Quick Answer

Yes, you can usually keep a U.S. S-corp after a move if owner eligibility remains valid and filings stay controlled. For s-corp moving abroad situations, treat relocation and expatriation as different decisions: routine relocation remains in the normal U.S. filing lane, while status-ending events can trigger Form 8854 and covered-expatriate tests. Before departure, lock ownership records, payroll continuity, and Form 1120-S readiness, then recheck those assumptions shortly after arrival.

Start Here if You Are Moving Abroad With an S Corporation#

Yes, you can often keep a U.S. S Corporation after moving abroad, as long as the eligibility and ownership rules still hold.

Relocation alone does not automatically end S-corp status. A U.S. citizen can live abroad and continue running a U.S.-based company. The real risk is whether a shareholder, residency, or ownership change makes the entity ineligible.

What usually keeps the entity intact#

If you remain a U.S. citizen, the structure can often stay in place as long as the shareholder rules stay clean. Key constraints in the excerpts include one class of stock, up to 100 shareholders, and no direct share ownership by a Nonresident Alien.

Start with records, not optimization. Review your cap table or shareholder ledger, confirm current ownership, and confirm any planned transfers before or after departure. If a spouse, partner, foreign person, or foreign entity may receive shares, treat that as a pre-move decision point.

Scope of this article#

This guide covers moving abroad while still remaining in a U.S. filing posture. It is not a guide to giving up U.S. tax status.

If your facts are more complex than "U.S. citizen living overseas," residency classification can matter. The excerpts describe a Resident Alien as someone with a green card or someone who meets the Substantial Presence Test, which counts U.S. days over a three-year period. They distinguish that from a Nonresident Alien for direct S-corp ownership.

What to verify before you move#

Before departure, confirm these in writing:

| Checkpoint | What to confirm |

|---|---|

| Share ownership | Current and planned share ownership, including whether any owner could be a Nonresident Alien |

| Operations from abroad | Whether payroll, officer compensation, and annual filings can still be run on time from abroad |

| Scope of change | Whether this is only a relocation, or part of a larger change that needs specialist review |

If you keep the entity, the compliance work does not stay behind. The filing cycle still applies, including Form 1120-S, which the excerpted checklist lists as due March 15. If you use salary plus distributions, keep the same guardrail: a lower salary can reduce payroll tax, but setting it too low can increase audit risk.

When to involve a CPA or tax attorney#

Bring in a CPA or tax attorney early if any of these apply:

- you may add, gift, or transfer shares and eligibility is unclear

- your residency classification depends on green card or Substantial Presence Test facts that are not settled

- a possible exit-tax or citizenship- or residency-ending path is on the table (outside this section's scope)

- payroll, books, or Form 1120-S execution already feels unstable

The rest of this article follows a practical order. Confirm status and shareholder eligibility first. Then decide whether the entity can stay in place, then tighten filing, payroll, and documentation.

For a step-by-step walkthrough, see Delaware C-Corp Franchise Tax: Filing Methods, Deadline, and Annual Checklist.

Know the Terms That Decide Your Outcome#

Classify your IRS tax status first, before you change structure, because that status drives what you report and how you file from abroad.

Treat Resident Alien and nonresident labels as filing-critical, not casual descriptions. The IRS says U.S. citizens and resident aliens abroad are taxed on worldwide income, and their filing and estimated tax rules are generally the same as if they were in the United States. In the self-employment tax context, individuals who are neither U.S. citizens nor U.S. residents are not subject to U.S. self-employment tax.

For status classification, do not guess based only on where you currently live. Confirm the status you are filing under and keep your records aligned with that filing position. If you use the automatic overseas extension, attach the required statement to the return.

One easy-to-miss edge case is timing. The IRS says self-employment income received while you are a U.S. resident can still be subject to self-employment tax, even if the services were performed while you were a nonresident. If your status may change during the year, keep dated proof of travel, immigration status, and when income was earned versus received.

Decide if You Can Keep Your S Corporation Before You Move#

Start with tax-status checks before you make ownership or restructuring moves. If your status could change, pause structural changes until you confirm the tax consequences.

