Quick Answer

Start with currency hedging for freelancers by fixing invoice terms first, then hedge only the exposure you can clearly measure. Build an exposure map, set budgeted exchange rates, and apply trigger rules by invoice size, margin sensitivity, and payment certainty. Use internal methods before external contracts, and move to forward contracts only when amount and timing are reliable. Finish each cycle with reconciliation so you can confirm whether the method reduced loss risk.

Currency hedging for freelancers starts with cash-flow protection, not market prediction#

Treat hedging as a cash-flow control choice, not a bet on FX market movements. The goal is to reduce foreign exchange risk that appears between transaction start and settlement. For freelance work, that means protecting what you keep after payment arrives, conversion happens, and funds are withdrawn.

Timing risk and payment friction often drive the losses and extra admin work. International payments can take several business days, wires may take longer depending on countries and banking relationships, and some processors can place temporary holds in certain cross-border cases. Each delay can change your effective payout and make reconciliation harder. A hedge can reduce rate risk, but it cannot remove provider holds.

Think through the money path in the order it actually happens: invoice issued, client pays, provider receives the funds, funds become available, conversion happens, and payout is completed. Exposure can stay open across more than one of those steps. That is why freelancers often feel FX risk as a smaller final payout rather than as one obvious market event.

That sequence also shows why many freelancers misdiagnose the problem. You may feel that the loss happened "at payment," but it may have started earlier with weak invoice terms or later with delayed conversion after funds were already available. A useful hedge decision depends on knowing which step stayed open the longest. Before receipt, you are relying on the client. After receipt, you may be relying on provider processing. After conversion, you may still be waiting on payout completion. Those are different risks, and they should not be treated as one blur.

Set your outcome before choosing any method: predictable take-home amounts, fewer losses between invoice and withdrawal, and clearer go or no-go terms for each client. Use a simple rule. If margin is thin and payment timing is uncertain, fix contract terms first. If timing and amount are reliable, then add hedging.

Use this pre-commit check before accepting cross-border terms:

- Confirm invoice currency, settlement currency, and where conversion will happen.

- Ask for the expected clearing window and whether extra holds apply to your account profile.

- Document who absorbs FX spread and transfer fees in the contract or statement of work.

- Verify country support, identity checks, and payout eligibility with your provider before signing.

If any of those answers are vague, do not jump straight to hedging. First tighten the payment terms or confirm the payout route. A weak process with a hedge layered on top is still a weak process.

Keep those answers with the proposal, statement of work, or invoice terms. If the final payout is weaker than expected, you need a clean record of what was agreed, what the provider setup allowed, and what actually happened in execution. That makes later review easier because you can compare expected timing and conversion steps with the real path rather than relying on memory.

Scope limits matter. Product access, compliance checks, and payout rules vary by country and provider, so what works for one freelancer may be unavailable to another. A common failure mode is agreeing to terms that assume instant conversion when your provider applies risk checks or hold periods. Confirm those constraints up front, especially before committing to financial contracts. Then map exactly where exposure appears in your payment timeline. For a deeper dive, read A Guide to Currency Hedging for Freelancers.

Build your exposure map before choosing any hedge#

Start with the map. Hedging is a risk-management move, and foreign exchange risk appears when rates move between transaction initiation and settlement.

Start with two buckets in your workflow:

- Foreign currency receivables: what you expect to receive, by currency.

- Foreign currency payables: what you expect to spend, by currency.

Then make timing visible. Currency markets run 24/7, so even short delays can change your effective result. Track the key steps in each payment cycle so you can see where exposure stays open the longest.

A one-page map is enough:

- List each receivable by currency, amount, and expected payment date.

- List each payable by currency, amount, and due date.

- Record your payment-cycle checkpoints and note where processing delays occurred.

- Mark periods when funds stayed unconverted.

For each line item, note when the amount became known, when payment was expected, and when you planned to convert or use the funds. That helps you separate three problems that can look similar from the outside: late client payment, delayed provider availability, and delayed conversion after the money is already sitting in the account.

The map should be simple enough that you will actually update it. If it takes too long to maintain, you will stop trusting it and fall back to guesswork. Use the same labels every month so you can scan quickly for the same types of gaps: amount known, due date, funds available, converted, paid out. Consistency matters more than complexity. The purpose is to see open exposure clearly, not to build a treasury dashboard.

