Quick Answer

For most solo professionals, the better choice is usually the home state, not Delaware or Nevada by default. The article explains that Delaware vs Nevada LLC branding does not by itself improve enforceable protection, tax treatment, or operating compliance. Start with your real risk, where you conduct business, whether an exception applies, and whether you can maintain any added registration and reporting load.

Stop Asking "Delaware or Nevada?" - Here's the Right Way to Build Your Liability Shield#

If you are a solo professional, stop treating delaware vs nevada llc like a brand choice. Much of the noise around this topic comes from corporate law, and that does not automatically translate into a better LLC setup in your day-to-day business.

Terms like Corporate Transparency Act and foreign qualification often get pulled into this debate, but the materials here do not establish specific CTA or foreign-qualification rules. The practical filter is simpler: prioritize what gives you enforceable protection, manageable compliance work, and clean operations.

Some of the current chatter comes from DExit, which frames Nevada as a challenger to Delaware. But the analysis behind that story is about corporate domicile and reincorporation of corporations from 2012 to 2024. Its findings are narrower than the headlines: Delaware has led corporate law for over a century, exits are described as minimal, and broad near-term spread is unlikely.

| Comparison point | State-brand promise | Operational reality | Practical consequence for a solo professional |

|---|---|---|---|

| Delaware | Prestige and a long corporate-law reputation | The cited support is about corporations, not a typical solo LLC decision | Prestige alone does not tell you whether your structure is easier to run or more protective in practice |

| Nevada | Framed as Delaware's challenger in DExit discussions | The cited support does not show a broad Delaware exodus, and does not prove a solo-LLC advantage | Treat broad state-brand claims as unproven until they match your exact entity and risk pattern |

| Delaware vs. Nevada debate overall | Sounds like the core decision | The strongest evidence here is about corporate reincorporation patterns, not one-owner LLC outcomes | Start with your operating reality and risk profile, then evaluate state choice |

Start with risk. Separate inside-business threats, outside-creditor threats, and any cross-border friction before you pick a state. That reframes the choice from "Which state sounds stronger?" to "Which setup can I actually defend, document, and maintain?" If you also want the banking side set up cleanly, see The 'Profit First' Method Part 2: Setting Up Your Bank Accounts.

Before You Ask 'Which State?', Ask 'What's My Real Risk?'#

Before you pick a state, define the risk you are actually trying to manage. For most people, the default is still straightforward: "For most people, it's best to form your LLC in your home state." The real question is whether your facts justify an exception.

Step 1. Name the risk before you name the state#

Start with three working buckets. If you skip this step, state choice turns into guesswork:

- Primary risk: the main problem you want the LLC setup to help you manage.

- Operating footprint: where you are actually "conducting business."

- Operational friction: the extra filings and ongoing compliance work you can realistically maintain.

This works better if you write one sentence for each bucket instead of keeping it abstract. Note what could go wrong in your business, where your work really happens, and what extra admin you realistically will or will not keep up with. If you cannot describe the risk in plain language, you probably are not ready to use state choice as the fix.

Step 2. Map where you actually operate#

This is the step people often rush past, and it is where many out-of-state filings stop looking efficient. Ask where you are really "conducting business." The source also warns that if you form out of state, you "probably need to register the out-of-state LLC in your home state." That word matters. Verify your facts before you file.

Use a plain-language operational checkpoint: where your work happens and where money is made. The same source gives the high-level tax checkpoint: "Taxes Are Paid Where Money Is Made." Use this practical flow:

- If you are mainly operating from one home state, including a home office, start with home-state formation as your baseline.

- If your activity or revenue spans more than one place, document that before choosing a state.

Do not do this from memory. Make a short operating map and keep it with your filing notes. List where you live, where you perform the work, where clients are located, where you invoice from, and where the money is received. You are not trying to create a law-school memo. You are trying to avoid a common mistake: choosing a filing state first, then discovering later that your real operating footprint still pulls you back into home-state registration or added compliance work.

