, Form 8938 and FBAR are separate filings even when they rely on overlapping records.

| Profile or check | Threshold point | Note |

|---|---|---|

| Certain taxpayers | Aggregate value above $50,000 | A commonly referenced Form 8938 baseline |

| Joint filers or taxpayers residing abroad | Higher thresholds can apply | Threshold outcomes depend on filer profile |

| Specified domestic entities | $50,000 on the last day of the year or $75,000 at any time during the year | Specified domestic entities use different tests |

| No income tax return required for the year | Form 8938 is not required for that year | Final annual check |

Form 8938 is attached to your income tax return when specified foreign financial assets exceed the applicable threshold. FBAR is a separate FinCEN Form 114 requirement, and filing Form 8938 does not remove that duty. Form 8938 threshold outcomes depend on filer profile.

| Stream | Trigger or checkpoint | Evidence to pull first |

|---|---|---|

| ESR documentation track (if applicable) | Your internal ESR review timeline | Decision log, contract approvals, activity records tied to core income-generating work |

| Form 8938 | Applicable threshold is exceeded | Foreign account statements, asset summaries, year-end value worksheet |

| FBAR (FinCEN Form 114) | Foreign account reporting requirement is met | Highest account value support, account list, ownership notes |

| Form 8938 threshold profile check | Return preparation | Same asset file used for Form 8938, then profile-specific threshold review |

Keep those threshold notes visible on your calendar. Add one FinCEN calculation checkpoint: record maximum account values in U.S. dollars, round up to the next whole dollar, and convert non-U.S. currency using the Treasury Financial Management Service rate. Example: $15,265.25 is recorded as $15,266.

Use a monthly reconciliation step so the same account list feeds Form 8938 prep and FBAR prep. If ownership or account status changes mid-year, update both tracks at once instead of waiting until filing season.

Before submission, apply one decision rule: if your records cannot support the values reported on Form 8938 or FBAR, pause and reconcile before filing. Final annual check: if you are not required to file an income tax return for that year, Form 8938 is not required for that year. For related reporting context, see What is FinCEN? A Guide for Freelancers and FinTech Users.

Red Flags That Trigger Penalties or Forced Cleanup#

Penalties and forced cleanup often start with evidence gaps. Treat any claim you cannot tie to dated records as a fix-now item.

| Red flag | Why it creates exposure | Immediate check |

|---|---|---|

| Paper-only presence | Cayman requires a relevant entity to be directed and managed in the Islands, so a registration address alone may be weak support. | Confirm where key decisions were made and whether dated minutes or decision records match that location. |

| Evidence mismatch | If contracts, invoices, and activity records point to different jurisdictions, your position can be harder to defend. | Reconcile one month of approvals, billing, and activity logs into one consistent jurisdiction record. |

| Filing-season scramble | ESR and U.S. foreign-asset reporting are recurring obligations, so late assembly leaves less time to resolve conflicts before filing. | Check that records are maintained during the year, not only at filing time. |

| Template-heavy governance text | Generic language does not prove core income-generating activities were carried on where claimed. | Attach one concrete record to each key claim showing who did the work, where, and when. |

Cayman illustrates the cost of weak execution. Missed reporting and ES-test failures are listed as penalty triggers. A first ES-test failure can trigger a ten thousand dollar penalty, and a subsequent-year failure can trigger a one hundred thousand dollar penalty. Cayman ES notifications are also due no later than 31 March each year.

BVI applies the same principle around real activity. Core income-generating activities must be carried on in the Virgin Islands, and mobile income should not be parked in a zero-tax jurisdiction without matching core functions.

Use this pre-submission checkpoint:

- Verify directed-and-managed statements against dated decision records.

- Match contract and invoice evidence to the same place you report for core income-generating activities.

- Confirm FBAR account records are retained, and keep Form 8938 support aligned with that same evidence set.

Treat the U.S. side as a parallel exposure. FBAR is annual and requires recordkeeping, and Form 8938 obligations are additional to FBAR and carry penalties for non-reporting.

Final jurisdiction check: UAE announced ESR reporting was lifted for financial years ending after 31 December 2022. If your structure spans countries, confirm current obligations by jurisdiction before filing.

Your First 30 Days of Action#

Use the next 30 days to make your compliance story easy to trace, so an external reviewer can follow each claim to proof across your compliance preparation, FBAR records, and Form 8938 support.

