Quick Answer

Yes, a coworking space membership may be deductible if you are self-employed, report business expenses on Schedule C, and can show the cost was ordinary, necessary, and tied to real business use. It is not automatic just because you work remotely or like the environment, so keep invoices, payment proof, and calendar or usage records that show consistent business activity.

The Qualification Framework: Is Your Coworking Space a Deductible Business Asset?#

Short answer: possibly, if you are claiming it as a self-employed business expense and you can show it is both ordinary and necessary. It is not automatically deductible just because you work remotely or prefer the environment. That ordinary-and-necessary standard does the real work here, and both parts matter:

- Ordinary: common and accepted in your trade or industry.

- Necessary: helpful and appropriate for your business, even if not strictly required.

Who gets to make the claim#

Start with filing status. For self-employed filers and sole proprietors, business expenses are reported on Schedule C. That is the main lane this section addresses. Keep your categorization and records clean; misclassification can invite scrutiny or cause missed deductions.

What strong business use looks like#

A workable position comes from repeatable business use, not personal preference. Use this quick pressure test:

| Weak justification | Stronger justification | Why it is stronger |

|---|---|---|

| "I focus better there." | "I use it regularly for billable work and client calls." | Preference is personal; recurring business use is easier to defend. |

| "I like the atmosphere and perks." | "I use the workspace for client meetings and core admin work." | Bundled perks can blur purpose unless business use is clear. |

| "I go when I feel like it." | "My calendar shows recurring work sessions tied to business tasks." | Consistency supports the business-use story. |

One important boundary: general business-expense guidance treats commuting from home to your regular office as non-qualifying. If the main purpose is simply having a nicer place to go each morning, the case is weaker.

Where the business actually runs#

The practical question is simple: does the membership function like a real business asset, or like a convenience purchase? Use this checklist to answer with records, not memory:

- Where do you usually do revenue-producing work?

- Where do you handle core management/admin work?

- Where do client calls or meetings typically happen?

- What location shows up consistently in your calendar and business records?

- Do invoices and payment records match periods of active business use?

If your records and explanation point to the space consistently, your file is stronger. Keep the core support aligned with that story: the membership agreement or invoice, proof of payment, and a calendar trail showing real business activity.

Gray areas and when to ask a tax professional#

Gray areas do not automatically kill the deduction, but they do raise the standard for your records. Common examples include:

- Mixed personal and business use in the same year

- Plans that bundle workspace with lifestyle perks you cannot separate clearly

- Inconsistent usage patterns that are hard to tie to business activity

- Uncertainty about categorization on Schedule C

If you cannot explain the business purpose clearly and match it to records, get professional advice before claiming it. You might also find this useful: How to Write Off a Home Office as a Renter.

The Home Office Dilemma: A Decision Framework for Deducting Both#

You may be able to deduct both, but the position is usually strongest when each location has a distinct, provable business role. Your home office must qualify on its own, and coworking costs should reflect separate business use that is properly substantiated, not duplicate claims for the same function. This is where many otherwise reasonable positions break down. The issue usually is not that both spaces exist. It is that the records describe both as doing the same job.

For home-office treatment, the home area must be used exclusively and regularly for a qualifying business purpose. If that area is also used as personal space, it generally does not meet the exclusive-use requirement.

Start with a simple decision flow#

Use this sequence before you try to claim both:

| Check | What to confirm | Risk noted |

|---|---|---|

| Home-office qualification | A specific home area is used exclusively and regularly for business | If that area is also used as personal space, it generally does not meet the exclusive-use requirement |

| Principal-place reality | The home area aligns with where important business activities happen and where you spend business time | The records describe both as doing the same job |

| Admin-rule conflict | If you rely on admin/management work, there is no other fixed location where substantial admin/management happens | Recurring invoicing, bookkeeping, and planning at a fixed coworking desk can undercut the home-office claim |

- Home-office qualification first: Is there a specific home area used exclusively and regularly for business?

