Quick Answer

For German residents, the key issue is how Germany classifies the U.S. LLC. That case-specific classification drives whether payments are analyzed as dividends under Article 10 or business profits under Article 7, so the operating agreement, actual management, transfer rules, profit mechanics, and treaty filings all need to tell the same story.

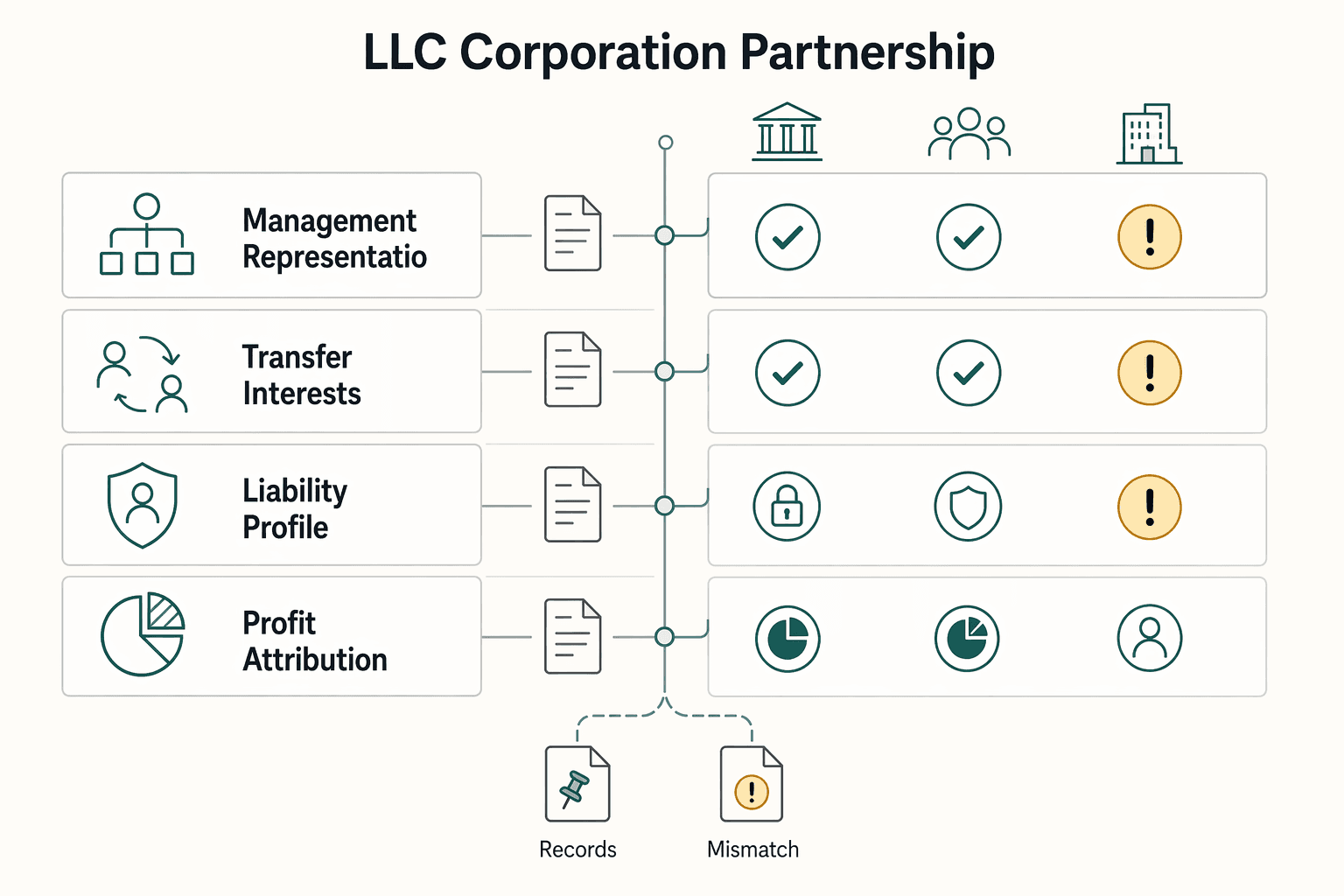

The German Litmus Test: Is Your US LLC a Corporation or a Partnership?#

Everything that follows starts with German classification, not the U.S. LLC label and not your U.S. tax election. For German tax purposes, an LLC can be treated as a corporation, a partnership, or, if there is only one owner, a branch. That classification changes how domestic rules and treaty rules apply.

