Quick Answer

Start by deciding whether crypto tax loss harvesting fits this year’s realized gains, then execute only disposals supported by reconciled lot records. For U.S.-connected filers, run FBAR and Form 8938 checks before trading because they are separate filings. If basis data is incomplete or residency scope is unresolved, pause, reduce trade size, or get professional review before adding fast sell-and-rebuy sequences.

Crypto Tax-Loss Harvesting Requires Real Disposals and Defensible Records#

Crypto tax loss harvesting can lower capital gains exposure, but only when you turn a paper loss into a real disposal and can support the numbers afterward. A market drop by itself does not create a usable tax loss.

That is the central idea, and the rest is execution. Tax results are usually set at disposal by comparing the amount realized with adjusted basis. Sell above basis and you have a capital gain. Sell below basis and you have a capital loss. The math is simple. The hard part is getting the basis right when your history is spread across exchanges and self-custody wallets. If those records are fragmented or inconsistent, it is easy to sell the wrong assets, misstate the result, or overestimate the benefit.

Treat this as decision support, not individualized legal or tax advice. Outcomes depend on residency, filing profile, holding period, and local treatment of digital assets. In the U.S., holding more than one year is generally long-term, and one year or less is short-term. In Canada, dispositions can include selling, exchanging, spending, or gifting, and some wallet-to-wallet transfers you own may not be taxable disposals.

A practical rule runs through everything that follows: optimize only after you can defend the numbers. Before you trade, verify lot-level basis and transaction history across the platforms involved. On trade day, keep confirmations, exports, and reconciliation notes together so the final filing position is easier to trace.

You will usually make three decisions in order:

- Fit: decide whether harvesting belongs in this tax year based on realized or expected gains and your residency footprint.

- Execution: choose lots and timing that fit your portfolio intent, not just the tax result.

- Documentation: keep a filing-ready record trail so your position is explainable later.

That sequence matters. A common failure mode is executing first and trying to reconstruct the file later. You can sometimes still file on time, but with weaker support for basis, timing, and intent.

Keep one more caution in view as you read. Flexibility to rebuy does not make every rapid sell-and-repurchase pattern defensible. If a transaction appears to exist only to manufacture losses, authorities may challenge it and disallow the loss. The safest path is the boring one: clear basis, real investment intent, and records you can hand to another reviewer without a long explanation.

What crypto tax-loss harvesting actually does#

At its core, this strategy means selling digital assets that declined in value so you realize a capital loss that can offset capital gains. It becomes tax-useful only after a taxable disposal, and the result still depends on your filing profile and local rules.

That distinction between unrealized and realized losses is where most confusion starts. If a position is still unsold, the decline changes your portfolio value but usually does not change your taxes yet. The tax effect generally begins when you dispose of the asset for less than its basis. If you want a simple checkpoint, use this: no disposal, no harvested loss.

The upside is real, but it is not unlimited and it is not the same everywhere. Realized losses can reduce current capital gains exposure, and some jurisdictions allow losses to be used across tax years. Canada-focused guidance describes carrying net capital losses back to the three preceding years or forward indefinitely, but that treatment is not universal. The point is not to memorize every rule here. It is to stop assuming that a market loss will automatically help on your return.

It also helps to separate harvesting from two lookalike ideas. First, it is legal tax planning when reporting is accurate and the transaction is defensible. Second, it is different from simply holding through a drawdown, because holding does not realize a loss for tax purposes.

In practice, the order is disposal first, relief second. You do not claim a strategy in the abstract. You report a transaction and its measurable result. If the disposal record is weak, the tax benefit is weak too, even when the trade itself happened exactly as intended.

Before you execute, run a basic defensibility check:

- Reconcile cost basis across wallets and exchanges so you do not dispose of the wrong assets.

- Confirm the disposal actually realizes the loss you intend.

- Avoid trades that appear designed only to manufacture losses, since transactions without economic substance can be challenged.

Use those checks even for small trades. One minor reporting mistake might be fixable. The same mistake repeated across many disposals can erode the value of the whole exercise.

