Quick Answer

Start by treating costa rica tax residency as a two-part classification, not a day-count shortcut. Article 5 of the Costa Rican Income Tax Law Regulations and Article 2 of Administrative Regulation DGT-R-033-12 are core anchors for deciding likely resident versus non-resident treatment. Build one fiscal-year file with your timeline, income-source mapping, and supporting records before filing. If your documents still support conflicting conclusions, stop and get written local advice.

Start Here if You Want a Defensible Costa Rica Tax Position#

A six-month day-count threshold is a useful starting filter, not the full test. A defensible position depends on both time in country and Costa Rica-source income, using definitions tied to Article 5 of the Costa Rican Income Tax Law Regulations and Article 2 of Administrative Regulation DGT-R-033-12.

For foreign individuals, the baseline is at least six months in Costa Rica plus Costa Rica-source income during the fiscal year. Costa Rican individuals with Costa Rica-source income can be treated as tax residents whether or not they lived in the country during that same year. If those requirements are not met, treatment is non-tax resident.

Use this guide to classify your likely status, assemble proof for one fiscal period, and spot when to escalate for written advice before filing.

Start with this quick classification pass:

- Check your day count, but treat it as one input.

- Map each main income stream to source treatment.

- Apply the legal fork: likely resident if the criteria are met, likely non-resident if they are not.

- Write a dated memo for that tax year with the legal references you relied on.

If you do only one thing now, create one fiscal-year file and put every residency note, timeline record, and income-source document in that folder. That single habit helps avoid a common failure mode: deciding status first, then trying to rebuild evidence later from scattered records.

Success here is practical: fewer assumptions, cleaner records, and a position you can explain clearly to the Tax Administration of Costa Rica.

Define the Terms Before You Make Any Decision#

Separate immigration status from tax status before you decide anything else. They are related in practice, but they are not interchangeable for classification.

Under the cited rules, foreign individuals are treated as tax residents when they have continuously lived in, or spent at least six months in, Costa Rica and received Costa Rica-source income in that fiscal year. The same legal references state that Costa Rican individuals with Costa Rica-source income can be treated as residents whether or not they lived in the country during that year. If those requirements are not met, treatment is non-tax resident.

| Term | Use it for | Do not use it for |

|---|---|---|

| Immigration status | Keeping immigration records separate from tax classification | Proving tax residency by itself |

| Tax residency | Applying the cited tax criteria to fiscal-year facts | Proving immigration status |

| Non-tax resident status | Classification when cited resident requirements are not met | Assuming your records no longer matter |

| Tax Residence Certificate | Documentation issued through the tax authority process | Overriding conflicting facts on its own |

A Costa Rica digital nomad visa does not automatically settle tax status. Treat a Tax Residence Certificate the same way: it should match the same fiscal-year presence and income facts, not work as a shortcut around conflicting records.

A practical red flag is language drift inside your own notes. If one note says "resident because of visa" and another says "resident because of source income," your decision basis is already unstable. Pick one legal basis for each conclusion and make sure every document in the file supports that same basis.

Quick checkpoint before you label status:

- Confirm the fiscal year.

- Match presence records to that year.

- Match each income stream to source treatment for that year.

- If you have a certificate, confirm it matches the same dates and facts.

For a quick next step, run your dates through the tax residency day counter and keep the result in your fiscal-year file.

Reconcile the Two Tests People Quote Most#

Do not merge the shorthand and article references into one rule until you verify the primary legal text. The 183-day shorthand and the article references cannot yet be fully reconciled.

That distinction matters. Secondary summaries can help frame questions, but they are not enough to lock a filing position on their own. The current pack does not include the primary Costa Rica residency-law text needed to confirm how the cited article references should be applied.

| Item people cite | Useful now | Not enough yet |

|---|---|---|

| 183-day summaries | Signal that day count may matter and should be tested | Do not prove legal treatment by themselves |

| Article references in secondary summaries | Identify which primary provisions must be reviewed | Do not confirm legal effect without the text |

| Additional article mentions in commentary | Flag counting logic to verify | Do not settle counting disputes without primary language |

Use one control rule: if a claim depends on a cited article and you cannot show the primary text you relied on, mark it unverified. Do not treat it as final.

It also helps to assign a confidence label to each conclusion in your memo. Mark conclusions as confirmed only when they are backed by primary text and matching facts. Mark everything else as provisional. This keeps your filing posture honest and makes escalation faster when conflicts appear.

