Quick Answer

Start by mapping your case to the right lane, then pick the credential. In cpa vs enrolled agent vs tax attorney decisions, CPAs, EAs, and attorneys can all represent clients before the IRS for audits, collections, and appeals, so the split is usually role fit and escalation risk. Use a CPA or EA for filing cleanup and administrative notice work, and move to a tax attorney when legal interpretation, privilege needs, or likely Tax Court movement appears. Confirm scope in writing before engagement.

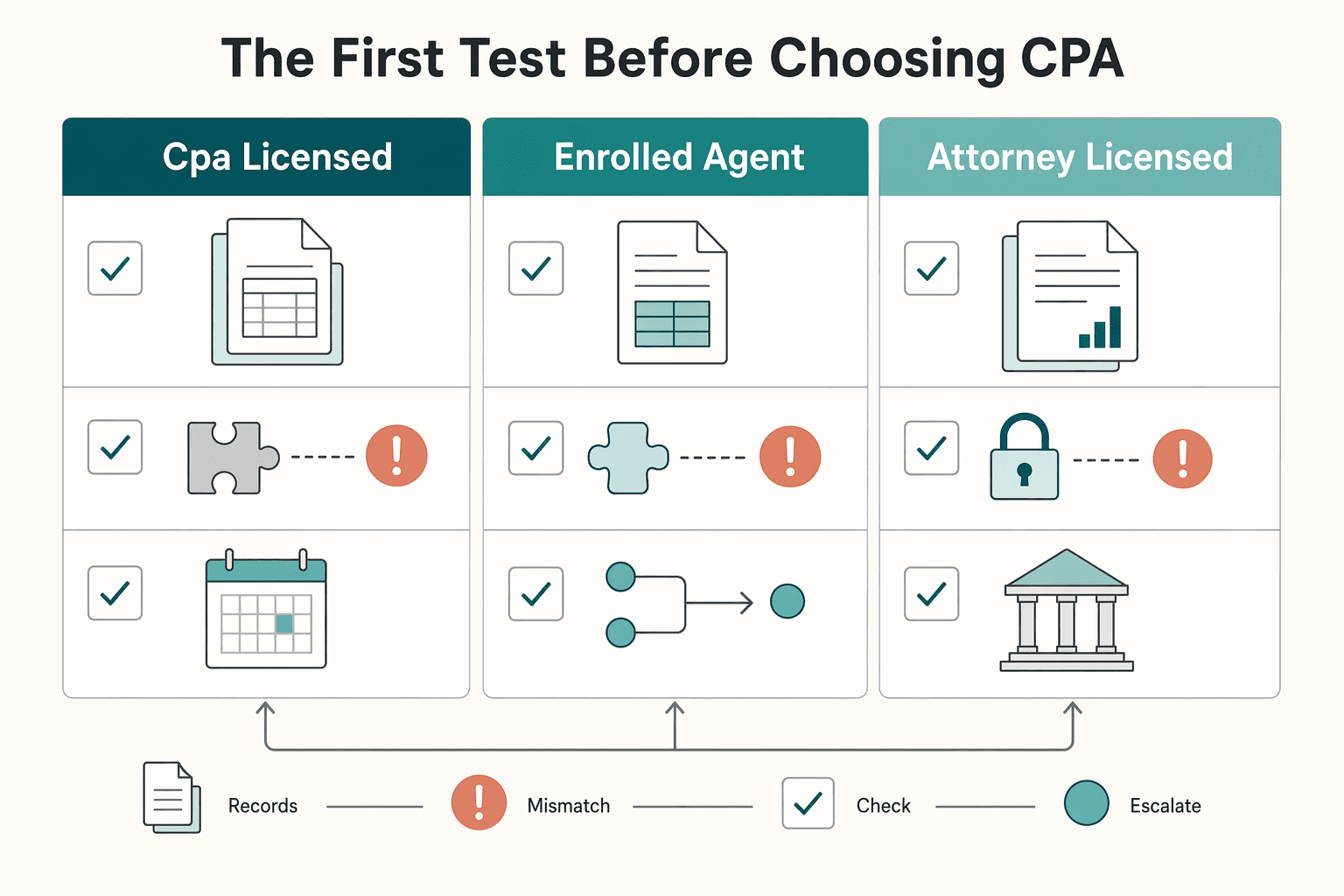

Case stage and representation rights: the first test before choosing CPA, EA, or tax attorney#

Choose by case stage and representation rights, not by title prestige. In cpa vs enrolled agent vs tax attorney, the safest first move is to match the credential to the work in front of you and the likely escalation path if the IRS pushes back.