- Principal-place reality check: Does that area align with where important business activities happen and where you spend business time?

- Admin-rule conflict check: If you rely on home-office eligibility through admin/management work, do you have no other fixed location where substantial admin/management happens?

That third step is where dual claims often fail. If your records show recurring invoicing, bookkeeping, and planning at a fixed coworking desk, that can undercut a home-office claim that depends on home being your only fixed admin location.

Split roles clearly (and keep records aligned)#

A defensible dual-claim file usually assigns each location a different business role and keeps your records consistent with that split:

| Business function | Stronger home-office case | Stronger coworking case | Dual-claim risk |

|---|---|---|---|

| Deep work | Exclusive, regular home area for core solo work | Project-based focus blocks | Risk rises if both are described as your main work base |

| Admin/management | Home handles substantial admin work, with no other fixed admin location | Occasional overflow admin only | High if coworking is also a fixed, substantial admin base |

| Client-facing work | Limited home role | Calls, meetings, presentations, room bookings | Stronger when client activity is clearly centered at coworking |

| Collaboration | Minor/occasional | Team sessions and partner work | Moderate if infrequent and poorly documented |

| Specialized facilities | Not available at home | Printing, meeting rooms, mail handling, studios | Strong when invoices/bookings match business activity |

Separate costs so you do not double-claim#

Once the role split is clear, keep the cost treatment separate too:

| Cost type | Treatment |

|---|---|

| Coworking membership, room bookings, printing, similar workspace charges | Potential business expenses when tied to actual business activity and properly substantiated |

| Home-office costs under regular method | Allocate home costs between personal and business use |

| Home-office costs under simplified method | $5 per square foot, up to 300 square feet |

You cannot use both simplified and actual home-office methods for the same home in the same tax year.

Do-not-double-claim check before filing:

- Use distinct business roles for each location. Do not reuse the same justification twice.

- Keep one home-office method for the year, simplified or actual, not both.

- Treat daily home-to-regular-coworking travel as generally nondeductible commuting.

- If relevant, treat travel between business locations as generally deductible business transportation.

Run a repeatable evidence routine#

Dual claims need a clean paper trail. A simple routine is enough if you apply it consistently:

- Keep calendar entries with business purpose + location, not just "work."

- Keep task logs by location so the pattern matches your role split.

- Keep supporting documents such as invoices, receipts, and paid bills, and match them to calendar and task dates.

- Keep records long enough to support deductions claimed.

A useful control is to sample one month and confirm your calendar, task history, and billing records all tell the same story.

When to escalate to a tax professional#

Escalate when the facts are messy, not just because two locations are involved. The main pressure points are:

- mixed personal/business use in the claimed home-office area

- location patterns that shift without a clear operating reason

- coworking becoming your practical admin base while home-office eligibility depends on admin use

- major work-pattern changes during the year, such as moving or changing where core work happens

If you claim both in one year, your records should show one coherent operating reality.

Related: How to Handle Taxes for a Side Hustle. Before you finalize your filing position, run the home office deduction calculator to pressure-test your home-vs-coworking allocation using the same logic as this section.

The Maximization System: Claiming Every Legitimate Coworking Expense#

Treat each charge as a business-expense candidate first, then claim only what you can clearly support as ordinary, necessary, and tied to business activity. The goal is not to force every line onto the return. A deduction reduces taxable income, not tax owed dollar for dollar, so the real gain is clean classification backed by records.

Classify charges before you total them#

Do not start with the annual total. Start by deciding what each charge actually is so every line has one clear home:

| Charge category | What it covers |

|---|---|

| Membership access | Core workspace access tied to your business activity |

| Add-on services | Extra workspace charges billed on top of membership |

| Travel-related workspace access | Temporary workspace access connected to business travel activity |

| Ancillary business services | Non-desk services attached to the account that support operations |

