Quick Answer

Croatia tax residency should be handled as a compliance decision system, not a one-off guess. Start with a status check under Croatia’s legal framework, then use the correct questionnaire path, build evidence for each key answer, and apply treaty tie-breaker analysis when two countries may claim you. If your facts conflict, mark status as uncertain and escalate before filing.

Croatia Tax Residency Without Guesswork#

Treat Croatia tax residency as a compliance decision you can defend later, not a tax hack you hope nobody questions. If you are a freelancer or consultant working across borders, use a process that turns messy real life into a clear, supportable position. You are the CEO of a business-of-one, and residency is one of those decisions you run like operations, not vibes. This guide stays compliance-first, gives you practical defaults, and shows you when to stop DIY and escalate.

Here is the core workflow. Keep it simple, and keep it disciplined:

| Phase | What you do | Safe default |

|---|---|---|

| Fast status check | Map your current facts against the applicable residency rules and treaty context under Article 4 of the Croatian Model of Tax Agreement. | If facts conflict, mark status as uncertain instead of forcing a conclusion. |

| Document workflow | Complete the relevant residency questionnaire and attach supporting records. Questionnaire TU supports non-resident to resident changes, and Questionnaire TI supports resident to non-resident changes. | Assume every answer needs evidence you can show later. |

| Escalation trigger | Escalate when your record shows ambiguity, cross-border conflict, or unresolved interpretation points. | Contact Porezna uprava directly and, where needed, involve a qualified adviser before you file. |

A few boundaries matter:

- This is an explainer, not individualized legal or tax advice.

- Public English-language materials may not confirm every procedural detail, so verify final steps before submission.

- When you submit a questionnaire, you are accountable for truthfulness, accuracy, and completeness. Documentation quality is not optional.

If your life is split between countries, do not anchor everything on a single rule. Run the checklist, assemble evidence, and escalate unresolved points early.

Use this section as your operating baseline. When you need broader multi-country controls, go deeper with The Ultimate Digital Nomad Tax Survival Guide for 2026. If you want a quick next step for "croatia tax residency," try the tax residency day counter.

Your Mental Model for Croatia Tax Residency#

Treat residency as a legal classification problem, then apply income scope and treaty rules from that classification. With the workflow in place, you need a mental model that keeps you consistent under pressure. This section gives you a clean way to reason through your status when your housing, work, and travel do not stay neatly inside one border.

Start with the legal backbone#

Croatia frames residency through domestic law, with treaty logic layered on when cross-border conflict appears. Use the same sequence every time: start with the General Tax Act, then the Ordinance for the implementation of the General Tax Act, then Article 4 of the Croatian Model of Tax Agreement when treaty issues arise. That order prevents ad hoc reasoning.

Tax residency is your legal status for income-tax scope. In Croatia, a resident taxpayer has permanent residence or habitual residence in the Republic of Croatia. A non-resident taxpayer has neither.

| Status | Core test language | Tax scope outcome |

|---|---|---|

| Resident taxpayer | Permanent or habitual residence in Croatia | Worldwide income principle (income in Croatia and abroad) |

| Non-resident taxpayer | No permanent or habitual residence in Croatia | Principle of domestic income (income acquired in Croatia) |

| Dual-claim case | Two states both claim residency | Apply Double Tax Treaty (DTT) tie-breaker rules under Article 4(2) |

Handle dual claims with evidence#

When two countries claim you, tie-breaker rules determine the stronger claim. A core factor asks where your personal and economic relations are closer, so the outcome should follow documented facts, not preference. If your situation stays split, build a file that makes those facts legible.

Treat the 183-day rule as a signal, not the entire framework. Croatia applies broader residence concepts, and published wording indicates that short interruptions of stay, including up to one year, are not decisive on their own. In practice, the move stays the same: classify status first, map income scope second, and escalate unresolved conflicts early.

Next-step checklist:

- Classify yourself as resident, non-resident, or dual-claim.

- Map each income stream to the correct scope before filing.

- If facts conflict, trigger DTT review and prepare your evidence pack.

Do You Trigger Croatia Tax Residency Under the Core Tests?#

Use a two-path test, then classify only after you verify your evidence. With the mental model set, run a concrete decision flow instead of guessing from a headline rule. This turns the question into yes-or-no checks you can defend during tax review.

