Quick Answer

Choose policy type first: start with Travel Insurance for trip disruption and emergency events, or International Health Insurance for long stays with likely ongoing care. Then compare providers on one pass/fail card covering Coverage Area, Pre-existing Conditions, Deductible, repatriation wording, and major exclusions. Keep any unclear item in a needs verification column, and do not buy until your policy certificate, active dates, and emergency contact steps are confirmed in current provider documents.

Introduction: Pick the Right Nomad Insurance Before You Fly#

Use focused time now to avoid expensive mistakes later. Start with a practical digital nomad health insurance comparison, then map your route in Gruv's visa planner so we anchor policy checks to your real plan before pricing pages pull you off course.

This is for remote professionals planning a move or long stay, especially when insurance details must align with your travel plan and fixed departure dates. The goal is not to find the most polished provider page. It is to confirm that the policy you buy matches how you will actually travel, what kind of care you may need, and what proof you may have to show before or after arrival.

Skip generic top-10 lists. Use a yes-or-no decision path that filters out plans that read well in summaries but fail your actual trip. Follow this sequence:

- Type first: start with insurance type, not brand. If your main risk is trip disruption and emergency events, begin with

Travel Insurance. If your plan includes a longer stay and ongoing care needs, start withInternational Health Insurance. - Define gates: set go or no-go criteria before comparing providers. Examples: geographic scope, emergency care wording, repatriation wording, pre-existing condition handling, and policy effective dates.

- Score like-for-like: compare the same criteria across

Safety Wing,Insured Nomads,Heymondo,Genki,PassportCard, andTrue Traveller. Keep one worksheet so each provider is judged on identical checks. - Verify documents: confirm official policy wording before purchase. Third-party comparisons help with orientation, but plan conditions can change, so unresolved items stay in a

needs verificationcolumn.

That order matters because each stage removes a different kind of mistake. Insurance type removes category errors. Non-negotiables remove plans that can never work for your route. Provider comparison helps you rank only the options that survive. Official wording resolves the details that summary pages often smooth over.

Use that sequence as a gate, not as a browsing suggestion. A provider should not move forward just because the landing page looks polished or the price feels attractive. If the policy type is wrong, or if must-have clauses are still unclear, you are not comparing real options yet. You are comparing impressions.

The checkpoint that matters most is simple: confirm the policy certificate, active dates, and exact wording for must-have items before you fly. If a provider page and an article summary conflict, trust current provider documents and pause the shortlist until the gap is resolved.

In practice, keep one worksheet for the entire process. Use the same lines every time: plan type, Coverage Area, Policy Exclusions, Pre-existing Conditions, Deductible, Medical Repatriation, policy start date, and claims path. If a detail is not confirmed in current provider materials, mark it unresolved. Do not fill the gap with assumptions because the headline summary sounds broad enough.

Make each note traceable. If a detail came from a comparison article, mark it as orientation only. If it came from current provider wording, mark it as verified. That way, if two notes conflict later, you know which document needs a second look. The worksheet is not only for comparison. It is also your record of why a plan survived the shortlist in the first place.

A common failure mode is straightforward: choosing a cheap plan from a comparison post, skipping wording checks, then paying out of pocket when an event is excluded. A disciplined first pass prevents that.

At-a-Glance Comparison of Top Digital Nomad Insurance Options#

Use this as a verification screen, not a ranking: separate what is confirmed from what needs provider-level confirmation before you shortlist. For route prep, keep insurance notes next to the digital nomad visa cheatsheet.

Travel Insurance is generally described as covering travel-related incidents (like accidents, baggage loss, and delays), and nomad-focused insurance is often described as a hybrid with travel-incident coverage plus broader health-style benefits.

| Criteria | SafetyWing | Cigna Global | Insured Nomads | World Nomads | True Travlr |

|---|---|---|---|---|---|

| Best-fit traveler profile | Mentioned in one comparison source; exact fit unknown | No confirmed detail in this evidence pack | Mentioned in one comparison source; exact fit unknown | No confirmed detail in this evidence pack | Mentioned in one comparison source; exact fit unknown |