German reviewers use a Typenvergleich or type comparison based on German standards and the LLC's actual features. Before you assume a favorable result, use this quick self-audit:

| Decision signal | Partnership-leaning | Corporation-leaning | What to review |

|---|---|---|---|

| Management and representation | Members directly control key decisions | Centralized control in a manager or manager group | Operating Agreement, signing authority, approval workflow |

| Transfer of interests | Transfers require member consent | Interests are freely transferable | Transfer clauses, admission rules, buy-sell terms |

| Liability profile | Less complete owner liability shielding | Clear limited liability for all owners | Applicable LLC law plus agreement language |

| Profit attribution | Profits allocated to members under agreed economics | Distribution mechanics that function more like dividends | Allocation and distribution clauses and bookkeeping treatment |

A practical way to approach the review is in two passes. Start with legal design, meaning the agreement plus the applicable LLC law. Then compare that design with actual operation, meaning how decisions, approvals, transfers, and payouts work in practice.

That makes the Operating Agreement a key proof document, but not the only one. Draft it so the intended mechanics are easy to see: member management, consent-based transfer limits, and member allocation economics. Be careful with features that read more like a corporation, such as broad manager authority, easy transferability, and dividend-like payout mechanics.

One last check matters more than most people expect. If your documents say one thing and your day-to-day conduct says another, stop before you file a treaty position and get cross-border advice. That kind of mismatch can increase reclassification risk. Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025).

Design Your Armor: Structuring the Operating Agreement for German Tax Success#

Treat the Operating Agreement as a control document, not as a guarantee of any tax result. The practical goal is simpler: use precise terms, remove contradictions, and make sure daily operations match what the document says. The excerpts here do not provide authoritative US-Germany LLC classification criteria, so treat the checklist below as drafting hygiene and advisor-prep, not as a legal test.

What to include and what to avoid#

| Clause area | Include | Avoid |

|---|---|---|

| Governance and decision rights | Clear authority lines, explicit approval steps, and written decision records | Overlapping authority, undefined roles, or broad power with no boundaries |

| Transfer restrictions | Direct rules for sale, assignment, pledge, inheritance, and member admission | Partial restrictions that leave key transfer paths undefined |

| Capital and profit allocation mechanics | One consistent vocabulary for contributions, allocations, and payments | Mixing terms without definitions or relying on ad hoc practice |

| Document consistency | Matching language across agreement, amendments, ledgers, consents, and signing authority | Clean drafting in one file but conflicting language or behavior elsewhere |

Check the text against behavior#

As a practical matter, drafting is most useful when operations follow it. Before you rely on the agreement, compare what you signed with what you actually do:

| Area | Agreement text | Behavior to compare |

|---|---|---|

| Approvals | Approval rules | Real approvals in recent decisions |

| Signing authority | Signing authority language | Bank and contract signers |

| Economics | Economic terms | Bookkeeping labels and member payment records |

- Compare approval rules to real approvals in recent decisions.

- Compare signing authority language to bank and contract signers.

- Compare economic terms to bookkeeping labels and member payment records.

If the text and the behavior do not match, fix that first. A position built on inconsistent facts is hard to defend.

