Quick Answer

Yes, in most hosting setups you should carry separate short-term rental insurance. Standard homeowners and many landlord policies may not fit paid short stays, while AirCover and Vrbo protections are supplemental and usually tied to platform bookings. Massachusetts adds a concrete benchmark: Chapter 337 of the Acts of 2018 requires at least $1,000,000 in liability insurance per short-term rental. Use your channel mix and occupancy style to choose coverage, then get insurer approval documented before going live.

Why standard coverage often falls short once paid guests are in the picture#

Often, yes, but it depends on your setup. If you host paying guests on Airbnb, Vrbo, or similar platforms, treat separate short-term rental insurance as a default starting point, even when local rules are not explicit.

The issue is coverage fit. Once you accept payment, many insurers treat hosting as business use, and standard homeowners coverage often does not fully cover short-term rental activity.

Use platform protection as a supplement, not your foundation. These programs can help, but they are still one layer, not complete primary coverage.

Use this guide for a quick first-pass decision, then verify your exact setup before your next booking. Start with your rental scenario, because coverage depends on how you host. If any policy wording is unclear, confirm it directly with your insurer instead of guessing from a listing dashboard or marketing page. That step matters. One concrete failure mode is cancellation tied to undisclosed rental activity.

The goal is simple: reduce claim surprises, protect against liability exposure, and run your rental like a real business. Keep one rule in mind as you read: move from "maybe covered" to "confirmed and documented."

For a step-by-step walkthrough, see Short-Term Rental Industry in 2026: Compliance, Automation, and Niche Strategy.

Do you actually need separate short-term rental insurance?#

In many cases, yes. If paid guest stays are a real part of how you use the property, treat dedicated short-term rental coverage as the default. Standard homeowners and traditional landlord policies are often built for different use patterns. A simple decision rule:

- If you host regularly, move to coverage designed for short-term rental activity.

- If you host only occasionally, a short-term rental endorsement may be enough, but only if your insurer or agent confirms your exact setup.

For occasional hosting, verify three specifics before you rely on existing coverage. Confirm whether paid short stays are allowed for your room or unit, whether liability applies during guest occupancy, and what your policy documents or endorsements say about that activity.

Massachusetts shows why this matters. Under Chapter 337 of the Acts of 2018, operators must carry at least $1,000,000 in liability insurance for each short-term rental. The state also says it does not review individual host-platform coverages, so operators must confirm coverage amounts themselves with the platform and licensed professionals. A policy can look strong on property damage and still miss the liability level you actually need.

Related: The Pros and Cons of Short-Term vs. Long-Term Rentals.

Know the four coverage layers before you compare quotes#

Compare coverage by occupancy state, not by marketing label. One layer rarely covers every hosting scenario. In practice, homeowners insurance, landlord insurance, platform protections, and dedicated short-term rental insurance are built for different triggers.

Use this checkpoint: homeowners coverage is generally for owner or vacant periods, while paid guest stays can move risk into short-term-rental or commercial-use territory. Verify that handoff in writing before you rely on any quote.

| Layer | What it is designed to do | Property damage scope | Liability scope | Loss-of-income treatment | Booking-channel limits | Common stop point |

|---|---|---|---|---|---|---|

| Homeowners insurance | Protect an owner-occupied home | Usually oriented to owner use, not paid guest activity | Personal liability may not extend to paid hosting activity | Policy-specific; verify whether guest-related interruption is covered | Not platform-linked, but paid hosting can fall outside intended use | Business-use exclusions may apply |

| Landlord insurance | Protect long-term rental activity | Oriented to tenant occupancy, not nightly turnover | Framed around long-term landlord risk, which may not fit short stays | Policy-specific; verify whether short-stay income disruption is covered | Not platform-linked, but can mismatch nightly hosting | Assumes long-term tenants, not rotating guests |

| Platform protections (for example, AirCover / Host Protection Insurance) | Supplemental, platform-linked protection | Can provide some guest-damage protection | May include liability protection with exclusions | Not a full substitute for primary coverage | Usually tied to bookings on that platform | Off-platform bookings may fall outside protection; hosts also report partial reimbursement, denials, or slow claims |

| Dedicated short-term rental insurance | Coverage built for short-term rental operations | Typically covers guest-caused property damage | Typically covers liability tied to paid stays | Policy-specific; confirm exact terms | Policy-specific; confirm coverage for each booking channel you use | Must match your actual operations and declared use |

One common mistake is treating platform protection as the foundation. Use it as a layer, not your base insurance.

