Quick Answer

Start with a registration decision before your next billing cycle for canada gst hst for freelancers: confirm small-supplier status, classify services, and verify account readiness in My Business Account. Then apply client-location treatment before issuing final invoices, keep collected tax separate from business cash, and file on your assigned reporting period. If effective-date timing or service classification is uncertain, pause final sends and confirm with the Canada Revenue Agency or a qualified tax professional.

Start With Your GST/HST Status#

For globally mobile freelancers, GST/HST gets easier when you decide a few key points early: when registration is required, what to charge, which GST/HST treatment applies, how often to file, and when to escalate unclear facts.

GST is tax you collect from customers and remit to the Canada Revenue Agency (CRA). HST combines GST with provincial sales tax. Once registration is required, you must charge and collect tax on taxable supplies you make in Canada.

Rate treatment is not a single national setting. Place of supply determines whether a supply is made in Canada and which province drives GST/HST treatment.

Use this guide as a practical decision path you can apply before each invoice cycle:

- Registration: determine whether registration is required for your situation.

- Charging: confirm the service is a taxable supply made in Canada before finalizing invoices.

- Rate treatment: apply place-of-supply logic before selecting GST/HST treatment.

- Filing cadence: set a monthly, quarterly, or annual filing rhythm and manage remittance cash separately.

- Escalation: when facts are mixed, document assumptions and confirm with CRA or a qualified tax professional.

A quick anchor: if a $1,000 service is subject to 5% GST, the client pays $1,050. The GST portion is collected tax to remit, not business revenue.

The main operational risk is delay. Late registration, filing, or payment can lead to penalties or interest, so this article focuses on clear decisions now and documentation you can defend later.

If you keep one idea in view, make it this: treat each GST/HST decision as a record you may need to explain later. That mindset changes how you price, invoice, reconcile, and escalate. It also removes a lot of stress, because you are no longer relying on memory when a return is due or when a treatment call is questioned.

Define the terms that decide your obligations#

Treat these terms as decision controls, not just vocabulary. Define them first, and it becomes much easier to decide when to register, what to charge, which account to use, and when to file and remit.

Goods and Services Tax (GST) is the federal tax on most goods and services for domestic consumption. Harmonized Sales Tax (HST) combines GST with provincial sales taxes. GST is commonly described at 5%, while HST includes a provincial component.

A Business Number (BN) is your CRA business identifier with 9 digits. Your GST/HST number is the GST/HST program code attached to that BN. A BN alone is not the same as having a GST/HST program account.

| Term | What it changes in practice |

|---|---|

small supplier | This status is tied to the registration trigger. Once you surpass $30,000 over four consecutive calendar quarters and are no longer a small supplier, registration is generally required. |

taxable supplies | Registered businesses collect GST/HST at sale and remit it to CRA. |

zero-rated supplies and exempt supplies | This section flags these as separate terms, but does not define their full legal treatment. Confirm exact treatment in CRA guidance for your situation. |

reporting period and GST/HST return | Your reporting period sets your filing cadence, and returns follow that cadence: monthly, quarterly, or annually. |

These terms interact. Registration status affects whether you should be charging GST/HST, and your reporting period affects when you file and remit. When one term is unclear, later steps get harder and error risk rises quickly.

Before invoicing at scale, keep one checkpoint record. Include your current four-quarter sales total, when you crossed or expect to cross $30,000, BN status, GST/HST program account status, and assigned reporting period.

Use CRA guidance to orient your decisions, but keep one legal guardrail in mind: CRA publications are informational and do not replace the law. For edge cases, confirm directly with CRA or a qualified tax professional.

A practical habit is to store these definitions and your current status in one short internal note that you update monthly. You do not need a long memo. A single page with your current classification calls, account status, and next review date is enough to keep the next filing cycle predictable.