You can make a solid first decision quickly if you focus on three things: decision rules, an escalation path, and a document checklist. Pick the right first lead, then decide when to escalate.

Start with one distinction that trips people up. Return preparation authority is not the same as IRS representation authority. Any tax professional with a PTIN can prepare federal tax returns, but the IRS is clear that practitioners differ in skills, education, and expertise.

When representation risk is on the table, start with this checkpoint. Enrolled agents, certified public accountants, and attorneys have unlimited representation rights before the IRS, including audits, payment or collection issues, and appeals. Some other preparers may only represent clients on returns they prepared and signed, and cannot represent clients in appeals or collection issues, even if they prepared the return.

The credential boundaries are straightforward:

- A CPA is licensed by state boards of accountancy and has passed the Uniform CPA Examination.

- An enrolled agent is licensed by the IRS, must pass a three-part Special Enrollment Examination, and must complete 72 hours of continuing education every 3 years.

- An attorney is licensed by state courts or their designees, generally after earning a law degree and passing a bar exam.

Be cautious about price comparisons. The evidence here is strong on licensing and representation rights, but not on broad national fee comparisons. Start with role fit and escalation coverage before you compare cost.

At-a-glance comparison for CPA vs EA vs Tax Attorney#

Use case stage as your first filter: a CPA for accounting-heavy cleanup, an EA for IRS administrative matters, and a tax attorney when legal exposure is credible.

| Comparison point | CPA | EA | Tax Attorney |

|---|---|---|---|

| Licensing path | Licensed by state boards of accountancy; passed the Uniform CPA Examination | Licensed by the IRS; passed a three-part Special Enrollment Examination; must complete 72 hours every 3 years of continuing education | Licensed by state courts or bar authorities; generally has a law degree and passed a bar exam |

| Federal return prep authority | Can prepare federal returns with a PTIN | Can prepare federal returns with a PTIN | Can prepare federal returns with a PTIN |

| IRS administrative level work (IRS audit, IRS collections, IRS appeals) | Unlimited representation rights before the IRS, including audits, collections, and appeals | Unlimited representation rights before the IRS, including audits, collections, and appeals | Unlimited representation rights before the IRS, including audits, collections, and appeals |

| Tax Court and criminal tax matters | Confirm with the relevant authority | Confirm with the relevant authority | Available sources explicitly tie tax attorneys to Tax Court representation; serious legal exposure is the escalation point |

| Legal privilege | No attorney-client privilege claim supported here | No attorney-client privilege claim supported here | Available sources tie attorney representation to attorney-client privilege in serious IRS legal matters |

| Best-fit use cases | Accounting-record cleanup where books or reconciliations are the bottleneck | IRS notice response, collections pathways, and administrative resolution | Likely Tax Court path, or risk of fraud, criminal scrutiny, or DOJ involvement |

| Best first hire for this scenario | Accounting-heavy cleanup | Active IRS notice still at the administrative level | Potential legal exposure where privilege or court-capable representation may matter |

The key boundary is administrative IRS work versus court or criminal exposure. Audits, collections, and appeals are one lane. Tax Court and criminal-risk matters are another.

That split leads to a practical rule. Start with a CPA or EA for notice response and administrative resolution, then escalate if the facts change. If fraud allegations, criminal scrutiny, DOJ involvement, or a likely Tax Court path are on the table, start with a tax attorney.