Another mistake is assuming two partial protections add up to full protection. They often do not, because each layer can have different triggers.

Before you compare quotes, get written confirmation on three points: paid short stays, direct bookings, and liability during guest occupancy. If those points are unclear, treat that as a red flag, especially because some insurers may cancel coverage after undisclosed rental activity.

The practical test is whether your stack matches how you actually host. The more channels you use, the more important it is to treat dedicated short-term rental coverage as the primary layer and platform protections as supplemental. Once you know which layer should carry the risk, look at where claims can still fall through.

You might also find this useful: Liability Insurance for Freelance IT Consultants: Do You Need It?.

Where standard and platform protections usually fail#

Claims usually fail when the policy does not match occupancy use or the booking-channel trigger, even when you thought you were covered.

| Scenario | Why it fails | Article note |

|---|---|---|

| Standard homeowners policy with paying guests | Short-term hosting may be treated as business activity instead of personal home use | If your documents do not clearly confirm your hosting model in writing, treat that as a coverage gap |

| Personal-use or long-term-tenancy liability terms during a paid short-term stay | A policy written for personal use or long-term tenancy can misalign at claim time | Do not rely on coverage that only might allow hosting |

| Platform protection for direct or other off-platform bookings | Platform protection is typically tied to bookings made on that platform | Do not assume the same protection applies unless current terms explicitly say so |

Guest-caused damage can miss standard policy language#

Standard homeowners coverage is generally not built for paying-guest damage in short stays, and short-term hosting may be treated as business activity instead of personal home use. That mismatch is where common losses can break. It can affect guest-caused damage, theft or burglary during a paid stay, guest liability, and lost business income.

Use the policy wording as your checkpoint. If your documents do not clearly confirm your hosting model in writing, treat that as a coverage gap.

Liability risk changes when occupancy use changes#

Liability outcomes can change based on how the property was being used at the time of the event, not just on the fact that an injury happened. If a stay is paid short-term occupancy, a policy written for personal use or long-term tenancy can misalign at claim time. Some insurers may allow infrequent hosting through a rider or even a homeowners policy, but that varies by carrier and terms. If that exposure would materially affect your finances, do not rely on coverage that only might allow hosting.

Platform protections are useful, but usually channel-limited#

AirCover and Vrbo protections can be helpful layers, but platform protection is typically tied to bookings made on that platform. For direct or other off-platform bookings, do not assume the same protection applies unless current terms explicitly say so.

Dedicated short-term rental insurance is designed for short stays, often framed as 30 days or less. It is positioned to cover property, liability, and income across booking channels. It still has exclusions, so the real goal is fit: match coverage to how you host, channel by channel, and keep written confirmation with your policy records.

Next, choose a policy type that fits your operating model instead of forcing your operating model into a policy built for something else.

We covered this in detail in The Best Software for Managing Short-Term Rentals.

Choose policy type based on how you rent#

Choose your policy based on how you actually host: frequency, booking channels, and how much your budget depends on rental income. If you host infrequently on one platform, a rental rider may be worth exploring. If you run a whole property, cross-list, accept direct bookings, or rely on the income, a dedicated short-term rental policy with clear liability and income-loss terms is often the safer fit.

As use shifts from personal residence to rental use, policy treatment can change. Many homeowners or dwelling policies are not designed for short-term-rental accident exposure, so a setup that felt fine for personal use can break at claim time once paid guest stays become regular.