If a receivable and a payable are in the same foreign currency and close in timing, mark them together when you review the map. The point is not just to list gross amounts but to see where a real mismatch leaves cash flow exposed.

That review should focus on net exposure, not headline invoice value. A large foreign-currency invoice may look risky on its own, but if you have same-currency expenses due in a similar window, the real conversion need may be smaller. The reverse is also true: a natural match that looks good on paper may fail if the timing is off and you still have to convert earlier than planned. A map that ignores timing will overstate protection.

Use one anchor currency pair that reflects your largest mismatch, then expand only after the first map is reliable. If the first version is messy, adding more currencies will not improve the decision. It will just make the rule harder to trust.

Choose invoicing currency with a clear decision rule#

Choose invoice currency based on one goal: reduce avoidable FX exposure while keeping cash flow predictable. Cross-border payments often involve conversion, and exchange-rate moves, processing delays, fees, and country-specific rules can change what you actually receive.

The currency choice is not just a billing preference. It decides who carries more of the timing friction and how much control you keep over conversion.

| Path | Main upside | Main tradeoff | Best fit |

|---|---|---|---|

| Invoicing in local currency | Simpler billing terms | Less control over conversion timing and rate | You want straightforward payment terms |

| Invoicing in client currency | More control over when and how conversion happens | More exposure if funds stay unconverted | You can actively manage conversion timing |

Apply this cost-structure rule before negotiating terms. If most of your costs are in one home currency, favor terms that shorten the time funds stay unconverted. If your costs are spread across currencies, keep flexibility and convert in stages.

The comparison only works if you judge it against your real payment flow. A client-currency invoice may look riskier at first glance, yet still be the better choice if it gets paid cleanly and lets you manage conversion on your schedule. A local-currency invoice may look simpler, yet still produce a weaker result if spread, fees, or delayed settlement do most of the damage.

A useful way to compare the paths is to walk through the full timeline for each option before you send the first invoice. Ask what happens at receipt, who controls conversion, when funds become usable, and where the uncertainty sits. The best choice is often the one that gives you the cleanest operational path, not the one that sounds easiest in conversation. If a currency choice creates less confusion around settlement and fewer points where value can leak, it is often the stronger choice for cash flow.

Add a client-level gate before you accept a currency mismatch: only proceed when margin can absorb normal rate movement and payment behavior is reliable. If either condition is weak, tighten terms first and revisit currency choice.

A useful decision rule is to ask two questions in order. First, which option shortens the open exposure window? Second, which option gives you the cleaner, more controllable settlement path? If the answers point in different directions, choose the path that protects cash flow more reliably, not the one that looks better as a pricing story.

If the client strongly prefers one currency, keep the question practical: can your margin and process absorb the remaining exposure under those terms? That framing helps avoid abstract debate. You are not trying to pick the universally best invoice currency. You are trying to decide whether a specific payment path is workable for this client, with this provider setup, under this timing pattern.

Before you sign, confirm in writing the invoice currency, who covers conversion costs, expected settlement timing, and any payment-rail constraints linked to currency, region, value, or speed. Write down why the currency was chosen so you can review later whether the result was driven by rates, fees, or timing. For a practical next step, try the free invoice generator.

Set hedge triggers and hedge size before each invoice cycle#

Set trigger and sizing rules before each invoice cycle so hedging is driven by cash-flow risk, not market opinions.

Use a must-hedge test when each invoice is created. Flag invoices where downside risk is harder to absorb, such as larger-than-usual amounts, thinner margins, or longer payment timelines. If risk is lower, use lighter coverage or no hedge.

Set coverage by payment certainty, not one fixed level for every client. Higher-certainty receivables can support higher coverage. Lower-certainty receivables should use lower coverage because forward contracts are binding obligations and are better suited to known, certain cash flows.

A practical way to apply this is to answer the same questions every time an invoice is issued: Is the amount stable? Is the due date credible? Is the payer reliable? Is the conversion path clear? The more uncertainty remains, the lighter the hedge should be. If the basics are not settled, the correct answer may be no hedge yet.

Use this monthly checklist:

- Set a budgeted exchange rate for each main currency pair as your planning baseline.

- Compare each invoice against that baseline and your margin sensitivity.

- Assign a coverage band based on payment certainty, and log the rationale.

