Quick Answer

Yes. You can often deduct education costs as a freelancer when the training maintains or improves skills used in your current business or keeps an existing credential active. Put qualifying expenses on Schedule C, and keep a file with the syllabus, provider description, receipt, and a brief business-purpose note tied to current client work. Do not claim programs that meet minimum entry requirements or qualify you for a new trade, and never double-claim the same expense with the Lifetime Learning Credit.

Don't Just Learn. Invest. A CEO's Guide to Deducting Education Costs.#

Start with this filter: as a freelancer, treat education as deductible only when it is an ordinary and necessary business expense that maintains or improves skills you already use in your current work, or is required to keep your current status or pay. If you cannot clearly connect it to your present trade or business, do not deduct it yet.

The key is business purpose. A course can still be nondeductible if it qualifies you for a new trade or business, or if it is needed to meet minimum entry requirements for your current one. If you are self-employed, qualifying education expenses are generally reported on Schedule C, and you should be ready to substantiate what you claim.

This guide follows the decision order that matters in practice. First comes the qualification test, then documentation, then international and cross-border complications, and finally the deduction-versus-credit choice without double counting the same expense.

| Education scenario | High-level treatment | Why |

|---|---|---|

| Course that sharpens skills used in your current freelance service | Often eligible | Fits the maintains-or-improves-skills test |

| Required continuing education to keep a license or status | Often eligible | Supports keeping your current professional standing |

| Books, supplies, and lab fees tied to qualifying education | Often eligible | Can be part of qualifying education costs |

| Program that qualifies you for a new trade or business | Usually not eligible | New-trade disqualifier |

| Education needed to meet minimum entry requirements | Usually not eligible | Minimum-requirements disqualifier |

| Course with mixed personal and business purpose | Edge case, verify before filing | Business purpose can be harder to prove |

If your situation involves a career pivot, mixed personal and business intent, foreign travel or conventions, or section 911 excluded income, that is usually the point to bring in a tax pro before you file.

You might also find this useful: The Best Ways to Invest in Your Freelance Business.

The CEO's Litmus Test: Does Your Education Qualify as a Business Asset?#

Before you enroll, run a quick screen. If you cannot tie the provider's own course description to work you already sell now, or to a credential you already hold and maintain, pause and treat the expense as high risk.

| Test | Question |

|---|---|

| 1. Current-service link | Does the course clearly improve services you already deliver? |

| 2. Current-credential maintenance | Is it tied to keeping a status, registration, or credential you already rely on? |

| 3. New-business pressure test | Does the program look more like an entry path into a different line of work? |

This is a practical pre-enrollment filter, not a legal ruling. The goal is a clear, defensible business case before you spend.

Sharpen the saw#

Start with provider documents, not memory. Use the course description, subject catalog page, syllabus, module list, and prerequisite language. Before you register, write down the answers to three questions:

- Which current paid service does this improve?

- Which client deliverable changes because of what I will learn?

- Where does the revenue use case show up now: active clients, open proposals, or a service I already market?

If you cannot answer all three cleanly, your linkage is weak. Use the catalog language itself in a simple mapping table:

| Course or program signal | Map to your current business | What to retain | Risk read |

|---|---|---|---|

| Focused advanced module in an area you already sell | Map each module to a current service, deliverable, or client problem | Course description, syllabus, receipt, written module-to-service notes | Lower risk when fit is specific and current |

| Required renewal training tied to an existing credential/status | Link directly to the credential or renewal requirement you already use | Renewal requirement, provider page, registration confirmation, completion proof, payment record | Lower risk when maintenance need is documented |

| Mixed-purpose program (some relevant, some broad) | Separate directly relevant modules from broad career content | Full syllabus, module list, business-use statement, advisor notes | Needs review when linkage is partial |

| Broad introductory or degree-track foundation | Test whether it builds a new capability base versus upgrading a current service line | Catalog page, admissions page, prerequisite chain, program description | Higher risk when it reads like a starting point |

Catalog details can change, so verify you are using the current version and save the version you relied on. University of Baltimore, for example, directs students to MyStudent Center or the Office of Records and Registration at 410.837.4825 for up-to-date course information.