Advisor handoff checklist#

When you bring in legal and tax advisors, give them one review pack instead of scattered files and ask for one integrated review across authority clauses, transfer mechanics, economic terms, and consistency across the full document set:

- Current Operating Agreement and all amendments

- Formation document(s)

- Membership ledger or cap table

- Bank authority and signature permissions

- Written consents, resolutions, and side letters

- Sample bookkeeping entries describing member payments

One legal-source warning is worth keeping in mind. Convenience compilations can help you orient yourself, but they may not have legal effect on their own. For example, the EUR-Lex consolidated text says it is a documentation tool without legal effect, notes that EU institutions do not assume liability for its contents, and points readers to authentic Official Journal versions. That EUR-Lex text concerns Belarus-related restrictive measures, not US-Germany LLC dividend classification. Verify against authentic texts before you rely on any legal citation.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The Two Futures for Your LLC Income: Dividend vs. Profit Share#

Once classification is set, the rest of the analysis is usually whether the income is treated under Article 10 for dividends or Article 7 for business profits. Each path comes with its own treaty logic, evidence burden, and filing risks.

This is not a rate-shopping exercise first. It is a characterization question first, then a treaty-entitlement and filing-consistency question.

The practical decision grid#

| Decision point | Dividend path | Profit-share path |

|---|---|---|

| Income characterization | Distribution is treated like a dividend from a company | Income is treated as direct business profit or profit share |

| Treaty article | Article 10 | Article 7 |

| Likely tax friction points | Beneficial-owner requirement, Article 28 Limitation on Benefits, current administrative views reported in some transparent-entity cases, and reduced withholding treatment that must be verified | Whether Article 7 fits your facts, whether a permanent establishment exists, and how much profit is attributable to it |

| Cash-flow impact | Possible source-state withholding once the applicable treaty rate is confirmed, with risk of denial or delay if treaty access is challenged | Often less about dividend-style withholding and more about defending the business-profits position and profit attribution |

| Documentation burden | Residency and treaty-benefit support, withholding paperwork, and proof that treaty conditions are met | PE evidence pack, business records showing where activity is carried on, and any treaty-based return disclosure that may apply, including checking Form 8833 |

The treaty separates these buckets for a reason. Article 7 covers business profits and Article 10 covers dividends. If a reviewer places your payment in the dividend bucket, the focus shifts quickly from entity design to treaty access, withholding, and anti-abuse screens.

What changes under Article 10#

Under Article 10, the payer's state may tax dividends subject to treaty limits. Confirm the applicable treaty rate for your facts before using a reduced withholding position in planning.

This route also carries interpretation risk. Recent practitioner reporting points to a restrictive administrative view in some reduced withholding scenarios and a separate lower-tax-court outcome allowing 0% withholding in a specific U.S. S corporation fact pattern. Those signals do not resolve LLC treatment and do not make dividend relief automatic for transparent or hybrid entities.

Before you file, make sure the withholding position matches the full record: beneficial-owner analysis, any required Article 28 review, and consistent forms and return disclosures.

What changes under Article 7#

Article 7 is simpler on paper than in application. Business profits are generally taxed in the residence state. If the enterprise carries on business in the other state through a permanent establishment, only the profits attributable to that PE are taxed there.

In practice, disputes often turn on two proof questions: whether a real PE exists and whether the profit attributed to it is supportable.

What a reviewer expects to see on PE#

The treaty defines a PE as a fixed place of business and gives examples such as a branch, office, factory, and workshop. A workable evidence pack can include the following:

| PE factor | Reviewer view | Details |

|---|---|---|

| Operational presence | Supports a PE position | A real business location in the state where PE is being asserted, with contracts and invoices that line up with the activity |

| Decision-making footprint | Supports a PE position | Records showing where material decisions are made, by whom, and with authority that matches the governing documents |

| Business records | Supports a PE position | Books, banking, client files, and accounting records that trace the activity and the profits attributed to it |

| Bank account alone | Not sufficient on its own | A bank account alone does not prove a PE |

| Mailing address alone | Not sufficient on its own | A mailing address alone does not settle the issue |

- Operational presence: a real business location in the state where PE is being asserted, with contracts and invoices that line up with the activity.

- Decision-making footprint: records showing where material decisions are made, by whom, and with authority that matches the governing documents.

- Business records: books, banking, client files, and accounting records that trace the activity and the profits attributed to it.

Avoid one-factor arguments. A bank account alone does not prove a PE, and a mailing address alone does not settle the issue either. Reviewers often look for one consistent story across address records, signers, contracts, books, and actual operations.