Before hiring, verify scope directly. Ask, "Will you represent me through IRS appeals if this escalates?" and "At what point would you bring in a tax attorney?" Choose by fit and escalation coverage first, not title prestige or a headline hourly rate.

Licensing paths and IRS representation scope are clear in IRS materials. Broad fee rankings between credentials are less certain, so they should not drive your first decision on their own. If you want a broader advisor comparison, see The Best Accounting and Tax Advisors for US Expats.

What each credential actually authorizes in practice#

The useful question is not who sounds most senior. It is who is authorized for the work you need and fits the lane your case is in.

Certified Public Accountant#

A Certified Public Accountant (CPA) is licensed by state boards of accountancy, including the District of Columbia and U.S. territories, and has passed the Uniform CPA Examination. In practice, CPAs are often most useful when accounting execution is the bottleneck: filing, planning, bookkeeping cleanup, and reconciliations.

CPAs also have unlimited representation rights before the IRS on audits, payment or collection issues, and appeals. If your issue is both records-heavy and administrative with the IRS, that mix is why a CPA is often a practical first hire.

Enrolled Agent#

An Enrolled Agent (EA) is licensed by the IRS and focused on federal tax practice. The credential requires a suitability check, a three-part Special Enrollment Examination, and 72 hours of continuing education every 3 years.

With a PTIN, an EA can prepare federal returns, and EAs have unlimited representation rights before the IRS, including audits, payment or collection matters, and appeals. If your issue is mainly federal tax rules and IRS process, an EA is often a direct fit. For a deeper breakdown, see What is an Enrolled Agent (EA) and When Should You Hire One?.

Tax Attorney#

A tax attorney is a lawyer licensed by a state court, the District of Columbia, or a bar-designated authority. They generally have a law degree and bar admission. Attorneys also have unlimited representation rights before the IRS.

The practical difference is legal-risk handling. Think legal analysis, legal-position strategy, and matters that may move toward litigation. For this guide, the clearest court-related support ties tax attorneys to Tax Court representation.

What "can represent you" actually means#

Treat representation as a scope question, not a yes-or-no label. It can include:

- Responding to IRS correspondence

- Handling audits

- Negotiating payment or collection issues

- Building and defending the record in appeals

- Coordinating legal strategy if escalation is likely

Use a two-step hiring check: confirm the credential, then confirm escalation coverage. A common failure mode is hiring based on PTIN alone. Some preparers with limited rights cannot represent clients in appeals or collection matters even if they prepared the return. If your situation also involves mobility or residency questions, Canada Tax Residency Ties for Freelancers Who Move Often covers a related fact-pattern issue.

Where representation lines matter most#

Representation lines matter most when a case stops looking like a normal IRS administrative matter and starts moving toward court or higher legal risk. That is where hiring mistakes get expensive.

| Matter | CPA | EA | Tax attorney |

|---|---|---|---|

| IRS audit | Can represent before the IRS | Can represent before the IRS | Can represent before the IRS |

| IRS appeals | Can represent before the IRS | Can represent before the IRS | Can represent before the IRS |

| IRS collections | Can represent before the IRS | Can represent before the IRS | Can represent before the IRS |

| Tax Court | Do not assume court representation; verify admission and who files or signs | Do not assume court representation; verify admission and who files or signs | Practitioner sources present this as attorney-led; verify Tax Court admission and procedure |

| Potential criminal exposure | Confirm with the relevant authority | Confirm with the relevant authority | Not established here as defense scope; treat this as legal-risk triage and verify the right counsel path |

The first three rows are straightforward because IRS guidance is explicit. EAs, CPAs, and attorneys have unlimited representation rights before the agency, including audits, collection or payment matters, and appeals. The harder part is escalation.

Use two practical checkpoints. First, a statutory notice of deficiency is a clear signal to switch from a tax-prep mindset to legal-risk triage. Second, if the IRS shifts from reviewing your return to questioning your conduct, treat that as immediate escalation.

At that point, privilege posture matters. In the source material for this guide, attorney-client privilege is a real distinction, and non-attorney communications may not carry the same protection. Before you sign, ask directly: if this matter escalates, who takes the next procedural step, and what is the handoff plan?