License to operate#

If the training supports a credential or status you already use, keep a tight compliance file alongside your payment records.

Keep the following records:

- Renewal or maintenance requirement

- Course description

- Registration confirmation

- Completion certificate

- Proof of payment

- Any client, portal, or professional-body record showing the status needed to stay active

The point is to show how the training connects to work you already perform.

The new business trap#

The fastest way to misread a program's business fit is to ignore how the program is structured. Foundational language is a warning sign. University of Baltimore describes ACCT 201 as "A complete study of basic financial accounting processes applicable to a service, merchandising, and manufacturing business," which reads as broad foundational training.

Prerequisite chains are another signal. If courses require prior coursework with a minimum grade of C, that can point to a progression path into a field rather than a targeted update inside your current one.

Use this quick comparison:

| Program pattern | Likely read in this screen |

|---|---|

| Advanced, narrow training for services you already sell | More defensible business-link position |

| Credential maintenance for status you already hold | More defensible business-link position |

| Broad introductory sequence with prerequisite ladder | Higher-risk, possible new-lane build |

| Mixed-purpose program with partial overlap | Ambiguous; professional review recommended |

If the result is still unclear after module mapping, prerequisite review, and document collection, pause the decision until your documentation and advisor review support a clear business link.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Building Your 'Audit-Proof' File: A 4-Part Documentation Strategy#

If you want a defensible deduction, build the file before, during, and after the training, not at tax time. The goal is simple: records that support your books and return, especially where estimates are not enough for Section 274 travel-related items.

1. Write a short intent memo before you pay#

Do this before money leaves your account. This is a practical documentation step, not an IRS form requirement. Use a dated memo that explains why the cost belongs in your current business.

| Memo item | What to include |

|---|---|

| Course and provider | Course and provider |

| Business purpose | What current-work skill is being maintained or improved |

| Current service linkage | The existing service, deliverable, or credential it supports |

| Expected client application | How you expect to use it in current client work, active proposals, or services you already market |

| Expected cost categories | Tuition, books, supplies, lab fees, travel |

| Retention location | Exact folder path or bookkeeping attachment location |

If you cannot clearly complete the current-service linkage and expected client application, pause and reassess before spending.

2. Build an evidence binder that supports each claim#

Build a digital, searchable file tied to the transaction it supports.

| Document type | Why it matters | Where to store it | Common gaps to avoid |

|---|---|---|---|

| Provider page, syllabus, module list | Shows what was taught and whether it maps to current work | Course folder saved as PDF or screenshot | Relying on memory after provider pages change |

| Invoice, receipt, payment proof | Supports payee, amount, date, and proof of payment | Attached to bookkeeping entry and stored in the course folder | Keeping only a card statement with no item detail |

| Completion proof, if available | Strengthens proof that training occurred | Course folder | Skipping available completion records |

| Business-use notes | Connects course content to existing client work or services | Dated note in the same folder | Notes that summarize content but not business use |

| Travel records, if relevant | Supports transportation, lodging, and business-purpose elements | Travel subfolder linked to the course file | Mixing personal and business costs without clear separation |

3. Categorize and reconcile every related cost#

Track more than tuition. Qualifying costs can include tuition, books, supplies, lab fees, and certain transportation and travel costs. If you are self-employed, qualifying education expenses are generally reported on Schedule C.

Use consistent categories in your bookkeeping and reconcile each line to source documents. At minimum, each entry should match payee, amount, date, proof of payment, and item or service description. Tag all related course costs so you can pull one complete audit trail. Also make sure the same expense is not used for another education tax benefit for the same student.

4. Flag risk early and retain records for the right window#

Education claims are harder to defend when the facts are mixed and the records are thin.