Step 3. Compare options by durability, compliance load, and fit#

Once you know the risk and operating footprint, compare choices by what they change in practice, not by reputation alone. The source also notes there are 4 exceptions, so treat the default as a starting point, not a blind rule. It also warns that forming in Delaware, Nevada, or Wyoming can often be a bigger headache and cost more money.

| Option | Risk impact (verify) | Compliance load | Operational fit | Current fee check |

|---|---|---|---|---|

| Your home state | Default starting point when this is where you conduct business | Often lighter because you avoid starting out-of-state | Usually best first path for most owners | Current home-state requirement pending official or counsel verification |

| Delaware | Do not assume reputation alone changes risk outcomes | Can increase load if home-state registration is still required | Consider only with a verified exception | Current Delaware requirement pending official or counsel verification |

| Nevada | Do not assume out-of-state filing alone changes risk outcomes | Can increase load for the same reason | Consider only if your facts support it | Current Nevada requirement pending official or counsel verification |

| Wyoming | Do not assume out-of-state filing alone changes risk outcomes | Can increase load for the same reason | Consider only if your facts support it | Current Wyoming requirement pending official or counsel verification |

A useful way to test an exception is to force yourself to state the result you expect. Not "Delaware is stronger" or "Nevada is more private," but the exact operational result you think changes. If you cannot point to that result, the filing path is probably being driven by marketing language instead of your facts.

Before you move on, use this checkpoint:

- Identify your primary risk bucket.

- Write down where you are actually conducting business and where money is made.

- Use home-state formation as your provisional path unless you can verify an exception.

- If your setup is atypical or spans multiple places, keep a short fact file before you finalize.

- Confirm whether one of the 4 exceptions applies before filing.

If you want the broader asset-protection blueprint, we covered it in US LLC and BVI Company Blueprint for Asset Protection.

The Global Compliance Layer: How a US LLC Interacts With Your Expat Reality#

If you live and work abroad, the state-choice debate drops down the list. Your real decision is whether the LLC stays clean across tax, reporting, and invoicing everywhere you operate.

Tax treatment beats state branding#

State branding does not determine your federal tax treatment. Your LLC's federal tax treatment comes from IRS classification rules, not from whether you file in Delaware or Nevada. The IRS classification depends on member count and elections, and a single-member LLC is generally a disregarded entity unless you elect corporate treatment. In that default case, the LLC's activity is reported on your federal return.

| Topic | Article fact | Why it matters |

|---|---|---|

| Federal tax treatment | IRS classification rules determine federal treatment, not whether you file in Delaware or Nevada | State branding is not tax planning by itself |

| Single-member LLC default | A single-member LLC is generally a disregarded entity unless you elect corporate treatment | In the default case, the LLC's activity is reported on your federal return |

| FEIE eligibility path | One eligibility path is the physical presence test: 330 full days in 12 consecutive months | FEIE relevance depends on your facts, not the formation state |

| FEIE filing | Claiming FEIE requires attaching Form 2555 to Form 1040 or 1040X | The filing step is separate from state choice |

| Self-employment tax | FEIE can reduce regular income tax, but it does not reduce self-employment tax | Do not treat FEIE as a complete tax answer |

If you are a U.S. citizen or resident alien abroad, you are still taxed on worldwide income. The FEIE (Foreign Earned Income Exclusion) is eligibility-based relief for qualifying taxpayers, not a benefit tied to Delaware or Nevada. One eligibility path is the physical presence test (330 full days in 12 consecutive months), and claiming FEIE requires attaching Form 2555 to Form 1040 or 1040X. FEIE can reduce regular income tax, but it does not reduce self-employment tax.

The practical takeaway is simple: do not let the formation state stand in for tax planning. First confirm how the LLC is classified. Then confirm whether FEIE is even relevant to your facts. Only after that should you decide whether the state filing creates a workable operating structure.