Travel Insurance or International Health Insurance focus | Unknown, verify official plan type | Unknown, verify official plan type | Unknown, verify official plan type | Unknown, verify official plan type | Unknown, verify official plan type |

Coverage Area including United States options | Unknown, needs policy check | Unknown, needs policy check | Unknown, needs policy check | Unknown, needs policy check | Unknown, needs policy check |

Emergency Medical Treatment and Medical Repatriation scope | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check |

Trip Cancellation Coverage and baggage/travel disruption | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check | Unknown, needs policy wording check |

Pre-existing Conditions stance | Unknown, needs inclusion/exclusion review | Unknown, needs inclusion/exclusion review | Unknown, needs inclusion/exclusion review | Unknown, needs inclusion/exclusion review | Unknown, needs inclusion/exclusion review |

Deductible structure and tradeoffs | Unknown, verify current terms | Unknown, verify current terms | Unknown, verify current terms | Unknown, verify current terms | Unknown, verify current terms |

Major Policy Exclusions to verify | Unknown, confirm exclusions directly | Unknown, confirm exclusions directly | Unknown, confirm exclusions directly | Unknown, confirm exclusions directly | Unknown, confirm exclusions directly |

| Evidence confidence (confirmed vs unknown) | Medium for provider mention, low for plan specifics | Low | Medium for provider mention, low for plan specifics | Low | Medium for provider mention, low for plan specifics |

A row full of unknowns is not a negative review. It is a signal that the provider has not yet earned a place on your paid shortlist because the items that matter are still unverified. That distinction matters. Unknown does not mean bad. It means unresolved.

To make this table useful, turn every blank into a question you can answer from provider materials. If a cell says unknown for geography, write the exact geography question beside it. If a cell says unknown for claims, note what you need to confirm about first contact, document requirements, or claim-start instructions. We grade each unresolved cell at 0%, 25%, 50%, 75%, or 100% clarity before moving it forward.

How to read this table: a cheaper headline is not a better choice if policy wording does not match your trip needs. Treat the table as a live worksheet. Next to each unresolved cell, note the exact question you still need answered, such as whether the policy type is really the right lane, whether the geography fits your route, or whether claims instructions are clear enough to use under pressure.

Also keep provider familiarity separate from confirmation. A provider that appears often in articles can feel safer simply because you have seen the name more times. That is not evidence about your route, your claim scenario, or your document requirements. Only confirmed wording should move a provider out of the unknown column.

Checkpoint before shortlist approval: if any key cell is unclear or below 90% clarity, keep that provider in needs verification until official, current provider materials confirm what is included, excluded, and how claims are handled. If a provider looks attractive only because you are mentally filling in blank cells, it is not ready for a serious comparison.

Decide Insurance Type First So You Do Not Compare the Wrong Products#

Pick the insurance type before you compare brands. Travel Insurance is built around trip costs and unexpected emergency medical costs, whereas longer stays with likely non-emergency care needs usually call for starting in the International Health Insurance lane and checking policy wording carefully.

For digital nomads, risk patterns are often different from short vacations, so this split matters early. If you skip it, you can end up comparing plans that solve different problems.

A fast way to decide is to write a single sentence describing your likely first use of the policy. If the sentence is mostly about cancellations, delays, expensive equipment, and emergency incidents while moving across borders, that points you toward the Travel Insurance lane. If the sentence is mostly about a longer stay, continuity, and non-emergency care needs, start with International Health Insurance. The labels on provider pages matter less than that use case.

Then pressure-test that first sentence with the rest of the trip. If your first likely use points one way, but the longer-stay reality of the plan points another way, pause there. That tension usually means you are still mixing categories. It is better to catch that at the beginning than after you have already compared quotes that were never solving the same problem.

Use this rule before you shortlist:

- Long-stay lane: start with

International Health Insurancewhen non-emergency care continuity is likely. - Movement lane: start with

Travel Insurancefor multi-stop travel with higher disruption risk (cancellations, delays, gear loss, emergency incidents). - Unclear route: start with your biggest travel-risk concerns, then confirm whether broader health-style coverage is required.