Use a yes or no decision tree#

| Decision question | If yes | If no |

|---|---|---|

| Do you have real estate in your ownership or at your disposal in Croatia for an uninterrupted period of at least 183 days? | Treat the property pathway as triggered, even when you do not stay in that property every day. | Move to the physical presence pathway. |

| Are you physically present in Croatia for at least 183 days in one or two calendar years? | Treat the presence pathway as triggered, then validate with records. | Continue to non-resident analysis under PIT Act logic. |

| Do your facts stay split between Croatia and another country? | Flag the case for deeper evidence review before final classification. | Document your provisional status and keep a full support file. |

The 183-day rule matters, but it does not carry the whole decision on its own. Run both pathways, and document interruptions instead of hand-waving them away.

Build your evidence file before finalizing status#

Do not pick a final label first and hunt for proof later. Build your file while you run the tree:

| Evidence item | What to keep | Stated focus |

|---|---|---|

| Trip log | A log that matches your calendar, travel records, and work pattern | Build your file while you run the tree |

| Property access records | Records that show ownership or disposal period in Croatia | Supports the property pathway |

| Residency-tie records | Records of ties with the Republic of Croatia and with other countries | Those ties can decide hard cases |

| Questionnaire support | Documents backing key questionnaire answers | Unsupported statements create risk |

Make those records agree with each other. Your trip log should match your calendar and travel records. Property access records should show the ownership or disposal period in Croatia. Ties to the Republic of Croatia and to other countries should be explicit, because those ties can decide hard cases. And if a questionnaire answer matters, back it with documents.

If your year is split across borders, the win is not a clever interpretation. The win is a clean file that makes your story consistent across logs, contracts, and filings.

Related: The Future of the Agency Model in the Age of AI.

What Happens If Two Countries Claim You as Tax Resident?#

When two countries claim you, resolve the conflict through treaty tie-breaker rules backed by objective evidence, not preference. You already ran the core residency checks. Now you need a conflict workflow for mixed facts across borders. This is where people get hurt by treating one factor as decisive.

Run the conflict workflow in order#

Start with facts, then apply the relevant Double Tax Treaty (DTT) rules. Keep the sequence tight:

| Step | Action | Record or check |

|---|---|---|

| 1 | Build a fact file first | Capture objective ties across jurisdictions and keep the supporting records organized |

| 2 | Map facts to Article 4(2) tie-breaker rules | Do not skip straight to a conclusion because one data point looks favorable |

| 3 | Test consistency | Check whether your position stays consistent across your records and filings |

| 4 | Write your residency memo | State why one jurisdiction has the stronger claim and keep supporting records ready for review |

The order matters. Facts come first, treaty analysis comes second, consistency testing comes third, and the written memo comes last. If your facts are split, do not treat the tie-breaker as a simple hierarchy. You need structure, evidence, and a rationale that holds together.

Understand what changes when you classify wrong#

| Classification outcome | Income-tax scope effect |

|---|---|

| Resident position holds | Exposure can extend to income under the worldwide income principle. |

| Non-resident position holds | Exposure generally centers on Croatian-source income. |

That difference is why you should treat treaty analysis as a decision system, not a one-line argument. If your evidence conflicts, escalate early and resolve the conflict before you lock your filing position.

Which Forms and Documents Keep Your Position Defensible?#

Use Questionnaire TU or Questionnaire TI with matching evidence to make your residency position defensible. Once your classification logic is clear, the next job is proving it. This is the operational layer. You are packaging your story so Porezna uprava can review it quickly and consistently, especially when your facts are cross-border.

Croatia's residency determination process runs through the General Tax Act and the Ordinance for the implementation of the General Tax Act. When treaty issues arise, it also runs through Article 4 of the Croatian Model of Tax Agreement. In that process, questionnaires are part of status determination, not optional narrative forms.

Use the required Croatia forms#

| Form | When to use it | Evidence focus |

|---|---|---|

| Questionnaire TU | Change from non-resident to resident of the Republic of Croatia | Presence dates, housing status, permit details, and records that support each answer |

| Questionnaire TI | Change from resident to non-resident of the Republic of Croatia | Facts supporting the status change and related ties, with records that support each answer |

Submit the completed questionnaire with your taxpayer register application for registration or deregistration. Keep one discipline rule: when your facts change, update your file promptly and follow the change window described in the form instructions.

Build one audit-ready packet around both forms:

- Travel logs and date-level presence records you can substantiate.

- Housing-status records and permit context that align with your questionnaire answers.