- Recheck amount, due date, and payer reliability before execution.

- If any input is unclear, pause and fix terms first.

Coverage bands do not need to be complicated. A simple internal label is enough if you apply it consistently and record why. What matters is that the rule is visible before the cycle starts and that you do not change it midstream because the market moved.

Before the cycle begins, decide what makes an invoice hedge-ready in your own process. For example, the amount should be settled enough to trust, the due date should be credible enough to plan around, and the payout route should be clear enough that you know where conversion will happen. You do not need a complex scoring model. You need a small set of readiness checks that stops you from locking in a hedge against a receivable that still has basic business uncertainty around it.

Add one written stop rule: delay FX hedging when terms, timing, or payer reliability are unclear, then hedge after those are clarified. Keep that stop rule with your invoice terms so the business facts and the hedge decision stay tied together.

A good trigger rule also protects you from emotional changes after rates move. If the plan said no hedge because payment certainty was weak, do not reverse that decision just because the market became uncomfortable to watch. Likewise, if the plan called for coverage because the receivable was clean and material, do not abandon the rule because you suddenly want to wait for a better rate. The point of triggers is to separate business decisions from reactive market behavior.

Use internal hedging methods first because they are simpler#

Start with internal methods first: they reduce exposure without binding contracts and are usually simpler to run day to day. Their main advantage is that they change the exposure itself before you reach for outside products.

Use invoicing in the client's local currency when your negotiation position is strong and churn risk is low. This can make invoice value clearer for the client, but you still need to watch margin impact if your costs are in a different currency.

Use leading and lagging only when payment timing is realistic and contractually reliable. If timing is unclear or frequently missed, avoid timing shifts that can create friction or weaken trust. A timing tactic only helps when both sides actually operate on the timing written in the agreement.

Expand natural hedging before adding external products. Match same-currency income and expenses where possible so fewer conversions are needed and less cash flow is exposed to exchange-rate moves. In practice, that means checking whether upcoming same-currency costs can be covered directly from same-currency income before you convert everything out of habit.

| Internal method | Certainty gained | Client friction | Admin burden | Use it when | Main failure mode |

|---|---|---|---|---|---|

| Invoicing in local currency | Medium to high on invoice-value clarity | Low to medium | Low | You can set terms without raising churn risk | Margin pressure if costs are mostly in another currency |

| Leading and lagging | Medium when timing is reliable | Medium | Medium | Contract timing is explicit and consistently met | Trust damage if timing changes feel opportunistic |

| Natural hedging | Medium to high, based on match quality | Low | Medium | You have steady same-currency income and expenses | Weak tracking creates a false sense of protection |

Internal methods also reveal where your process is weak. If you cannot track same-currency inflows and outflows accurately, natural hedging will look stronger on paper than it is in practice. If clients rarely pay on the expected date, leading and lagging will create more noise than protection. That feedback is useful because it shows what needs fixing before you consider external tools.

A practical internal workflow is simple: when a foreign-currency payment becomes available, first check whether you have near-term same-currency obligations that can be covered directly. If yes, hold only the amount needed for those obligations and convert the remainder according to your rule. If no, convert on the schedule you set rather than leaving the balance unreviewed. This keeps natural hedging tied to actual payables instead of turning into an informal excuse to delay conversion.

Keep one monthly checkpoint: compare contract timing with actual settlement timing. If timing gaps keep widening, tighten payment terms first, then reassess whether you need external hedging. Do not keep treating the paper terms as the real exposure if the actual pattern says otherwise.

Use external hedging tools only when internal controls are not enough#

Use external hedging only for residual exposure after internal controls are working, and treat execution as a verification step, not a shortcut.

For a freelancer, the test is narrow: is the receivable clear enough that a binding rate lock solves a real cash-flow problem? If not, adding an external contract can leave you managing a separate obligation without fixing the business issue underneath it.

Forward contracts are the external tool to evaluate when receivables are predictable and timing is clearly defined in your agreement. If amount or timing is still unstable, keep the focus on tightening terms and payout reliability before expanding contract coverage.

External hedging should sit at the end of the decision chain, not the beginning. By the time you evaluate a forward, you should already know the invoice currency, expected amount, expected timing, and payout route. If any of those inputs still depend on guesswork, the process is not ready.