Should you harvest now or wait?#

Harvest now only when the benefit is real and the records are clean enough to defend. If either side of that equation is weak, waiting or scaling down is usually the better call.

| Decision | When to use it |

|---|---|

| Harvest now | Gains are material, lot data is reconciled, and your records are defensible. |

| Scale down | A benefit exists but repurchase timing would disrupt your holding plan. |

| Wait | Basis history is fragmented, exports are missing, or expected benefit is marginal. |

| Pause | The strategy depends on rapid rebuys you cannot defend with real investment intent. |

Realized losses help most when they offset capital gains in the same filing year. That is usually when the strategy is most efficient. In the U.S., net losses may also offset up to $3,000 of ordinary income at the federal level, but that is filer-specific and not a universal result. So the right question is not just whether a position is down. It is whether the realized loss has a clear use in your filing picture.

Portfolio intent still matters. If selling and rebuying would disrupt the holding timeline for a core position, harvesting a smaller slice or deferring may be smarter than forcing a full exit. A smaller, well-supported disposal is often easier to defend than an aggressive plan that looks good in a spreadsheet but is hard to explain from the records.

Avoid year-end panic trading. When wallet or exchange data is incomplete, you can easily sell the wrong lots and end up with little or no tax benefit. Reconcile cross-platform basis first. Then confirm the exact lot you intend to dispose of. That sequencing choice prevents a surprising amount of cleanup later.

Timing should also reflect compliance risk, not just market movement. According to the IRS digital assets guidance, reporting duties follow transaction type and facts, not social-media rules of thumb. Rapid sell-rebuy patterns that look purely tax-driven and lack economic substance can be challenged. The absence of a simple rule is not permission to ignore how the transaction looks.

If your records are mostly complete but one account is unresolved, split the decision instead of forcing an all-or-nothing move. Harvest only from the accounts you can defend now, then revisit the rest after reconciliation. That keeps the filing position cleaner and avoids contaminating a good trade with a weak record set.

Use the same checkpoint before placing orders:

- Harvest now when gains are material, lot data is reconciled, and your records are defensible.

- Scale down when a benefit exists but repurchase timing would disrupt your holding plan.

- Wait when basis history is fragmented, exports are missing, or expected benefit is marginal.

- Pause when the strategy depends on rapid rebuys you cannot defend with real investment intent.

The practical standard is simple. Prioritize clean execution over volume. One well-documented capital loss is usually better than a batch of rushed trades you cannot explain at filing time.