Review these red flags before you claim:

- Mixed personal and business travel: if the trip is primarily personal, trip costs are nondeductible

- Bundled programs: confirm the education is not part of a program that qualifies you for a new trade or business and is not needed to meet minimum educational requirements for your current trade or business

- Missing proof set: weak or missing support for payment, business purpose, or completion when available

- Bookkeeping disconnect: documents exist, but there is no clean link to the Schedule C entry

Keep records until the applicable IRS limitation period runs out. In many cases that is 3 years, but longer periods can apply, including certain unreported-income situations. If classification is unclear, especially for mixed travel or bundled programs, treat the expense conservatively and consult a tax professional before claiming it.

We covered this in detail in Can I Deduct My Coworking Space Membership?.

If you want a lower-stress compliance workflow year-round, use the Tax Residency Tracker to keep your travel and filing records organized alongside your deduction file.

The Global Professional's Edge: Deducting International Courses and Travel#

International training can still be deductible, but only if it meets the business-education rules and you can support it with records. The core test does not change abroad. The education must maintain or improve skills you already use in your current work, and it is not deductible if it qualifies you for a new trade or business. If you are self-employed, qualifying education expenses are generally reported on Schedule C. In practice, the biggest risk points are travel purpose, currency conversion, and FEIE interaction.

Book the trip around the business purpose#

Treat business purpose as the lead decision, not something you try to justify after the trip. Travel deductibility starts with your tax home, generally the city or area of your main business. If a trip is primarily vacation or investment, the entire trip cost is personal and nondeductible.

Before you book, save the agenda, syllabus, registration details, and a dated calendar that ties the trip timing to your current client work. If the event is a convention outside North America, flag it for extra review because special rules apply.

| Trip component | Usually deductible when | Usually not deductible when | Documentation to keep |

|---|---|---|---|

| Course tuition or registration | The course maintains or improves skills used in your current business | The program qualifies you for a new trade or business | Invoice, syllabus, provider page, Statement of Intent |

| Transportation between tax home and course destination | Trip is primarily for a qualifying business purpose | Trip is primarily vacation or investment | Itinerary, registration proof, agenda, payment records |

| Lodging | Nights directly tied to course or business travel days | Extra personal nights before or after program dates | Hotel folio, dated schedule, calendar notes |

| Local transportation | Trips directly tied to course attendance or business needs | Personal outings or unrelated side trips | Receipts, ride logs, dated business schedule |

| Meals during business travel | Business-travel meals, generally subject to the 50% limit | Personal-day meals | Meal records showing time, place, business purpose |

For mixed-purpose itineraries, separate business and personal components in your records instead of trying to reconstruct intent later.

Convert foreign currency the same way every time#

Consistency matters more than cleverness here. Your U.S. return is in U.S. dollars, and if your functional currency is USD, you translate foreign-currency items using the rate when you pay, receive, or accrue the item.

Use this routine:

- Choose one posted exchange-rate source and use it consistently.

- At payment time, keep the original-currency invoice and capture rate evidence for that date.

- Record the USD amount in bookkeeping and attach payment proof plus conversion support to the same entry.

Your file is stronger when each entry shows original amount, currency, date, rate source, USD amount, payee, and business purpose.

FEIE changes the economics, not the qualification test#

FEIE can change the tax value of the deduction, but it does not change whether the education itself qualifies. To claim FEIE, you need foreign earned income, a foreign tax home, and a qualifying residence or presence test. Under the physical presence test, the benchmark is at least 330 full days in a 12-month period.

| FEIE point | Article detail |

|---|---|

| Basic requirements | Foreign earned income, a foreign tax home, and a qualifying residence or presence test |

| Physical presence test | At least 330 full days in a 12-month period |

| 2026 maximum exclusion | $132,900 per person |

| Regular income tax effect | FEIE reduces regular income tax |

| Self-employment tax effect | FEIE does not reduce self-employment tax |

| Exclusion computation | Reduced by related expenses plus the deduction for half of self-employment tax |

For tax year 2026, the maximum exclusion is $132,900 per person, so re-check the current amount for later filing years.

