Quick Answer

Start by treating moving from california to texas tax planning as a documentation project, not just a relocation. Choose a clear domicile date, complete Texas identity and address updates quickly, and save dated proof for every change. Keep a continuous travel and work log so your records support your filing position on Form 540NR. If equity compensation, large gains, or post-move California work overlap your timeline, get written state-tax advice before you file.

Moving from California to Texas is one of the bigger financial decisions a high-earning professional can make. It is not just a change of address. It resets your tax position, your records, and the facts that will define your filing story. The appeal is obvious, and so is the risk. California's Franchise Tax Board can scrutinize residency changes closely, and a sloppy move can turn into a long audit and an expensive dispute.

The way through that risk is to treat the move like a documented project, not a personal errand. This playbook is built around that idea. It gives you a three-phase plan to turn a stressful move into a documented, defensible change in domicile. Your record should start taking shape well before you cross the state line.

Phase 1: The 90-Day Countdown - Your Pre-Move Strategic Plan#

This is your pre-move risk-control window. Your job over the next 90 days is to document a permanent domicile shift, not just a relocation, with a specific date and a defensible evidence trail. California treats residency as a question of fact and looks at where your closest connections are.

Moving day alone does not end California exposure. California can still treat you as a resident if you are there for other than a temporary or transitory purpose, or if California remains your domicile while you are away temporarily. In a part-year filing year, California taxes worldwide income while you are a resident. It then taxes California-source income while you are a nonresident. Build your plan around that split.

Time your income before you time the truck#

If you can control timing, avoid major income events in the transition gap, before your Texas ties are active and documented. Timing helps, but it does not by itself determine sourcing outcomes. Use this framework:

| Income item | Key caution | Records or support |

|---|---|---|

| Capital gains | Be cautious about selling appreciated assets during the transition gap; timing can matter, but outcomes depend on asset type and facts | Brokerage confirms, trade dates, sale instructions, and written tax advice before closing |

| Equity compensation | California can source compensation based on where services were physically performed, and grant, vest, exercise, or sale timing can straddle the move | A sourcing memo |

| Business sale proceeds or installment payments | Do not assume a post-move payment is outside California; asset type, deal structure, and sale date all matter | Written advice before signing an LOI, purchase agreement, or installment note |

- Capital gains: If you control the sale date, be cautious about selling appreciated assets during the transition gap. Timing can matter, but outcomes depend on asset type and facts. Keep brokerage confirms, trade dates, and sale instructions, and get written tax advice before closing.

- Equity compensation: Treat this as fact-sensitive. California can source compensation based on where services were physically performed, and the FTB describes a day-ratio method using California workdays over total workdays. If grant, vest, exercise, or sale timing straddles the move, plan for a sourcing memo.

- Business sale proceeds or installment payments: Do not assume a post-move payment is outside California. FTB Pub. 1100 says California taxes certain nonresident installment gains when sourced to California, while installment gains from intangible property are generally sourced to the recipient's state of residence at sale. Asset type, deal structure, and sale date all matter, so get written advice before signing an LOI, purchase agreement, or installment note.

Before any material close, use one checkpoint: if the date, income character, and sourcing support file are not assembled, pause.

Give the business a clean break#

If you run an LLC or corporation, an address change is not a complete story. Your entity footprint needs to match your personal move, with records showing when California activity ended, what moved to Texas, and what remains. Work through this checklist to line those up:

- Confirm California registration status for each entity, permit, and filing account.

- Decide whether each entity must register in Texas, including foreign-registration status if it is doing business there.

- If California activity is ending, complete the correct withdrawal, dissolution, or cancellation steps and calendar final California returns. California's LLC cancellation form requires final returns required under the Revenue and Taxation Code to be filed with the Franchise Tax Board.

- Update contracts and statements of work to reflect where services are actually performed.

- Retain work-location evidence such as calendars, travel records, invoices, and meeting logs.

The Texas side also needs to be realistic. Texas has no state income tax. But taxable entities formed in Texas or doing business in Texas still face franchise tax rules. The Comptroller's small-business guidance says businesses with annualized total revenue of $2,650,000 or less starting Jan. 1, 2026 do not have to pay franchise tax. Still verify what filings your entity must make.