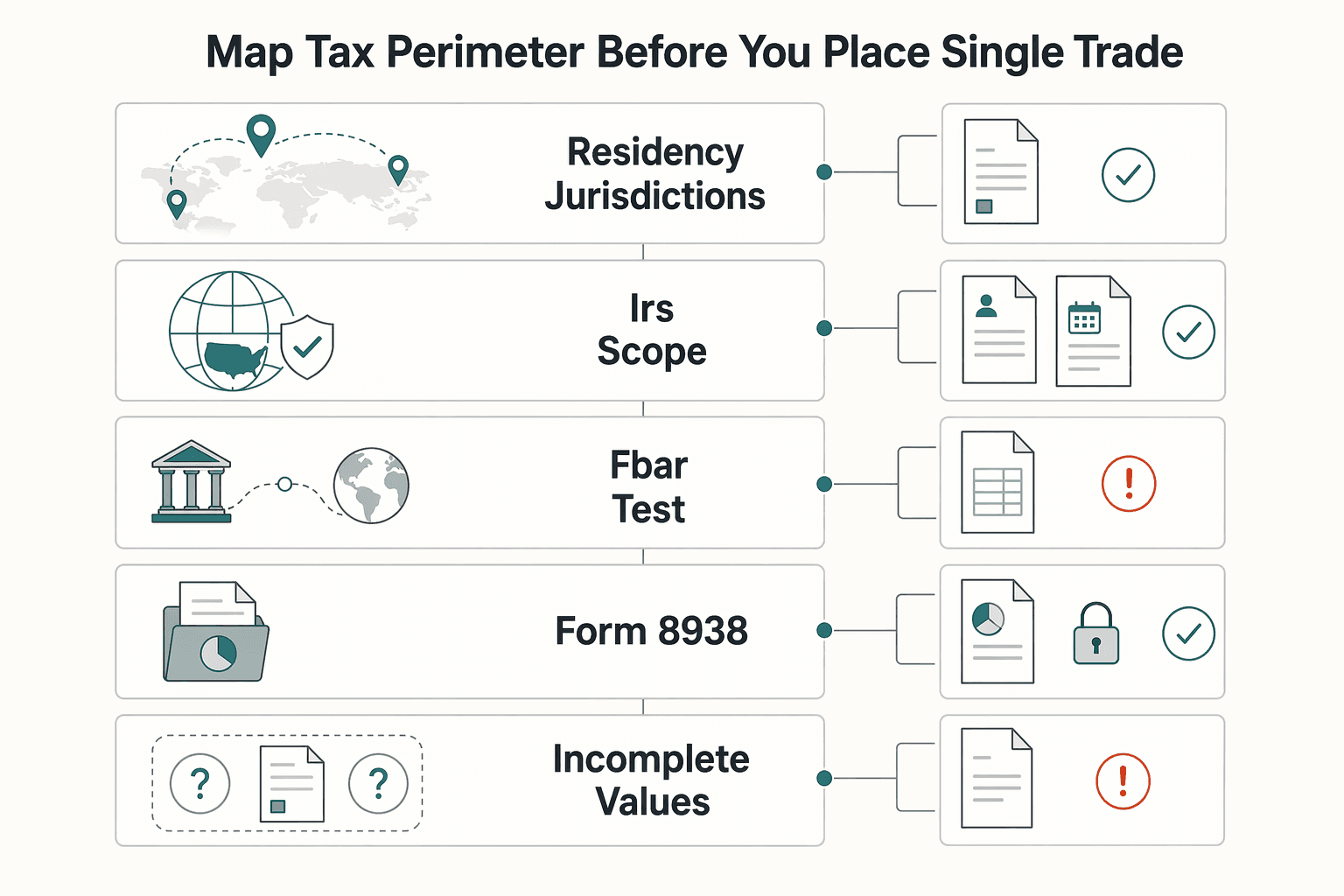

Map your tax perimeter before you place a single trade#

Set the filing perimeter first. If you are unclear on residency, filing jurisdiction, or U.S. reporting scope, the trading decision is not ready yet. Start with the Tax Residency Tracker so your day-count assumptions are explicit before trading.

| Check | What to confirm |

|---|---|

| Residency and jurisdictions | List where you are tax resident and where you expect to file this year. |

| IRS scope | Confirm whether your filer profile can trigger Form 8938 review. |

| FBAR test | Value each account separately, then check whether any single-account maximum or aggregate maximum exceeded $10,000 during the calendar year. |

| Form 8938 test | Apply the threshold set for your filer profile. A common baseline reference is aggregate value over $50,000 for certain U.S. taxpayers, and specified domestic entities can face a $75,000 at-any-time test. |

| Incomplete values | If you have fewer than 25 accounts and cannot determine whether aggregate maximum values exceeded the threshold, record that and use the FinCEN amount unknown step where applicable. |

This matters most for globally mobile filers, but the habit is useful for anyone with accounts across platforms or countries. Start with footprint: where you are tax resident, where returns are likely due, and whether you fall into a U.S.-linked filer category, including specified individuals for Form 8938 review. Once that is clear, separate the reporting tracks. Form 8938 is attached to your annual return and filed by that return's due date, including extensions. FBAR is a separate FinCEN filing with its own requirements. FATCA is the broader regime connected to Form 8938, and Form 8938 and FBAR are not interchangeable. If you are not required to file an income tax return, Form 8938 is not required.

A one-page perimeter note is a useful control here. In our workflow, we keep it simple. List the countries where you expect to file, the return type, and which reporting checks may apply, including a quick FBAR pre-check. It is not a legal opinion, and it does not need to read like one. Its job is to show why you believed a trade would land on a particular return and why you ran the next set of checks.

Use this same pre-trade checkpoint before execution:

- Residency and jurisdictions: list where you are tax resident and where you expect to file this year.