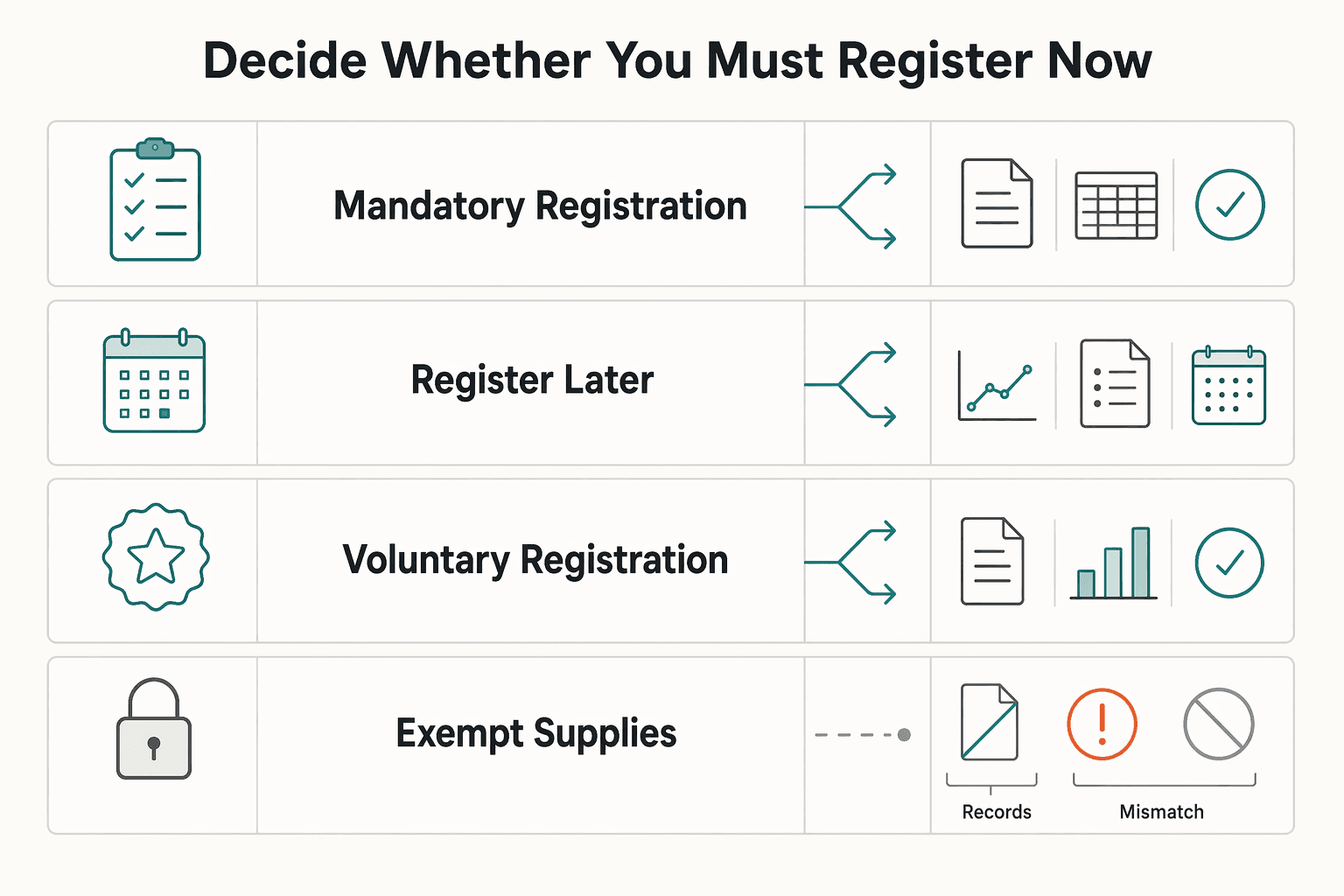

Decide whether you must register now, later, or voluntarily#

Make this call before your next invoice: mandatory now, later with monitoring, or voluntary.