Quick contrast: someone relocating to one country with regular care expectations should not start from the same product type as someone moving across countries with expensive equipment and high trip-disruption exposure.

What usually goes wrong here is simple. A traveler sees that multiple products mention medical coverage and assumes they are close substitutes. They are not necessarily substitutes if one is centered on emergency events and the other is a better fit for longer-term continuity. That is why type comes before brand.

The error is not only comparing the wrong prices. It is solving the wrong problem well. A plan can be good within its own category and still be a poor match for your trip. That is why category fit has to feel almost boringly clear before you spend time ranking brands.

Red flag: cancellation flexibility can be optional rather than automatic, so treat these details as plan-specific until verified in current policy terms. The same caution applies to any feature that sounds broad in a summary but becomes narrower in policy wording.

Set Your Non-Negotiables Before You Look at Price#

Set pass-or-fail criteria first, then compare price. A lower premium is only relevant after a plan clears your minimum requirements.

This is the point where vague preferences turn into decision rules. "Looks comprehensive" is not a rule. "The Coverage Area matches where I will actually be, and the exclusions are acceptable for my route" is a rule. If you cannot state the requirement clearly, you cannot compare providers cleanly.

Keep hard requirements separate from preferences. A cleaner dashboard, a smoother quote flow, or a small headline saving can matter later, but those are not in the same category as route fit, usable emergency wording, workable deductible, or acceptable exclusions. If you mix them together too early, presentation quality starts doing the job that policy wording should be doing.

Use one requirements card for every option, and keep each item binary (meets it or does not):

- Coverage Area for your actual travel pattern, including whether

United Statesaccess is required. - Pre-existing Conditions language you can accept.

- Deductible you can realistically handle if you need care early.

- Medical Repatriation terms that match your risk tolerance.

- Policy Exclusions wording for your most likely scenarios.

For each line, copy the exact wording or keep a clear note tied to the exact wording. Avoid notes like "probably included" or "seems fine." Those are the notes that create problems later, because they do not tell you what was actually confirmed.

If a provider makes the relevant clause hard to find, treat that as a reason to slow down, not as permission to assume. Difficulty locating the rule does not make the rule less important. It only increases the chance that you will rely on memory or marketing language instead of the actual document.

The Deductible check is especially practical. Do not treat it as an abstract tradeoff. Ask whether you could absorb that amount if you needed care early in the trip, before any claim is processed. If the answer is no, the plan may be a poor fit even if the headline price looks attractive.

Apply one rule with 0% exceptions: if a plan fails one non-negotiable, remove it, even if it is cheaper. Decision order: if U.S. access matters, verify Coverage Area terms first; if not, prioritize exclusion clarity and the rest of your card. Treat vague wording as unresolved, not acceptable.

That last point matters because ambiguity can quietly act like a discount. An unclear policy often looks competitive simply because the hard questions are still unanswered. The discipline here is to count ambiguity against the plan until it is resolved, not in its favor.

A good way to pressure-test Policy Exclusions is to read them against the scenario most likely to happen to you, not the rarest disaster. If your plan involves border movement, long stay timing, equipment risk, or concern about pre-existing-condition language, those are the scenarios your notes should focus on. The exclusion review should answer, in plain language, whether the policy still works for the trip you are actually taking.

Before moving any provider into your final two, copy the exact Policy Exclusions wording into your notes from current policy documents.

If you want a travel-first companion piece, read The Best Travel Insurance for Digital Nomads.

Match Provider to Trip Pattern and Risk Profile#

Choose by trip pattern, not popularity: the best fit depends on how long you stay, how often you cross borders, and the protection you expect.

After your pass/fail filters, compare SafetyWing, Cigna Global, Insured Nomads, World Nomads, and True Travlr against your movement pattern first, since that is where gaps often appear. Nomad-focused policies are often positioned for longer stays and frequent border crossings, and many standard travel policies may limit long stays, repeated trips, or activities treated as work.

Trip pattern is the operating context for every other clause. A plan can look fine in isolation and still be wrong for the way you move. That is why the route comes before the ranking.