Keep contract risk separate from business risk. A hedge can address exchange-rate exposure, but it does not fix late payment behavior or invoice disputes. Write down what the hedge is meant to protect and what it is not meant to solve so you do not use a financial tool to compensate for weak collections.

That written distinction matters in practice. If an invoice is late, disputed, or delayed by provider processing, the problem may feel financial because the end payout changed, but the root issue may still be operational. External hedging works best when it is protecting a clean exposure with known timing. If you find yourself explaining the hedge with several moving reasons at once, the setup is probably not clean enough yet.

Before execution, confirm provider-specific constraints directly for your account and corridor, including eligibility, settlement mechanics, supported countries, and required compliance steps. If those details are unclear, treat that as an unresolved risk, not as a small admin detail. Keep whatever confirmation you receive with the invoice record so the hedge decision is linked to the actual product access and payout path available to your account. For legal interpretation, do not rely on FederalRegister.gov prototype pages alone: those pages state they are not the official legal edition and should be verified against official Federal Register editions (including govinfo.gov).

Run a monthly execution checklist that keeps decisions auditable#

Use one repeatable monthly checklist so each decision is easy to trace, review, and improve.

- Confirm receivables expected to settle in the current cycle.

- Apply your hedge rules against budgeted exchange rates.

- Execute the selected method (for example, natural hedging or forward contracts).

- Reconcile planned versus actual outcomes after payout, then log gaps and causes.

Each step should remove uncertainty, not add it. If an invoice no longer looks likely to settle in the current cycle, pull it out before execution. If the selected method changed, note why. If the outcome differed from plan, record whether the gap came from rate movement, fee impact, provider timing, client timing, or your own delay.

Keep one monthly evidence pack, even at low volume. Include invoice terms, chosen method, execution timestamps, provider confirmations, and brief outcome notes. One folder or file per month is enough if it lets you reconstruct the decision without relying on memory.

Make the evidence pack useful, not decorative. If you decided not to hedge, store that reason too. If a provider placed a hold or if conversion happened later than planned, keep the related confirmation with the file. The goal is to preserve the logic of the decision and the sequence of events around it. When you review later, you should be able to see what you expected, what you did, and where the path diverged.

Track the full money path with four status checks: payment received, funds available, conversion completed, and payout completed. When timing slips, record whether it came from client timing, provider timing, or your own execution choice.

An auditable file is useful because it lets you separate symptoms from causes. A poor result might look like an FX problem when the real issue was that funds sat unconverted after becoming available. It might look like a provider issue when the delay really started with the client. Without a clean record, you cannot improve the rule.

Add one policy/compliance checkpoint for account dependencies that affect execution, such as required verification steps or corridor availability where applicable. Keep legal interpretation tied to controlling rules, and treat older macro commentary as context rather than current operating guidance.

If you operate through an LLC, align this file with the same bookkeeping cadence you use for tax and expense records. See Separating Business and Personal Finances: An Important Step for LLCs.

Avoid the mistakes that make freelancers lose money even when they hedge#

Hedging protects cash flow only when you avoid preventable process errors. Use this screen before and after each decision:

| Mistake | Why it fails | What to do instead |

|---|---|---|

| Hedging uncertain receivables | If payment probability is weak or the amount or timing changes, the protection no longer matches a clean exposure | Pause financial contracts, tighten terms first, and confirm the invoice amount and approval status are stable enough to settle this cycle |

| Over-hedging small invoices | Complexity has a cost when exposure is limited | Keep methods simple when exposure is limited and reserve external contracts for larger, cleaner receivables |

| Copying enterprise playbooks without adapting them | A process that assumes constant monitoring or a treasury-style workflow is probably too heavy for a freelancer | Simplify execution to match solo cash-flow reality |

| Treating forum tactics as universal rules | What works in one corridor or account setup may fail in another | Check legal, tax, and provider implications for your setup |

| Skipping post-cycle review | Without reconciliation, you cannot tell whether your hedging rules reduced risk or just moved losses to a different step | Compare the plan with actual payout timing and the final cash outcome, not just the rate you expected to get |

- Hedging uncertain receivables. If payment probability is weak, pause financial contracts and tighten terms first. You want the invoice amount, timing, and approval status to be stable enough to settle this cycle. Otherwise, the hedge and the real exposure drift apart.

- Over-hedging small invoices. Complexity costs time and attention. When exposure is limited, tighter terms or staged conversion usually works better than another layer of admin.