Your reporting file matters more than your formation certificate#

In cross-border operations, missed filings are often a bigger risk than LLC state choice. Review this checklist before year-end and again before filing season:

| Filing item | Grounded point | Timing / status |

|---|---|---|

| FBAR / FinCEN Form 114 | Review filing if aggregate foreign account value exceeds $10,000 at any point in the year | Due April 15 with automatic extension to October 15 |

| Form 8938 | Separate from FBAR; filing one does not replace the other | Current threshold pending tax-advisor verification |

| Form 5472 scope | Review whether your facts trigger filing | Current filing trigger pending tax-advisor verification |

| BOI | The March 26, 2025 interim rule narrows reporting to foreign reporting companies; confirm current status before assuming you are in or out | The rule references a 30-day from publication timeline |

- Foreign accounts (FBAR / FinCEN Form 114): If aggregate foreign account value exceeds $10,000 at any point in the year, review FBAR filing. Due April 15 with automatic extension to October 15.

- Specified foreign financial assets (Form 8938): Separate from FBAR. Filing one does not replace the other. Current threshold pending tax-advisor verification.

- Foreign-owned U.S. disregarded entity reporting (Form 5472 scope): Review whether your facts trigger filing. Current filing trigger pending tax-advisor verification.

- Beneficial ownership reporting (BOI): The March 26, 2025 interim rule narrows reporting to foreign reporting companies and references a 30-day from publication timeline, but FinCEN portal wording has not always matched that framing. Confirm current status before assuming you are in or out.

In practice, list each non-U.S. account, ownership fact, and cross-border payment rail, then map each item either to a required form or to a documented "not applicable."

That file should be usable by someone other than you. Include the account or asset, the name it is held under, the country, the rough function in your business, and the form you think may apply. If your answer is "not applicable," write down why. The point is to avoid year-end scrambling. You do not want to vaguely remember an account, a payment processor, or a foreign banking relationship and then fail to reconstruct whether it affected reporting.

Invoicing changes by client location#

This is where state choice often gets mistaken for operating compliance. Your invoicing should follow client-jurisdiction rules. The LLC formation state does not solve that for you.

| Client jurisdiction | Invoice content checkpoint | Tax handling model | Recordkeeping expectation |

|---|---|---|---|

| U.S. payer | Match legal business/tax details to payer onboarding records | Payer may use Form W-9 for information-return reporting | Keep W-9 support in files for 4 years |

| EU business client | For most B2B supplies, invoices are generally required under EU VAT rules. Confirm any local wording. | For services to a business in another EU country, you usually do not charge customer VAT | Keep invoice copies and your basis for B2B/VAT treatment |

| UK business client | Confirm place-of-supply wording and any reverse-charge reference | UK guidance states no UK VAT is charged when place of supply is outside the UK. Reverse charge can apply. | Keep invoices and your VAT-treatment basis in your records |

The same LLC can need different invoice handling depending on who is buying the service. That is the point. A Delaware filing certificate does not turn an EU client invoice into a U.S.-style invoice. A Nevada filing does not answer UK place-of-supply questions. Treat invoicing as a client-location workflow, not as a state-of-formation perk.

If anything is unclear, use this order: confirm federal tax classification, map filing obligations, align invoicing by client jurisdiction, then escalate to a qualified cross-border tax advisor before filing.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

The Anonymity Myth: What the Corporate Transparency Act Means for You#

If privacy is driving your choice, separate two systems: state public records and federal ownership reporting. In this decision, that distinction matters more than "anonymous LLC" marketing.