Write the trip as a route, not just a duration. A long single-base stay creates one set of checks. The same overall period spread across multiple countries creates a different review, because geography wording, duration limits, and border movement all matter more. Even if your later stops are tentative, include them in your notes so the comparison reflects the trip you might actually take.

- Single-base stay for months: prioritize

International Health Insurancedepth and continuity wording, then reviewPre-existing Conditionslanguage. - Regional hopping with frequent border changes: prioritize duration limits, country restrictions, and movement-related terms that could interrupt coverage.

- Frequent returns home with changing routes: prioritize route-fit rules so border movement and stay length do not create accidental gaps.

If you carry expensive equipment and your itinerary is volatile, weight Trip Cancellation Coverage and disruption terms higher than small price differences. If treatment continuity matters more, prioritize health coverage depth and Pre-existing Conditions terms over trip perks.

Write out your likely country sequence before final ranking, even if some later stops are tentative. That exercise forces you to check where coverage could break: at a border crossing, at a duration limit, or when the route changes from the original plan. If the sequence itself reveals uncertainty, that is not a reason to stop checking. It is a reason to put more weight on geography wording and movement-related terms.

A rough route note is often more useful than a polished provider score. It tells you where the comparison has to be strongest: before entry, during movement, or during a longer stay. It also keeps both finalists honest, because each provider is being tested against the same route rather than against a simplified version of your plan.

Before final ranking, map your likely country sequence and confirm restrictions, duration limits, and visa-related coverage rules in current policy documents and your visa planner.

Use a two-provider shortlist:

- Finalist 1: provider, why selected, main risk, what must be confirmed before purchase.

- Finalist 2: provider, why selected, main risk, what must be confirmed before purchase.

You can also add a short note for each finalist that answers one practical question: what would most likely make me use this policy first? That helps separate a provider that looks broad on paper from one that fits your real exposure. If a provider only stays competitive because you are assuming away an unclear clause, it is not truly competitive.

Keep both finalists on the same page and in the same format. The more consistent your notes are, the easier it is to see whether one option is actually stronger or just better explained in your own worksheet.

Do not purchase until both finalists have no unresolved questions on duration limits, border movement rules, and your highest-risk scenario.

Hidden Policy Traps That Create Claim Problems#

Most claim problems are created at purchase, not at the moment of emergency. If you buy quickly and skip wording checks, you can discover too late that the policy is built for short-trip events, not longer stays.

This is where similar-looking options separate. Traditional travel policies are often framed for short, defined trips and may cap duration at 30 to 90 days, which can break coverage for longer plans. Purchase timing is another common trap, since some policies may not cover you if you buy after departure.

Read this section as a purchase audit. The question is not just whether the benefit exists somewhere in the marketing copy. The question is whether the wording is clear enough that you could explain to yourself how the policy would respond to your trip pattern.

A practical way to review each important clause is to ask what event triggers the benefit, what conditions limit it, and what evidence you would probably need later. If the clause sounds reassuring but you still cannot describe those basics in your own notes, the benefit is not really clear yet. That is often where claim problems start.

Watch these red flags before you pay:

- Emergency Medical Treatment language is narrow or unclear.

- Policy Exclusions are broad, vague, or not tied to your trip pattern.

- Medical Repatriation terms are unclear on when it applies.

- Pre-existing Conditions wording is unclear.

- Claims evidence expectations are not clear enough to prepare upfront.

- Duration terms do not match your planned stay.

- Cancellation wording is stricter than expected. One published World Nomads description says fear of travel is not a valid cancellation reason.

Each red flag needs an action, not just a note. Copy the relevant clause into your worksheet, write the scenario it must cover, and decide whether the wording answers the question or leaves room for doubt. If it leaves room for doubt on a non-negotiable point, the policy should stay unresolved until you get clarification or remove it from the shortlist.

If you ask support for clarification, save the question and the answer next to the clause. That is useful even when the answer is incomplete, because it shows exactly what remained unclear at the time of purchase. What you want to avoid is a vague memory that support was "helpful" without a clear link back to the wording.

Duration terms deserve extra attention because they are easy to ignore when you are focused on price. A duration limit can feel minor until your actual stay runs into it. At that point, the cheapest option may become the one with the biggest gap. The same logic applies to purchase timing. If a plan may not cover you after departure, that is not a detail to solve later.