- IRS scope: confirm whether your filer profile can trigger

Form 8938review. - FBAR test: value each account separately, then check whether any single-account maximum or aggregate maximum exceeded

$10,000during the calendar year. - Form 8938 test: apply the threshold set for your filer profile. A common baseline reference is aggregate value over

$50,000for certain U.S. taxpayers, and specified domestic entities can face a$75,000at-any-time test. - Incomplete values: if you have fewer than 25 accounts and cannot determine whether aggregate maximum values exceeded the threshold, record that and use the FinCEN

amount unknownstep where applicable.

Do not treat unknown values as a small gap you can fix later. Unknowns should be logged and either resolved or escalated before you lock in optimization decisions. That discipline reduces late-stage surprises, especially when a good tax trade sits inside a weak reporting perimeter.

Once the perimeter is clear, the lot and timing questions get much easier. Without it, even a well-timed loss can create filing risk you did not mean to take on.

Before placing harvest trades, map your travel-day and filing footprint so your residency call is defensible: Use the Tax Residency Tracker.

Pick the right lots and avoid cost-basis errors#

Lot selection is where a sensible tax move often turns into a reporting mistake. If basis quality is weak, harvest fewer positions and fix the data first.

A loss is harvested when market value is below original purchase price, so your lot record has to be right before you place the order. Across multiple wallets and exchanges, that is not a small detail. It is the difference between realizing the loss you expected and discovering later that the software matched a different purchase history. For Canada filers, use adjusted cost base (ACB) when evaluating losses.

Misaligned basis settings are a common source of trouble. CoinTracker notes you can still file if settings drift, but reporting may be inaccurate, and current IRS-focused guidance makes the same point about keeping software and exchange cost-basis settings aligned. That is why basis verification belongs before trade placement, not after. It is also why a position that looks obviously underwater on one platform may not produce the number you expect once the full history is reconciled.

If you file in Canada, sequence trades carefully because repurchasing the same asset within 30 days can trigger superficial-loss denial. The legal labels matter less than the operating point: the lot method and the repurchase pattern both affect whether the loss holds up.

Before you select lots, run this checkpoint:

- Map each candidate position to the wallet or exchange account where it will be sold.

- Confirm amount to sell, market value, and recorded cost basis align for that position.

- Make sure your tax software lot-relief method matches the exchange setting for that account.

- Sort candidates using wallet, amount to sell, market value, cost basis, or max harvestable loss before you execute.

Add one more quality check right before the trade goes live: verify that the selected wallet and amount-to-sell details still match the lot you intend to dispose of. That final check is boring, but it catches the last-minute mismatch that otherwise shows up months later during filing.

The decision rule is straightforward. If basis quality is weak, reduce scope. A few well-documented disposals are more reliable than scaling the strategy across uncertain records.

Related: Vancouver, Canada: The Ultimate Digital Nomad Guide (2025).

Plan the sell-and-rebuy sequence without inviting challenges#

Rapid sell-and-rebuy patterns need more care than many investors give them. Treat the sequence as a recordkeeping job first and a portfolio decision second.

Some guidance says wash-sale rules can apply to harvesting and can differ across jurisdictions, so do not assume a universal answer. Treat any flexibility as a guardrail, not a loophole. Trades that look tax-only may still attract scrutiny, especially when the file is thin or the pattern looks like a quick round trip with no investment reason beyond the loss.

For U.S. filers, keep the reporting checkpoint central. Taxable gains or income from digital assets still need to be reported, and treatment depends on transaction type. That means each disposal and each rebuy should be logged as separate events with on-chain records, timestamps, values, and fees. If you do that in real time, the story of the trade is much easier to defend later.

Use this order every time:

- Select lots first: confirm units, quantity, basis, and account location.

- Execute the disposal: record execution time, proceeds, fees, and resulting loss.

- Capture evidence immediately: save exchange confirmations, wallet transaction IDs, and a short rationale.

- Evaluate re-entry last: rebuy only if it matches target allocation, and record the new lot's acquisition date.

That order reduces hindsight editing. If you document intent before and during execution, the record reads like a real investment decision with tax consequences. If you skip those steps and write notes afterward, the file can look like a tax-only pattern retrofitted after the fact.

The rationale note matters more than people think. If your only explanation is tax optimization, the file looks weak. A stronger note ties re-entry to allocation, concentration, or risk tolerance and explains what changed between the sale and the repurchase.