| Scenario | When it applies | Key note |

|---|---|---|

| Mandatory registration now | You are not a small supplier and you make taxable sales, leases, or other supplies in Canada | Registration is required under CRA's two-condition test |

| Register later, but monitor closely | You are still a small supplier | Registration is generally not yet mandatory; a commonly cited marker is staying under $30,000 across four consecutive calendar quarters |

| Voluntary registration | You are still a small supplier and choose to register for business reasons | CRA says the effective date is usually the date of your request |

| Exempt supplies only | You provide only exempt supplies | You generally cannot register for a GST/HST account |

- Mandatory registration now: register if both CRA conditions apply: you are not a small supplier, and you make taxable sales, leases, or other supplies in Canada.

- Register later, but monitor closely: if you are still a small supplier, registration is generally not yet mandatory under CRA's two-condition test. A commonly cited marker is staying under $30,000 across four consecutive calendar quarters, but confirm your status against current CRA guidance before relying on that number.

- Voluntary registration: if you are still a small supplier, you can choose to register for business reasons. In that case, CRA says your effective date is usually the date of your request.

Apply one filter before you choose a branch: if you provide only exempt supplies, you generally cannot register for a GST/HST account. Classify your supplies first, then proceed.

The tradeoff is admin load versus timing control. Staying unregistered while still eligible as a small supplier can reduce admin now, but it can force a rushed setup once mandatory conditions are met. Voluntary registration starts your account earlier, which means handling account administration earlier as well.

Before issuing new invoices, run one verification checkpoint and save a dated note. Include your current small-supplier status, whether you make taxable supplies in Canada, your taxable versus exempt classification, and your registration status. If anything is unclear, pause and confirm your status with CRA guidance first.

One simple way to avoid drift is to set a monthly registration review date before invoicing close. Check the same fields every time, then sign off the result in writing. This is faster when your records are current and can reduce cleanup if your status changed mid-quarter.

If your facts are mixed, choose the lower-risk path for timing. Finalize status first, then issue invoices. Guessing under deadline pressure can create back-charging disputes, customer friction, and extra reconciliation work in the next return cycle.

Pin down the effective date so you do not back-charge yourself#

If registration timing is unclear, treat it as a billing risk and resolve it before sending more final invoices. Once you are a GST/HST registrant, you usually have to collect GST/HST on amounts charged for taxable supplies, so uncertainty can force invoice corrections later.

Late registration is a compliance risk, and delay plus assumptions can create avoidable billing cleanup. Use one control point so you are not fixing this after the fact.

Before you release invoices when timing is unclear, verify and document these points:

- Registration submission timestamp and confirmation details.

- The start date currently used in your books.

- Invoices issued during the uncertain period.

- Draft correction language if invoices need revision.

- A dated note of what is known, unknown, and who owns follow-up.

If facts are still messy, consider holding new final invoices as drafts until your account start-date record is confirmed. Keep category-specific rules in view too. CRA notes taxi and commercial ride-sharing fares usually include tax, and that treatment should not be copied into unrelated freelance services. If uncertainty remains after internal checks, consider contacting CRA or a qualified professional before the next invoice batch.

You can also reduce risk by ring-fencing the uncertain window. Tag every invoice created during that period in your books and keep them in one folder. If the effective date needs correction, you have a complete list ready for review. You can then update clients in a controlled sequence instead of searching line by line later.

When you do need corrections, consistency matters more than speed. Use one approved correction note format, apply it the same way across affected invoices, and keep both original and corrected versions together with date stamps. That record trail can make later filing support more straightforward. Related: Ho Chi Minh City, Vietnam: The Ultimate Digital Nomad Guide (2025).