Bring in a CPA or tax attorney early if you have equity comp, an earnout or installment sale, payroll in multiple states, California work trips after the move, or a business that keeps California customers and personnel. Those facts can change sourcing, filing, and recordkeeping requirements fast.

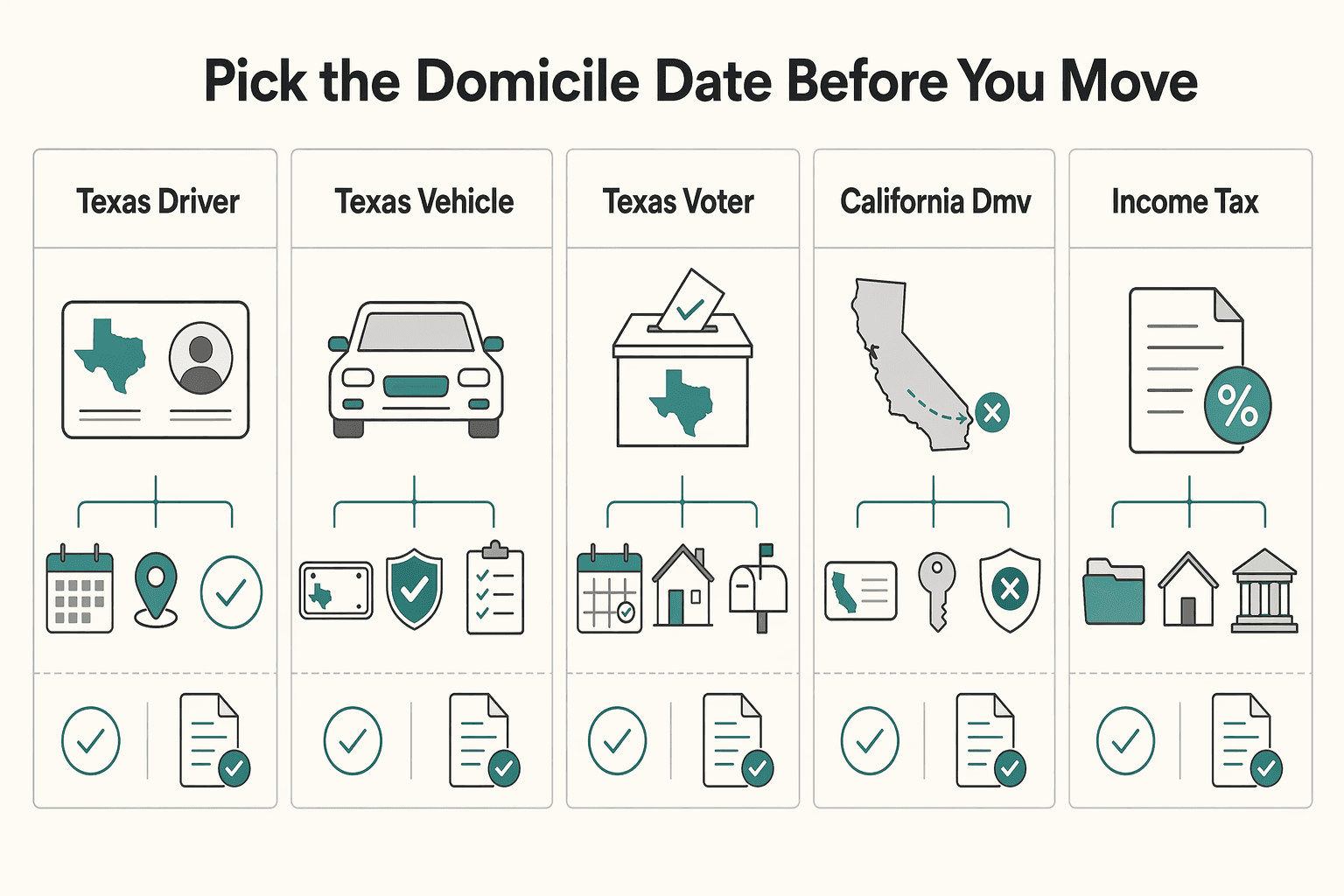

Pick the domicile date before you move#

A clear chronology is usually more persuasive than any single document. Choose your domicile date first, then line up the first-week Texas actions that will support it.