Run this checkpoint before final classification:

- Label each rule in your notes as primary law text, secondary summary, or non-authoritative context.

- Require primary-language support before treating cited article references as decisive.

- If 183-day shorthand and article-based interpretation point in different directions, pause and escalate for written advice.

- Keep unresolved items in the same fiscal-year file so your final position and evidence stay aligned.

Count Days the Way the Tax Authority Can Defend#

Build a dated ledger first, then classify each period with documents. Rough calendar estimates are not enough when dates are disputed.

| Ledger item | What to record | Handling note |

|---|---|---|

| Presence dates | Entry date, exit date, and total nights in Costa Rica | Start with a dated ledger, not a rough calendar estimate |

| Movement evidence | Passport stamps, tickets, and lodging records for each movement | Use documents for each movement rather than memory |

| Gaps | Each gap as a short absence or longer break | Note what supports the classification |

| Status by period | Visa status, including tourist or digital nomad status | Keep immigration and tax tracking in separate columns |

| Income by period | Income-source activity during each period | Add a note for the same period |

| Uncertain dates | Any date you cannot verify | Flag it immediately instead of fixing it later |

Keep immigration and tax tracking in one file, but in separate columns. The systems are separate, so use the 90-day tourist limit and the often-quoted 183-day threshold as review triggers, not automatic conclusions.

If you use a day-count method from secondary summaries, treat it as a working approach, not confirmed legal text. Classify periods consistently, and record every assumption.

- Record each entry date, exit date, and total nights in Costa Rica.

- Keep passport stamps, tickets, and lodging records for each movement.

- Mark each gap as a short absence or longer break, with supporting records.

- Tie each period to visa status, including tourist or digital nomad status.

- Add a note on income-source activity during each period.

- Flag uncertain dates immediately instead of fixing them later.

Do not collapse brief exits and re-entries into one clean block just to simplify the file. Keep each movement visible and test whether your classification still holds under different assumptions.

A useful operational habit is a monthly close of your day ledger. Reconcile the month while records are fresh, then lock that month unless new evidence appears. This reduces year-end reconstruction errors and gives you an audit trail of what changed and why.

If you claim residence elsewhere in the same fiscal year, pair that claim with matching travel and status records for the same period. Treat any single document as supporting context, not a fix for contradictions in dates or income records.

Use one checkpoint before filing: can a reviewer reproduce your count from documents alone, without memory-based explanations? If not, treat status as disputed and get written professional review before taking a filing position.

After you lock your ledger method, use it consistently for the full year so your file stays coherent. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