Classify your services before you invoice any client#

Classify each service before you price or invoice it: taxable services, zero-rated services, or exempt services.

| Classification | What the article says | Common error noted |

|---|---|---|

| Taxable services | Services provided in Canada are generally taxable unless a specific exemption applies | Not charging tax when required is listed as a common misclassification error |

| Zero-rated services | Some services are zero-rated at 0% when required conditions are met | Applying the wrong treatment is listed as a common misclassification error |

| Exempt services | A separate category that should be identified deliberately | Charging tax on exempt services is listed as a common misclassification error |

Under the Excise Tax Act, services provided in Canada are generally taxable unless a specific exemption applies. Some services are zero-rated at 0% when required conditions are met, and exempt services are a separate category that should be identified deliberately.

Do not rely on generic advice that freelancers usually charge GST/HST when you have a varied service mix. Common misclassification errors include charging tax on exempt services, not charging tax when required, or applying the wrong treatment. These errors can lead to CRA reassessments, denied ITCs, and penalties.

Keep a service classification log for each offer type:

- Offer name and scope used in your proposal or statement of work.

- Chosen treatment: taxable, zero-rated, or exempt.

- Rationale for the treatment and conditions or exemption relied on.

- Decision date and reviewer.

- Recheck trigger such as scope change, delivery model change, or new client type.

Recheck classification whenever service facts change. CRA plain-language guidance is useful for orientation, but it is informational and does not replace the law.

A useful sequence is classify first, then price, then draft invoice lines. When this order is reversed, you may need to rewrite pricing terms after treatment is clarified. That can confuse clients and create avoidable negotiation about who absorbs tax differences.

Service bundles need extra care. If a package contains multiple deliverables, write the scope in a way that keeps the treatment rationale clear in your log. Clear scope language now makes rechecks faster when the engagement expands, and it gives you a clean explanation if treatment is reviewed later.

Apply place of supply rules for cross-border freelance work#

For cross-border freelance work, place of supply is the key GST/HST decision. It determines whether a supply is made in Canada, and the rate to charge follows that result. If registration is required, you must charge and collect GST/HST on taxable supplies made in Canada.

The same service can lead to different invoice treatment when client facts differ. Do not reuse a prior invoice decision without rechecking place of supply for the current client and engagement.

Channel can also change who has to charge tax. In some digital economy cases, obligations can differ for supplies made directly to recipients versus through a distribution platform, and recipient category and registration path can matter.

Use this order every time:

- Gather the client facts needed to determine place of supply.

- Determine place of supply and assign GST/HST treatment.

- Create the invoice based on that result.

For recurring billing, keep a verification checkpoint. If cross-border facts are unclear, document your assumptions and confirm treatment against current CRA guidance before billing continues.

Keep a clear record of the facts you relied on and the place-of-supply result for each engagement. If relevant facts change over time, update the record so earlier decisions remain traceable.

A practical red flag is copying treatment from one foreign client to another without checking facts. Similar engagements can still differ on place-of-supply details.

Set up your GST/HST account correctly the first time#

Set up your GST/HST account before recurring billing starts, and make sure the account details match the legal business setup you invoice under. A clean setup now is easier than fixing filings after your first return cycle begins.

| Setup item | What to confirm | Related detail |

|---|---|---|

| Account details | GST/HST account details align with your legal invoicing setup | Pause and correct mismatches before continuing |

| My Business Account access | Verify access for the person handling filings | Business owners can view their GST/HST access code there |

| Reporting period | Record your reporting period and filing cadence | Monthly, quarterly, or annually |

| Ownership | Assign one owner for filing, payment approval, and reconciliation | Missing a GST/HST payment deadline can lead to penalties and interest |

| Setup memo | Save a setup memo with date, assumptions, and any follow-ups | Open questions should have an owner and due date |

Register through a CRA channel, then save a dated setup record with your confirmation details. If core account details do not match your invoicing setup, pause and correct them before continuing.

Open My Business Account early. CRA states business owners can view their GST/HST access code there (My Business Account only), and early access helps you confirm access before deadlines.

Use this readiness checklist before your first invoice batch:

- Confirm your GST/HST account details align with your legal invoicing setup.

- Verify My Business Account access for the person handling filings.