| Action | Timing in article |

|---|---|

| Texas driver license | Texas allows eligible new residents to drive on an out-of-state license for up to 90 days after moving |

| Texas vehicle registration | It gives 30 days to register a vehicle |

| Texas voter registration | Texas requires registration by the 30th day before Election Day |

| California DMV new address notice | California DMV requires notice of a new address within 10 days of moving |

Before departure, schedule your Texas driver license appointment, vehicle registration plan, voter registration steps, bank and address changes, and any estate-planning updates. Texas allows eligible new residents to drive on an out-of-state license for up to 90 days after moving. It gives 30 days to register a vehicle. Treating those as maximums can weaken your timeline. If you plan to vote, Texas requires registration by the 30th day before Election Day. California DMV requires notice of a new address within 10 days of moving.

Retain sequence evidence: lease or closing documents, moving contract, appointment confirmations, utility start dates, mailing-address changes, client notices, and Texas professional appointments booked before arrival. One record does not prove domicile. A dated sequence before and after the move makes your intent far more credible.

Before you finalize timing, model the cost picture on both sides:

| Cost category | California side to model | Texas side to model |

|---|---|---|

| Income tax | Part-year resident treatment on worldwide income during resident periods, plus California-source income during nonresident periods | State income tax is 0% |

| Property tax | Home-location assumptions and carrying costs | Property tax is local, not state-level, so county assumptions matter |

| Business compliance and admin | Entity registrations, final returns, closure or withdrawal work, and advisory time | Texas registration, franchise-tax compliance, and ongoing admin |

| Travel-back risk cost | Trips to California, California workdays, and the cost of blurred facts if ties stay active | Ongoing cost of maintaining a Texas-centered life while avoiding California fact patterns that weaken nonresident status |

If you execute this phase well, Phase 2 becomes operational follow-through instead of damage control. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Phase 2: Execution Week - Building Your Mountain of Evidence#

This week is about facts, not intentions. Build a dated record showing your move timeline and how your day-to-day life shifted to Texas. Residency is determined from all circumstances, not from one document.

Use one proof standard for every action: keep (1) receipt or confirmation, (2) effective date, (3) account or record updated, and (4) screenshot or PDF showing the Texas address when available. If one item is missing, log what you have and what is unavailable.

First-week action flow#

Move through the week in sequence. Update core identity and address records first. Shift day-to-day money movement and account activity next. Close, transfer, or downgrade remaining California ties last, and keep records aligned with your physical move.

| Action completed | Proof to retain | How it supports your fact pattern |

|---|---|---|

| Texas identity/registration actions completed | Appointment confirmation, receipt, issued record, effective date | Adds dated evidence that core records moved to Texas |

| Primary mailing address updated across institutions | Change confirmations and dated account notices | Creates a consistent, time-stamped address trail |

| Primary banking/card/payroll records updated | Confirmation plus first statement or payroll record showing Texas address | Shows day-to-day financial records were updated to Texas |

| California memberships/services/accounts canceled or transferred | Cancellation/transfer notices, final invoices, effective dates | Adds dated evidence that California ties were reduced (not determinative by itself) |

California severance checklist#

This is where records can become inconsistent, so save the proof artifact before you move to the next item. No single checklist item proves residency status on its own.

| Category | Updates or records mentioned |

|---|---|

| Financial | Update bank, brokerage, credit card, insurance, payroll, and tax-portal records where applicable |

| Professional | Update client records, contracts, invoices, and license-related records where applicable |

| Personal services | Transfer healthcare and other recurring providers where applicable |

| Memberships | Cancel or transfer gyms, clubs, and local associations where applicable |

| Property and personal footprint | Document physical move-out actions, for example mover inventories, receipts, photos, and access logs |

Shift your center of gravity#

Your goal here is to show that the move is operational, financial, and long-term rather than temporary. Move the personal items that signal real life. Route primary spending and deposits through Texas-based records. Update legal documents tied to long-term intent, such as estate, insurance, and beneficiary records where applicable.