| Week | Focus | Key actions |

|---|---|---|

| Week 1 | Classify structure and exposure | Split your file into Single-Member LLC only and Offshore Company with cross-border exposure; record where decisions are made, where contracts are approved, where billing happens, and where records are stored; mark mixed facts immediately; end the week with a short list of unresolved facts that need advisor review |

| Week 2 | Map core activities and location proof | List three to five revenue-driving activities and tie each to person, place, and document; build one row per activity with evidence fields for each relevant jurisdiction where you operate; if an activity spans locations, split the row so each location has its own evidence line |

| Week 3 | Set documents, calendar, and owners | Keep one calendar for compliance preparation and U.S. reporting checkpoints, with a clear owner and backup reviewer for each task; track whether the filer must file an income tax return for Form 8938; keep threshold notes visible; for FBAR preparation, keep maximum account value support in U.S. dollars rounded up to the next whole dollar and document non-U.S. currency conversion using the Treasury Financial Management Service year-end rate; filing Form 8938 does not replace FBAR |

| Week 4 | Run a one-hour mock review | Ask someone who did not build the file to test it claim by claim; the standard is traceability in under one hour, not formatting perfection; log every question they cannot answer quickly, then fix naming mismatches, missing dates, and unsupported lines before the next filing cycle |

If the mock review fails, pause new entities or cross-border expansion until core records are coherent. Use this Week 4 pass-or-fail check:

- Can the reviewer trace each claim to a dated document in minutes?

- Do Form 8938 and FBAR support files tell the same ownership and account story?

- Are threshold decisions and filing assumptions written in plain language?

This sequence is a practical operating routine, not a legal mandate. Its value is speed and clarity under pressure: fewer surprises near deadlines and fewer conflicts between what you did and what you reported.

Conclusion#

The core judgment is simple: build a credible evidence trail before you add structural complexity. Economic substance conclusions should be treated as unresolved unless you have direct, jurisdiction-specific support. Keep records that show what happened, when it happened, and who approved key actions.

The next step is practical. Run your action sequence, then schedule jurisdiction-specific review before making material claims. Keep one rule active across your process: if a material claim cannot be traced to dated evidence, treat it as unresolved until you fix, rewrite, or remove it.

Planning and documentation work best together. Planning sets intent. Recordkeeping shows execution. Keep that habit active month to month, not only when pressure rises.

Solo ownership creates constant tradeoffs between speed and certainty. A short recurring evidence routine reduces that tension: update decision notes while events are fresh, store supporting documents immediately, and retire claims that no longer match facts.

Before your next review window, run this closeout check:

- Re-run your action checklist against current facts and records.

- Confirm each material statement has dated support, then rewrite or remove unsupported statements.

- Book a jurisdiction-specific review early enough to close gaps.

If this check does not pass, pause expansion until your base file is coherent. Disciplined evidence and clear judgment records put you in a stronger position than reactive cleanup later.

Frequently Asked Questions

What is economic substance for solopreneurs, in one sentence?

Use the rules in the relevant jurisdiction rather than a one-sentence test.

Does a one-person offshore company still need to meet Economic Substance Requirements?

There is no universal yes or no answer. You need a local rule check before filing.

What counts as real presence if I do most client work remotely?

This evidence set does not provide one legal test for all jurisdictions. Use local rules to determine the standard you must meet.

Is economic substance the same thing as tax write-offs or Schedule SE planning?

This evidence set does not cover Schedule SE or deduction rules, so do not rely on this section for those topics.

How do FBAR, FATCA, and Form 8938 relate to economic substance without being the same rule?

Form 8938 is used to report specified foreign financial assets and is attached to your income tax return when the applicable threshold is met. A commonly cited baseline is aggregate value above $50,000 for certain filers, and higher thresholds can apply to joint filers and taxpayers living abroad. If no income tax return is required, Form 8938 is not required even if asset value is above a threshold. FATCA is the IRS topic linked to Form 8938, while FBAR is a separate FinCEN Form 114 duty, and filing Form 8938 does not remove that requirement.

What should I do this month if I am unsure whether my current setup is compliant?

First, confirm whether you must file an income tax return, because that affects whether Form 8938 applies. Next, identify your Form 8938 threshold profile and whether separate FBAR filing may apply. Then gather account summaries and maximum account values needed for Form 8938 and run a jurisdiction-specific compliance review before making structural changes.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Manage Your Time Effectively as a Freelancer

Most freelancers struggle not because they work too few hours, but because they misallocate the hours they have—treating time as an infinite resource rather than a finite business asset with a real cost per unit. The solution is a three-layer operating system: a Time Budget Framework that commits hours to four categories before any client work is booked, a Weekly Operating Template that assigns those categories to specific calendar windows, and a monthly Admin Audit Checklist that reconciles invoicing, bookkeeping, and compliance records. Multi-client orchestration requires a WIP limit, dedicated client windows, and a capacity decision rule run before accepting new engagements. Together, these systems replace reactive decision-making with a repeatable structure that keeps delivery quality consistent, records audit-ready, and the freelance practice operationally durable.

What Is FinCEN for Freelancers and FinTech Users

If you are asking **what is fincen**, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.

What Is an 'Evergreen' Clause in a Retainer Agreement?

Steadier payment continuity starts with one clear rule: when the balance drops below the agreed floor, funding is restored to the target amount. That is the job of an evergreen clause in a retainer agreement, and it can keep payment expectations explicit before work gets ahead of cash.