For self-employed taxpayers, FEIE reduces regular income tax but does not reduce self-employment tax. The exclusion computation is reduced by related expenses plus the deduction for half of self-employment tax. So if most of your income is already excluded, do not assume the education deduction creates a full additional U.S. tax benefit.

When to involve a tax pro#

Some international fact patterns are still manageable on your own. Others are not. Bring in a tax pro before you file if your trip spans multiple countries, business intent is only partial, FEIE allocation is unclear, or your records are inconsistent. Also escalate when conventions outside North America or tax-home changes create classification uncertainty.

Bring one clean packet: itinerary, agenda or syllabus, receipts, currency-conversion support, tax-home explanation, and your draft FEIE math.

Related: How to Handle Taxes for a Side Hustle.

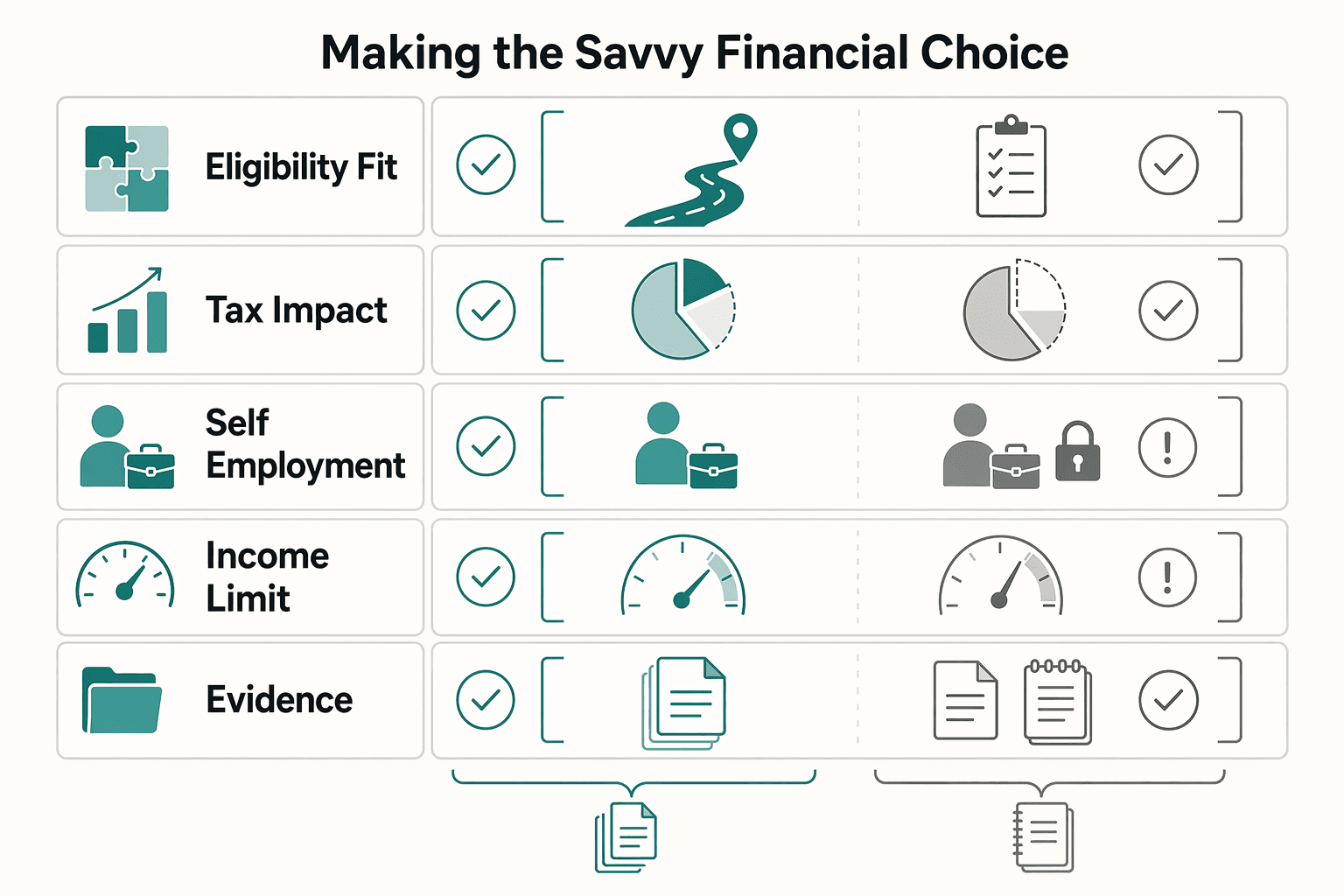

Deduction vs. Credit: Making the Savvy Financial Choice#

Make this choice by math, not instinct: for the same qualifying education expense, you generally choose either a Schedule C deduction or the Lifetime Learning Credit, not both.

Before you compare outcomes, make sure the expense is in the right lane. A cost can be treated as work-related education on Schedule C, while the credit has its own eligibility rules for qualified tuition and related expenses, the student, and the institution.

| Decision point | Schedule C deduction | Lifetime Learning Credit |

|---|---|---|

| Eligibility fit | You are self-employed, and the education qualifies as a deductible business expense | You meet the credit's rules for the student, institution, and qualified tuition or related expenses; job-skill courses can qualify |

| Tax impact type | Reduces business income and taxable income | Reduces tax owed directly; nonrefundable |

| Self-employment tax effect | Yes. Lower net earnings can reduce Schedule SE tax | No. It does not reduce self-employment tax |

| Income-limit sensitivity | Not tied to LLC MAGI phaseout rules | Subject to MAGI limits |

| Documentation burden | Business-purpose file, syllabus, receipts, payment proof, Schedule C support | Form 8863 support, institution records, qualified-expense support, and typically Form 1098-T |