- Record your reporting period and filing cadence: monthly, quarterly, or annually.

- Assign one owner for filing, payment approval, and reconciliation.

- Save a setup memo with date, assumptions, and any follow-ups.

If your situation is unclear, use CRA guidance to confirm whether you need to register and start charging GST/HST before recurring billing starts.

A failure mode is partial setup: registration is done, but no one owns filing and remittance tasks. Missing a GST/HST payment deadline can lead to penalties and interest, so set ownership and timing at setup and review once before the first deadline.

Add one backup control before your first return period. Make sure at least one additional person can locate account details, filing dates, and prior confirmations if the primary owner is unavailable. Even a short absence can cause deadline misses when all knowledge sits with one person.

Your setup memo should also capture open questions that were not resolved at registration time. Mark each item with an owner and due date. Clearing those items early keeps your first filing cycle from becoming a mix of return prep and unresolved treatment research.

Charge GST/HST on invoices with evidence you can defend#

Your invoice should make the tax treatment obvious and traceable from day one. Treat each final invoice as both a billing document and a filing record.

Issue a valid GST/HST invoice with required identifying details, tax details, and total amounts, and keep the service amount, GST/HST charged, and total clearly separate. Avoid blended totals or vague descriptions that make reconciliation harder later.

Before sending, confirm the client's province, then apply GST/HST treatment accordingly. If the invoice is for Quebec, include QST handling separately instead of assuming GST/HST treatment covers everything.

If treatment is uncertain, hold the final send. Create an internal draft, resolve the province-based tax treatment first, then issue the final invoice.

Use a short, strict pre-send checklist:

- Confirm client legal and province details are saved in the client file.

- Link invoice line items to the tax treatment decision on record.

- Record the province used for GST/HST rate selection in one clear sentence.

- Show service amount, GST/HST amount, and total as separate values.

- For Quebec invoices, handle QST separately, including QST registration and QST amount entries.

Store supporting records together: final invoice copy, client tax treatment notes, and any reversal or credit notes. Keeping the full trail in one place makes GST/HST return support and later corrections much cleaner.

If an exception to charging tax may apply, treat it as conditional, not automatic. Document the basis before sending, and escalate unclear cases to CRA or a qualified advisor.

You have the strongest control when each invoice line can be traced to one tax treatment decision and one client-province decision. That traceability keeps period-end reconciliation fast and reduces debates about why a specific treatment was used.

When a correction is required, close it fully. Issue the needed adjustment, update your decision note, and tie both records to the same client file entry. Partial fixes can become a source of repeated errors on later invoices for the same engagement.

File and remit on the right reporting period without cash surprises#

Your reporting period is a cash-control decision, not just an admin cadence. It determines how often you file GST/HST returns and remit collected tax. During setup, you choose filing frequency, and that choice is tied to expected annual revenue, so it is worth revisiting when revenue changes materially.

Use the same close process every period:

- Close the books for the reporting period.

- Reconcile GST/HST collected against eligible credits for that same period.

- File the GST/HST return.

- Remit on time and keep proof with your filing records.

If your cash discipline is uneven, consider a tighter filing cadence even if a slower one is available. For some teams, more frequent filing can make deadlines and remittance balances easier to manage.

Treat collected GST/HST as a liability instead of operating cash. Another avoidable risk is late registration: if you register too late, CRA may expect remittance on tax you never collected. Ignoring obligations can also lead to penalties, interest, or audits.

To improve close quality, set an internal cutoff for invoice finalization and classification updates before your reconciliation step starts. If records are still changing while you reconcile, your filing review becomes a moving target.

Keep proof files with the same naming pattern each period so retrieval is faster during review. You want remittance confirmation, return copy, and reconciliation support together in one place. That simple structure can save time when a question comes up after filing.

Use input tax credit claims without creating audit risk#

Input tax credits can reduce your GST/HST payable, but only for GST/HST paid on eligible business expenses that you can substantiate. Claim only what your records already support.