- Copying enterprise playbooks without adapting them. Keep the principle, but simplify execution to match solo cash-flow reality. If a process assumes constant monitoring or a treasury-style workflow, it is probably too heavy for you to run consistently.

- Treating forum tactics as universal rules. Community tips can be useful prompts, but they are not policy until you check legal, tax, and provider implications for your setup. What works in one corridor or account setup may fail in another.

- Skipping post-cycle review. Without reconciliation, you cannot tell whether your hedging rules reduced risk or simply moved losses to a different step. Compare the plan with actual payout timing and the final cash outcome, not just the rate you expected to get.

The pattern behind these mistakes is false confidence: assuming the exposure is cleaner, smaller, or more controllable than it really is. Good hedging process is less about perfect prediction and more about refusing to act on weak inputs.

Another warning sign is when the explanation for a bad outcome keeps changing after the fact. If one month's result is blamed on the market, the next on the provider, and the next on the client, that may simply mean the original rule was not clear enough. Strong process makes it easier to say, with evidence, whether the miss came from pricing, timing, fees, settlement friction, or a preventable decision error.

Keep two grounding checks in place: define a forex payment as a cross-border payment that requires currency conversion, and track timing risk from transaction initiation through settlement. Also tag outside guidance by date so older market context does not drive current decisions. If a rule came from an earlier provider setup or older commentary, revisit it before repeating it.