- Status-change and residency-tie facts, with supporting records for each declaration.

- Filing correspondence and confirmation records tied to each declaration.

Add U.S. annexes when relevant#

If you are a U.S.-linked freelancer, keep a separate annex for cross-border reporting:

- FBAR (FinCEN Form 114): file with FinCEN, not the IRS.

- FATCA Form 8938: do not treat this as a replacement for FBAR.

- Schedule SE (Form 1040): use it to compute self-employment tax.

- Keep FinCEN confirmations, account support records, and IRS filing copies together.

The goal is one packet that a professional can review without re-interviewing you from scratch.

When Should You Talk to a Pro Instead of DIY?#

Talk to a qualified adviser as soon as your facts conflict across countries, timing, or filing systems. You have the forms and the evidence workflow. Now set a hard escalation rule so you do not force a DIY answer when the facts are split or unclear.

Escalation triggers you should treat as mandatory#

Use this decision grid before you file:

| Trigger | Why DIY gets risky fast | What to do next |

|---|---|---|

| Dual-residency indicators | Family location points to one country while usual work pattern points to another, so tie-breaker judgment drives the outcome. | Run Article 4(2) Double Tax Treaty (DTT) analysis with an adviser and document your rationale. |

| Inconsistent cross-border facts | Your records and residency statements do not tell one coherent story. | Reconcile records first, then review your file with a specialist before submission. |

| Mid-year status change | A change in facts can trigger a Croatian reporting update window, including a 30-day notification timeline in form guidance. | Flag the change immediately and confirm filing sequence with a pro. |

| Uncertain treaty interpretation | You cannot confidently map your facts to tie-breaker rules. | Escalate early, then contact Porezna uprava directly if questions remain unresolved. |

Do not rely on a single day-count test alone in these cases. It can help you track patterns, but it will not resolve the hard calls.

U.S. overlap that should trigger professional review#

If you touch U.S. obligations, raise your escalation level:

- Check whether you must file Form 8938, FBAR, or both. One does not replace the other.

- Treat late or missing foreign-account reporting as a remediation issue, not a quick correction.

- Review eligibility for the IRS Streamlined Filing Compliance Procedures only when facts support non-willful conduct.

- Keep FinCEN and IRS records aligned with your Croatia residency narrative.

If you want a broader cross-border control system, use The Ultimate Digital Nomad Tax Survival Guide for 2025 as your next playbook.