Also check filing alignment. W-8BEN instructions address treaty claims for business profits not attributable to a PE, and Form 8833 is the IRS disclosure channel for treaty-based return positions. Treaty language by itself is not enough if the forms and the return posture do not match. If your facts involve mixed residency signals, inconsistent entity treatment, or weak profit attribution, escalate before filing.

For a step-by-step walkthrough, see A Deep Dive into the US-Mexico Tax Treaty for Remote Workers.

Your Ongoing Compliance Checklist: Execute with Precision#

Once you choose your treaty lane, execution matters more than theory. Most failures in this area come from incomplete submissions or records that do not line up.

- Send the treaty documentation the payer asks for, and keep the exact filed record.

If a payer or withholding agent requests treaty documentation, submit it and keep the signed copy, delivery proof, and any account-coding follow-up. Before filing season, confirm that the form language still matches your return position and records. If treaty paperwork and filings conflict, your treaty claim can break down.

- Run the Form 8802 to Form 6166 process exactly.

If you need U.S. residency certification, request Form 6166 through Form 8802. The IRS says Form 8802 is mandatory. For current-year requests, include the signed penalties-of-perjury attestation.

If you use Pay.gov, treat the uploaded Form 8802 copy as payment validation only. Your full Form 8802 application still must be submitted to the U.S. Residency Certification function by mail or fax, and a Pay.gov-only upload is not processed. If you combine multiple applications in one Pay.gov PDF, stay within the 15MB limit. The mobile-friendly Form 8802 effective Sept. 28, 2025 is only for individual applications, not business entities.

After issuance, send Form 6166 to the foreign withholding agent, or other appropriate foreign-country person, requesting treaty support. Do not treat Form 6166 as proof of beneficial ownership or proof that U.S. tax was paid.

- Keep a complete Form 8802/Form 6166 evidence file.

Keep payment confirmation, mail or fax submission proof, copies of the submitted package, and issued Form 6166 copies. Organize records by tax year and country request so you can respond quickly when a payer or foreign-country person asks for support.

- Run an annual consistency check before filing.

Review payer-facing treaty paperwork, your Form 8802/Form 6166 records, and signer/attestation details together. Flag any changes early and update the documentation before filing deadlines.

Keep this evidence pack ready#

| Task | Who requests it | What to retain | Common failure mode |

|---|---|---|---|

| Treaty documentation delivered to payer | Payer or withholding agent | Signed copy, delivery proof, payer correspondence | Treaty paperwork conflicts with filed position |

| Form 8802 request for Form 6166 | IRS | Final Form 8802, payment confirmation, mail or fax submission proof, issued Form 6166 | Assuming Pay.gov upload alone filed the application |

| Form 6166 use abroad | Foreign withholding agent or other foreign-country person | Copy sent, request email, date used | Treating Form 6166 as beneficial-ownership proof or proof of U.S. tax paid |

| Current-year Form 8802 attestation | IRS | Signed penalties-of-perjury attestation with the application file | Current-year request submitted without the required attestation |

| Annual consistency review | You and your advisor | Short change memo and supporting updates | Documentation updated late, after filing pressure starts |

When to talk to a pro#

Do not wait for a filing deadline if the paperwork no longer lines up. Get help before filing if payer-facing treaty paperwork conflicts with your Form 8802/Form 6166 file, if a current-year attestation is missing, or if you are relying on a Pay.gov upload without separate mail or fax submission. Those may look like checklist issues at first, but they can derail treaty-claim support quickly.

| Trigger | Why it matters | When to act |

|---|---|---|

| Payer-facing treaty paperwork conflicts with your Form 8802/Form 6166 file | It can derail treaty-claim support quickly | Before filing |

| A current-year attestation is missing | It can derail treaty-claim support quickly | Before filing |

| You are relying on a Pay.gov upload without separate mail or fax submission | It can derail treaty-claim support quickly | Before filing |

| You are pursuing a German withholding exemption certificate or refund | Reported processing can run about 12 to 24 months | Escalate early |

You might also find this useful: How to Avoid Dynamic Pricing When Booking Travel. Before your next filing cycle, keep your residency timeline and evidence in one place with the Tax Residency Tracker.