Start with frequency and channel mix#

For occasional hosting, a rider can be worth checking because it is an add-on often presented for infrequent renting. But treat it as a possibility, not an assumption. Get written confirmation that your insurer accepts your exact paid-guest setup.

Channel mix is the next checkpoint. Platform protection generally applies only to stays booked on that platform. Once you list across multiple platforms or take direct bookings, look for coverage that follows all booking sources, not just one trigger.

Spare room versus full-property operation#

A spare room with infrequent one-platform stays is the closest case to "a rider might be enough." Even then, confirm in writing how liability and guest-caused losses are handled during paid stays. Also confirm whether coverage depends on platform-only bookings.

A whole property listed across multiple channels can look more like ongoing rental use than incidental home sharing. In that setup, dedicated vacation-rental or short-term-rental coverage is often a stronger match because these policies are positioned to address property, liability, and rental-income risk across booking sources.

When vacation rental insurance may be enough#

Vacation-rental coverage may be enough when one policy clearly handles property damage, liability, and lost rental income for your real operating model, including channel mix. Some policies frame short stays around rentals of 30 days or less, but that is a policy framing point, not a universal rule.

Before binding, read declarations, endorsements, and exclusions together. If occupancy use, booking model, or channel scope is unclear, treat that as a coverage gap until it is clarified in writing.

When commercial liability terms become hard to skip#

Commercial liability is not mandatory in every scenario, but liability terms can become harder to treat as optional when guest injury exposure is financially material and bookings run across platform and direct channels. The core question is simple: do your documents clearly provide paying-guest liability coverage across every booking source you use?

Whether liability is bundled into a short-term-rental form or purchased separately matters less than scope clarity. If scope is incomplete, lower price alone can be a false economy.

| Host profile | Likely policy path | Minimum questions to ask your insurer |

|---|---|---|

| Spare room in your primary home, infrequent one-platform stays | Rental rider may be worth checking | Does my homeowners policy accept paid guest stays in an owner-occupied home? Is guest injury liability covered? Is approval limited to platform-booked stays only? |

| Whole home rented occasionally, one platform only | Rider or dedicated vacation-rental policy, depending on insurer acceptance | Is the home treated as personal or rental use? Are guest-caused property losses and liability claims covered during paid stays? Is any loss of rental income included after a covered loss? |

| Whole property across multiple platforms | Dedicated short-term-rental or vacation-rental policy (often the better fit) | Does coverage apply across both platforms? Are stays of 30 days or less accepted under this form? What exclusions apply to paying-guest liability? |

| Whole property with multiple platforms and direct bookings, and you rely on the income | Dedicated short-term-rental coverage with broad liability and income-loss terms (and confirm whether separate liability coverage is needed) | Are direct bookings covered on the same terms? How is lost rental income triggered and calculated? Is liability coverage included across all booking sources or sold separately? |

Watch for operational creep: a setup can start with one room and one platform, then add channels or direct repeat guests without updating coverage. If you accept off-platform stays or depend on rental income, prioritize clear liability and income-loss scope over the lowest quote.

Once you know the policy type you need, verify that the rest of the setup actually allows you to use it.

If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

What to verify with your lender, permit office, and insurer before listing#

Before you publish, verify three things in order: lender requirements, local permit rules, and insurer approval for your exact booking model. That order is practical, not a universal legal rule, and it helps you avoid setting up coverage for a use you may not be able to run.

Start with the lender#

If the property is a mortgaged secondary or vacation home, your lender may require homeowners insurance, and secondary-home policies can include extra stipulations tied to part-time occupancy. Confirm both the baseline insurance requirement and any occupancy-related stipulations that apply. Ask for written confirmation and save it with your loan and policy documents.

Then verify local permit and licensing rules#

Permit and insurance requirements are jurisdiction-specific, so check the rules where the property is located. Local approaches can include licenses or permits, and some locations may also reference liability insurance.

Confirm:

- whether short-term-rental use is allowed for that address or property type

- whether a license or permit is required before bookings

- whether local materials reference insurance proof

- whether local rules distinguish between hosting arrangements

If a requirement is unclear, treat it as not approved yet.