Claims evidence expectations also matter before you travel, not after. If the policy does not make the claims path clear enough for you to prepare your document pack, that is already a usability problem. A process you cannot follow quickly is risky even if the benefit sounds strong in a summary.

Before purchase, imagine your most likely claim scenario and ask whether the evidence path is clear. What document would you show first? Which contact method would you use? What clause would you point to if you had to confirm eligibility? If those answers are fuzzy, the policy is operationally weaker than it looks.

Marketing summaries often smooth over differences that matter during a claim. A broad sentence about medical cover does not tell you how the policy treats your dates, your movement pattern, or your exclusions. Claim decisions happen against the wording and the evidence, not against the shortest version of the plan description.

The failure pattern is consistent: buy fast, skip clause checks, hit an excluded event, then face denial or partial payout. Personal claim stories can be useful warnings, but treat them as anecdotal rather than proof of universal outcomes.

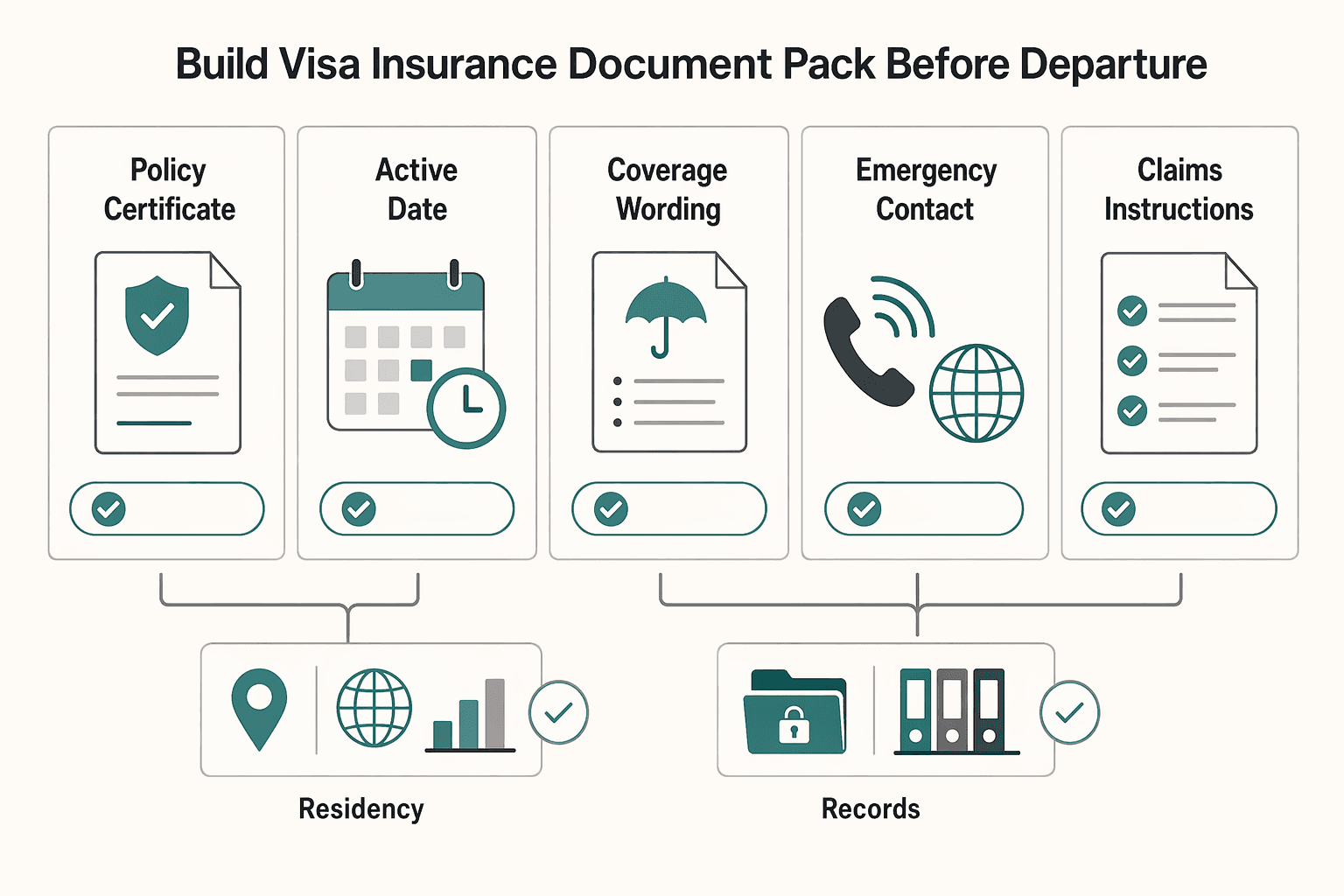

Build the Visa and Insurance Document Pack Before Departure#

For Digital Nomad Visa readiness, build one pre-departure pack that proves coverage and is usable in an emergency.

Visa review can work like multiple gates, each asking for specific proof. Keep this section answer-first: can you show active insurance for your entry plan, and can you use that coverage quickly if something happens? Before final submission, compare destination assumptions with CDC Travelers' Health, U.S. State Department travel guidance, and the WHO travel health overview.

Think of the pack as serving two separate moments. The visa-facing moment is about showing that coverage exists, that it is active, and that it applies where you say it applies. The emergency moment is about speed: who to contact first, what policy number to give, and which document to show without digging through a long policy file.

That split helps you design the folder well. The visa side should be short and easy to inspect. The emergency side should be fast to use when attention is low and time matters. One pack can do both, but only if the quick-proof documents sit on top and the fuller wording is easy to reach behind them.

| Pack item | Why it matters | What to verify now | If you skip it |

|---|---|---|---|

| Policy certificate | Core proof that cover exists | Name matches passport exactly | Extra review friction |

| Active-date proof | Confirms coverage window | Start date aligns with planned entry | Possible gap between arrival and policy start |