Public records and federal BOI reporting are different#

Start here, because this is where a lot of bad advice begins. The Corporate Transparency Act (CTA) is the federal legal framework for BOI reporting. FinCEN receives BOI reports.

| Layer | What the article says | Why separate it |

|---|---|---|

| Delaware state filing | The core LLC filing requires the LLC name plus registered office and registered agent details | Public state-record exposure is not the same question as federal BOI scope |

| Nevada state filing | Required filings can include manager/member names and an address, residence or business; the Nevada Secretary of State describes public access to organizational and amendatory documents | State filing details differ from Delaware and do not answer federal reporting duties |

| Federal BOI / FinCEN | BOI reporting is under the Corporate Transparency Act; FinCEN receives BOI reports, and a reporting company is the entity category used to determine filing duty | Federal ownership reporting is separate from what appears in state search results |

A beneficial owner is an individual identified through substantial control and/or an ownership-interest test. For the ownership-interest prong, verify the current federal threshold before relying on a specific percentage. Substantial control includes at least senior-officer authority and other control indicators under 31 CFR 1010.380. A reporting company is the entity category used to determine BOI filing duty, subject to exemptions.

At the state level, Delaware and Nevada do not expose the same filing details. Delaware's core LLC filing requires the LLC name plus registered office and registered agent details. Nevada required filings can include manager/member names and an address, residence or business, and the Nevada Secretary of State describes public access to organizational and amendatory documents.

That means you need to break "privacy" into two separate questions. First, what appears in public state search results? Second, what still may need to be reported federally if your entity is in scope? If you collapse those into one idea, you can end up overvaluing a state filing difference while missing the reporting framework that actually applies.

What changed under current BOI rules#

Current BOI scope matters more than state marketing. As of the March 26, 2025 interim final rule, FinCEN narrowed BOI reporting to entities previously defined as foreign reporting companies. It also exempted entities previously defined as domestic reporting companies. The same rule exempted U.S. persons from having to provide BOI to a foreign reporting company for which they are a beneficial owner.

When BOI is required, it is treated as confidential, not public state-record data. Access is structured for authorized recipients, not for general public browsing.

| Myth | State-record reality | Federal reality |

|---|---|---|

| "A registered agent makes my LLC anonymous." | A registered agent does not remove all required state disclosures. | It does not remove BOI duties when your entity is in scope. |

| "Delaware and Nevada privacy are basically the same." | They are not identical in public filing exposure. | BOI scope is not based on choosing Delaware vs. Nevada. |

| "If ownership is not public, government access is blocked." | Public state databases are only one channel. | BOI, when required, is reported to FinCEN and available to authorized recipients. |

Your practical checklist#

Once you separate public records from federal reporting, the next step is simple: verify scope, identify the people involved, and keep the file current.

- Confirm whether your entity is currently a reporting company or exempt under current rule text.

- Identify who qualifies as a beneficial owner through substantial control and the ownership-interest prong.

- Prepare the BOI information the current filing framework requires for in-scope entities.

- Track changes and file updates or corrections on the required timeline (30 calendar days for changes under current rule text).

- If you use Delaware search results, treat them as a lookup tool, not definitive proof of current legal status.

It also helps to save what you checked and when you checked it. Public search output, portal wording, and your own ownership or control facts can change over time. A dated compliance note is more useful than relying on memory if you need to revisit scope later. Choose your structure for liability protection and compliance you can actually maintain, not for secrecy claims.

You might also find this useful: Delaware C-Corp vs. Wyoming LLC: Choosing a US Business Entity.

