Quick Answer

Start with the BVI Business Companies Act as the baseline for bvi corporate law, then pause execution until your registered agent and local counsel confirm current filing duties. The article stresses preparing a single evidence pack, reconciling ownership and director data across drafts, and using explicit go/pause gates when timelines, exemptions, or penalty mechanics are unresolved.

What this article will help you do#

Decide quickly whether a BVI company fits your goals, then execute with fewer surprises. You will leave with a working baseline, a list of unknowns to confirm, and a practical set of next steps for your registered agent and counsel.

Use these points as planning anchors. The BVI Business Companies Act is described as the core statute for BVI business companies. Practitioner commentary describes the Act as enacted in 2004 and fully in effect from 1 January 2007. Incorporation is described as filing the memorandum and articles with the Registrar of Corporate Affairs. A registered agent and registered office in BVI are also described as required.

Do not treat summary material as enough for final execution. Exact duties, timelines, penalties, exemptions, and filing mechanics under current BVI law and related instruments still need current legal confirmation for your facts.

| Clearly known now | Needs confirmation before you act |

|---|---|

| The main company law statute is the BVI Business Companies Act. | Which current provisions and updates apply to your company today. |

| Incorporation filings are made with the Registrar of Corporate Affairs using memorandum and articles. | Exact filing timelines, fees, and penalty mechanics for your company type. |

| A registered agent and registered office in BVI are required. | How nominee, ownership, or director arrangements change your filing set and timing. |

| One secondary guide says no BVI resident director is required. | Whether regulated activity or edge-case facts change that position. |

Speed claims should stay in the planning column. References to incorporation within 24 hours can describe a typical case, but they are not a promise. Treat timing as a planning assumption until your agent confirms document readiness, name checks, and filing queue conditions.

A useful first move is to prepare your adviser handoff pack before you ask legal questions. When we send counsel and the agent complete facts in one pass, review quality usually improves and rework drops. When facts arrive in fragments, legal answers often come back with caveats and may require another cycle.

Use this checklist before you commit:

- Build one evidence pack with draft memorandum, draft articles, legal names, ownership percentages, and proposed directors.

- Ask your registered agent for a written split of preparation, review, submission, and required inputs.

- Ask local counsel to tag each high impact item as confirmed now or pending confirmation.

- Reconcile names, percentages, and director details across every draft before filing.

- Set a go or pause gate: if ownership, control, or filing responsibility is unclear, pause.

Build the legal mental model before you pick a structure#

In this analysis, once your baseline is clear, map the legal stack before choosing structure. We recommend labeling each key point as confirmed or pending legal confirmation so decisions are tied to evidence, not memory.

Start with the core company law text, then layer amendments, regulations, and institutional touchpoints. Commentary describes offshore law as flexible and often not tied to audited account requirements. The same commentary also describes pressure for economic substance measures and better access to beneficial ownership information. That combination creates a practical tradeoff: flexibility on setup, higher expectations on documentation quality.

Legal change pace matters as much as legal content. A Governor's Office speech released on 13 January 2026 reported 25 bills in the prior session, with 21 passed and 18 assented. The speech also named the BVI Business Companies and Limited Partnerships (Beneficial Ownership) (Amendment) Regulations, 2025 among measures debated and passed. Use that signal to date-stamp assumptions and refresh them regularly.

| Layer in your one-page map | Why it matters for decisions | What still needs confirmation |

|---|---|---|

| Base company law text | Anchors structure and governance choices | Which provisions apply to your facts now |

| Amendments and regulations | Highlights where obligations may have shifted | Current triggers, mechanics, and filing impact |

| Institutions and filing steps | Clarifies where oversight and filings sit | Exact role split for your entity type and activity |

| Adviser interpretation | Translates legal text into execution steps | Whether advice is current and complete |

| Your facts and draft documents | Connects law to ownership and control reality | Any mismatch between documents and assumptions |

If your plan touches insolvency risk or regulated investment activity, treat that as an immediate counsel review trigger.

However, a practical way to keep this map useful is to tie each line item to one owner and one next review date. Without ownership, the map becomes a static note. With ownership, it becomes a live decision tool your team can update before each filing or structural change.

Practical next step:

- Build a one-page authority map with a date and owner for each layer.

- Tag each high impact point as confirmed in current text or pending legal confirmation.

- Get written confirmation from your service provider and counsel on role and filing assumptions.

- Reconcile memorandum, articles, and ownership facts against the map before filing.

If you are also weighing freelancer tax structure decisions, this companion article can help frame that part of the choice: A Guide to Italy's 'Regime Forfettario' for Freelancers.