Use a four-step decision check#

- Confirm the education qualifies first. If it is not a qualifying education expense for the treatment you want to claim, stop.

- Check whether the credit is actually available. Verify the institution, student, and records needed for Form 8863 before you model it.

- Model the full Schedule C effect. Deductible education goes on Schedule C, and Schedule SE is based on net earnings, so a deduction can affect both income tax and self-employment tax.

- Pick the lower total tax result. Run two clean versions, one using Schedule C treatment and one using the credit, then compare total federal tax due.

Where freelancers misread this choice#

The most common mistake is comparing only the credit amount and ignoring self-employment tax. Credits reduce tax owed, but a Schedule C deduction can also reduce the net earnings used for Schedule SE.

The other mistake is double counting. Keep one expense set for the deduction scenario and a separate set for the credit scenario so the same invoice is not used twice.

If you use FEIE, add a review step#

If you exclude foreign earned income, allocable expenses can change this comparison. Deductions generally cannot be taken against excluded income, and the exclusion math can be reduced by pro rata expenses and related deductions.

If your FEIE allocation is close or unclear, treat this as a professional-review case before you file.

For a step-by-step walkthrough, see Can I Deduct My Cell Phone Bill as a Freelancer?.

Conclusion: Your Expertise is Your Most Defensible Asset#

The cleanest way to handle education costs is to treat them like a business decision before tax season, not a cleanup project after the fact. The core test is straightforward: if the training maintains or improves skills you use in your current work, and it does not qualify you for a new trade or business, it may be deductible. Use this sequence and apply it consistently:

- Qualify the expense. Match the course content to the services you already sell. If it is really retraining for a different field, stop.

- Document business purpose and evidence. Keep the course description or syllabus, invoice, proof of payment, and completion record. You carry the burden of proof, so your records need to support what you report.