Then get insurer approval for your real operating model#

This is where your setup has to match your documents. Regular homeowners coverage may be insufficient for short-term rentals, and platform protection is not the same as insurer approval of your policy terms. Available AirCover material references $1 million USD in liability or legal liability coverage, and it also notes exclusions.

Be explicit about:

- which booking channels you use, including direct bookings

- spare-room versus whole-home occupancy

- whether the home is primary, secondary, or purely rental use

- whether rental income is operationally important

| Party to verify | What to confirm | What to save |

|---|---|---|

| Lender | Whether homeowners insurance is required for a mortgaged secondary home and whether occupancy-related stipulations apply | Written confirmation plus relevant loan terms |

| Permit office | Whether permits or licenses are required and whether local rules reference liability insurance | Permit page or portal record, application or approval records, published requirements |

| Insurer | Whether policy terms fit your actual short-term-rental use, booking channels, and occupancy style | Declarations page, endorsements, exclusions, and written confirmation |

Keep declared operations aligned with reality#

Coverage issues can arise when operations drift from what was declared. If you expand from one channel to multiple channels, add direct bookings, or shift from room-share to whole-home stays, re-verify and document the change.

Keep a simple verification file and review it at least annually, including an up-to-date home inventory. The goal is fit, not maximum coverage: over-insuring can waste money.

Once those approvals are in place, set up your records before the first stay rather than trying to reconstruct them after a problem.

Need the full breakdown? Read What is Cyber Liability Insurance and Do Freelancers Need It?.

Build a claim-ready evidence pack before first guest#

Build your claim file before the first guest, not after an incident. Once you accept that first booking, your risk profile changes, and clear records can make the difference between a smoother claim and a dispute.

A practical evidence pack should help you show two things: property condition around each stay, and consistency between your hosting activity and what you disclosed to your insurer.

What to keep together#

Use one repeatable file structure and keep practical records like these together:

| Record | Article detail |

|---|---|

| Policy documents | Declarations page, endorsements, exclusions, and insurer claim contacts |

| Platform contacts | Platform claim or support contacts for the channels you use |

| Booking terms | Guest terms or house rules shown at booking |

| Stay evidence | Before-and-after stay condition photos |

| Incident file | Incident notes and related communication records |

At a minimum, keep those items in one place you can reach quickly. These are operating records, not a universal insurer-mandated checklist.

Keep policy documents next to stay evidence#

Store policy documents and booking evidence in the same place so you can match an incident to the right coverage path quickly. Your standard homeowners policy may not cover guest-related incidents, and platform protections are not the same as a full insurance policy and can have limits.

Failure modes to avoid#

Common claim friction points include record gaps:

- incomplete property-condition documentation around a stay

- hosting records that conflict with insurer disclosures

- scattered incident notes or communication records after an incident

If your records contradict what you disclosed, you can trigger a misrepresentation dispute and risk coverage being voided.

Make retrieval routine#

Use a simple, repeatable storage habit so records are easy to find under time pressure. One property folder, one reservation subfolder, and the same set of documents each time is usually enough to keep your process consistent.