What changed and why this is not just a Revised 2020 story#

Revised 2020 is a baseline, not the full operating picture. Later changes affect recurring compliance work, so older summaries can mislead if you use them as filing instructions.

A clear example in the draft record is the amendment package described as effective on 1 January 2023 under the BVI Business Companies Act. The excerpts point to added reporting requirements and updated dissolution and reinstatement mechanics for struck off entities. In practice, this shifts attention from one-time setup to ongoing compliance discipline.

| Practical change described in the draft | Day to day impact | Verify before acting |

|---|---|---|

| Companies must prepare an annual return. | Recurring reporting becomes a scheduled obligation. | Confirm fiscal year end and return owner. |

| The return is submitted to the registered agent within nine months after year end. | Deadline management becomes a core control point. | Set dated reminders and accountability now. |

| Annual returns are not public, and there is no default requirement for the agent to file them with the Corporate Registry. | Privacy can remain, but preparation responsibility stays with the company. | Get written confirmation of delivery and storage. |

| Records must be kept for five years, even if not audited or filed with a BVI authority. | Missing records can stall later reviews or transactions. | Keep a dated archive and retention log. |

| Current director names are described as publicly searchable, while former directors are described as private. | Governance visibility expectations change over time. | Recheck director records before appointments or changes. |

That is why this is not only a Revised 2020 story. Later instruments belong on your verification list before execution, including the BVI Business Companies (Amendment) Act, 2024 and the BVI Business Companies (Amendment of Schedules) Order, 2025. This section does not establish their detailed mechanics.

The operational pressure point is coordination, not legal theory. Annual returns, record retention, and director visibility can all be handled well when ownership is explicit. They become risky when nobody owns the calendar, evidence archive, or escalation call.

Use this checkpoint before your next filing cycle:

- Build a dated amendment tracker starting at 1 January 2023.

- Assign one owner for annual return preparation, one for delivery to the registered agent, and one for five-year retention.

- Ask counsel to mark what is confirmed now and what remains pending review for 2024 and 2025 instruments.

- Pause if any step still depends on a pre-2023 checklist or undated summary.

If you want a deeper dive, read What is FinCEN? A Guide for Freelancers and FinTech Users.