| Coverage wording extract | Clarifies what is covered | Coverage Area language matches destination plan | Border or consular friction |

| Emergency contact path | Enables fast first contact | Hotline, app, and first-call steps are saved | Delays in urgent care steps |

| Claims instructions | Sets evidence expectations | Required documents are listed in notes | Preventable claim delays later |

Arrange the pack so the short proof items are easy to pull up first, with the full wording behind them. If someone asks for evidence quickly, you do not want to hunt through the entire policy for the active dates or the geography wording.

Use this order:

- Download set: buy the selected policy, then save the certificate, wording, and confirmation email.

- Date gate: check effective dates against departure, arrival, and buffer days, with 0% mismatch tolerance.

- Identity gate: match legal name fields to passport spelling, including middle names, with 100% alignment.

- Access gate: save one cloud copy and one offline copy, then confirm 100% readability on your phone.

- Action gate: print a one-page summary with policy number, emergency contacts, and claim-start steps, and confirm at least 90% clarity.

Name files clearly enough that you can tell what each one is without opening it. The certificate, full wording, confirmation, and summary should each be obvious at a glance. If you are stressed, or if someone else needs to help you find the right file quickly, good naming matters more than neat folder design.

After that, do a practical access test. Open the offline copy once before departure. Confirm that the files you plan to rely on are actually readable on the device you will carry. A backup only helps if it is easy to use when you need it.

The pack is only ready when the short proof documents are fast to locate and the full wording is still attached for deeper checks. A readable file with an unclear name can still slow you down at exactly the wrong time. The goal is not just storage. It is quick, calm retrieval.

No clarity means no purchase.

Add a known unknowns box at the end of the pack. Log anything not clearly confirmed yet, such as unclear geography, uncertain activation timing, or vague claim evidence rules. If one unknown could affect visa review or claim handling, pause and get written clarification.

That known unknowns box is not administrative clutter. It keeps unresolved issues visible instead of letting them disappear into general confidence. A question that stays visible is much more likely to get resolved before departure.

It also helps to assign a next step to each unknown. Either find the clause, ask for clarification, or remove the provider. An unresolved item with no next action has a way of surviving right up to departure.