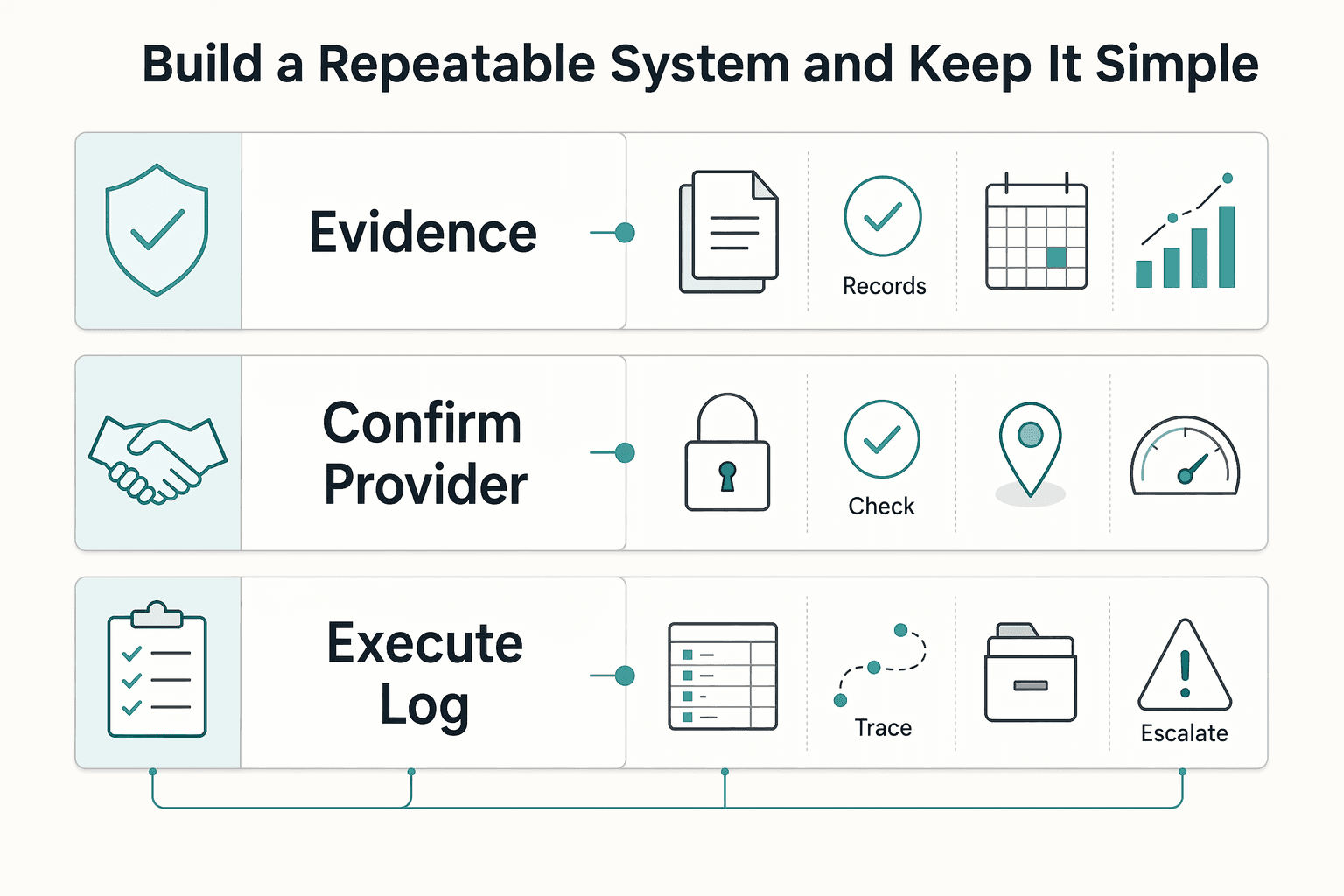

Build a repeatable system and keep it simple#

The most reliable hedge process is a repeatable monthly decision system, not constant market watching. Build from simple to complex: start with internal controls, add external tools only when exposure is clear and repeatable, and keep every step documented.

Keep one monthly cycle that is easy to audit:

- Record the rule before execution and why the invoice was hedged or not hedged.

- Confirm provider fit for the corridor using practical checks like fees, reach, and ease of use.

- Execute and log key timestamps, including exchange-rate checks.

- Reconcile planned versus actual outcomes and record one improvement for next month.

A good system answers the same questions every month and makes exceptions obvious. The point is not to make the perfect call every time. It is to make consistent calls from the same rule set so you can improve the process with evidence instead of memory.

This works only if your records are complete. In cross-border payment work, monitoring exchange rates and keeping detailed records are basic operating habits. Automation can support execution by syncing invoices, payments, and ledgers with accounting workflows and reducing manual work, but it does not guarantee savings in every case.

A useful sign that the system is working is that monthly review becomes easier, not harder. You should be able to tell quickly which invoices created real exposure, which method was used, what actually happened in settlement, and what should change next cycle. If the process is so complicated that you avoid the review step, simplify the rule set until it fits how you actually work.

Simplicity is a control. If a rule is too complicated to follow during a busy month, it will fail when you need it most. Use the same verification standard for every execution-critical claim: confirm legal and provider constraints in authoritative channels, document assumptions, and keep decisions auditable. For legal research, treat prototype Federal Register pages as informational and verify against official editions.

Frequently Asked Questions

What is currency hedging for freelancers?

It is a way to reduce foreign exchange risk between invoicing and payment. The main issue is timing: rates can move between when you invoice and when funds arrive.

Do I need hedging or just better invoice terms?

Start with invoice terms and payment behavior. If timing is unstable, tighter terms can be a practical first step before adding financial contracts. Add hedging when margin risk remains clear and repeatable.

What is the simplest low-complexity hedging method?

Start with internal controls. Use invoicing in local currency where it improves collections, and set an invoice-time exchange rate that you record and compare at payment. These methods are often simpler than external contracts.

How do I choose invoice currency versus convert later?

Base the choice on cost currency, margin buffer, and how long funds remain exposed to rate moves. If clients pay faster in their local currency, that can reduce friction and shorten open exposure.

How much exposure should I hedge?

Use a rule tied to payment certainty and margin sensitivity, not market opinions. There is no single hedge ratio that fits every freelancer.

When should I consider forward contracts?

Consider them when receivables are large enough to matter, timing is predictable, and internal controls are no longer enough. They can lock a future rate for larger amounts, but they do not remove all FX downside.

What varies by country or provider?

Payment-processor suitability can vary by currency. Fee examples and currency-support figures are snapshots, so verify them before execution.

Try a related tool

Yuki writes about banking setups, FX strategy, and payment rails for global freelancers—reducing fees while keeping compliance and cashflow predictable.

Sources

- bankingsupervision.europa.eu/framework/legal-framework/public-consultatio...trusted

- federalregister.gov/documents/2020/01/24/2020-00040/use-of-deriv...trusted

- federalregister.gov/documents/2020/12/21/2020-24781/use-of-deriv...trusted

- home.treasury.gov/system/files/206/December-2020-FX-Report-FIN...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.