Living abroad is not the deciding event. U.S. citizens and resident aliens are still taxed on worldwide income. The key go/no-go factors here are your U.S. taxpayer status and whether near-term life changes could move you into expatriation rules.

| Decision check | If yes | If no or unclear | Why this is the real risk point |

|---|---|---|---|

| You will remain a U.S. citizen or resident alien after the move | Plan for continued U.S. filing and compliance from abroad | Stop and assess whether you are approaching a status-ending event or ending long-term resident status | Moving overseas is not the same as ending U.S. tax status |

| You are not planning a renunciation or long-term-resident status termination | Continue with a compliance-first move plan | Pause major ownership or restructuring steps until reviewed | Expatriation rules apply to formal status changes, not just relocation |

| You can meet filing obligations while abroad | File on time (or use available extensions correctly) so eligible FEIE/foreign tax credit claims stay available | Fix filing ownership and timeline before making structural changes | Tax benefits require a filed U.S. return; extensions do not stop interest on unpaid tax |

Use this as a screening tool, not a substitute for legal advice. A full set of "yes" answers suggests no immediate expatriation trigger from the move itself. Any "no" or "unclear" answer means the risk is the status change, not the relocation.

The keep rule#

If you remain a U.S. citizen or resident alien, treat "now I live abroad" as a compliance issue, not an automatic change in U.S. tax exposure. File when required, because benefits like FEIE or the foreign tax credit are available only when an eligible taxpayer files a U.S. return.

If you expect to use the automatic 2-month extension available to some taxpayers abroad, attach the required statement when you qualify. Also remember that interest still accrues on unpaid tax after the regular due date. If you have net earnings from self-employment, self-employment tax can still apply (generally at $400 or more), even when foreign earned income is excluded.

The stop rule#

If your plan includes a possible status-ending event or ending long-term resident status, stop before restructuring. That is where a routine relocation can turn into a separate regime with its own tests and filings.

Form 8854 is a key checkpoint. Failure to certify five years of U.S. federal tax compliance is itself a covered expatriate trigger. Other triggers can include net worth of $2 million or more on the expatriation or residency-termination date. The IRS also lists a $206,000 income-tax-liability threshold for 2025. If those outcomes are even a medium-term possibility, get review first and change structure second.

What to verify before departure and after arrival#

Before departure, verify these three items in writing:

- Status assumptions: whether you expect to remain a U.S. citizen or resident alien, and whether any planned event could end that status for tax purposes

- Filing readiness: return ownership, required data flow, and extension handling; if you are planning around FEIE, remember one path requires 330 full days in 12 consecutive months

- Expatriation checkpoints: whether Form 8854 certification, the $2 million net-worth test, or the year-specific income-tax-liability threshold could become relevant

After arrival, re-check the same three items within the first few weeks. Make sure immigration records and tax files reflect the same move timeline and facts.

Moving Abroad and Expatriation Are Not the Same Event#

Treat relocation and expatriation as two different paths from day one. Moving abroad can still leave you in the regular U.S. compliance lane, while expatriation is a separate IRS track with its own filings, timing checkpoints, and tax treatment.

Two different buckets#

If your facts are relocation only, you may still be dealing with ongoing cross-border operations and compliance while the business continues. The other bucket is different. The IRS states that tax provisions in this area apply to U.S. citizens who relinquish citizenship and long-term residents who end residency. That is a status-ending event, not just a move.

Why expatriation is a separate file#

Once that regime is in play, you are in a separate filing track. Form 8854 is the Initial and Annual Expatriation Statement, and the IRS says it is used by individuals who expatriated on or after June 4, 2004.

The Form 8854 instructions also show that this is its own regime. They include Who Must File, When To File, Where To File, Taxation Under Section 877A, Penalties, and procedures for deferral of mark-to-market tax payment. In practice, that means expatriation-specific tax treatment and compliance risk beyond normal move-abroad administration.

The decision rule for today's entity choices#

If this path is even a medium-term possibility, keep today's entity moves easy to unwind. Avoid rushed ownership changes, speculative conversions, or cleanup steps based on assumptions about future status.

The default is to keep the company stable until your path is clear. Relocation usually calls for tighter execution. A status-ending event calls for a separate decision process. Mixing the two is where avoidable cost and complexity show up.

Ownership Changes That Create Immediate Risk#

A high-risk ownership move is making a transfer before shareholder eligibility is reviewed. If you rely on S-corp treatment, keep core eligibility checkpoints in view, including Form 2553 on file and domestic U.S. corporation status, and treat ownership changes as active compliance work rather than admin cleanup.