Inclusion/exclusion screen#

A quick screen up front will usually catch overclaim risks before they reach your books:

| Charge pattern | Initial treatment | Evidence to keep | Guardrail |

|---|---|---|---|

| Workspace access with clear business use | Keep as a potential claim candidate | agreement, invoice, payment proof, usage dates | Tie the charge to actual business activity |

| Add-ons connected to specific work activity | Review case by case before treating as a claim candidate | booking/service record, invoice, receipt, calendar note | Avoid vague labels with no business context |

| Temporary workspace tied to business travel work | Review separately before treating as a claim candidate | itinerary, work schedule, invoice, payment proof | Keep workspace items distinct from broader travel totals |

| Bundled plans with both business and personal-style benefits | Allocate before claiming | plan terms, tier details, allocation note, invoices | Do not claim the full bundle by default |

| Personal amenities, social use, guest convenience | Keep out of claim candidates unless business purpose is documented | receipt plus exclusion note | Personal benefit is the main overclaim risk |

| Transportation costs grouped with coworking charges | Separate for independent review | fare/mileage records, trip-purpose notes | Do not bury transport inside workspace totals |

This screen helps you classify consistently; it does not guarantee that a line is deductible.

Allocate mixed-use plans the same way every month#

Mixed-use plans are manageable if you use one reasonable method and stick to it:

- Identify components with personal benefit.

- Isolate the business portion using a reasonable method you can explain.

- Document that method in a short note.

- Apply the same method consistently unless the plan changes.

For bundled plans, keep a tighter file: plan description, invoices, payment proof, and your allocation memo. If guest or perk usage is unclear, treat that piece conservatively.

Pre-filing check#

Before filing, confirm every claimed line has all three:

- A specific business purpose

- A clean category: membership, add-on, travel-related access, or ancillary service

- Matching documentation: invoice, payment record, and aligned notes

This check helps you avoid both missed deductions and weak ones. For a related freelancer deduction topic, see Can You Deduct Health Insurance Premiums as a Freelancer?.

The Global Professional's Ledger: Deducting a Foreign Coworking Space#

Yes, you can usually deduct a foreign coworking membership on your U.S. return when the cost is ordinary, necessary, and business-used. The baseline deductibility test is the same, but cross-border files usually need tighter execution. In practice, foreign charges get harder to defend when the file is thin on business use, currency conversion, or mixed-use allocation. If the activity is real and the records are clean, the position is much easier to support.

Use one FX method you can defend#

Consistency and a method that fits your facts and circumstances are critical. For most taxpayers, functional currency is generally USD, and amounts on a U.S. return must be reported in USD. The IRS also says to use the rate when you pay, receive, or accrue the item, while generally accepting posted rates used consistently.

| Conversion method | When to use it | Documentation needed | Consistency rule |

|---|---|---|---|

| Transaction-date spot rate | Usually appropriate for individual invoices, card charges, and wires, especially with noticeable FX movement | Invoice date, payment date, exchange-rate source, USD worksheet | Use the same timing and rate-source rule for similar charges |

| Card/bank posted USD conversion | Useful when your bank/card statement clearly shows the USD conversion for that exact charge | Statement with merchant and posted USD amount, matching invoice (local amount if shown) | Use only when the converted USD amount clearly matches the specific charge |

| Yearly average rate | Practical for recurring foreign-currency amounts when that method reasonably fits your facts | Foreign-currency totals worksheet, yearly-average source, method note | Do not switch between average and spot methods just to optimize tax outcome |

If the country has multiple exchange rates, use the rate that matches your specific facts and circumstances, and document why.

Minimum audit file for foreign coworking#

For foreign charges, the minimum file should be obvious to a reviewer without extra explanation. Keep one file per provider with:

| File item | What it should show |

|---|---|

| Invoice | Provider, service period, description, and local-currency amount |

| Proof of payment | Card statement, bank record, or canceled-check equivalent |

| Conversion worksheet | The rate used, source, and USD amount reported |

| Business-purpose note | Client meetings, delivery work, admin blocks, or travel workdays |

| Allocation note | Any part of the plan that includes personal use or nonbusiness amenities |

Keep FEIE separate from the expense analysis#

Do not let the foreign-earned income exclusion blur the expense analysis. FEIE can reduce regular income tax, but it does not reduce self-employment tax. For 2026, the FEIE maximum is $132,900 per qualifying person. Self-employment tax is still relevant when net self-employment earnings are at least $400 unless a separate rule changes that result.