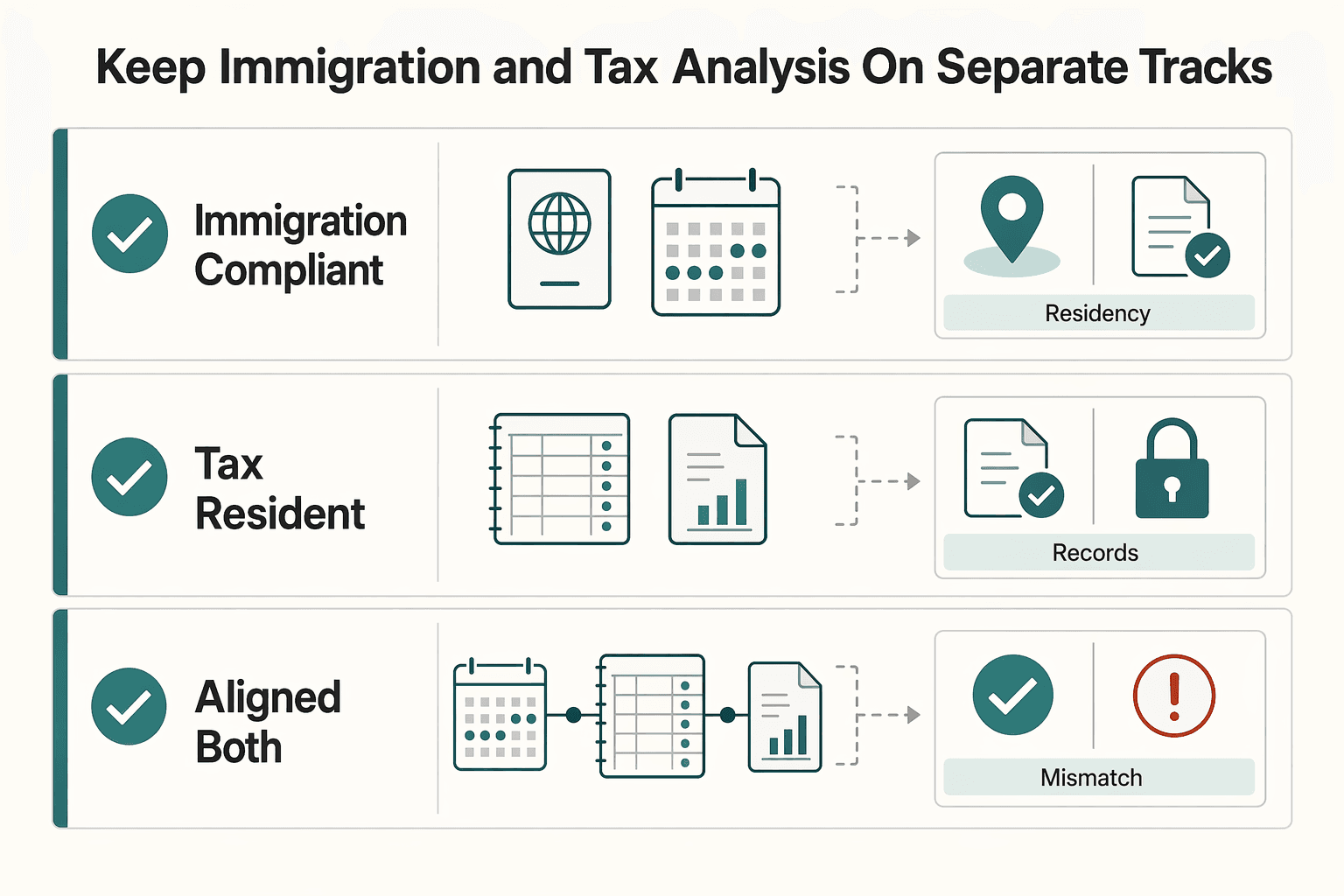

Keep Immigration and Tax Analysis on Separate Tracks#

Do not treat immigration approval as proof of tax classification. Keep immigration status and tax status as separate decisions until the same fiscal-year records support both.

Use your day ledger as a shared timeline, then test tax status with matching tax records for that same period. If travel dates are clean but tax evidence is weak or conflicting, treat the tax position as uncertain even if your stay is compliant.

This mismatch can occur when people rely on remote-worker permission. A 2021 EY alert described a proposed non-resident immigration category that could allow up to one year in Costa Rica for work with non-Costa Rica clients. It also said the bill was under review at that time. Use that type of approval to document stay rights, not to conclude tax status.

Apply the same separation to property-based residency narratives. Public summaries may cite a $150,000 investment path, 2 years of temporary status, and possible permanent residency after 3 consecutive years. Those points are immigration context, not stand-alone tax proof.

Keep transaction-specific tax rules in scope too. One Costa Rican resolution describes a 2.5% capital-gains withholding process for non-resident real-estate sales using Form 129 through TRIBU-CR. That shows a narrow non-resident tax procedure can apply even while broader residency classification is still being evaluated.

| Outcome | Immigration track | Tax track | Required action |

|---|---|---|---|

| Immigration-compliant, tax-uncertain | Permission to stay is documented | Tax evidence is incomplete or conflicting | Mark tax status provisional and complete the tax file before filing |

| Tax-resident view, immigration-expiring | Stay rights are near expiry | Tax facts support resident treatment | Renew or change immigration status while preserving tax documentation |

| Aligned on both tracks | Stay rights and dates are consistent | Tax evidence supports the same fiscal-year result | Finalize your annual memo and retain supporting records |

Before filing, confirm these in writing:

- Immigration status type and validity dates.

- Day ledger and tax records covering the same fiscal period.

- Income-source records matching the filing position.

- Any visa or permit approval language marked clearly as not being tax proof by itself.

- Written professional review if the two tracks still point to different outcomes.

One practical sequence helps: finalize immigration dates first, close the day ledger second, and lock tax classification last. Reversing that order can create rework when late travel evidence changes the timeline.

Account for Individual, Spouse, and Entity Exposure#

Split this analysis into three lanes: individual, spouse, and entity. Then make sure those lanes stay consistent for the same fiscal year.