The edge cases people treat too casually#

Most problems start with ordinary life events, not big restructures. Common examples include:

| Ownership move | Article note |

|---|---|

| Adding a spouse to ownership | Can change the ownership and reporting picture |

| Gifting shares to a family member | Can change the ownership and reporting picture |

| Transferring shares into a holding company, trust, or other entity | Can add cross-border reporting complexity |

Each of these can change the ownership and reporting picture, and some can add cross-border reporting complexity. A transfer that feels practical for family or asset planning can still create a tax-position mismatch if the documentation and analysis lag behind.

Why cross-border owner discussions are a review trigger#

If a proposed transfer introduces cross-border facts, pause and get the shareholder analysis confirmed before you sign or record the transfer.

Cross-border structures add jurisdiction questions, and U.S. tax and reporting obligations still need active tracking. Keep your stock ledger, transfer documents, and tax position aligned so your records tell one consistent story.

The ESBT point you may see online#

You may also see ESBT mentioned in this area. The narrow grounded point is this: for section 1361 purposes, beneficiaries of an Electing Small Business Trust (ESBT) are treated as S corporation shareholders.

That confirms ESBT treatment exists, but it does not mean a trust automatically resolves foreign-owner concerns. Once trusts and cross-border facts are involved, specialized review is the right move.

Your decision checkpoint#

Use this internal control: no ownership transfer proceeds until shareholder eligibility is reviewed and documented. At minimum, keep:

- current cap table or stock ledger and the proposed post-transfer ownership

- the exact transfer paperwork, whether gift, assignment, trust transfer, or similar

- a written memo or advisor confirmation describing the assumed shareholder treatment for the transfer

For cross-border, foreign-entity, or trust scenarios, treat ownership changes as legal and tax events, not routine admin.

Related: A Deep Dive into the 'At-Risk' Rules for S-Corp Losses.

How Taxes Actually Change After the Move#

Moving abroad does not shut off U.S. filing. It means you now have to qualify for international relief each year and file it correctly.

Think of this in two layers: your regular filing flow, plus FEIE or Foreign Tax Credit analysis on top. Relief may be available, but it is not automatic.

| Item | What changes after you move abroad | What to watch |

|---|---|---|

| U.S. filing obligation | Your move does not automatically remove U.S. reporting obligations for income. | Keep your filing process organized so income is reported on your U.S. return. |

| Physical presence test | FEIE can apply only if you meet a qualification test. | You need 330 full days in a 12-month period. If you miss that threshold, the test is not met. |

| Bona fide residence test | This is a different FEIE qualification path. | It is facts-and-circumstances based and must include an uninterrupted period with an entire tax year. |

| FEIE claim | FEIE can apply only if you qualify under IRS tests and file correctly. | Qualifying does not eliminate filing; you still report the income on your U.S. return. |

| Foreign Tax Credit | FTC may be relevant instead of, or alongside, FEIE depending on your facts. | Form 1116 is category-specific. Use separate forms by category, and check only one category box per form. |

FEIE helps only when you meet the tests#

For 2026, the maximum FEIE is $132,900 per person. For 2025, it is $130,000 per qualifying person, limited to the lesser of foreign earned income or that amount.

Under the physical presence test, you need 330 full days in a 12-month period. A full day is 24 consecutive hours, midnight to midnight. This test applies to both U.S. citizens and U.S. residents. If you miss 330 days, the test is not met regardless of reason.

The bona fide residence test is different. It is facts-and-circumstances based and requires an uninterrupted period that includes an entire tax year. Living abroad for one year does not automatically qualify you.

FEIE is not filing relief#

Even when FEIE applies, you still file a U.S. return and report the income. FEIE changes the tax calculation, not the filing duty.

If you claim a foreign housing exclusion, figure that first, because it reduces foreign earned income available for FEIE. The general housing expense limit is 30% of the FEIE maximum: $39,000 (2025) and $39,870 (2026) under the general rule.

FTC comparison is process-heavy, not one-size-fits-all#

Do not assume one approach always wins. The practical move is to model FEIE and FTC from your own facts instead of using a generic expat template.

On execution, Form 1116 is where the complexity shows up: category-by-category treatment, one category box per form, and separate forms when income spans categories.