The source material for this guide also includes conflicting practitioner statements on non-attorney court representation, so do not rely on assumptions about Tax Court eligibility without verifying the exact procedure for your case.

The 10-minute decision sequence for low-stress compliance#

If you want a quick, low-drama decision, start with the lane, then match the professional. A common mistake is starting with the title instead.

| Step | Focus | What to confirm |

|---|---|---|

| Classify the issue by lane | Filing and planning, an IRS administrative-level dispute, or a matter that may move beyond administrative IRS work | Keep prep and representation separate |

| Score urgency and downside | Check deadlines, open notices, missing filings, and whether the facts suggest more than a paperwork issue | Gather all IRS notices, response dates, and tax years that are missing or in question |

| Choose the initial owner and escalation rule | For routine compliance, filing backlog, and IRS administrative disputes, a CPA or EA can be a practical first lead | Ask who stays lead if this escalates and who takes over the next procedural step |

| Define the success artifact | Examples include missing returns prepared and filed, notice responses submitted, documented IRS communications, or a completed financial disclosure package | For legal-risk triage, request a written strategy memo or written next-step recommendation |

| Set a 30-day review checkpoint | Verify deadlines are calendared, records are gathered, and a lead strategy is set | Make sure at least one concrete action is complete |

Classify the issue by lane#

Classify the issue by lane before you pick a title. Many situations fit one of three lanes: filing and planning, an IRS administrative-level dispute, or a matter that may move beyond administrative IRS work.

Keep prep and representation separate in your mind. Any professional with a PTIN can prepare a federal return, but representation rights differ. The IRS states that EAs, CPAs, and attorneys have unlimited representation rights before the agency, including audits, payment or collection matters, and appeals.

Score urgency and downside#

Score urgency and downside next. Check deadlines, open notices, missing filings, and whether the facts suggest more than a paperwork issue.

A common complexity pattern is multiple unfiled years with penalties and collection notices. That usually means more document preparation and more IRS communication. Before hiring, gather all IRS notices, list response dates, and list tax years that are missing or in question.

Choose the initial owner and escalation rule#

Choose the initial owner and set the escalation rule in the same conversation. For routine compliance, filing backlog, and IRS administrative disputes, a CPA or EA can be a practical first lead because both can represent you before the IRS in audits, collections, and appeals.

Escalate when the work starts shifting from return mechanics to legal-risk strategy or potential non-administrative proceedings. Ask directly: who stays lead if this escalates, and who takes over the next procedural step if needed?

Define the success artifact#

Define the success artifact before the engagement starts. "Help me with the IRS" is too vague, so name the concrete output you expect.

Examples include missing returns prepared and filed, notice responses submitted, documented IRS communications, or a completed financial disclosure package. For legal-risk triage, request a written strategy memo or written next-step recommendation so progress is visible and testable.

Set a 30-day review checkpoint#

Set a 30-day review checkpoint to confirm progress. This is not a legal requirement. It is an operating control.

At that checkpoint, verify deadlines are calendared, records are gathered, and a lead strategy is set. Also make sure one concrete action is complete, such as filing missing returns, answering a notice, preparing financial disclosures, or opening an IRS communication channel. If progress is weak, keep control of the case by narrowing scope, adding support, or replacing the lead.

For more on workflow discipline, see The Best Tax Research Software for Accountants. If your next step is clarifying day-count and residency facts before you hire a pro, use the Tax Residency Tracker.