Operationally, keep income-tax treatment and self-employment-tax treatment separate, and apply allocation discipline when only part of income is excluded. FEIE does not make coworking expense tracking optional.

When to escalate#

Some foreign files are routine. Others are not. Escalate to a cross-border tax professional when your facts include multiple countries, mixed entities, frequent currency swings, or hard-to-defend partial personal use. Escalate as well when totalization-agreement treatment may affect social tax exposure, since that can require agreement-level review and, in many cases, a Certificate of Coverage.

For a step-by-step walkthrough, see Can I Deduct Education and Professional Development Costs?.

The Defense Protocol: Building Your Bulletproof Documentation System#

Once you have a defensible business-use position and, for foreign charges, a consistent FX method, the next job is evidence. If you want to deduct the membership with less stress, build one complete file per charge, not a pile of receipts. The burden of proof is on you, and IRS audit guidance is clear that no single document carries the whole story. A receipt can show payment, but by itself it does not show business purpose or how the expense connects to your work.

Build an evidence chain, not a receipt folder#

A strong file reads from left to right: contract, bill, payment, use, business reason.

| Link in the chain | Save this | What it proves | Common weak spot |

|---|---|---|---|

| Contract | Signed membership agreement or plan confirmation | Real provider relationship and service terms | Missing provider name, start date, or plan details |

| Invoice | Invoice with provider, service period, description, amount, and currency | What was charged and for which period | Generic receipt with no service period or description |

| Payment proof | Card statement, bank record, or similar proof matched to the invoice | The charged amount was actually paid | Payment record does not clearly match invoice amount/date |

| Usage evidence | Room bookings, entry logs, calendar entries, or deliverable timestamps | Business use actually occurred | No time-based or third-party evidence of use |

| Business-purpose note | Short note tied to client/project outcome | Why the cost was ordinary and necessary for your business | Vague note like "worked there" with no outcome |

Keep that chain intact from contract to outcome. Your note can stay short, but it should answer four questions every time:

- What happened: "Weekly delivery block and client calls from coworking on 2026-02-14."

- Who it was for: "Client: Northstar Advisory, retainer work."

- Why coworking was necessary: "Needed quiet workspace and meeting room access; home setup not used for client calls that day."

- Where support lives: "Support:

/2026/Expenses/Coworking/ProviderName/2026-02."

If reviewed, you should be producing records you already kept, not creating them after the fact.

Run a monthly capture workflow#

A practical way to keep the file clean is a short monthly pass while the details are still fresh:

- Collect all coworking invoices and matching payment proofs for the month.

- Tag each file consistently, for example:

2026-02 ProviderName Coworking Membership. - Add business context while fresh: what happened, who, why needed, and file path.

- Reconcile each final USD booked amount to saved support.