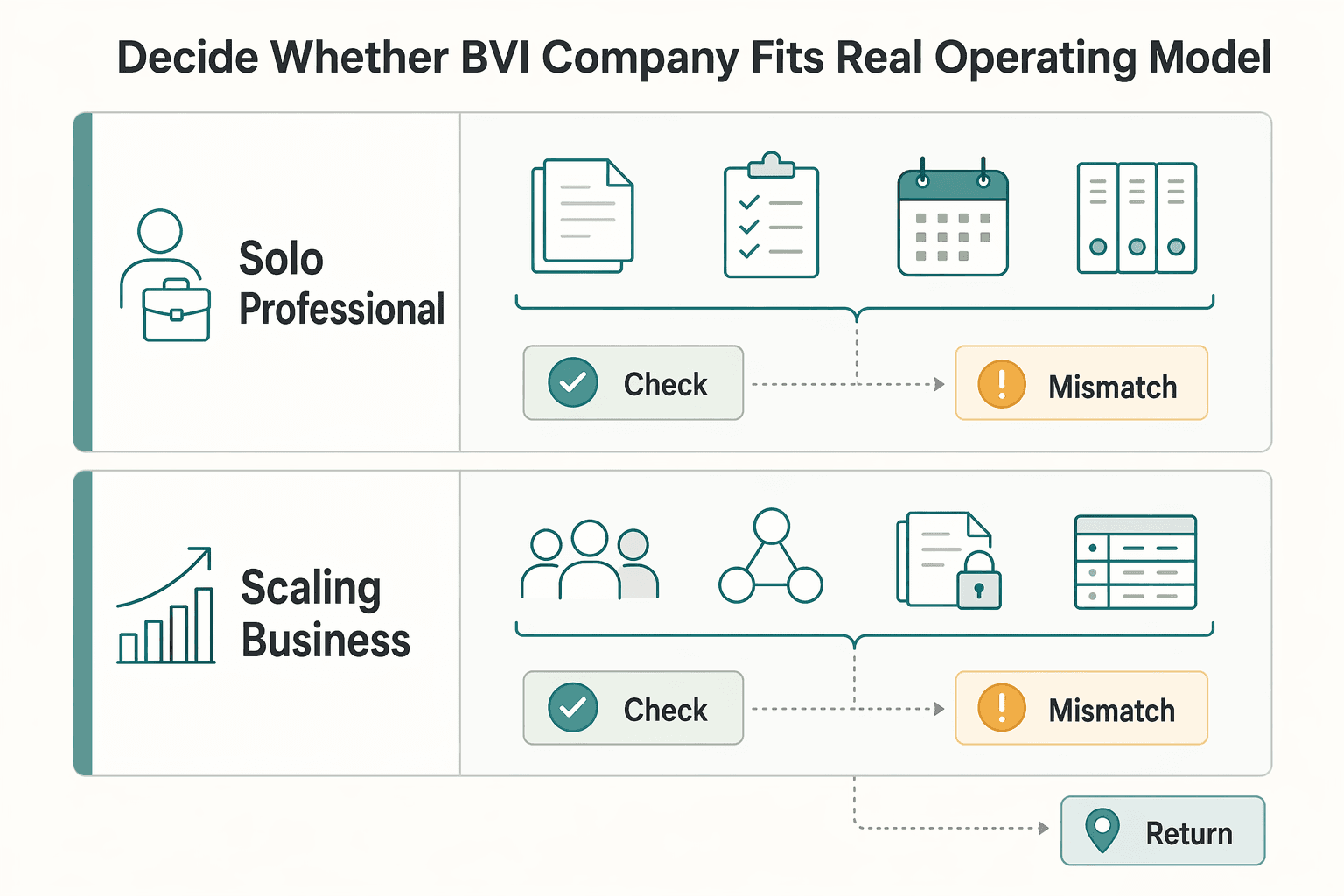

Decide whether a BVI company fits your real operating model#

Use this decision rule first: if your operating model can support ongoing compliance and filing workflows, a BVI company may fit. If minimal admin is your top priority, compare structure alternatives before you commit.

Structure should match operating reality. A solo practice with few contracts and rare ownership changes can be simpler to manage than a scaling business with investors, multiple counterparties, and frequent governance updates.

| Operating pattern | Fit signal | Main pressure point |

|---|---|---|

| Solo professional with few contracts | Fewer moving parts to coordinate | Compliance ownership can drift |

| Scaling business with investors and multiple counterparties | Formal governance can support complexity | More change events require tighter record discipline |

Use reporting obligations as a realism check. Where BVIFARS applies, recurring tasks can include updating reporting obligations after enrolment, creating Change of Reporting Obligations filings, submitting US FATCA data, and creating CRS filings. It can also include viewing submitted filings. That is ongoing work, not one-time setup.

Coordination across your team and service providers can be a real constraint, so assign responsibilities early. Decide who prepares data, who validates it, who confirms submissions, and where evidence is stored for fast retrieval.

A simple scenario contrast helps. If you expect one owner, low transaction volume, and rare structure changes, control effort is usually more predictable. If you expect investor updates, director changes, and more counterparties, the same structure can still work, but document discipline and review cadence usually need to be stronger from day one.

Do not proceed yet if any of these remain unresolved:

- Business purpose is still unclear.

- Ownership or control map is incomplete.

- Responsibility across your team and service providers is not explicitly assigned.

- You cannot confirm whether BVIFARS-related filings apply.

If you are still at structure stage, compare this decision against Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers before committing.

Use an authority hierarchy so you do not over-trust summaries#

Execution quality depends on source order: primary law text first, regulator materials second, commentary third. That order helps prevent polished summaries from driving legal decisions.

For this section, anchor the top tier on primary company-law text, including the BVI Business Companies Act (Revised 2020) and related beneficial ownership regulations. Exemptions, penalties, and filing mechanics should be confirmed against the operative statutory text before relying on summaries.

Use British Virgin Islands Financial Services Commission guidance as support, not replacement. The beneficial ownership AML guidelines are dated December 2024 and include sections on identifying beneficial owners, verifying beneficial owners, and failure to comply with obligations. That helps with verification discipline, while final obligations still need confirmation in current primary materials.

Treat references to the Law Revision Act 2014 as reading context, not proof that obligations are unchanged, because the operative provisions are not excerpted here. Amendment tracking protects execution accuracy.

| Decision area | Known from current excerpts | Unknown until primary text review |

|---|---|---|

| Exemptions | FSC guidance addresses beneficial ownership identification in an AML context | Which company law exemptions apply to your entity and ownership facts |

| Penalties | The guidelines include a non-compliance section | Exact penalty triggers, amounts, and relief under current company legislation |

| Procedural mechanics | Guidance indicates what to identify and verify | Exact filing steps, forms, and timing under current law |

A VISTA trust FAQ published on 27 March 2025 notes that VISTA is restricted to shares in BVI companies. That can inform trust planning, but it remains commentary rather than binding company law authority for filing decisions.