Build an audit-ready evidence pack on trade day#

The best time to build the file is the same day you trade. Waiting until return prep usually means you remember the result but not the path you took to get there.

| Evidence item | What it should show |

|---|---|

| Core transaction records | What happened, when, and for how much. |

| Methods note | Key assumptions used in your calculations. |

| Supporting balance or account context | Context from the relevant wallets and exchanges, where available. |

| Reconciliation notes | How your working records link back to source exports. |

| Brief index | How another reviewer can follow the file quickly. |

The goal is traceability, not paperwork volume. A compact, consistent evidence pack is more useful than a large folder full of unlabeled exports and screenshots. Another reviewer should be able to move from the transaction to the supporting records without guessing which file matters or how you derived the math.

Use this as a practical working bundle, not a legal checklist:

- Core transaction records that show what happened, when, and for how much.

- A short methods note explaining key assumptions used in your calculations.

- Supporting balance or account context from the relevant wallets and exchanges, where available.

- Reconciliation notes that link your working records back to source exports.

- A brief index so another reviewer can follow the file quickly.

Treat software output as a draft until you validate it. Software limitations are a known failure mode in crypto tax reporting, so sample-check transactions against raw exports before you close the file. This is especially important when lots move between exchanges and self-custody, because that is where a clean-looking report can hide a basis mismatch.

Keep compliance artifacts separate from raw exports so review is faster. If you receive formal compliance correspondence, such as an HMRC letter of enquiry, store it with a short reconciliation note that explains which records support your response. That keeps the audit trail coherent instead of scattering it across email, downloads, and tax software.

Portability matters too. Use a consistent folder structure, share redacted copies when needed, and keep a secure full record for your own files. If you use Gruv where supported, its tax document workflows and export artifacts, where enabled, can centralize traceability while limiting unnecessary PII exposure.

One small upgrade pays off repeatedly: keep a short change log in the evidence pack. Note what was corrected, when, and why. That makes later review faster and reduces the risk of conflicting versions when you or an advisor revisit the file.

Cross-border reporting traps freelancers miss#

A clean trading record is not enough if you treat forms as interchangeable. Tax optimization and reporting are separate tracks, and getting one right does not automatically satisfy the other.

For U.S.-connected filers, Form 8938 and FinCEN Form 114 (FBAR) are separate checks. According to the IRS Form 8938 instructions, Form 8938 is tied to the annual return and its due date. As published by the FinCEN FBAR filing page, FBAR is a separate filing channel with its own logic. Filing Form 8938 does not replace FBAR, and each form has its own requirements. If you want a fast internal screen, run the FBAR Calculator.

Threshold handling is another common problem. For FBAR, value each account separately using its maximum value during the calendar year, then check whether the single or aggregate maximum value reached $10,000 during the year. Form 8938 uses different asset and filing tests, and a commonly cited baseline is $50,000 for certain U.S. taxpayers. If you are not required to file an income tax return for the year, you generally do not file Form 8938 for that year. Use the FBAR Calculator to organize account-level maxima before final filing.

Classification can also break otherwise solid work. Some accounts maintained by U.S. payers can be exceptions under Form 8938 rules, so use account-level classification rather than broad labels. In practice, review what the account actually is, not what you call it in your spreadsheet.

Use this pre-filing check before you finalize:

- List each relevant account separately and record maximum yearly value for FBAR testing.

- Mark which items may be specified foreign financial assets for

Form 8938review. - Confirm whether you must file an annual income tax return for the year, since that affects

Form 8938filing. - If you cannot determine aggregate maximum values, for fewer than 25 accounts, use the FBAR "amount unknown" option where applicable.

- If obligations are unclear, escalate to a tax professional before filing.

Keep FATCA duties in scope, but do not guess. Resolve reporting obligations first, then lock in optimization positions. A strong trade file helps, but it does not fix a reporting framework you mapped incorrectly.

You might also find this useful: A Guide to QuickBooks Self-Employed for Freelancers.

When tax-loss harvesting is not worth it#

Do not harvest just because the market is down or the calendar is closing. If the expected benefit is small and execution is messy, the downside can outweigh the tax result.