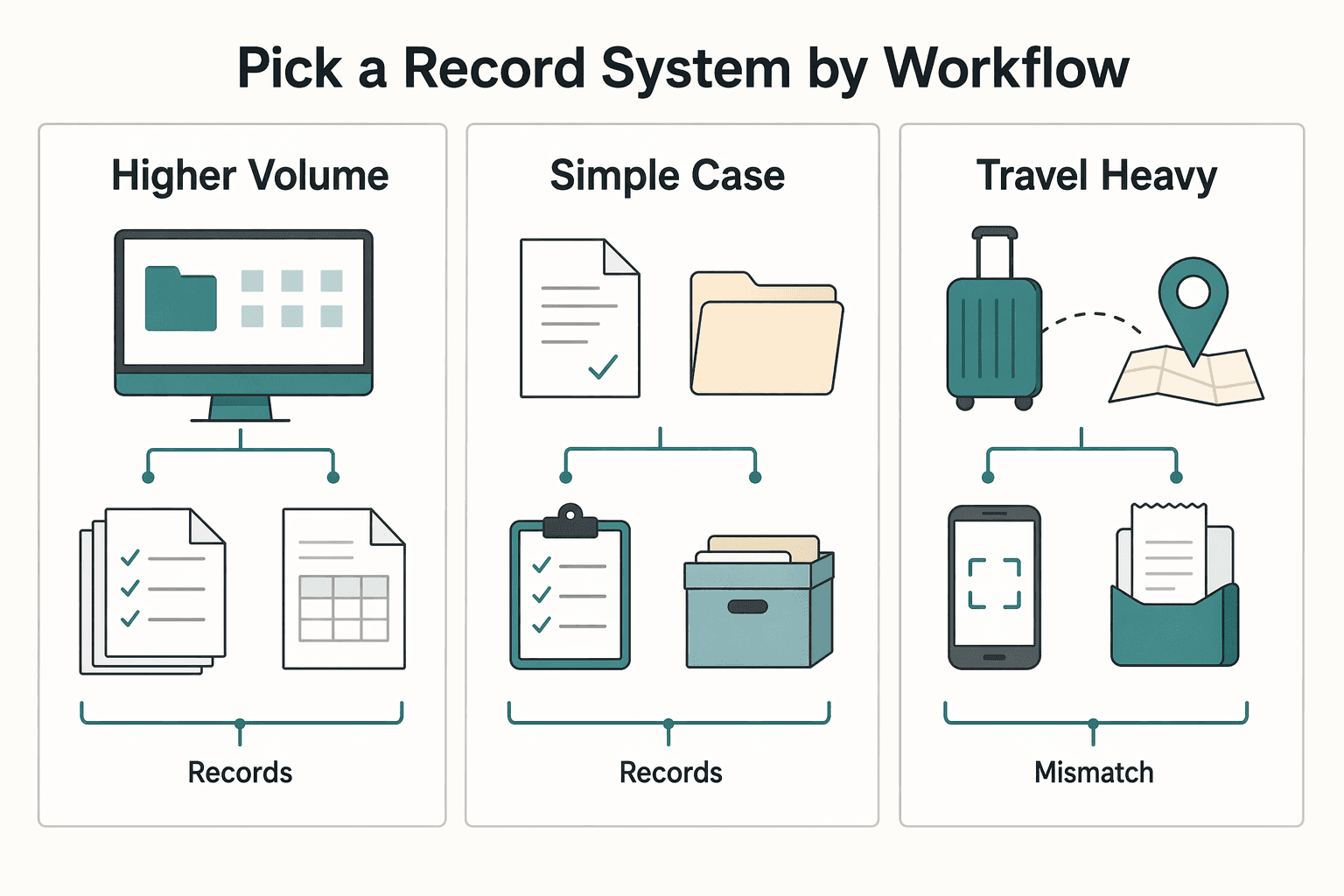

Pick a record system by workflow, not hype#

The best record system is the one you will actually maintain under workload:

| Your profile | Recommended setup | Why it fits | Watch-out |

|---|---|---|---|

| Higher volume, wants automation | Accounting system with receipt attachments | Can make matching faster and reduce manual chasing | Verify each attachment still includes business context |

| Lower volume, comfortable manual controls | Structured cloud folders + consistent naming | Simple and workable when discipline is high | A common breakdown is inconsistent tags and missing notes |

| Travel-heavy workflow | Mobile-first capture + same-day naming and tagging | Can reduce lost receipts and memory gaps | Backfilling later can weaken business-purpose notes |

Electronic records are acceptable if they meet the same standards as paper records.

Add a foreign-membership lane#

Foreign memberships need the same core evidence plus the currency layer. Keep the local-currency invoice, payment proof, and the conversion record used for USD reporting. U.S. return amounts must be in U.S. dollars. There is no single official IRS exchange rate, and posted rates can be used if applied consistently. If multiple rates exist, keep a short note explaining why your chosen rate best matches the payment facts.