Scenario picks for globally mobile freelancers and consultants#

For globally mobile work, scenario routing is often more useful than title-based hiring. Cross-border filing issues, state and federal notice overlap, and potential non-disclosure risk can each point to a different first move.

| Scenario | First lead | Why this fits | What to verify before you hire |

|---|---|---|---|

| Foreign account and asset reporting cleanup with no active dispute | Credentialed preparer (EA, CPA, or attorney) with cross-border experience | The work is often filing accuracy, records, and reporting workflow | Use the IRS Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, and confirm they regularly handle Form 8938 cases |

| State tax notice plus IRS correspondence | One lead professional | A single owner helps keep facts, deadlines, and responses aligned across both notice streams | Confirm who owns the master notice tracker, response dates, and shared document set |

| Prior non-disclosure, possible willfulness, or enforcement-oriented language | Tax Attorney as an initial triage option | Early decisions may depend on legal-risk framing, not only return mechanics | Ask for a written next-step recommendation after document review |

| Messy books plus notice response | Split work into preparation lane and defense or strategy lane | Cleanup and controversy work often require different pacing and decision ownership | Define who owns return reconstruction and who owns agency-facing strategy before work starts |

Cross-border filing hygiene#

If your main problem is foreign reporting cleanup, a credentialed preparer with real cross-border experience is often the practical first step. The IRS lists preparers including CPAs, enrolled agents, and attorneys, and notes that preparers differ in skills, education, and expertise. The IRS also says Form 8938 is used to report specified foreign financial assets, is attached to your annual return, and is filed by that return's due date, including extensions. Form 8938 does not replace FinCEN Form 114 (FBAR) when FBAR is otherwise required.

A practical competence check is to ask how they evaluate thresholds, account types, ownership, and timelines up front. The IRS notes certain U.S. taxpayers file Form 8938 when aggregate specified foreign financial assets exceed $50,000, and foreign financial accounts can be part of that analysis.

State and federal notices in the same case#

When state and federal notices are both open, coordination is the first control. Pick one lead, keep one fact set, and use one deadline tracker so responses do not drift.

Before engagement, provide both notice streams, prior returns, and a short timeline of filed, missed, and open items. That keeps responses consistent from the start.

When legal-risk signals change the first call#

If facts include prior non-disclosure, possible willfulness, or enforcement-oriented language, consider starting with a Tax Attorney for triage. This is a first-step routing decision, not a claim that a lawyer must own the case forever.

Set a narrow first scope: document review, risk assessment, and a written recommendation on next steps.

Split cleanup from defense on purpose#

If your case combines bookkeeping reconstruction and controversy handling, split roles deliberately. Use a tax specialist for return reconstruction and filing support, and assign defense or strategy ownership separately when legal-risk decisions are in play.

Keep one shared evidence pack from day one: prior returns, notices, account summaries, and any Form 8938 history or gaps. For a step-by-step walkthrough, see A Guide to US Tax Court for Freelancers.

The document checklist to prepare before first consult#

A strong first consult depends more on your packet than your backstory. Bring a decision-ready file so your advisor can assess risk and next steps instead of rebuilding basic facts in the meeting.

| Packet piece | What to include | Why it matters | Check before you send |

|---|---|---|---|

| Filing history | Prior returns for the years in question, plus any amendments already filed | Shows what position was filed | Match tax years to the years mentioned in your IRS notices |

| Notice set | Every Internal Revenue Service (IRS) notice you have, plus any open IRS audit or IRS appeals correspondence | Notices often carry deadlines, issue framing, and document requests | Include every page, especially deadline and response pages |

| Cross-border records | FBAR filings (or clear gaps), Form 8938 history, and foreign account summaries | Helps your advisor check reporting consistency across years and forms | Tie each account to year, owner, and account status |

| Account-value and asset-change summary | Year-linked account max values, plus whether foreign assets were acquired or sold during each year | Form 8938 asks for maximum account values and whether assets were acquired or sold | Flag unknowns clearly instead of guessing |

| Working papers | A one-page timeline (what happened, when, who responded, next deadline) and a facts vs assumptions sheet | Can keep first-call triage focused on evidence and open questions | Separate confirmed facts from uncertain items in plain language |

For cross-border cleanup, flag one failure mode early. Filing Form 8938 does not replace FBAR obligations. If Form 8938 is required, attach it to your annual return and file by that return's due date, including extensions.

If you are unsure whether Form 8938 applied for a year, mark it as an open question. The IRS notes that if no income tax return is required for the year, Form 8938 is not required. Threshold analysis can also turn on aggregate value, with $50,000 as a baseline figure in some contexts.