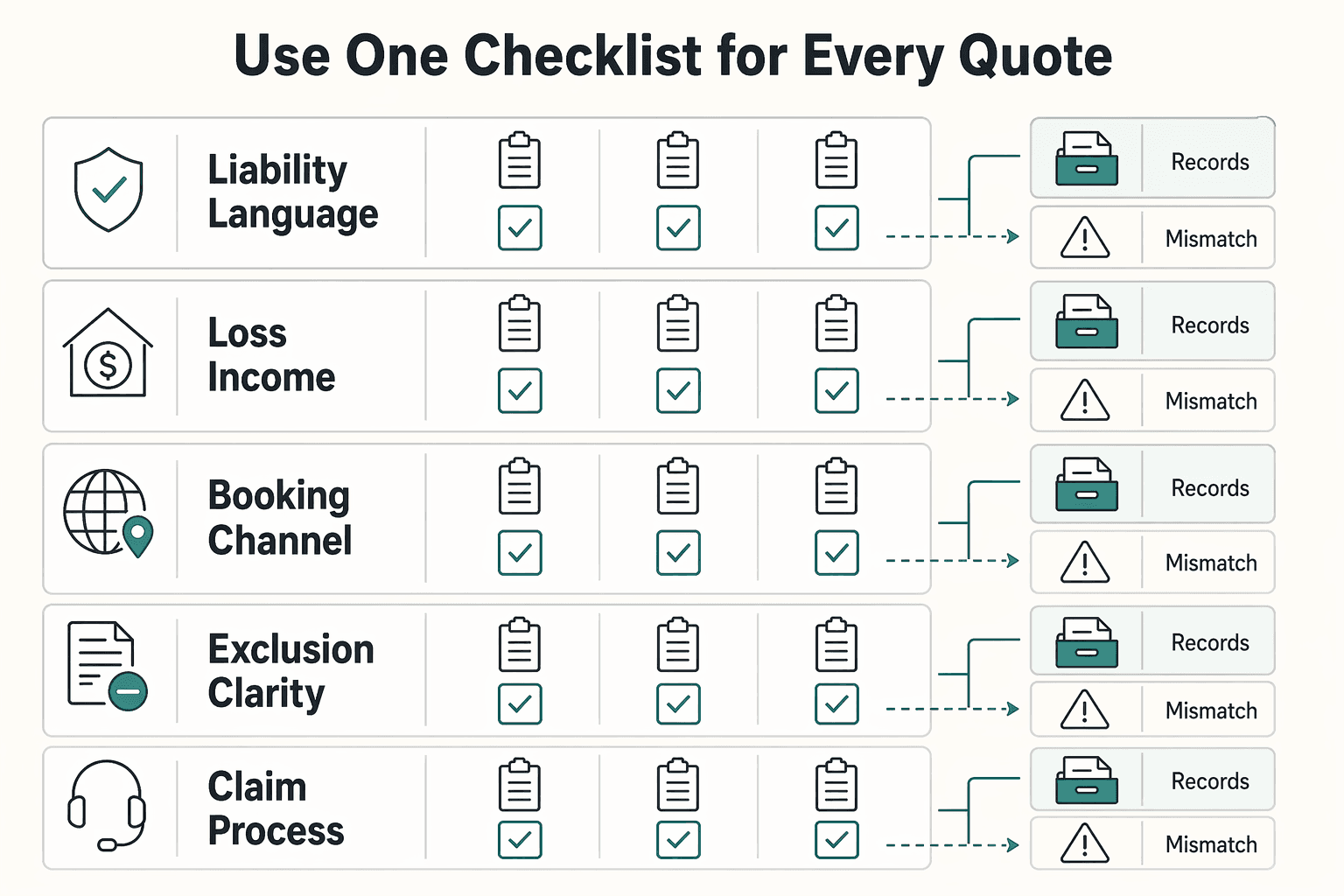

Compare quotes without getting tricked by price-first marketing#

Compare fit first, then price. The most useful quote is the one that matches how you actually host, with terms documented in writing.

A low headline premium does not tell you whether two quotes are truly comparable. Use one checklist for every quote, then compare written answers side by side.

Use one checklist for every quote#

| Comparison point | What to verify | Why it matters |

|---|---|---|

| Liability language | Whether paid guest activity is clearly contemplated and matches your actual setup | Helps keep your review tied to actual use |

| Loss-of-income logic | What has to happen before income loss is considered | Income-risk terms can differ from property-damage terms |

| Booking-channel treatment | Any assumptions the quote makes about where bookings come from | Different assumptions can make price comparisons uneven |

| Exclusion clarity | Hosting or business-use exclusions in plain language | Written exclusions can change how quotes compare |

| Claim process expectations | How claims start, what documents are usually requested, and any required reporting path | Documentation requirements can differ across quotes |

Use a simple operator rule: send the same five questions to each provider, and save the quote version, proposal, exclusions, and written replies in your policy records. File discipline is a practical risk-control habit, not admin busywork. Before you compare price, confirm the basics match reality: property address, named insured, occupancy style, and booking model.