Also keep a short invoice-field verification note covering the provider legal name, service period, amount, currency, and any country-specific fields shown on the invoice. Where local requirements are unclear, note that the invoice field needs verification instead of guessing.

Keep records through the applicable period of limitations, commonly 3 years, and longer where specific rules require it.

If a tax authority reviews the deduction#

If this ever gets reviewed, organization matters almost as much as content. Send a packet organized by tax year and expense type. Start with a one-page transaction summary, then provide:

- Summary sheet: each charge, date, payee, amount, and bookkeeping reference

- Contract and then each invoice with matched payment proof

- Usage evidence and business-purpose note for each item

- FX worksheet and saved rate source for foreign charges

If mailing documents, send copies, not originals. Present receipts by date with notes showing what each charge was for and how it relates to your business.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Conclusion: From Anxious Expense to Confident Investment#

Confidence should come from process, not optimism. The sequence is simple: confirm your business purpose, record only the costs and treatment your facts support, and keep a file that can defend your position later. That is the shift from uncertainty to a measured, supportable approach.

You are not documenting a perk or a vague productivity spend. You are documenting how the expense relates to work, and your records should show that story in real time. Keep the agreement or plan confirmation, the invoice, proof of payment, and dated notes or calendar support tied to actual work use.

Use safe defaults. Keep business and personal elements clearly separated in your records. Keep records contemporaneously. If a membership includes nonbusiness value, document that clearly and avoid aggressive interpretations.

For 2026, use actual IRS guidance when you need interpretation, not IRB issue highlights alone. The IRS states those highlights are reader aids and may not be relied on as authoritative interpretations. If an exam becomes technical, Rev. Proc. 2026-2 explains how technical advice memoranda are handled and the rights you have when a field office requests one.

If your facts include cross-border charges, mixed-use treatment, or uncertainty about taxpayer classification, escalate to a tax professional before filing. Otherwise, run the same documentation routine every month so your position is easy to substantiate if reviewed.

This pairs well with our guide on How to Deduct Startup Costs for Your Freelance Business.

If your work and travel pattern changes during the year, use the tax residency tracker so your coworking expense records stay aligned with your broader compliance file.

Frequently Asked Questions

Can I deduct a coworking space if I also have a home office?

Possibly, but treat the home office and coworking space as separate fact patterns. The position is strongest when each location has a distinct business role and your records do not describe both as doing the same job. If your home-office claim depends on admin use, a fixed coworking desk used for substantial admin work can weaken it.

How do I prove my coworking space is for business use?

Build a contemporaneous evidence trail instead of relying on a receipt alone. Keep the membership agreement or invoice, proof of payment, and calendar, booking, or task records that show actual business activity. Short notes tying the expense to client work, meetings, or core admin tasks make the file stronger.

Is a WeWork All Access pass tax deductible for a freelancer?

It depends on actual use, not the brand name. Analyze whether the pass is ordinary, necessary, and tied to real business activity, and separate any personal or perk-like elements. If the treatment is unclear for your facts, confirm it before claiming it.

How do I handle a foreign coworking charge on my U.S. return?

Handle it like any other business-expense claim, but keep a tighter file. Save the local-currency invoice, proof of payment, the conversion method you used to report the amount in USD, and a note showing the business purpose. Use one reasonable FX method consistently and keep income-tax treatment and self-employment-tax treatment separate.

What percentage of my membership can I claim?

Claim only the business-used portion you can support. If the plan includes personal use or bundled benefits, isolate the business portion with a reasonable method and apply it consistently. Do not assume 100% when nonbusiness use exists.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

How to Write Off a Home Office as a Renter

A renter can claim the home office deduction when IRS eligibility tests are met and the business use of the home is clear to document. You are the CEO of a business-of-one, so run this like an operating decision: qualify first, document second, then calculate. If you want a low-friction approach, start with compliance, not aggressive tax savings.