For each claim, keep a simple evidence pack with core support records, such as:

- Supplier invoice.

- Brief business-purpose note.

- Any records that connect the expense to your business activity.

This is the core tradeoff: broader ITC claims can reduce your GST/HST payable, but weak documentation can increase review risk. Detailed GST/HST records keep your position defensible if a claim is questioned.

If your support is incomplete, narrow the claim instead of stretching it.

A practical pre-filing check is to review claims that rely on short or unclear expense descriptions and confirm business purpose in plain language. If you cannot explain a claim clearly, treat it as higher risk until your support improves.

Some self-employed taxpayers may face a tax review or audit soon after the June 15 income tax-filing deadline, so keep ITC evidence organized with the same period file as your return support. Co-locating records can make a review faster and reduce delays in substantiating claims later.

Build a monthly compliance checklist you can actually maintain#

Run one monthly checklist and do not move to filing until it is complete. Consistency supports timely filing, accurate reporting, and complete record-keeping.

Use a short checklist that directly supports filing accuracy and defensible records, then run it in the same order each month:

- Confirm your records and account details are current for the period.

- Review any new services or delivery changes for consistent tax treatment.

- Validate invoice tax treatment for accuracy.

- Reconcile GST/HST figures against your books before remittance.

- Track payroll deduction and corporate tax filing tasks in the same monthly cycle.

- Prep GST/HST return tasks in advance: draft figures, internal review date, submission date, and remittance date.

- File records in one fixed monthly structure: invoices, tax summaries, filing confirmations, and remittance proofs.

- Maintain a known-versus-unknown log for unresolved tax treatment questions, with an owner, due date, and interim treatment note.

Keep the close strict: unresolved items should never be ownerless. Consistent monthly execution helps avoid penalties, maintain good standing, and keep filing positions clear when records are reviewed.

The checklist works best when it has two gates: preparation and sign-off. Preparation confirms records are complete. Sign-off confirms each unresolved item has an owner, due date, and interim handling note before the period is closed.

Treat the known-versus-unknown log as an active decision tool, not a storage list. Review open items before the next cycle so unresolved assumptions do not roll forward.

If you miss a month, restart with a catch-up pass that reconciles the gap period first. Skipping forward without clearing the gap can create rework and conflicting notes in later months.

Know the red flags that mean talk to a tax pro now#

Escalate now if uncertainty could change what you file or remit. A solid monthly close helps, but it does not replace professional review when core GST/HST treatment is unclear.

Use red-flag lists as practical warning signs, not official CRA formulas. Advisory sources flag GST/HST filing errors, mismatches between income reporting and HST reporting, and weak input tax credit documentation as risk areas.

- You are not confident your GST/HST return is complete or free of filing errors.

- Your sales totals used for income reporting do not align with what was reported on your HST return.

- You cannot produce clear support for one or more input tax credit claims.

- The same discrepancy or documentation gap keeps showing up from one filing period to the next.

Before speaking with an advisor, prepare your recent GST/HST returns, remittance confirmations, sales totals used for income reporting, and support for disputed ITCs. If a discrepancy or documentation gap repeats, stop self-diagnosing and get advice before the next return.

Escalation is most effective when the question is precise. Write down the exact treatment call you need confirmed, the period affected, and the invoices or claims involved. Focused questions lead to faster, clearer guidance and reduce back-and-forth before filing deadlines.

After you receive advice, update your decision notes and checklist controls immediately. The value of escalation is not only fixing the current issue, but also preventing the same issue in the next filing period.

Conclusion#

The goal is consistent execution, not perfect tax theory. GST/HST is collected at sale and remitted to the Canada Revenue Agency, so the practical move is to decide treatment early, document each decision, and escalate edge cases instead of guessing.

Run one recurring status check so registration risk does not sneak up on you. Use a recurring revenue-threshold check as your first screen. Treat the commonly cited $30,000 over four consecutive calendar quarters as a trigger to review, not a complete legal test on its own. If facts are unclear, confirm your position against current CRA guidance before issuing invoices.