Our team uses a simple release gate: 100% name match, 100% active-date alignment, 90% claims-step clarity, and 0% unresolved exclusions before we approve payment.

If you are deciding between Travel Insurance and International Health Insurance in a close call, favor the option with clearer visa-facing documents and clearer emergency instructions. Clear documents reduce friction at the exact moments when ambiguity is most expensive.

Run a 14-Day Pre-Departure Verification Checklist#

Use this 14-day checklist as a final risk screen before departure, not as a legal or insurer-mandated standard. We treat it as a scorecard: 100% identity match, 100% policy-date alignment, 90% emergency-path clarity, and 0% unresolved entry blockers.

One reported nomad case described a $2,100 out-of-pocket bill after lacking usable international coverage, which is a caution example, not a typical outcome for everyone.

The point of a final checklist is not perfect certainty. It is to catch unresolved basics while there is still time to pause, ask for clarification, or stop a bad purchase from becoming a travel problem.

| Window | Verification focus | What to confirm | No-go trigger |

|---|---|---|---|

| Day 14-10 | Policy status and wording | Active policy status, support channel response, exact Policy Exclusions and Pre-existing Conditions language | Any clause you still cannot explain clearly |

| Day 9-5 | Emergency protocol | First contact step for Emergency Medical Treatment, escalation path for Medical Repatriation, and which document to present first | You do not know who to contact first during an emergency |

| Day 4-2 | Visa and access proof | Digital Nomad Visa file completeness, identity match across documents, cloud and offline copies | Name mismatch, missing certificate, or inaccessible offline copy |

| Day 1 | Final go or no-go | Geographic scope, Deductible, policy dates, and unresolved shortlist unknowns | Any unresolved unknown that affects entry or claim eligibility |

If a provider only moved forward because you intended to verify later, this is where that delay catches up with you. The checklist is a final compression of all earlier work, not a substitute for it.

Use each window for a different kind of check. During Day 14-10, do not only confirm that the policy exists. Confirm that you understand the wording well enough to explain the important clauses in your own notes. If your clarity is below 85% on exclusions or claims steps, pause and resolve that gap before moving forward.

During this first window, update the worksheet so it reflects the plan you actually expect to buy or have already bought. Old notes from earlier comparisons can create confusion if they sit next to current wording without a clear label.

During Day 9-5, rehearse the emergency path while you are calm. You want the first contact step to feel obvious, not something you must reconstruct under pressure. That means knowing where the contact details live, which document you would open first, and how the Medical Repatriation path would be escalated if needed.

If your route includes early movement after arrival, make sure those emergency details travel with you rather than sitting only in an inbox. This is less about organization and more about response speed. A good emergency path is one you can use without thinking too much.

During Day 4-2, test access rather than assuming access. Open the cloud copy and the offline copy. Check that the certificate is readable, the name matches, and the one-page summary is easy to find. If your route changed after purchase, this is also the right time to rerun the geography check and confirm the document pack still matches the trip.

A simple standard helps here: the pack should be usable even if you are tired, rushed, or handing the device to someone else to locate the policy proof. If it takes too long to find the certificate or the summary page, the pack needs work.

During Day 1, read the no-go triggers literally. "Almost resolved" remains unresolved if the issue affects entry, coverage geography, or claim eligibility. Treat this as a hard gate rather than a motivational checklist item.

Also make sure the final version of your notes matches the actual policy, not an earlier draft comparison. The last review should remove stale assumptions, old route notes, and any clause text that no longer applies.

During this window, contract wording should outweigh anecdotal reviews. Personal reviews can surface questions, but they are subjective and should not replace your own clause check.

Also verify duration fit. Some travel-focused coverage is described as a poor fit when care needs continue beyond 90 days, so confirm what happens after any initial coverage window.

Treat Day 1 as a hard gate. If geographic scope, start dates, or emergency contact steps are unclear, pause and get written confirmation.

Conclusion: Choose With Evidence, Not Marketing Copy#

Choose category first, compare providers second, and verify critical wording before you pay. Reversing that order leads to long comparisons of plans that were never a fit.