Start with your individual file, then run the same review for your spouse rather than assuming one profile covers both. Under CRS, financial institutions assess tax residency at the customer level. They usually do this where that person or entity is liable for income or corporate tax, so mismatches can surface even when finances are shared.

If you invoice through a company, review entity exposure in parallel with your personal file and anchor legal interpretation to applicable local rules and professional advice. Keep personal income and entity income streams clearly separated before any filing or declaration.

| Exposure lane | Core question | Minimum evidence to review now | Red flag |

|---|---|---|---|

| Individual | Which amounts are personal income under your filing position? | Day ledger, signed contracts, invoice copies, personal account inflows | Personal return position conflicts with bank tax-residence self-certification |

| Spouse | Do spouse records point to the same or a different outcome? | Separate travel log, spouse contracts or income records, spouse account self-certs | One spouse file reuses the other spouse dates without matching records |

| Entity | How are company revenues sourced and classified versus owner income? | Incorporation documents, invoices by legal entity name, client location map, payout trail | Entity declarations and owner filings describe the same revenue with opposing source treatment |

Do one pre-filing consistency check across all three lanes:

- Compare tax-residence self-certifications used with each financial institution for each person and entity.

- Assign each major income stream to either personal or entity treatment, not both.

- Confirm certificate requests and return positions rely on the same fiscal-year facts.

- If individual and entity conclusions diverge, pause and get a written cross-file opinion before filing.

A useful check at this stage is a one-page reconciliation sheet listing each major income stream and its owner. If two lanes claim the same income stream, resolve it before filing. This catches duplicate or conflicting treatment early, when fixes are still manageable.

This step takes longer upfront, but contradictions are easier to catch now than after submission and much harder to unwind once records are filed.

Build the Evidence Pack Before You Need to Defend It#

Build your evidence pack before filing season and tie every conclusion to documents from the same fiscal year. The strongest position is the one you can reconstruct quickly if a bank, advisor, or tax reviewer asks questions.

Use a practical annual pack: travel logs, signed contracts, invoices, bank records, and any Tax Residence Certificate for that same period. Treat this as a defense set, not a statutory checklist.

Keep your legal anchors attached to the memo: Costa Rican Income Tax Law Regulations Article 5 and Administrative Regulation DGT-R-033-12 Article 2 (November 14, 2012). For individuals, the OECD summary indicates foreign individuals may be treated as tax residents when they have continuously lived or spent at least six months in Costa Rica and receive Costa Rican-source income. For entity exposure, note that the OECD summary describes legally incorporated Costa Rican entities and irregular entities receiving Costa Rican-source income during the fiscal year as potentially resident.

Write a dated decision memo for the year with your classification and why: facts used, provisions referenced, and unresolved points. State clearly whether the file supports resident treatment or non-resident treatment.

Before any filing or certificate request, run one verification pass:

- Confirm every document is tagged to the same fiscal period.

- Tie each income stream to personal or entity treatment, not both.

- Check that certificate-request facts match memo facts.

- Flag any gap where related records point to different outcomes.

One point to take seriously: the OECD summary says Costa Rican regulations do not provide a single explicit provision stating where a person or entity would not be considered tax resident. If your file still conflicts after this pass, escalate early for a written opinion and record the listed competent authority contact point, the General Director of the Tax Administration.

Document control matters here. Save the memo version used for filing and keep it alongside the exact supporting files that were available on that date. If later evidence appears, create a new version with a clear change note instead of editing old reasoning in place.

If you use Gruv where enabled, export invoice, payout, and ledger records into the same annual folder so your income narrative stays consistent and traceable.

Use Scenario Rules Instead of Generic Advice#

Use scenario rules when facts are mixed or your legal read is unsettled. Generic advice is often where avoidable filing errors begin.

| Scenario | Action | Timing |

|---|---|---|

| Facts are close to your decision boundary and your income-source story is mixed | Treat the file as high risk and tighten documentation | before you proceed |

| Your day-count narrative looks clean but source-of-income treatment is unclear | Reconcile your position against the legal text you actually rely on, not blog shorthand | before any tax-residency representation |

| Your conclusion depends on residency claims in another country | Secure that supporting evidence first and keep your Costa Rica position provisional | until the file is complete |

| Documents conflict | Stop and resolve the conflict in writing | before submitting anything |

Apply this rule set before any tax-residency representation:

- If your facts are close to your decision boundary and your income-source story is mixed, treat the file as high risk and tighten documentation before you proceed.