Keep invoice treatment tied to customer location. Place of supply rules can change treatment based on where the customer is located, and HST is not used in every province. The Ontario 13% example (5% GST + 8% PST) is province-specific, not a Canada-wide default.

Use a lean evidence pack to stay defensible:

- A dated log of each tax treatment decision and what fact drove it.

- Client location and service details stored with each related invoice.

- Period-by-period records linking tax collected and remittance history.

- A tracked escalation note for unresolved items until final resolution.

Keep this process practical: decide, document, verify, and escalate when needed. That sequence keeps compliance clear as your client mix changes and gives you a repeatable way to handle uncertainty without last-minute panic.

Use this article as your working reference, then confirm unresolved jurisdiction-specific points directly with the Canada Revenue Agency or a qualified professional.

Frequently Asked Questions

When must a freelancer register for GST/HST in Canada?

Use small-supplier status as your first screen, and treat the commonly cited $30,000 sales level as a practical trigger check. Do not treat that alone as a complete legal test. Confirm your exact facts against current CRA guidance before deciding. A useful practice is to review this status before each major invoice cycle, not only at year end. That can give you more room to register before new invoices go out if your status changes.

Can I choose voluntary registration before I am required to register?

Confirm voluntary-registration eligibility rules against current CRA guidance or with a qualified advisor before you proceed. If you do proceed, plan for added filing and recordkeeping discipline. If your records are not ready for recurring compliance tasks, resolve that first.

When do I start charging GST/HST after I register?

Confirm timing directly with current CRA guidance or a qualified advisor before finalizing invoices. If you billed during an uncertain period, isolate those invoices and review them as one group. A grouped review can make corrections easier to manage.

How do input tax credits reduce what I actually remit?

Keep clear support for each ITC claim and the business purpose of related expenses, and confirm treatment before filing. If support is weak, treat the claim as higher risk until reviewed.

How often do freelancers file a GST/HST return?

It depends on your reporting period. Common reporting cadences are monthly, quarterly, or annually. Align your bookkeeping and cash planning to that cycle so remittance deadlines are easier to meet. If deadlines repeatedly feel tight, move internal close dates earlier in the period to reduce last-minute pressure.

What records should I keep to defend my GST/HST treatment if reviewed?

Keep organized records in a period-by-period structure, such as invoices, GST/HST return copies, remittance confirmations, and support for claimed input tax credits. Records must be kept at your place of business or residence in Canada unless CRA gives written permission otherwise. Records stored outside Canada and only accessed electronically from Canada are not considered records kept in Canada. Consider keeping treatment notes tied to client location and service classification decisions. These notes can help explain the logic behind invoice treatment when you revisit older periods.

What should I do first if I think I started charging too late or filed incorrectly?

Build a reconciliation pack first: what you invoiced, what you filed, what you remitted, and where treatment may be wrong. Then escalate quickly to a qualified tax professional so corrections are scoped before the next filing cycle. Move quickly on payment decisions, since missed GST/HST deadlines can lead to penalties and interest. Work from documented facts, not assumptions, while you correct the issue.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Ho Chi Minh City Digital Nomad Guide for a 30-Day Move (2026)

Ho Chi Minh City is a strong base if your priority is keeping work momentum while relocating. You get density, plenty of places to work from, and a social scene that can help you settle quickly. It is a weaker fit if your best days depend on calm streets, easy walking, and long stretches of quiet. In practice, Saigon tends to reward people who want convenience and activity more than retreat pace.

The Best Video Editing Software for Freelancers

**Choose the best video editing software based on the workflow you can repeat under pressure, not the tool that looks most impressive on YouTube.** You are the CEO of a business-of-one, and your editor is part of your delivery infrastructure. When a client changes scope, sends a new batch of footage, or asks for "one more revision," your editor stops being a creative playground and becomes a system you either trust or fight.