Start by separating Travel Insurance, nomad-focused plans, and International Health Insurance. Apply non-negotiables on geographic scope, exclusions, direct billing, and visa-document requirements where relevant. Then compare providers within the category that fits your situation.

Keep shortlist notes explicit. For each finalist, record why it fits, what remains uncertain, and what written confirmation is still required. This helps reduce late surprises during Digital Nomad Visa review or claim submission.

Good decisions here are usually unglamorous. You know which product lane you are in, you have a shortlist that survived your non-negotiables, and every important clause is either copied into your notes or confirmed in current documents. That process is more reliable than any marketing-heavy "best plan" ranking.

The right final choice is usually the one whose documents you understand, whose exclusions you can live with, and whose emergency steps you could actually follow without hesitation. That is a better standard than choosing the plan with the strongest headline or the most familiar name.

Use timeline as a reassessment trigger. If your stay extends past six months, re-check whether category fit still holds. Do the same when you change plans or carriers, since pre-existing-condition handling can reset at new plan boundaries.

Next step: complete your top-two shortlist and run the verification checklist today. Request a coverage letter, confirm geographic exclusions, and verify direct billing availability in destination countries. If our confidence is below 90% on any critical clause, we pause and re-verify with the digital nomad visa cheatsheet.

After purchase, keep the evidence pack current. If the route changes, if dates shift, or if a document is replaced, update the working file so your proof and your actual plan still match.

Final recommendation: trust the decision process over provider rankings. A category-first approach, clear caveats, and pre-departure verification will serve you better than any single best-plan list.

Frequently Asked Questions

What is the practical difference between `Travel Insurance` and `International Health Insurance` for digital nomads?

Travel Insurance is usually temporary trip protection, and medical scope is often centered on emergency stabilization and return-home treatment. International Health Insurance can be a better fit when you need longer-term continuity across locations. Start by matching policy type to trip pattern before comparing brands.

When is `Travel Insurance` not enough for a long stay?

It often becomes a poor fit when you expect ongoing care needs or uncertain return timing. If your trip may run longer than expected, verify how long coverage lasts before departure. Treat unclear duration language as a stop sign until you get written clarification.

What should I compare first: `Coverage Area`, `Policy Exclusions`, or claims process?

Start with geographic scope, because a plan labeled worldwide can still exclude your current location. Then review Policy Exclusions, and finally confirm claims steps and required evidence. That order eliminates plans that fail basic eligibility before you spend time on claims details.

How should I evaluate `Pre-existing Conditions` language across providers?

Treat this as a wording comparison, not a marketing comparison. Frequent moves can trigger repeated disclosures with different waiting periods, exclusions, or premium loading. Copy exact terms into your notes so you can compare like-for-like.

Do I need `United States` coverage if I am not planning to live there?

There is no single rule for everyone. Match geography to where you will live and transit, then verify location wording in writing. If U.S. access is irrelevant to your route, prioritize other non-negotiables first.

Which documents should I prepare for `Digital Nomad Visa` insurance proof?

Requirements vary by country, but visa screening is often framed around proof of remote income, background checks, and comprehensive expat medical insurance. For insurance proof, prepare clear evidence that your comprehensive cover is active and where it applies. Align the insurance details with the rest of your visa file.

What should I do if I change countries after buying a policy?

Re-check geographic scope and policy validity before the move. If the new location is unclear or excluded, request written confirmation and update your document pack before crossing borders. Do not assume the original plan still fits once routes change.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- cdc.gov/traveltrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12399223trusted

- travel.state.gov/content/travel/en/international-travel.htmltrusted

- bmispain.com/en/travel-insurance-for-digital-nomads-what-...external

- ipmiglobal.com/in-focus/digital-nomads-insurance/12-frequen...external

- nomadicmemoir.com/comparing-top-health-insurance-options-for-d...external

- now-health.com/en/blog/health-insurance-benefits-digital-no...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

How to Deal with Imposter Syndrome as a Freelancer

**Freelance impostor feelings can flare when your work lacks clear, documented boundaries-even when you *do* have talent.** You're the CEO of a business-of-one, and your job is to turn shaky moments into repeatable operations.