- Choose one claim path. If you are self-employed, qualifying education expenses go on Schedule C (Form 1040). If a credit is also available, compare outcomes and use only one education benefit for the same student and the same expense.

For globally mobile freelancers, the main controls stay the same: clear business-purpose linkage, complete records, and consistency across filings. If you paid in foreign currency, keep the payment date and the exchange rate you used so your U.S. dollar reporting is defensible. If you live abroad, you are still working inside the same U.S. income tax framework.

When the facts are mixed, pause the claim, check current IRS forms and instructions, and escalate to a qualified tax professional. The practical default for next cycle is simple: set up your documentation before purchase so every course starts with a defensible business case.

This pairs well with our guide on Can You Deduct Health Insurance Premiums as a Freelancer?.

If you want a cleaner operating setup for getting paid globally with traceable records, explore Merchant of Record for Freelancers and confirm coverage for your market.

Frequently Asked Questions

How do I prove the course was for my current business?

Show a clear link between the course content and the services you already sell. Keep the syllabus or course description, the receipt, and a short written note that maps key modules to current client work or skills you use now. If your file only says "career growth," tighten it before filing so it shows skill maintenance or improvement in your present business.

Is a master's degree, certificate program, or MBA deductible?

It is deductible only if it does not meet minimum entry requirements for your current trade or business and does not qualify you for a new trade or business. Programs that look like a career pivot are often higher-risk cases, even when some classes help your current work. If the facts are mixed, treat it as a review-with-a-pro situation before you claim it.

Can I deduct an online course or workshop?

Potentially. Deductibility is based on whether the education maintains or improves skills used in your current business and fits the ordinary-and-necessary business-expense standard, not just on delivery format. Keep the course page, syllabus, invoice, and completion record, then add a one-paragraph business-purpose note tied to current client services.

Should I take the Schedule C deduction or the Lifetime Learning Credit?

Use a side-by-side comparison and choose the option that lowers total federal tax. Do not use the same expense for both, because the same student expense cannot be claimed for multiple education benefits. The sequence is simple: confirm the expense qualifies for Schedule C, confirm current credit eligibility and filing requirements if relevant, then run both scenarios and keep one.

What records should I keep if I claim education costs?

Keep records that show payee, amount, date, and proof of payment, plus your business-purpose file with the course description, syllabus, and completion proof. If you claim related books, supplies, or similar items, keep those invoices too. For travel-related claims, keep stronger substantiation, including agenda details and travel receipts.

Are conferences and in-person events deductible?

They can be deductible when the event supports your current business and you can substantiate that connection. Registration alone may not be enough to substantiate business purpose. Keep the agenda, session descriptions, receipts, and a short note explaining how the event maintained or improved current skills. If the event is mainly broad networking, inspiration, or a move into a new trade, your position is much weaker.

What about subscriptions to journals, research services, or learning platforms?

These may qualify when they are directly tied to current services and are ordinary and necessary for your business. Keep billing records and a short note explaining how the subscription supports current client work. If the real purpose is retraining for a different field, do not treat it as routine skill maintenance.

I live abroad. How do FEIE and foreign-currency payments affect this?

If you claim FEIE, excluded foreign earned income reduces regular income tax but does not reduce self-employment tax. You generally cannot take deductions against excluded income, and if only part of foreign income is excluded, you cannot claim a credit or deduction for foreign taxes allocable to that excluded income. For foreign-currency payments, report in U.S. dollars using the spot rate on the payment date, or another posted rate used consistently, and keep the invoice, rate source, date, and payment proof.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

Invest in Your Freelance Business by Protecting Cashflow First

Start with payment reliability before you buy another growth tool. Courses, coaching, and software can help delivery, but they do not protect cashflow when payment is delayed, disputed, or never sent. A practical move is to make each engagement payable, traceable, and harder to derail from kickoff to settlement.