Escalate to a state tax professional if your facts are mixed, especially if you keep a California home, return for work, or physically perform services in California after the move. In that case, California-source income can still apply. Your California Nonresident or Part-Year Resident return may also need a sourcing workpaper using the FTB workday method: CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income.

You might also find this useful: A guide to the 'trailing tax liability' when leaving a high-tax state like California. As you collect move proof, track each address, travel day, and record in one place with the Tax Residency Tracker.

Phase 3: Post-Move Vigilance - Protecting Your New Tax Status#

Once you are in Texas, consistency matters more than speed. Your job is to keep a Texas-centered fact pattern month after month. Texas has no personal income tax, but California residency is still evaluated from your closest connections and whether any California presence is for other than a temporary or transitory purpose.

Turn travel into an audit file#

Treat every California trip as evidence. Schedule CA (540NR) asks for days spent in California for any purpose, and the FTB can issue an Information Document Request, so your log, receipts, and return need to match.

Run one master day log for the full year and reconcile it monthly against:

- Calendar entries

- Travel receipts

- Location or transaction records

Track departure date, return date, where you slept, trip purpose, and whether you physically performed work in California. Store the log with supporting PDFs, including flights, hotels, rental cars, tolls, and card statements, in one tax folder. Keep return support records for at least 4 years, and longer when extended assessment windows apply. If your log, calendar, and records conflict, resolve it immediately while details are still clear.

If California days start looking routine instead of exceptional, treat that as a risk signal. There is no universal California residency day-count rule, so set an internal caution line and escalate before you cross it.

Use safe harbor as a gating question, not a default answer#

Safe harbor is narrow and eligibility-based, not automatic, so start by asking whether it even belongs in your file.

Use this path:

- If you remain domiciled in California but are outside California under an employment-related contract, test safe-harbor eligibility.

- If your setup is not clearly within qualifying employment terms, do not assume safe harbor applies.

- If the absence period, return visits, or income limits fail current legal requirements, safe harbor fails.

Because the rules can change with the filing year, verify the absence period, return-visit limit, and any income cap for your filing year before relying on it. Build evidence beyond a contract: signed employment-related agreement, travel records, compensation records, and records showing your life actually operated outside California during the period claimed.

Keep your money and work patterns Texas-first#

Your monthly behavior should keep proving the same center-of-life story. Use that standard for habits such as:

- Run primary deposits, spending, and bill pay through Texas-addressed accounts.

- Shift recurring providers to Texas where practical, including medical, insurance, and other routine services.

- Keep business operations anchored in Texas records, invoicing, payroll, and mailing addresses.

- Keep your meeting pattern Texas-first and avoid making California your default client or networking hub.

Convenience can pull you back into old habits. The more your operating pattern drifts toward California, the more it can weaken your residency position.

Prepare the final California return like a handoff package#

Your final California filing is the formal handoff of facts: when resident treatment ended and what California-source income remained. Form 540NR and Schedule CA (540NR) are central. Schedule CA requires residency detail. For the 2025 tax year, the file-and-pay due date is April 15, 2026, with an automatic filing extension to October 15, 2026. Payment is still due April 15, 2026.

Give your preparer a complete package:

- Move-date memo

- Full day log

- W-2s/1099s and payroll detail

- Brokerage statements

- Contract list

- Income-allocation workpaper splitting resident-period worldwide income from nonresident-period California-source income

If you worked in California after the move, include a sourcing workpaper using the FTB method: California workdays divided by total workdays, then apply that ratio to the compensation at issue.

Escalate to a state tax professional if you physically performed services in California after moving, made frequent return trips, or have mixed-source income. Do the same if you and your spouse/RDP have different residency facts. Related: Moving From Hourly to Project-Based Rates.

Conclusion: Trade Anxiety for Agency#

Treat this move as an execution-and-documentation project, not a one-time paperwork event. You are building a defensible record: document changes to California ties, establish consistent Texas-centered signals, and keep records that still make sense at filing time.