Compensation changes are a separate review lane#

If you want to change compensation after moving, treat that as a separate review from the FEIE/FTC mechanics covered here. For a deeper treatment, read What is 'Reasonable Salary' for an S-Corp? A Guide to IRS Compliance.

Filing and Reporting Calendar You Need to Keep Clean#

After you move abroad, the safest approach is one annual filing calendar that keeps your business return, personal return, FEIE support, and offshore checks in sync. Once those live in separate trackers, mistakes usually follow.

Keep the business return and personal return on the same map#

Your U.S. filing obligation generally continues while you live abroad, including income tax returns and estimated tax. Keep your business return process and your individual return process on one timeline so handoffs are visible and accountable.

If you plan to claim FEIE, remember that the claim is made on a U.S. return that reports the income. FEIE can change the tax calculation, but it does not remove the filing requirement.

Build currency conversion into your process early. Amounts reported on a U.S. return must be in U.S. dollars, so if records are in another currency, make translation a standard prep step, not a last-minute scramble.

FEIE qualification needs evidence, not memory#

If you use the physical presence test, track days throughout the year. The standard is 330 full days in a 12-month period, and a full day is 24 consecutive hours, midnight to midnight. The days do not have to be consecutive, but missing the count fails the test regardless of reason.

If you use the bona fide residence route, keep records that support residence for an uninterrupted period that includes an entire tax year, January 1 through December 31. Living abroad for one year by itself does not automatically establish bona fide residence.

Add offshore checks every year#

Run two separate offshore checks every year:

- FBAR via FinCEN Report 114 if you had a financial interest in, or signature or other authority over, foreign financial accounts

- Form 8938 review when specified foreign financial assets are above the reporting threshold that applies to you

Treat Form 8938 as an annual applicability check, not a one-time assumption.

One calendar, three owner controls#

Keep one annual tracker with these fields:

- owner document deadline

- preparer handoff date for business return documents, FEIE support, FinCEN Report 114, and any Form 8938 review

- "ready for signature" date for each filing

This single control makes dependencies obvious. If business records are not final, personal and international filings are not truly ready.

Your First 90 Days Abroad Checklist#

Use your first 90 days abroad to lock down the facts your filing plan depends on. Do it early. Then year-end prep for FEIE/FTC workpapers and your U.S. return stays at a maintenance level instead of turning into a reconstruction project.

| Timing | What to lock down | Practical checkpoint |

|---|---|---|

| Week 1-2 | FEIE test assumptions (physical presence vs. bona fide residence) and a day-count method | Your plan states which test you are evaluating and how you will track full days abroad |

| Week 3-6 | Travel-log discipline for the physical presence window | You can show a current log that tracks full days and rolling 12-month coverage |

| Week 7-10 | FEIE and Foreign Tax Credit assumptions using Form 1116 scenarios | You have run both paths in U.S. dollars and are not assuming one always wins |

| Week 11-13 | Filing workpapers for FEIE/FTC and U.S. return reporting | Your travel records, FEIE assumptions, and foreign-tax records are organized for preparer handoff without guesswork |

Week 1-2. Start by writing down the eligibility assumptions behind your plan. If you expect to use the physical presence route, remember it applies to U.S. citizens and certain U.S. residents under IRC 7701(b)(1)(A) and is based on how long you are abroad.

If you are evaluating bona fide residence, do not treat one year abroad as automatic qualification. The uninterrupted period must include an entire tax year.

Week 3-6. Build your travel log now, not at year-end. For physical presence counting, a full day is 24 consecutive hours, midnight to midnight, and the target is 330 full days in any 12 consecutive months.

The checkpoint is simple: if your preparer asked today how your day count is trending, you should be able to show it from your records.

Week 7-10. Test FEIE and FTC paths before assumptions harden. If you miss the 330-day count, the physical presence test is not met regardless of reason. Days spent in a foreign country in violation of U.S. law also do not count for this test, and there is only a limited waiver path for war, civil unrest, or similar adverse conditions.

For FTC, Form 1116 is prepared by income category, you check one category box per form, and amounts are reported in U.S. dollars. If housing exclusion is relevant, compute it first because it reduces FEIE-eligible income. For 2026, FEIE is capped at $132,900 per person if you qualify.