Start with a hard gate. Consider selling only positions in taxable accounts that are below adjusted cost base. If adjusted cost base is uncertain, pause instead of forcing trades. That one rule eliminates a lot of unnecessary activity, especially when you are dealing with partial histories or inconsistent imports.

Complexity is another stop signal. Guidance on identical-asset repurchases is not framed the same way everywhere, including a 30-day framing in some contexts and a 61-day window around the sale in others. Loss-disallowance checks may also apply across multiple account and entity types. If timing rules are unclear, rapid sell-rebuy patterns are usually not worth the extra risk.

Also weigh strategy cost, not just tax outcome. A sold losing position can rebound after you exit, so harvesting can hurt if it breaks core exposure. Even when the loss is real and the paperwork is manageable, the portfolio tradeoff may still be unattractive.

Time cost belongs in the same analysis. If careful execution requires significant coordination across wallets, exchanges, and reporting checks, that effort may exceed the likely benefit for a small projected offset. In that case, deferring or scaling down is often the stronger decision.

Use this threshold test before placing any order:

- If projected benefit is modest and execution effort is high, scale down or skip.

- If adjusted cost base is unclear, do not trade yet.

- If identical-asset timing rules are unclear in your filing context, defer.

- If account or entity scope is unclear, pause until you can map it confidently.

- If uncertainty remains across rules and execution, get tax advice before making portfolio moves.

This is not an anti-harvesting section. It is a reminder that execution quality, not trade count, determines whether the strategy helps or creates rework.

Escalate to a tax professional when these triggers appear#

Get help early when reporting scope is unclear. Here, escalation is not a last resort. It is a control step that can prevent filing errors and conflicting records.

Foreign-asset reporting is not one combined task. Filing Form 8938 does not replace FBAR when FBAR is otherwise required, FBAR testing values each account separately, and Form 8938 is attached to your annual return and filed by that return's due date, including extensions. If your records do not cleanly support those differences, handing off early is usually cheaper than fixing the file later.

Timing matters here too. Escalation works best before you add more trades. Once more activity is layered in, the fact pattern is harder to explain, the calculations are harder to verify, and the advisor has less room to help you simplify the path forward.

Use this go-now trigger list:

- Multi-country filing exposure or uncertainty about which filing profile applies.

- Missing or conflicting account records needed to support maximum-value calculations.

- Uncertainty about whether

FBARandForm 8938both apply. - Uncertainty about whether

Form 8938is required for your year because of filing-status or threshold differences.

Thresholds are also a useful escalation checkpoint when you are near the line but not confident in your interpretation:

FBAR: if maximum value testing may exceed$10,000in a single account or in the aggregate during the year, and you are not confident in your calculation.Form 8938: if your profile may be near or above applicable thresholds, including$50,000for certain taxpayers, and you are unsure which threshold set applies.Form 8938: if you are unsure whether you must file an income tax return for the year, confirm that first, sinceForm 8938is tied to that return requirement.

When you do hand off, make it easy for the advisor to start in the right place. Give them a complete packet:

- Filing profile details that affect threshold selection, for example filing jointly or residing abroad.

- Account-level records and periodic statements used for maximum-value checks.

- A draft list of potentially reportable foreign financial assets and related accounts.

- Your current return timeline, including extension status and target filing date.

- A short list of open filing questions, for example overlap between

FBARandForm 8938.

Add a short cover note with the open questions at the top. Clear questions reduce back-and-forth and shorten the time to a defensible decision.

The practical rule is simple: if uncertainty touches both reporting scope and account-value calculations, pause new trades until a professional clears the path.

Conclusion#

The edge here is not finding the biggest paper loss. It is matching the right trade to the right lot, inside the right filing perimeter, with records you can defend later. If your travel pattern moved during the year, recheck assumptions in the Tax Residency Tracker before you scale.

Treat rebuy rules as jurisdiction-specific before you scale. One U.S.-focused source says crypto is not subject to the wash sale rule like stocks, where stock repurchases inside 30 days can limit deductions, while Canada-focused guidance says immediately rebuying the same asset can cancel the loss. If your filing facts are mixed or unclear, use the stricter path until a professional confirms treatment.