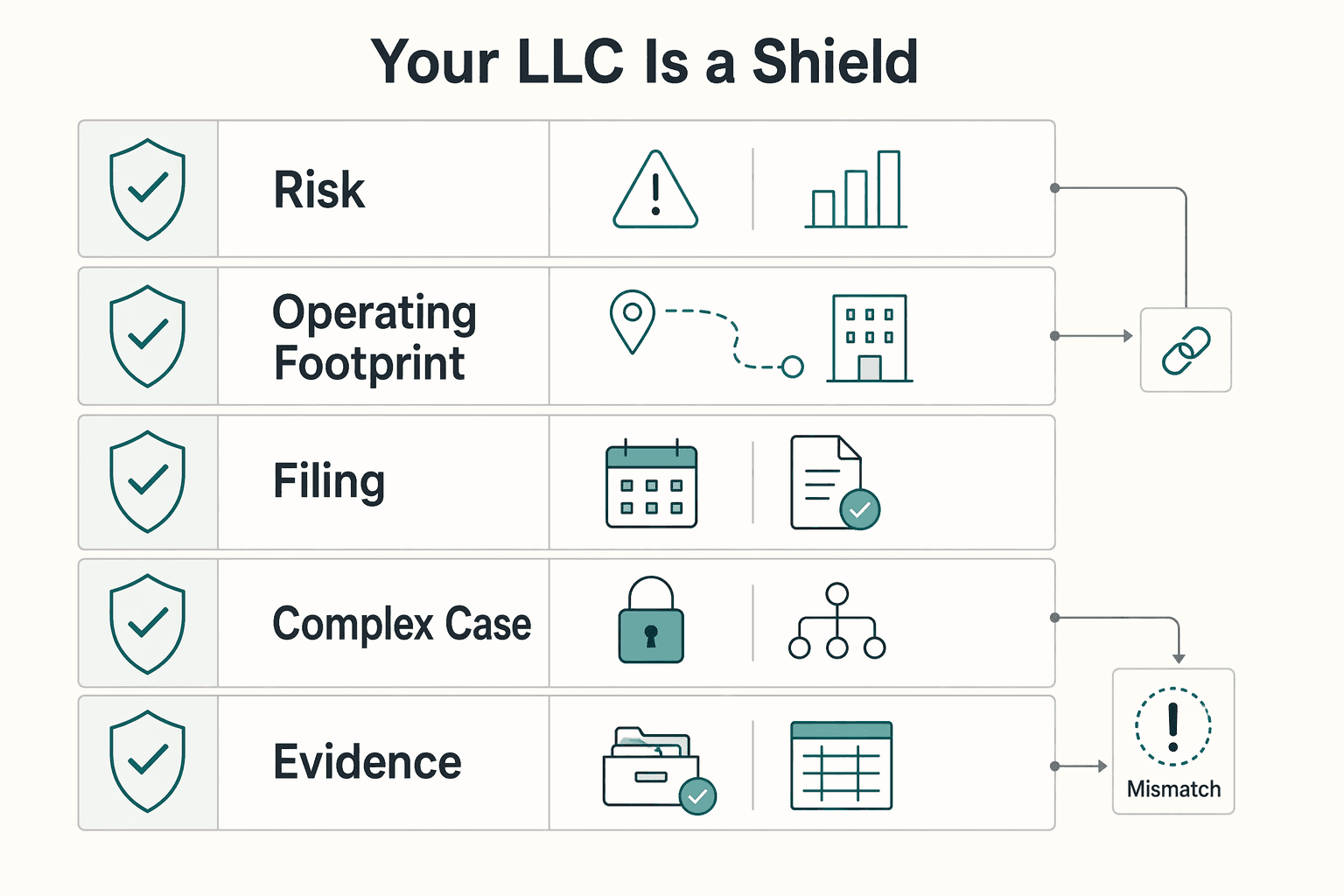

Your LLC is a Shield, Not a Silver Bullet#

Pick the structure you can run cleanly. If you are considering an out-of-state setup, verify that it changes a specific outcome for your situation before adding complexity.

Legal protections are not automatic, and they are not a substitute for consistent operations. In plain terms, treat the company as its own operating entity in your records and decisions. The exact legal standard is jurisdiction-specific, so confirm the current rule before relying on it.

A grounded reality check comes from Delaware corporate law, not LLC law. A March 2024 working paper (No. 762/2024) reviewed the 2022 reform allowing charter-based officer exculpation for duty-of-care monetary exposure and found tepid uptake through the first post-reform year. Different entity, different rule, same practical takeaway: legal protections on paper do less if adoption and follow-through are weak.

Before you add another state, use this filter:

- Risk type: Does the extra structure change your real exposure, or just sound stronger?

- Operating footprint: Are you truly operating across states, or mainly from one base?

- Compliance capacity: Can you reliably handle additional filings, renewals, and recordkeeping?