Week 11-13. By the end of month three, lock a working file for return prep. Include your dated travel log, FEIE test assumptions, draft FEIE/FTC calculations, and foreign-tax records for potential Form 1116 support.

Final checkpoint: each calculation should tie back to source records without reconstruction, and you should be ready to report income on your U.S. return even if you claim FEIE.

Want one place to track residency assumptions and filing deadlines during your first quarter abroad? Use the Tax Residency Tracker.

Build an Evidence Pack Before the IRS Asks#

Keep one evidence pack that ties your annual return support and foreign-reporting inputs together, so year-end stays focused on verification instead of reconstruction.

| File or record | What to keep |

|---|---|

| Core company file | Annual return materials and filing confirmations |

| International reporting file | Foreign account inventory, the account inputs used for Form 8938, and a record of whether any foreign deposit or custodial accounts were closed during the year |

| FBAR records | Keep FBAR (FinCEN Form 114) records alongside this file |

Keep the core company file and the international reporting file linked, and store FBAR records alongside them.

For Form 8938, keep the filing logic explicit. It applies when you are a specified person with reportable specified foreign financial assets. A U.S. citizen is a specified individual. Higher thresholds apply in some contexts, including joint filers or taxpayers residing abroad. Certain specified domestic entities have thresholds of more than $50,000 on the last day of the year or more than $75,000 at any time during the year.

Attach Form 8938 to your annual return and file it by that return's due date, including extensions. If no income tax return is required for the year, Form 8938 is not required.

Keep FBAR (FinCEN Form 114) records alongside this file, because filing Form 8938 does not replace a separate FBAR filing when FBAR otherwise applies.

Run one recurring checkpoint in your process: confirm your return records and foreign-account inventory still match what you would file today. One controlled audit trail with clear versioning and access controls keeps handoff fast if your preparer or reviewer asks for support.

Related reading: A Guide to Accountable Plans for S-Corp Expense Reimbursements.

Red Flags That Mean You Should Stop and Get Advice#

Stop DIY filing and get specialist international tax advice if any item below is true.

Expatriation or Form 8854 is in play#

If you are considering expatriation, Form 8854, or think U.S. exit-tax rules may apply, treat this as a high-risk transition, not routine move-abroad planning. IRS rules under IRC 877 and 877A can apply to U.S. citizens and to certain long-term residents who end U.S. resident status for federal tax purposes, and Form 8854 applies to people who expatriated on or after June 4, 2004.

A key danger point is covered expatriate status. IRS-listed triggers include net worth of $2 million or more, an average annual net income tax liability threshold that reaches $206,000 for 2025, and failure to certify 5 years of U.S. federal tax compliance on Form 8854. IRS guidance also flags significant penalty risk for not filing the form.

Planned ownership changes are not fully scoped#

If you are planning ownership or share-transfer changes and the tax consequences are not clearly documented, pause and get specialist review before making the change. Treat this as a structural tax and compliance decision, not admin cleanup.

Bring a clear review packet: current cap table, transfer drafts, tax-status documentation for the proposed owner, and a dated summary of what is changing. If classification or ownership facts are unclear, do not proceed on informal advice.

You are behind on offshore reporting#

If you are late on FBAR filings, get advice before filing catch-up forms. U.S. citizens and resident aliens abroad remain taxable on worldwide income, and foreign financial accounts can require reporting even when they produce no taxable income.

If your U.S. return positions and FBAR inputs do not reconcile cleanly in writing, that is a stop signal.