When summaries conflict, preserve momentum by documenting why you trust one source over another. A short note with source type, publication date, and unresolved points gives counsel a fast way to validate your logic and keeps your team aligned during review.

Use one pre-execution checkpoint:

- Build an obligation register with three labels: primary text confirmed, FSC guidance aligned, commentary only.

- Date-stamp each item with version or publication date, including December 2024 guidance where relevant.

- Pause any item labeled commentary only until primary text confirmation is complete.

Incorporation and governance records to set up correctly on day one#

Set up one clean record pack before filing and prioritize consistency over speed. Even if a provider says registration can happen in 1 to 2 days, pause if core details do not match across documents.

| Record | What it should show |

|---|---|

| Final legal name sheet | Identical spelling, capitalization, and suffix across all documents |

| Ownership and control sheet | Consistent names and percentages |

| Shareholder and director appointment records | Recorded and date-stamped |

| Internal approval note | Who reviewed incorporation data and when |

| Dated submission pack | Sent to the registered agent |

| Certificate of Incorporation | Stored with the approved submission pack |

| Change log | Post-submission edits with reason and approver |

Your day-one pack can include core governing records, ownership and control records, shareholder and director appointment records, and internal approvals. Date-stamp each version so changes are visible and traceable.

Define the filing process in writing from the start. A local registered agent is described as required. Incorporation is described as filing through a licensed registered agent, appointing shareholders and directors, and obtaining a Certificate of Incorporation. Because these are secondary sources, confirm current requirements with official BVI sources before acting. Document who prepares data, who approves it, and who submits.

Use this first-week checklist:

- Final legal name sheet with identical spelling, capitalization, and suffix across all documents.

- Ownership and control sheet with consistent names and percentages.

- Shareholder and director appointment records recorded and date-stamped.

- Internal approval note showing who reviewed incorporation data and when.

- Dated submission pack sent to the registered agent.

- Certificate of Incorporation stored with the approved submission pack.

- Change log for post-submission edits with reason and approver.

Run one reconciliation check before submission and one after the certificate is issued. If name, ownership details, or appointment records differ anywhere, correct the full set instead of patching one file. This helps reduce drift between internal records and filed records.

One practical control is to keep a single master data sheet for legal name, ownership percentages, and director details, then pull every form from that sheet. This can reduce copy-paste errors and make final review faster for both your internal reviewer and your registered agent.

Filing obligations that now create the biggest execution risk#

The biggest risk here is acting on assumptions that are not yet verified. For this section, the evidence pack does not include authoritative BVI rule text on register visibility, nominee-related disclosure triggers, or professional director update triggers.

| Step | Action | Detail |

|---|---|---|

| 1 | Confirm current entity data | Use the approved internal pack, including legal names, ownership splits, and current directors |

| 2 | Validate the ownership and control map | Check it against internal approvals |

| 3 | Draft filing instructions | Mark each legal point as confirmed or pending |

| 4 | Clear pending legal points | Do this with your registered agent and counsel before submission |

| 5 | Submit and archive an evidence bundle | Keep the final data sheet, approvals, submission copy, and acknowledgments |

| 6 | Schedule reconciliation checks | Use event-driven and periodic checks |

Treat register of members visibility as unresolved until you confirm current requirements through official channels, your registered agent, and counsel. Do not assume one visibility treatment is correct for every fact pattern.

Apply the same approach to nominee shareholders and professional directors. If ownership rights, control rights, nominee arrangements, or director status change, require a written decision note before filing. That note should record what changed, what interpretation was used, who approved it, and which records or filings are being updated.

Use this order of operations:

- Confirm current entity data from the approved internal pack, including legal names, ownership splits, and current directors.

- Validate the ownership and control map against internal approvals.

- Draft filing instructions and mark each legal point as confirmed or pending.

- Clear pending legal points with your registered agent and counsel before submission.

- Submit, then archive an evidence bundle with final data sheet, approvals, submission copy, and acknowledgments.

- Schedule event-driven and periodic reconciliation checks.

Some in-scope materials for this section are commentary or non-BVI materials, so they do not establish reliable BVI filing obligations. Keep unresolved points marked as unresolved until verified.

A useful discipline is to treat pending legal points as blockers, not reminders. If a point is pending, it should stop submission until cleared. That rule prevents last-minute assumptions from slipping into filed data.

Beneficial ownership disclosures without avoidable errors#

Treat beneficial ownership as a verification task, not a box-ticking task, to reduce avoidable errors.

In practice, this means identifying the real owner behind formal or nominee holders and documenting who actually controls or benefits from the company. Keep that lens when you review the BVI Business Companies and Limited Partnerships (Beneficial Ownership) Regulations, 2024.