One final checkpoint before you hire: do not assume every preparer can handle every IRS phase. EAs, CPAs, and attorneys have unlimited representation rights before the IRS, including audits, collection or payment issues, and appeals, while limited-rights preparers cannot represent clients in appeals or collection matters.

Escalate to a Tax Attorney when these triggers appear#

Escalate when legal risk starts driving the result. IRS contact by itself is not the trigger, because EAs, CPAs, and attorneys can all handle audits, collection or payment matters, and appeals before the IRS.

| Trigger | Why it changes the hire decision | What to do now |

|---|---|---|

| Your matter moves from routine IRS handling to legal interpretation of transaction treatment | The case shifts from filing execution to legal-risk management | Bring in a Tax Attorney before your written position hardens |

| Your strategy depends on privilege | This research set ties attorney-client privilege to attorney engagement for confidential strategy discussions | Route sensitive fact development and strategy through the attorney first |

| Facts are contested or documentation is incomplete | Incomplete submissions can escalate the examination, and outcomes can turn on legal characterization and how facts are framed | Stop casual explanations and build an evidence-backed response with counsel |

| Your current advisor is strong on filings but avoids legal-position analysis | You have reached their practical boundary | Keep them on compliance execution, but shift lead strategy to a Tax Attorney |

If an audit notice identifies specific years and items under review, including notices such as Form 556-B, treat that as a serious checkpoint. If the discussion shifts from document production to interpretive treatment of transactions, escalate.

Privilege and execution details matter here. If your representative needs to communicate directly with the IRS, confirm Form 2848 is signed and in place. Without it, IRS recognition of representative authority can fail and cost you time. Timing matters too. The source material for this guide notes a typical audit response window of about 30 days, extensions may be possible, and late or incomplete responses can escalate the examination.

The practical default is simple. If the issue may leave routine IRS administration, if privilege is part of your plan, or if legal interpretation is carrying the outcome, add a Tax Attorney immediately and keep your CPA or EA focused on filings and documentation.

Tradeoffs and hidden costs most articles skip#

The lowest quote is not always the best fit. Scope fit and representation coverage often matter more than headline price once handoffs and rework enter the picture.

A common mistake is treating all tax help as interchangeable. Any professional with a PTIN can prepare a federal return, but not every preparer has the same representation rights before the IRS. Some preparers have limited representation rights and cannot handle appeals or collection issues, even if they prepared the return. If your matter is in an audit, collection or payment issue, or appeal, verify that you are hiring an EA, CPA, or attorney with unlimited representation rights.

| Shortcut | Hidden cost | What to verify first |

|---|---|---|

| Picking the lowest quoted fee | The quoted scope may exclude the support you actually need if the issue escalates | Ask what deliverables are included and whether the professional has unlimited representation rights |

| Hiring a familiar return preparer for a live dispute | You may need a handoff if the matter moves into appeals or collection, which can duplicate fact-gathering | Confirm your current lane: return prep, audit, collection or payment issue, or appeal |

| Hiring two professionals without clear boundaries | Overlapping roles can create rework during IRS follow-up | Assign ownership in writing for filing cleanup, IRS contact, and legal strategy |

Wrong-role hiring can force a midstream handoff. If an engagement starts with limited representation rights and the matter moves into appeals or collection, another representative may need to step in.

A team can still be the right choice when scope boundaries are explicit. Before work starts, define the current IRS lane, the next deadline, and who owns communications, filings, and strategy.