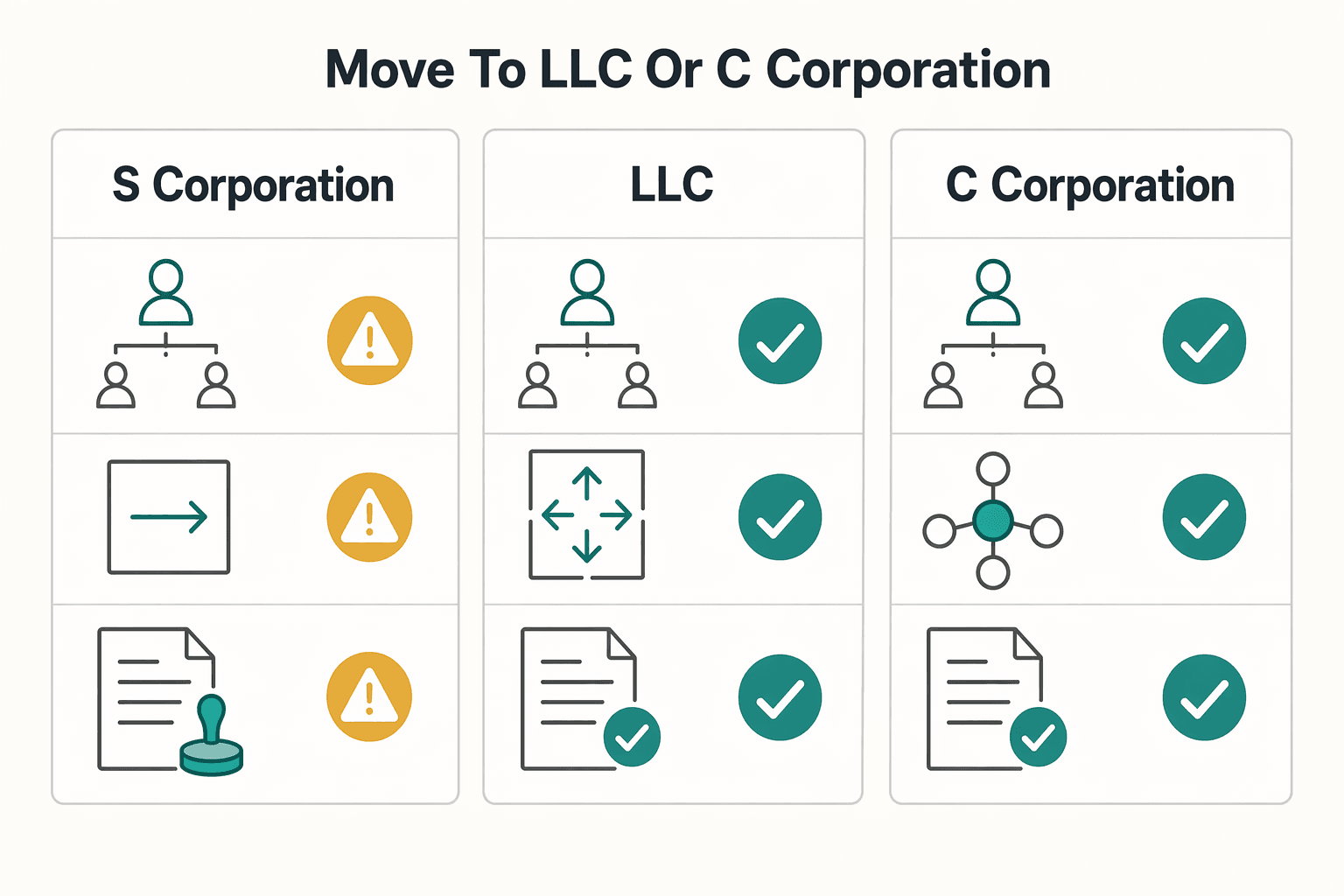

When It Is Smarter to Move to an LLC or C Corporation#

Keep the current structure unless your ownership or growth plan no longer fits S-corp eligibility rules. Moving abroad by itself is not the trigger.

One key checkpoint is ownership. S-corp treatment is generally limited to 100 shareholders, and shareholders must be U.S. citizens or residents. If your business remains a stable, closely held U.S.-owner operation, continuity may be the lower-disruption path.

| Entity | Best fit trigger | Key upside | Main tradeoff |

|---|---|---|---|

| S Corporation | Ownership stays within S-corp limits | Pass-through treatment and continuity with your current setup | Shareholder eligibility limits can block foreign participation |

| LLC | You need more ownership flexibility and a lighter-maintenance structure | Pass-through by default, optional C-corp tax election, and no U.S. citizenship or residency requirement in the comparison source | Transition work and ongoing tax handling depend on classification |

| C Corporation | You plan broader fundraising or international shareholders | No investor cap in the comparison source, international shareholders allowed, and stock can be sold to raise capital | Corporate-level filing (Form 1120), formal governance and recordkeeping, plus possible double taxation on distributed earnings |

Use this scenario contrast as a decision test:

- If you expect to stay a stable U.S.-owner business, keeping the current setup is usually the practical choice.