Treat market articles as question generators#

Market articles can help you build your question list, but they are not substitutes for quote documents. Some market content can be incomplete, access-limited, or published in test environments, which can prevent full term-by-term verification. Use those articles for vocabulary, then verify against actual quote documents and seller responses in writing.

Follow the operating-model rule#

If you are still deciding whether separate short-term rental insurance makes sense, use one rule: choose the policy that fits how you host now. If you rely on rental income, pressure-test income-loss triggers. If a quote blends different risks in marketing language, ask for exact terms in writing.

Red flags are simple: non-equivalent quotes presented as comparable, or a rep who will not confirm exclusions and key assumptions in writing. If you cannot attach those details to your file before binding, keep shopping.

If a quote still leaves you guessing, that is not a small paperwork issue. It is a sign to pause and clarify before binding.

Red flags that should stop you from listing this week#

Pause your launch if any of these are true, then fix them before your first guest.

| Red flag | Why it matters | Article note |

|---|---|---|

| Your current insurer cannot clearly map paid guest stays to your actual setup | Paid guest activity is often treated as business use, and undisclosed rental activity can lead to coverage loss or cancellation | If your homeowners insurance or landlord insurance treatment is still vague, assume there is a gap |

| You are relying only on AirCover or Vrbo protections while hosting across channels | Those programs are platform-specific and include exclusions, so they are not a full foundation by themselves | If you cannot clearly explain what coverage applies across your booking mix, stop and resolve it first |

| You cannot explain your liability coverage and loss of income coverage in plain language | You should be able to state what could trigger each one and what likely would not | Pause your launch if any of these are true, then fix them before your first guest |

If any of these still apply, stop and resolve them before you go live. For platform-specific detail, see A Guide to Airbnb's Host Protection Insurance (AirCover).

15-minute pre-listing checklist for independent hosts#

Before you go live, run a documented go or no-go check: make sure your exact setup and booking channels match coverage your insurer confirms in writing.

- Define your setup and channels in one sentence.

Write down the property type, whether guests book a room or the whole place, and which channels you will use, for example platform-only or mixed with direct bookings. Then ask your insurer to confirm in writing that this exact setup is covered. Keep it specific. Traditional homeowners and landlord or dwelling policies were not built for short-term rental risk, and short-term rental activity can void coverage under many standard policies.

- Get written confirmation before publishing availability.

Treat "Confirm Licences & Insurance" as a hard pre-launch checkpoint. Verify any licence or permit requirements that apply in your area and confirm insurer acceptance for your stated model. Save written proof, such as an email, portal message, or policy note, not just a phone reassurance.

- Check the protections you are most likely to need.

Review where your documents address property damage coverage and liability coverage. If your policy includes loss-of-income terms, note how they apply to short-term rental activity. You do not need to master every clause in one pass. You do need each item to be clearly addressed, with any channel limits or exclusions identified.

- Build your claim-ready evidence pack now.

Save your declarations page, endorsements, exclusions, insurer contacts, and written confirmations in one folder, plus a simple incident-log template. This reduces delay if something goes wrong. It also helps if coverage is challenged later, including cases where earlier short-term rental activity is argued to have compromised the policy.

If any item is still unclear, keep the listing offline until it is resolved.

Related reading: A Guide to Local Regulations for Short-Term Rentals.

If you are adding direct bookings to your hosting model, pressure-test your payment and payout workflow before going live with a quick Gruv consult.

Conclusion#

If you take paying guests, separate short-term rental coverage is usually the practical default. Your risk profile changes with guest stays, guest-caused damage, and liability exposure.