Common failure modes and how to avoid them#

Most avoidable mistakes come from mixing separate filing obligations or missing document checkpoints. Keep one deadline tracker and a year-labeled document pack before filing.

| Failure mode | Check | Key detail |

|---|---|---|

| Define the filing obligation before you file | Confirm specified-person status, the applicable reporting threshold, and whether an income tax return is required for the year | If no income tax return is required for that year, Form 8938 is not required |

| Keep Form 8938 and FBAR in separate lanes | Do not treat Form 8938 and FBAR as interchangeable | Filing Form 8938 does not relieve a required FBAR filing |

| Show up with a document set, not just a story | Bring year-by-year Form 8938 and FBAR records | Form 8938 should be attached to the annual return and filed by that return's due date, including extensions |

| Check filing conditions before assuming a gap | Confirm filing conditions before deciding there is a gap to fix | For certain specified domestic entities, the stated threshold is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year |

1) Define the filing obligation before you file#

Start by confirming whether Form 8938 filing conditions are met for that year:

- You are a specified person (a specified individual or a specified domestic entity).

- The total value of specified foreign financial assets is above the applicable reporting threshold.

- If no income tax return is required for that year,

Form 8938is not required.

2) Keep Form 8938 and FBAR in separate lanes#

Do not treat Form 8938 and FBAR as interchangeable. Filing Form 8938 does not relieve a required FBAR filing.

3) Show up with a document set, not just a story#

Bring year-by-year Form 8938 and FBAR records. For Form 8938, check these points before filing:

- It is attached to the annual return and filed by that return's due date, including extensions.

- The applicable calendar year or tax year is clearly identified.

- You checked whether any foreign deposit or custodial accounts were closed during the tax year.

4) Check filing conditions before assuming a gap#

Confirm filing conditions first, then decide whether there is actually a gap to fix.

Form 8938is required only when filing conditions are met, including specified-person status and applicable threshold tests.- For certain specified domestic entities, the stated threshold is more than

$50,000on the last day of the tax year or more than$75,000at any time during the tax year. - Some financial accounts are excluded from

Form 8938, so "report everything" is not a safe default.

Use these checkpoints against each tax year and return due date to catch preventable errors early.

How to run a two-professional setup without chaos#

A two-professional setup works best when one person leads and the other stays in a clearly defined specialist role. Without that split, overlap and fact drift are more likely.

Split the work by lane, not by title#

Title alone should not decide day-to-day ownership. EAs, CPAs, and attorneys all have unlimited IRS representation rights for audits, payment or collection issues, and appeals, so the lead should usually be the person closest to the facts and the file. If either person has limited representation rights, do not assign IRS appeals or IRS collections to that lane.

| Workstream | Lead owner | Specialist role | Checkpoint |

|---|---|---|---|

| Return prep, backlog cleanup, IRS notice responses | EA or CPA | Attorney reviews if legal exposure appears | Match tax-year labels across returns, notices, and support |

| IRS appeals or IRS collections | EA or CPA if already managing the admin file | Attorney advises on legal position and escalation risk | Tag each item as IRS appeals or IRS collections with one owner |

| California FTB residency or sourcing notices | EA or CPA | Attorney reviews contested legal arguments | Confirm Form 540NR and any workday-allocation support are in the file |

Run one shared case file#

Breakdowns often come from stale or split facts. Keep one shared evidence folder, one deadline list, and one issue timeline with issuing authority, tax year, due date, and owner.

For California items, keep the file fact-heavy, not narrative-heavy. Residency is facts and circumstances, and part-year or nonresident workflows can require Form 540NR plus workday-allocation support. If that packet is incomplete, the handoff is not ready.

Use a short recurring handoff note with explicit owner tags for federal and state items. Any item tagged California FTB, IRS appeals, or IRS collections should show exactly one lead and one reviewer.

Conclusion#

Pick by case type and escalation risk, not by title alone. In cpa vs enrolled agent vs tax attorney, the safer default is to match the professional to the work in front of you, then escalate quickly if the scope shifts.

If your matter is still routine, optimize for scope fit and clear ownership. If legal-risk questions start driving decisions, treat that as an early escalation signal and confirm ownership before scope expands.

For IRS-facing work, use one practical checkpoint in the first consult. Ask how they will verify the statute of limitations, review available IDRS data, define the examination scope, and handle representative authority when needed. IRS pre-audit workflow places these checks before taxpayer contact and explicitly includes Power of Attorney handling, Form 2848, Form 8821, and availability of books and records.