- If your day-count narrative looks clean but source-of-income treatment is unclear, reconcile your position against the legal text you actually rely on, not blog shorthand.

- If your conclusion depends on residency claims in another country, secure that supporting evidence first and keep your Costa Rica position provisional until the file is complete.

- If documents conflict, stop and resolve the conflict in writing before submitting anything.

This approach is slower upfront, but it helps prevent contradictions later. Cross-border digital work can span countries without significant physical presence. Source and residency conclusions can drift unless you force one written position tied to one period and one document set.

Keep the reconciliation note short and explicit: which text controlled, which facts decided the outcome, and what is still uncertain. If uncertainty is still material, escalate before filing. That caution matters in a context where public analysis has described Costa Rica as subject to debate and contradictory conclusions.

Treat information exchange and offshore-compliance scrutiny as real considerations in cross-border matters. You do not need to predict enforcement intensity. You need a coherent file that stays consistent across returns, account records, and supporting documents.

When you are unsure how strict to be, choose the version of your position that can survive a document-by-document review by someone who has never spoken with you. That standard avoids overconfident narratives built on memory.

Final guardrail: tax avoidance is legal tax reduction, while tax evasion is illegal tax reduction, and the line is not always clear. If your case is close, pause, close gaps, and get written review.

Know When to Escalate and What to Ask a Professional#

Escalate when your file supports more than one plausible outcome for the same fiscal year. If your legal read is unsettled or your records point in different directions, stop and get written advice before you file.

Use escalation triggers like these:

- Your memo relies on legal provisions that seem to conflict in your case.

- Personal, business, and bank records do not support one consistent story.

- Key facts are still uncertain, especially when more than one country is involved.

When you escalate, ask for a written opinion tied to your document pack, not verbal guidance. Ask the professional to state:

- Which facts were accepted, rejected, or treated as uncertain.

- Which legal text controlled the conclusion and why.

- What is still uncertain and what would change the outcome.

- What must be fixed before filing if conflicts remain.

Give the reviewer a clean packet so the answer is useful on the first pass: your day ledger, income-source mapping, current memo, and a short list of open conflicts. A vague request can lead to a vague reply and extra rework.

This is a risk-control step, not overkill. OECD reporting cites some estimates that tax evasion losses in Latin America amount to 6.1% of regional GDP. It also notes that four Latin American countries joined forces in November 2018 to address revenue collection and tax evasion challenges.

Final guardrail: tax avoidance is a legal reduction of taxes, while tax evasion is an illegal reduction of taxes. If material conflicts remain after review, pause filing, close the gaps, and then proceed with one coherent position.

Execute a 30-Day Compliance Checklist#

Use this practical 30-day checklist to finalize one defensible position. This timeline is a workflow tool, not a legal requirement. Your classification, records, and legal references should all support the same conclusion before filing.

| Week | Main task | Week-end output |

|---|---|---|

| Week 1 | lock terms and a preliminary classification | a drafted classification note |

| Week 2 | complete your day-count file and income-source evidence | a reconciled ledger |

| Week 3 | test for contradictions before submission | a contradiction log |

| Week 4 | get written sign-off where needed and freeze your annual memo | a signed final memo |

-

Week 1: lock terms and a preliminary classification. Define your working meaning of tax resident, non-tax resident, and Costa Rican-source income, then assign a provisional status. Keep your legal anchors visible from day one: Costa Rican Income Tax Law Regulations Article 5 and Administrative Regulation DGT-R-033-12 Article 2, dated November 14, 2012. Add a short reason for each condition you mark as met or not met.

-

Week 2: complete your day-count file and income-source evidence. Build a dated fiscal-year ledger with travel records for each counted period. In the same file set, match contracts, invoices, and bank records so income source is documented. If relevant, check Tax Residence Certificate issuance requirements and save the status in your records.

-

Week 3: test for contradictions before submission. Check your facts against the criteria line by line, including the six-month presence condition for foreign individuals together with Costa Rican-source income. Then test mismatch scenarios, such as day count and income evidence pointing to different outcomes, or individual and entity records pointing in different directions. If more than one plausible outcome remains, escalate before filing.