The decision should come from policy terms and your real hosting setup, not marketing labels. Confirm your exact setup directly with your insurer before relying on coverage. Some insurers may allow infrequent rentals under an existing policy, but you need that confirmed for your specific case.

Before you go live, do three checks: review the actual policy wording, confirm lender requirements, and verify how property damage and personal liability are covered. In Texas, home insurance is not required by law, but your lender can still require it if you still owe on the home, so do not treat "not required by law" as "not required for you."

The common failure mode is assumption. If you rely on homeowners coverage without verifying fit, claim-time surprises are more likely. Match coverage to how you actually host, then list only after your insurer confirms your setup is covered.

Once your insurance setup is confirmed, tighten the money side of operations with traceable disbursements through Gruv Payouts.

Frequently Asked Questions

Do you legally need short-term rental insurance if you only host occasionally?

Rules vary by jurisdiction, so do not assume a universal rule. In Massachusetts, Chapter 337 of the Acts of 2018 requires at least $1,000,000 in liability insurance per short-term rental, whether or not you use an online hosting platform. If you host there, occasional use does not remove that requirement.

Is Airbnb AirCover enough, or do you still need separate short-term rental insurance?

In Massachusetts, it can be enough for liability in some cases, but only if the platform coverage meets or exceeds the required amount. Massachusetts also says regulators do not review individual host-platform coverages, so you need to verify details yourself with the platform and a licensed insurance producer or attorney. For platform-specific context, see A Guide to Airbnb's Host Protection Insurance (AirCover).

Will homeowners insurance cover Airbnb guests in a spare room setup?

Usually, you should not rely on standard homeowners coverage for paid guest stays. Dedicated short-term rental coverage is designed to provide property and liability protection that homeowners policies typically do not. AirDNA also notes standard homeowners or landlord policies usually do not cover guest-related incidents.

What does short-term rental insurance usually cover that landlord insurance may not?

Short-term rental insurance is built for the risks of hosting paying guests on short stays, especially guest-related property damage and liability exposures. Standard homeowners or landlord policies and platform protections can leave gaps. Even with dedicated coverage, check exclusions such as wear and tear, intentional renter damage, and some natural disasters.

When should you move from a rental rider to commercial short-term rental insurance?

There is no universal booking-count or revenue threshold you can apply everywhere. Revisit your coverage when you add off-platform bookings or need protection for lost income, since platform protections may not cover those situations. At that point, ask your insurer to confirm in writing whether your current coverage still fits your exact operating model.

What should you verify first before listing a property on Airbnb or Vrbo?

Verify that your exact booking model is covered: room or whole place, and platform-only versus mixed or off-platform bookings. In Massachusetts, confirm whether platform coverage reaches the $1,000,000 liability minimum; if you rent without a platform, you may need a supplemental dwelling insurance policy. Also confirm whether your policy addresses property damage, liability, and lost income so you do not rely on protections that may not apply.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/committee-print/119th-congress/house-committ...trusted

- hud.gov/sites/dfiles/OCHCO/documents/52641ENG.pdftrusted

- journals.law.harvard.edu/jol/wp-content/uploads/sites/86/2016/02/HLL1...trusted

- mass.gov/info-details/short-term-rental-insurancetrusted

- mn.gov/commerce/insurance/other/vacation-property/i...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- offcampushousing.unt.edu/resourcestrusted

- sealbeachca.gov/Portals/0/Documents/Proposed%20Budget%20FY%2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

AirCover Is Backup for Hosts, Not Your Primary Insurance Plan

Before you rely on AirCover for Hosts, build your own base first. You need a legal setup you can defend, a policy that clearly allows how you host, and a simple exposure worksheet so you know what you are trying to protect.

The Pros and Cons of Short-Term vs. Long-Term Rentals

You are probably not chasing the biggest headline revenue number. You want rent that arrives, stays collected, and does not turn into a second job or a cross-border tax headache. For an owner living internationally, the real choice between a short stay and a long-term lease is about risk first. Which model gives you lower compliance exposure, less remote operating drag, and more cash left after fees, taxes, and reporting?