That standard is practical because California residency is a facts-and-circumstances question, not a single checkbox. If you are a part-year resident, California taxes worldwide income during your resident period and California-source income during your nonresident period. If you are a nonresident, California can still tax California-source income, and Form 540NR is often where that reporting comes together.

| Behavior | Reactive move | Defensible move |

|---|---|---|

| California ties | Leaves old ties in place and relies on an address change | Actively unwinds California connections and keeps dated proof |

| Texas domicile signals | Updates a few items late or inconsistently | Builds a consistent Texas-centered pattern across daily-life records |

| Recordkeeping | Scrambles for documents at filing time | Maintains dated records, travel logs, and sourcing workpapers throughout the year |

| California work after move | Assumes Texas residency ends California tax exposure | Tracks California workdays because services physically performed in California can still be California-source income |

If you want a simple next-step plan, do three things:

- Build one evidence file with dated move records, Texas-centered life records, and a California travel log.

- Set a compliance calendar to review California days, store new records, and flag any post-move California activity before year-end.

- Prepare your filing support early, including Form 540NR backup and sourcing workpapers. If compensation spans locations, keep the workday allocation support using

CA Workdays / Total Workdays = % Ratio, then% Ratio x Total Income = CA Sourced Income.

If your facts are mixed, your move date is close to a major income event, or you still perform services in California after the move, involve a qualified state tax professional before filing.

For related cross-border context, see A Deep Dive into the US-Japan Tax Treaty for Remote Workers. If your move plan includes business-entity changes or cross-border client payments, use Contact to confirm the right compliance setup before year-end filing.

Frequently Asked Questions

How does California tax my RSUs after I move to Texas?

Treat RSUs and other equity-based compensation as a high-risk area if the award period crosses your move date. California calls out special rules for deferred or equity-based compensation, so the result depends on the award terms, the related service period, and where you physically performed services during that period. Keep grant notices, vest schedules, plan documents, payroll and W-2 detail, your move-date memo, and a work-location calendar tied to California versus Texas days.

What is the best way to prove to the FTB that I moved?

Assume no single document proves the move. Residency is determined from all the facts and circumstances, and the FTB does not issue written opinions confirming residency for a specific period. What matters is a consistent Texas-centered fact pattern across your domicile and day-to-day presence. Keep your Texas license, voter and vehicle registration, housing and address-change records, banking and provider updates, and your California travel log. Escalate if you kept a California home or continued a regular California work pattern.

What is the 18-month rule for California residency?

Do not rely on the nickname alone. Safe harbor may apply when you remain domiciled in California but are outside California under an employment-related contract, and specific eligibility requirements must be verified for your filing year. Keep the signed employment-related contract, travel-day counts, payroll records, and housing proof outside California. Escalate if your facts do not clearly fit safe-harbor requirements.

Can I avoid California capital gains tax by moving?

Do not assume a post-move sale is automatically outside California tax. First confirm that your California residency actually ended before the gain was realized, because part-year residents are taxed on worldwide income during the resident period and on California-source income during the nonresident period. Keep trade confirms, closing statements, brokerage history, your move-date memo, and residency-timing evidence. Escalate if timing is close to your move date or the deal includes equity-compensation links.

What exactly is the "California exit tax"?

Use that phrase only as shorthand. California does not impose a standalone individual exit tax just for leaving. The real question is whether California can still treat you as a resident or tax California-sourced income as a nonresident, typically reported on Form 540NR with the nonresident/part-year effective-rate method rather than a separate departure tax. Keep your final California return package, sourcing workpapers, California workday logs, and support for trailing California income. Escalate if income continues from services performed in California, California real property, or a California business.

Do I still owe California tax on income from California clients?

Do not treat client location as decisive. Where you physically perform services is usually the key factor, and travel back to California for work can create California-sourced income after your move. When work spans locations, use the workday allocation method (CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income). Keep contracts, invoices, calendars, travel receipts, location-based work logs, and your Form 540NR allocation workpaper. Escalate if you also have signs of ongoing California business activity.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bpd.cdn.sos.ca.gov/llc/forms/llc-4-7.pdftrusted

- comptroller.texas.gov/taxes/publications/98-806.phptrusted

- comptroller.texas.gov/taxes/property-tax/exemptionstrusted

- dmv.ca.gov/portal/handbook/california-driver-handbook/c...trusted

- dps.texas.gov/section/driver-license/moving-texas-guide-dr...trusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- irs.gov/irb/2025-03_IRBtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.