Document readiness is the next filter. Bring a usable packet with the records tied to the years at issue, and ask directly whether Form 2848 or Form 8821 is appropriate and how it will be processed. That question quickly shows whether you are getting case handling or generic commentary.

Do these three things this week:

- Classify your issue: routine handling now, or likely escalation risk.

- Build your consult packet: books and records for the years at issue, plus the key notices and correspondence you already have. Ask about Form 2848 and Form 8821 if representation may be needed.

- Book the first consult with the scope-matched professional and confirm in writing what they will own first.

If you manage cross-border income flows, keep tax records and exportable history organized in one place where supported. Gruv can support that operating model for supported use cases, but the core principle is tool-agnostic: audit-ready records should be easy to retrieve, share, and defend.

If you want one audit-ready workflow for cross-border invoicing, payouts, and records where supported, contact Gruv.

Frequently Asked Questions

Who can represent me before the IRS in an audit or appeal?

For IRS administrative matters, the answer is clear: Enrolled Agents, CPAs, and attorneys have unlimited representation rights before the IRS. The IRS says these credentials can represent clients in audits, payment or collection issues, and appeals. Confirm you are hiring one of those three, because some PTIN preparers have limited rights and cannot represent clients in appeals or collection matters.

Who can represent me in Tax Court?

The sources for this guide do not establish who can represent a taxpayer in U.S. Tax Court. Do not assume IRS representation rights automatically carry into court. If your matter may move to Tax Court, verify representation authority directly before engagement.

When should I escalate from a CPA or EA to a tax attorney?

A cautious approach is to treat scope changes as a signal: if the work is no longer mainly return prep, notice response, or IRS administrative handling, consider adding a tax attorney for legal-position questions and possible court escalation. If there is uncertainty, define roles early and confirm scope in writing.

Is an Enrolled Agent always cheaper than a CPA or tax attorney?

No supported source here says an EA is always cheaper than a CPA or tax attorney. Fees can vary by scope, urgency, and file complexity, so broad price claims are unreliable. Compare proposals by scope and ownership, not by credential label alone.

Can I hire both an EA/CPA and a tax attorney on the same case?

A practical split can be EA or CPA for prep, cleanup, and IRS administrative work, with a tax attorney focused on legal-position and escalation-risk questions. Keep one shared evidence folder, one deadline list, and one lead owner per tagged item, such as IRS appeals, IRS collections, or California FTB, to avoid handoff errors.

What should I bring to the first consultation for an IRS or state tax issue?

A practical starter packet can include prior returns, IRS or state notices, current correspondence, and a one-page timeline with tax year, issuing authority, due date, and filing status. For California residency or sourcing matters, include any Form 540NR filings or drafts and your workday support, since residency is facts and circumstances and sourcing may use CA Workdays / Total Workdays = % Ratio.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ardot.gov/wp-content/uploads/040901_proposal_prelimina...trusted

- digitalcommons.law.uw.edu/cgi/viewcontent.cgitrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/forms/misc/1100.htmltrusted

- irs.gov/tax-professionals/understanding-tax-return-p...trusted

- irs.gov/forms-pubs/about-form-8938trusted

- lawfilesext.leg.wa.gov/law/wsr/2003/01/03-01.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level

**Pick the support level that matches your compliance surface area, then evaluate providers on written scope and form coverage.** The common failure mode for most U.S. expats is not "forgetting to file." It is hiring the wrong help model, under-scoping what you actually need, and finding the gap when IRS filings and related reporting obligations hit the critical path. You run a business-of-one, and your tax workflow is part of the system.

What is an Enrolled Agent (EA) and When Should You Hire One?

If you have cross-border income and still file with the IRS, an Enrolled Agent, or EA, can be a practical first partner for federal tax compliance and IRS-facing issues. U.S. citizens and resident aliens are [taxed on worldwide income](https://www.irs.gov/individuals/international-taxpayers/us-citizens-and-resident-aliens-abroad), so earning abroad does not remove IRS obligations.