- If you expect foreign equity participation or broader ownership, S-corp constraints can make continuity impractical, and an LLC or C corporation may be a better structural fit.

Before switching, weigh near-term change costs against long-term fit:

- legal transition work and operational disruption now

- ongoing compliance load after the switch

- tax tradeoffs tied to your planned ownership and distribution model

Plain rule: switch only when ownership constraints or growth plans make continuity impractical.

Keep the Entity if It Still Fits and Make Compliance Boring#

If your decision table did not surface an unresolved eligibility issue, you may be able to keep the current structure and avoid restructuring for its own sake. The lower-friction path is clean, repeatable compliance and no ownership or reporting moves you cannot clearly document.

Choose boring over clever#

Do not assume an address change alone requires an entity change. If a proposed fix relies on ownership changes, informal transfers, or a filing position you cannot explain plainly, treat it as a red flag and pause for review.

On the personal tax side, use Publication 54 as a recurring checkpoint because it is the IRS guide for U.S. citizens and resident aliens abroad. Then verify updates at IRS.gov/Pub54 instead of relying on a static copy.

Keep a calendar and evidence pack that survive year end#

Make compliance repeatable with one calendar, clear handoff dates, and no year-end guesswork. Keep an evidence pack with:

- the Publication 54 version you used, for example, Rev. December 2025

- a dated note that you checked IRS.gov/Pub54 for post-publication updates

- copies or screenshots of current threshold lookups at IRS.gov/InflationAdjustment

- tax payment proof and any electronic payment confirmation numbers

This matters because Pub. 54 moved to continuous-use revision in tax year 2025, and annual inflation-adjusted amounts were removed from the publication. The IRS also recommends paying electronically whenever possible.

Escalate early when the facts stop fitting on one page#

Escalate when your facts are no longer easy to summarize and support. If you cannot document ownership, residency assumptions, filing path, and open questions on one page, treat that as edge-case territory and get targeted review before filing.

Next step: finish the pre-move decision table, attach your first evidence-pack items, and book tax review only for unresolved items.

If your case includes expatriation risk, ownership changes, or late offshore filings, pressure-test your operating plan before you restructure: Contact Gruv.

Frequently Asked Questions

Does moving abroad automatically cancel my S Corporation?

How moving abroad affects S-corp status is an entity-specific legal and tax question. Get qualified advice before making ownership or structure changes.

Can a Nonresident Alien own shares in my S Corporation?

S-corp shareholder-eligibility rules, including nonresident-alien ownership, require qualified review. If a proposed transfer involves a nonresident, foreign spouse, or foreign entity, pause and get qualified review before you execute it.

What changes first after I move abroad: tax treatment, payroll setup, or filing obligations?

FEIE qualification and reporting checkpoints come first. Under the physical presence test, you need 330 full days in foreign countries within any period of 12 consecutive months, and a full day is 24 consecutive hours from midnight to midnight. If you miss that day count, the test fails regardless of reason, including illness, family issues, vacation, or employer orders.

What happens to my S Corporation if I later expatriate?

How expatriation affects S-corp status, elections, or continuity requires separate planning. Treat expatriation as a separate planning event and get entity-level guidance before making hard-to-unwind ownership or structure changes.

Can I use FEIE and still run payroll through my S Corporation?

This section does not provide a blanket yes-or-no rule on FEIE alongside S-corp payroll mechanics. What it does support is that FEIE applies only if you qualify and file a U.S. tax return reporting the income, and the exclusion is applied to the year the income was earned rather than when it was received. Keep payroll records, travel-day tracking, and FEIE assumptions aligned before filing.

When should I stop trying to keep the S Corporation and move to an LLC or C Corporation?

The legal and tax thresholds for when to switch entity type require entity-level guidance. If you are considering a change, get entity-level guidance first; if your immediate issue is compensation mechanics, start with reasonable salary for an S-Corp.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

What Is a Reasonable Salary for an S-Corp Under IRS Rules?

Start with this rule: if you actively work in your S corporation and receive, or are entitled to receive, payment for those services, that compensation is generally treated as wages. For federal employment tax purposes, [corporate officers, including S corporation officers, are employees](https://www.irs.gov/businesses/small-businesses-self-employed/s-corporation-employees-shareholders-and-corporate-officers), and service payments should be handled as wages rather than distributions or shareholder loans.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.