- Outcome change: Can you name the exact legal or operational result this added complexity creates?

Then use this maintenance checklist:

- Core entity documents kept current and internally consistent

- Contracts executed by the correct legal entity with the correct signer title

- Bookkeeping and records kept complete and consistent

- Payment flow and accounts aligned with the entity's operations

- Insurance and supporting records, if applicable

- Current veil-maintenance requirement pending counsel verification

- Current filing requirement pending official or counsel verification

- Current annual renewal/report requirement pending official or counsel verification

The point of that checklist is not formality for its own sake. It is to make the business legible as a real operating entity. If the company earns the income, the company should be the one named on contracts, receiving the funds, and carrying the records that support what happened. That routine discipline usually matters more than headline legal-shield language.

For a step-by-step walkthrough, see How Nevada LLC Legal Protections Work for Independent Professionals.

If you decide you want less entity admin while still operating globally, review Merchant of Record for Freelancers to compare that route against running your own LLC setup.

Frequently Asked Questions

Is a Nevada LLC truly anonymous anymore?

No, not if by anonymity you mean no meaningful disclosure. The article distinguishes public-record privacy from federal reporting and notes Nevada has a public manager list, while Delaware does not list managers in the Certificate of Formation. Delaware filings are still public record, so neither state should be chosen based on anonymous LLC marketing alone.

Do I have to pay taxes in my home state with a Delaware LLC?

This article does not establish that answer. It does not verify current state tax rules, and it warns against treating Delaware as a tax strategy. If you will operate outside Delaware, confirm foreign qualification triggers, tax nexus standards, and filing costs in each relevant state.

What is the total annual cost of a Delaware LLC versus a Nevada LLC?

The article does not give a verified total annual cost. It only supports minimum formation figures of $110 for Delaware and $425 for Nevada, with Nevada's package including the manager or member list filing, Nevada business license, and filing fee. To compare real cost, estimate recurring obligations line by line, including annual state requirements, any business license, registered agent fees, and any added out-of-state registration layer.

Is a Delaware LLC good for a solo consultant?

It can be, based on the filing mechanics described here. The article notes a lower quoted minimum formation fee than Nevada, no manager or member listing in the Certificate of Formation, and no Delaware business license if you are not doing business in Delaware. But you should confirm whether operating elsewhere adds a second-state registration or tax layer before filing.

What is a charging order, and is it really ironclad protection?

These materials do not verify charging-order rules or whether Delaware or Nevada offers stronger protection. They also warn that a fraudulent transfer can be undone and result in penalties. Do not choose a state based on claims of ironclad protection, and do not move assets after a claim appears without legal advice.

Does forming an LLC affect my ability to claim the Foreign Earned Income Exclusion?

Not by state choice alone. The article says FEIE is eligibility-based relief and not a benefit tied to Delaware or Nevada, and it notes FEIE does not reduce self-employment tax. Confirm your federal tax classification and get written guidance based on your residency, income, and filing posture.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- appropriations.senate.gov/download/fy26-interior-senate-reporttrusted

- attorneygeneral.gov/wp-content/uploads/2022/09/2022-09-07-Marine...trusted

- boiefiling.fincen.govtrusted

- boiefiling.fincen.gov/resources/BOIR_Filing_Instructions.pdftrusted

- documents.dnrec.delaware.gov/energy/Planning/Delaware-Energy-Security-Pla...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- federalregister.gov/documents/2025/03/26/2025-05199/beneficial-o...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The 'Profit First' Method Part 2: Setting Up Your Bank Accounts

Most freelancers who try Profit First open a few extra bank accounts and call it done. That's the wrong move.

Delaware C-Corp vs Wyoming LLC for Your Next Growth Stage

Choosing between a Delaware C-Corp and a Wyoming LLC is a stage-fit decision, not a state popularity contest. For `delaware c corp vs wyoming llc`, the real question is which structure you can run cleanly over the next 12-24 months while keeping room to scale.