Use this checklist before scaling:

- Confirm your tax perimeter and where gains and losses will be reported this year.

- Validate cost basis and identify positions currently below it.

- Run small test trades first.

- Assemble complete exchange and wallet records for each trade.

- Scale only after records are internally consistent and intent is clearly investment-driven.

Set expectations on taxable impact, not headline loss size. Canada-focused guidance describes partial recognition with 50% treatment and gives an example where a $4,000 loss reduces taxable gains by $2,000.

If residency, classification, or reporting treatment is unclear, take the low-pressure next step and get a pre-trade review before year-end decisions lock in. You can prep that review with the Tax Residency Tracker and FBAR Calculator.

If cross-border account reporting is part of your picture, confirm applicable filing requirements before you finalize year-end filings: Run the FBAR Calculator.

Frequently Asked Questions

What is crypto tax loss harvesting in plain English?

It means selling crypto below your purchase price so the loss is realized for tax purposes. Unrealized losses stay on paper until you dispose of the asset. The goal is to use realized losses to reduce realized gains where your tax rules allow.

How much can a capital loss offset in practice?

Start with same-year realized gains, because realized losses can offset realized gains. Beyond that, treatment depends on jurisdiction. U.S.-focused guidance often cites up to $3,000 against other income, while Canadian guidance describes 50% treatment, possible carryback to the three preceding years, and carryforward indefinitely. The practical takeaway is to model your own filing profile instead of assuming one rule applies everywhere.

Does the wash sale rule apply to cryptocurrency right now?

Many explanations describe wash-sale limits as applying to stocks and securities, not all digital assets. That is not a blanket exemption across countries or future years. Classification can change, so treat this as a filing-year question and document the interpretation you relied on.

Can I sell and rebuy the same asset immediately?

Not everywhere. Canadian superficial-loss treatment can deny current-year use of a loss if you repurchase the same or identical investment in the window from 30 calendar days before the sale to 30 calendar days after. Some U.S.-oriented guidance mentions rebuying after 24 hours, but that is not a global rule. If your filing context is mixed, use the stricter path until your advisor confirms otherwise.

What records do I need from wallets and exchanges?

Keep transaction records from each exchange and wallet involved in your trades. Basis records should support purchase cost plus acquisition expenses, such as commissions or similar fees. Also confirm the assets were held in taxable accounts, since this approach is not treated the same way in retirement accounts.

How do acquisition date and cost basis change after rebuying?

A sell-and-rebuy generally resets both cost basis and acquisition date for the new position. That can change later gain or loss calculations. It can also affect holding-period strategy, so plan rebuys with that tradeoff in mind. Record the new lot details immediately so you do not have to reconstruct them later.

When should I stop and talk to a tax professional?

Stop when jurisdiction, classification, or filing treatment is unclear enough that outcomes can change by interpretation. Stop if your basis records are incomplete or conflicting. When facts are highly individualized, custom advice is the safer path before placing more trades.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- eba.europa.eu/sites/default/files/document_library/Calenda...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/businesses/small-businesses-self-employed/di...trusted

- irs.gov/instructions/i8938trusted

- bitdegree.org/crypto/tutorials/crypto-tax-loss-harvestingexternal

- forbes.com/sites/digital-assets/article/crypto-tax-loss...external

- gordonlaw.com/learn/crypto-tax-loss-harvestingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Using a Data Processing Agreement with Subcontractors

Put your data processing agreement in place before a processor or sub-processor gets access to personal data. If you use a processor, UK GDPR guidance requires a [written contract or other legal act](https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/accountability-and-governance/contracts-and-liabilities-between-controllers-and-processors-multi/when-is-a-contract-needed-and-why-is-it-important). Set that contract boundary before support logins, shared folders, or troubleshooting access turn into live processing.

Vancouver Digital Nomad Guide 2026 for Long-Stay Remote Work

If you are planning a longer stay in Vancouver, make the go or no-go call before you commit to non-refundable flights, deposits, or a long lease. This guide is about remote work planning in Canada, not short-trip sightseeing. The goal is to help you validate route, documents, and budget in the right order so one weak assumption does not force a rushed decision later.

A Guide to QuickBooks Self-Employed for Freelancers

**QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.**