-

Week 4: get written sign-off where needed and freeze your annual memo. Request written conclusions tied to your document pack, including accepted, rejected, and uncertain facts. Finalize a memo that states your classification, controlling legal references, unresolved risks, and what would change the outcome. Lock the final record set with a date stamp, including travel log, income-source documents, Tax Residence Certificate status, and final memo version.

Treat each week as a deliverable checkpoint, not just a reminder. End each week with one output you can point to: a drafted classification note, a reconciled ledger, a contradiction log, or a signed final memo.

If a week slips, do not skip the missed task and continue. Move the timeline and complete the missing checkpoint first. Incomplete steps compound quickly in this process.

The Bottom Line for Pura Vida Nomads#

Given the evidence summarized here, treat your position as a documentation exercise, not a slogan about days present. Your position is strongest when records, assumptions, and your final narrative point to one consistent conclusion.

If you use a day-count shortcut to screen facts, do not let it replace a complete file. The practical risk is false confidence: if your documents support more than one story, you may be exposed.

Regional context supports this conservative approach. OECD reporting describes materially high tax-evasion losses in Latin America and calls for stronger cooperation so exchanged information is used more fully. That does not determine your status, but it is a practical reminder that weak records can create avoidable risk.

Before filing, do one written consistency pass:

- Confirm your timeline and income narrative do not conflict across documents.

- Flag assumptions that could change your classification.

- Separate verified facts from open questions and missing evidence.

- Set a stop rule: if one unresolved fact could flip the outcome, pause and escalate early.

After filing, keep the same discipline for the next cycle. Archive the memo, keep the evidence pack intact, and note any facts that changed during the year so next year starts from a clean baseline instead of a reconstruction exercise.

When clarity and speed conflict, choose clarity. File only when your record supports one coherent position. For cost-of-living context, see The Best Digital Nomad Cities for Affordable Living.

Frequently Asked Questions

Is Costa Rica tax residency based only on the 183-Day Rule?

No. A presence test over 183 days is one listed criterion, but the Article 5 summary used in this context also includes other taxpayer categories. That includes categories beyond individuals, such as Costa Rican legal entities and de facto companies.

Does legal residency or another immigration status automatically make me a tax resident?

No. Physical or legal residency is an immigration status, not an automatic tax classification on its own. Public summaries also state that spending more than 183 days can trigger tax residency regardless of immigration status, so keep immigration status and tax analysis as separate checks.

How are arrivals, departures, and sporadic absences counted for residency analysis?

Public summaries do not fully define every counting edge case. The computation is regulated by the Tax Administration, so use one consistent method across the fiscal year and keep dated entry and exit records. If your conclusion changes depending on counting assumptions, treat that as uncertain and get written local advice before filing.

Can married couples file jointly for tax residence determination in Costa Rica?

Do not assume a joint determination rule from the material provided here. The public material summarized here does not establish a joint filing standard for this analysis. A safer approach is to assess each spouse separately until a local professional confirms otherwise for your facts.

What does a Tax Residence Certificate actually prove in a residency dispute?

A Tax Residence Certificate is a Tax Administration document that certifies tax-resident status for a specific fiscal period. It is used to support treaty-related interactions and responses to foreign tax authority requests. It supports your position, but it should not be treated as a substitute for consistent underlying records.

What is still uncertain in public summaries, and how should I handle that uncertainty safely?

The biggest risk is treating the 183-day shorthand as the full legal test. Another uncertainty is wording differences like 183 plus days in 12 months versus exceeding 183 days during the fiscal year. If that distinction could change your outcome, document your assumption and get written local confirmation before you file.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cpilj-law.media.uconn.edu/wp-content/uploads/sites/2515/2020/06/Offsho...trusted

- oecd.org/tax/automatic-exchange/crs-implementation-an...trusted

- state.gov/wp-content/uploads/2019/11/TIAS-19-708-Costa...trusted

- state.gov/reports/2023-investment-climate-statements/c...trusted

- globalwealthprotection.com/costa-rica-tax-residency-vs-physical-residen...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Best Digital Nomad Cities for Affordable Living

If you want a low-cost base that still feels affordable after you land, start with friction, not rent. Affordability can break down when work setup and logistics wobble at once. Your best first move is the city you can operate from with the fewest unknowns.

How to Create a Speaker One-Sheet for Your Freelance Business

If you run a business-of-one, you're not here for vibes; you're here for a repeatable system you can actually use.