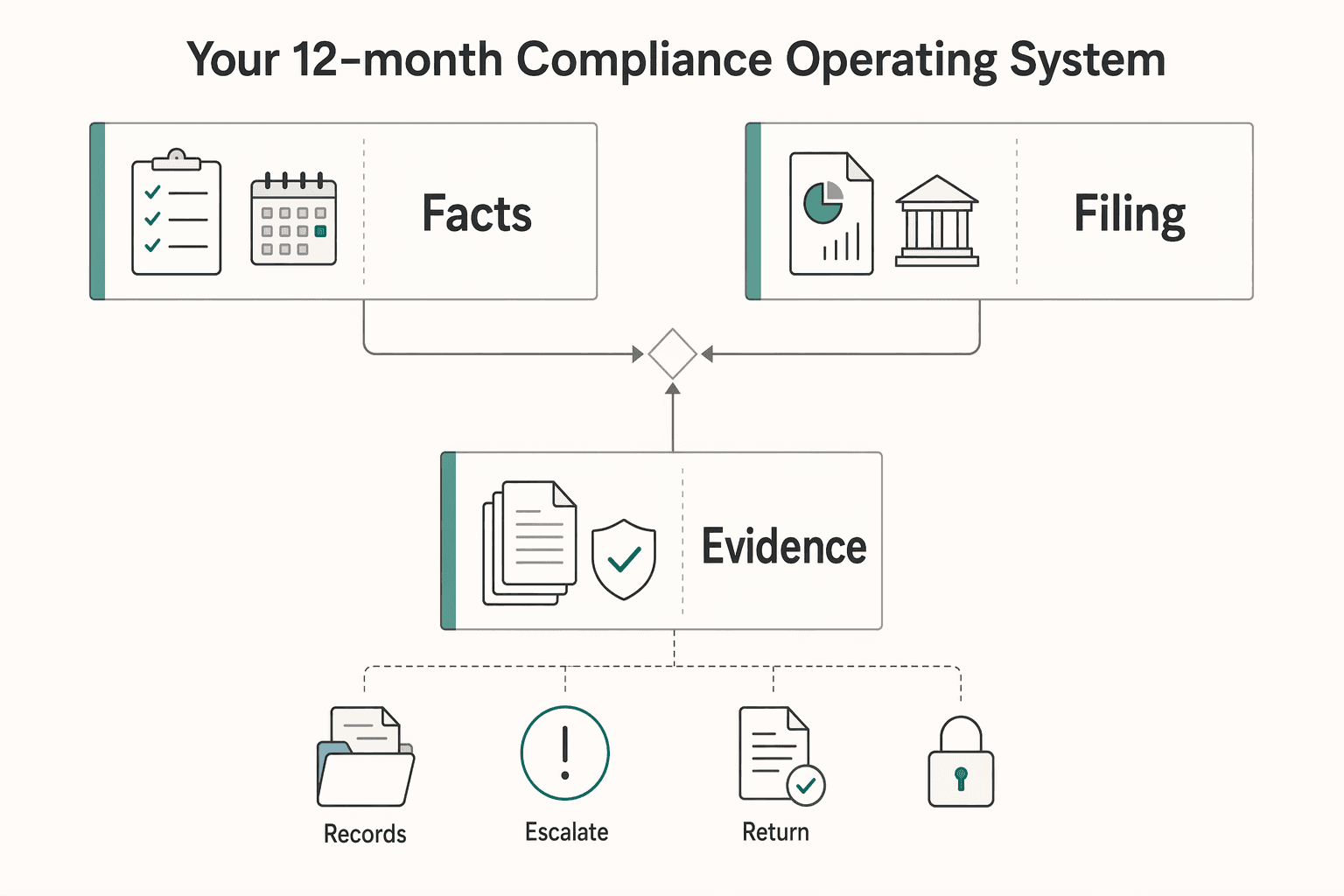

Your 12-Month Compliance Operating System#

Run your Croatia tax file as a repeatable operating cadence, then close the year with a written reconciliation of assumptions against records. You know when to escalate to a professional. Next, build a control system that catches issues early, before filing pressure creates rushed decisions. Treat this as operations, not theory, and keep your file defensible across Croatia and any other jurisdiction touching your expat tax footprint.

Use one standard for the Republic of Croatia file. Every decision needs a timestamp, a reason, and matching evidence. That rule helps keep your narrative coherent when facts split across countries, providers, or payout rails.

Run the quarterly control loop#

Set a quarterly review block and a year-end close process.

- Recheck your working assumptions for tax in Croatia and flag any fact that changed.

- Reconcile travel records, contracts, invoices, and payout histories in one timeline.

- Tag each payment under your operating classification, including source and benefit categories relevant to your file logic.

- Export a clean adviser packet with folders for decisions, raw documents, and open questions.

| Control gate | What you verify | Evidence to export |

|---|---|---|

| Residency narrative check | Your written assumptions still match current facts | Quarterly memo plus change log |

| Cashflow alignment check | Invoice and payout records match your classification labels | Ledger export, invoice set, payout statements |

| Escalation check | Split facts or unresolved items trigger adviser review | Issue tracker with owner and next action |

Classify payments and benefits with proof first#

Employment income includes salaries and other cash or in-kind remuneration. Non-taxable benefits can apply, but you still need to enforce the conditions and capture proof when you book each item.

| Category | Amount | Context |

|---|---|---|

| Business trips in Croatia | EUR 30 per diem | Listed as a verification checkpoint before filing |

| Personal car business use | EUR 0.50 per kilometre | Listed as a verification checkpoint before filing |

| Eligible voluntary pension premiums | EUR 67 per month (EUR 804 per year) | Listed for eligible voluntary pension premiums |

| Work performance awards | EUR 1,200 | Listed as a verification checkpoint before filing |

| Occasional awards | EUR 700 per year | Listed as a verification checkpoint before filing |

Build simple policy gates into your workflow:

- Record meal reimbursements only with invoice proof.

- Treat business-trip allowances as country-dependent and confirm the applicable implementation each cycle.

- Treat listed caps as verification checkpoints before filing for the listed categories, including EUR 30 per diem for business trips in Croatia, EUR 0.50 per kilometre for personal car business use, EUR 67 per month (EUR 804 per year) for eligible voluntary pension premiums, EUR 1,200 for work performance awards, and EUR 700 per year for occasional awards.