Conclusion: From Compliance Anxiety to Strategic Confidence#

At this point, more theory is usually not what you need. What you need is one position that your documents, your actual operations, and your filings can all support, because inconsistency is what creates rework, delays, and avoidable cost. The materials reviewed here do not establish specific US-Germany LLC treaty outcomes, withholding rates, or filing-form requirements, so treat those points as case-specific.

Use this as your closing execution check:

- Confirm your classification intent. Write down the treatment you plan to rely on, then test whether your signed documents and actual management and payment behavior support it.

- Confirm your documentation trail. Make sure your contracts, ownership records, payment records, and decision records tell the same story.

- Align your annual filing posture. Your filing positions and internal memo should not conflict.

If your position relies on agreement design, treat that agreement as a live control document. Make sure amendments, ownership records, approvals, and books still line up with it in practice.

If material uncertainty remains before filing, involve a qualified cross-border advisor. The goal is not a clever argument. It is a position you can explain, support, and repeat next year.

We covered this in detail in A Freelancer's Guide to the US-Germany Tax Treaty.

If your LLC classification or treaty position is still unclear, talk to Gruv to confirm workflow fit and coverage where supported for your setup.

Frequently Asked Questions

How does Germany classify your U.S. LLC for tax purposes?

Germany classifies a U.S. LLC for German tax purposes using a Typenvergleich under BMF criteria. The analysis is case-specific, so the U.S. label alone is not enough. Keep the agreement, amendments, approvals, and payment records together, and escalate if documents and day-to-day treatment do not match.

Can you rely on a generic operating agreement?

Usually not. Because classification is a Typenvergleich, generic language can leave key governance, transfer, or payment points unclear. If practice changed informally, get cross-border tax advice before filing.

How do you reduce double-taxation risk?

Start with consistency across your classification position, treaty position, forms, books, and annual filings. If you rely on Article 7, keep records that support whether the enterprise carries on business through a permanent establishment. Escalate when the facts are borderline.

If your payments are treated as dividends, what withholding rate applies?

Do not assume a single fixed rate applies. Reported treaty-reduced dividend rates include 0%, 5%, or 15% depending on conditions, and the current rate should be verified for your facts. Confirm beneficial-owner status, fiscal-transparency treatment, and any Article 28 Limitation on Benefits condition before relying on reduced withholding.

What do you actually file to support treaty withholding?

You give Form W-8BEN to the withholding agent or payer, not to the IRS. On that form, identify the treaty article, paragraph, and claimed rate so the treaty claim matches your classification position. Keep the signed form, delivery proof, payer correspondence, and any account-coding confirmations.

Do you need Form 6166, and what does it prove?

If a foreign withholding agent requests U.S. residency certification, request Form 6166 through Form 8802. Keep the Form 8802 package, payment confirmation, submission proof, and issued Form 6166 with the rest of your treaty file. Form 6166 does not prove beneficial ownership or that U.S. tax was paid.

When should you stop DIYing this?

Stop before filing if key facts changed, the classification call is close, or the paperwork no longer lines up. Escalate early if you are pursuing a German withholding exemption certificate or refund, because reported processing can run about 12 to 24 months.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/119/crec/2026/03/05/172/42/CREC-2026-03-05.pdftrusted

- irs.gov/pub/irs-trty/germany.pdftrusted

- irs.gov/businesses/international-businesses/germany-...trusted

- isb.idaho.gov/wp-content/uploads/ISB_Advocate_Aug_2025_Fin...trusted

- live.house.govtrusted

- sec.gov/Archives/edgar/data/1858985/0001193125212659...trusted

- sec.gov/Archives/edgar/data/1898496/0001104659220485...trusted

- ustr.gov/sites/default/files/files/Press/Reports/2025...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How to Avoid Dynamic Pricing When Booking Travel

Your edge is not predicting airfare. It is using a repeatable process that starts with your deadlines, compares like-for-like offers, and tells you when to book. If you want to avoid pricing mistakes during a move, treat fares as something you manage around, not something you fully control.