Keep time and document tracking as signals, not your full control system. If your file also includes other-jurisdiction items from earlier sections, use the same period tags across all annexes so your story stays consistent end-to-end.

Build a Low-Stress Residency File You Can Defend#

Build your residency position as a decision system, not a one-time guess, and keep a file another professional can verify fast. You have the workflow, the forms, the escalation triggers, and the operating cadence. This last step turns all of that into a defensible close process, especially when facts split across countries. The target is practical: every conclusion in your file should point to dated evidence and a clear decision rule.

Run a repeatable close checklist#

Use one annual cycle and follow it in order, from 01 January to 31 December.

- Re-run your status tree and determine where you are a resident taxpayer before you apply any Double Tax Treaty (DTT) outcome.

- If your status changed, use the correct form path: Questionnaire TU for non-resident to resident changes, and Questionnaire TI for resident to non-resident changes.

- Treat documentary support as essential. Back key questionnaire answers with the supporting documents requested in the questionnaire.

- Focus on ties to the Republic of Croatia and other countries, because those ties drive difficult residency calls.

- Flag unresolved items early and escalate for professional review when your analysis stays split.

| Control | Safe default | Escalate when |

|---|---|---|

| Residency decision | Determine residency first, then apply treaty tie-breaker rules (Article 4) | Two countries still claim you after your fact review |

| Questionnaire package | Submit the right questionnaire and attach supporting documents requested by the questionnaire | Your file contains gaps or conflicting statements |

| Final authority check | Confirm unresolved procedure questions with Porezna uprava | You cannot reconcile dual-residency interpretation internally |

Finish with clear next actions#

Do not force certainty when facts stay ambiguous. Ask a qualified adviser for treaty conflicts and bring your audit-ready records. Keep the 183-day rule as a signal, not your full model.

For deeper execution, read The Ultimate Digital Nomad Tax Survival Guide for 2025. If you also want deduction-side controls, read Can Digital Nomads Claim the Home Office Deduction?.

Frequently Asked Questions

What makes you a tax resident in Croatia?

Croatia tax residency follows domestic tests plus treaty logic. A common summary uses two pathways: real estate in your ownership or at your disposal for an uninterrupted 183-day period, or physical presence in Croatia for at least 183 days in one or two calendar years. For expat tax work, use the 183-day rule as one control, then validate with housing, ties, and documentation.

Do you owe Croatia tax on worldwide income?

If you are a resident in the Republic of Croatia, tax scope can include income earned in Croatia and abroad under a worldwide income principle. If you are a non-resident, Croatia generally taxes income acquired in the country. That scope decision should happen before you start arguing about rates, deductions, or treaty relief.

What if both Croatia and another country claim you as a tax resident?

Use treaty tie-breaker analysis under Article 4, including the Article 4(2) procedure when facts conflict. Croatia’s residency questionnaires can support that process, but they do not replace a coherent fact file. If family and work patterns point in different directions, treat your status as uncertain until you document ties and run the treaty workflow.

Which forms are used to change Croatian tax residency status?

Porezna uprava states that Questionnaire TI is used when changing status from resident to non-resident. Attach supporting records so your questionnaire and evidence tell one consistent story. For other status-change workflows, confirm current form naming and submission steps before you file.

Is having housing available in Croatia enough to trigger residency?

Housing availability can trigger residency analysis when real estate is available for the required 183-day period. In that pathway, continuous physical stay in that property is not the deciding factor. You still need to review your full cross-border fact pattern before final classification.

What is still unclear and should be confirmed with a professional?

Confirm procedural details under the General Tax Act and the Ordinance for the implementation of the General Tax Act when your facts are unusual. Confirm current administrative practice with Porezna uprava if your year includes status changes or competing country claims. If facts stay uncertain, default to documentation first, then get a review.

How does Croatia tax residency interact with IRS, FBAR, and FATCA obligations?

Croatia tax residency does not remove U.S. filing duties if you are a U.S. citizen or resident abroad. If U.S. reporting applies to you, treat it as a parallel workstream: keep FinCEN and IRS records consistent with your Croatia residency narrative, and escalate early when accounts, filings, or timelines do not line up.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

The Future of the Agency Model in the Age of AI

AI can increase agency speed, not agency responsibility. The future of agencies with AI is less about producing more output and more about deciding who owns judgment as execution gets faster. When automation is treated as a shortcut, weak briefs, unclear approval rights, and late client communication surface sooner.