Also account for the BVI Business Companies and Limited Partnerships (Beneficial Ownership) (Amendment) (No. 2) Regulations, 2025. From this evidence pack, the safe conclusion is narrow: a later amendment is referenced, but its exact operational impact still needs legal confirmation before filing.

Do not infer BVI access rules from cross-jurisdiction comparisons. Background material notes that some British Overseas Territories favor authority-only access models, and that public-access models exist in other jurisdictions. It also notes that public access alone is rarely treated as the final policy goal. Use that only as context, then confirm current BVI requirements in current legal text and adviser guidance.

Use this caution rule: if ownership or control is layered, nominee-based, or unclear, escalate to counsel before finalizing filing instructions. Then run one reconciliation checkpoint before each submission or update:

- Match names and entity details across company records, draft filings, and adviser instructions.

- Reconcile ownership and control descriptions so they tell one story.

- Keep nominee treatment consistent across records and filing data.

- Record approver, decision date, and final ownership position.

- Archive an evidence bundle with reconciled ownership trail, submission copy, and acknowledgment trail.

If review pressure rises near a filing date, keep the same standard. Speed should change sequencing, not quality thresholds. A complete ownership trail and a written legal position are a prudent minimum package before you file.

Your first-year compliance checklist for fewer surprises#

Use a fixed review cadence in year one to keep records, filings, and adviser instructions aligned.

| Cadence | Actions |

|---|---|

| Month 1 | Complete core records, assign a filing owner, confirm who prepares, reviews, and submits each item with the registered agent, and build one tracker for expected submissions and related internal approvals |

| Quarterly | Review any changes in ownership, control, or governance; if anything changed, reconcile internal records first, then update filing instructions so records stay consistent |

| Event-driven | Treat material ownership or control changes as priority review triggers; if facts are layered or disputed, escalate to counsel and your registered agent before submitting updates |

| Annual | Reconfirm current BVI requirements with counsel and your registered agent, then refresh checklist items and templates |

Treat this as an operating checklist, not a statement of statutory deadlines. What is supported here is high-level governance, such as maintaining a registered agent and registered office, not exact filing clocks, fees, or penalties. Confirm legal timing with counsel and your registered agent.

- Month 1: Complete core records, assign a filing owner, and confirm who prepares, reviews, and submits each item with the registered agent. Build one tracker for expected submissions and related internal approvals.

- Quarterly: Review any changes in ownership, control, or governance. If anything changed, reconcile internal records first, then update filing instructions so records stay consistent.

- Event-driven: Treat material ownership or control changes as priority review triggers. If facts are layered or disputed, escalate to counsel and your registered agent before submitting updates.

- Annual: Reconfirm current BVI requirements with counsel and your registered agent, then refresh checklist items and templates.

Add one handoff step after each review cycle: confirm that the next reviewer can trace decisions without asking for verbal context. If the trail is not clear from documents alone, tighten the record before the next cycle begins.

Watch for version drift between internal ownership records and filing instructions. If a reviewer cannot trace a change quickly from approval to filing pack, pause new submissions and reconcile before proceeding.

Red flags that should trigger immediate legal review#

Get legal review immediately when control or ownership cannot be explained clearly and documented consistently.

Escalate the same day if any of these appear:

- You cannot clearly explain who controls the company under beneficial ownership and control requirements.

- Internal ownership and control records conflict with other company records.

- You changed ownership or control arrangements without assessing legal and compliance consequences.

- You are relying on outdated guidance without confirming current BVI requirements.

Use documents, not recollection, to resolve issues. Section 98 of the BVI Business Companies Act 2004 is described as requiring records sufficient to show and explain transactions and determine financial position with reasonable accuracy. If records are not kept at the registered agent's office, the location must be given to the registered agent. Records and underlying documentation are also described as needing retention for at least five years.

When escalation starts, send one short issue packet: what changed, which records conflict, what action is pending, and what legal point is unresolved. A tight packet helps counsel and the agent respond quickly and reduces back-and-forth.

If records, approvals, and submission instructions do not tell one ownership story, pause updates and reconcile one master record before any new submission.

What to do next to stay compliant and move confidently#

Before any filing, ownership change, or restructuring step, require two things: current official legal text and written professional confirmation tied to your facts.

Use source quality as your first filter. One source in this section states it is not an official legal edition and should be verified against an official edition. Another is clearly a blog post. Commentary can help frame questions but does not, on its own, establish specific BVI company-law requirements. Final action should rely on official materials and adviser confirmation.

Use this pre-change sequence:

- State the exact decision and intended effective date in one line.

- Label each reference by type: official legal text, regulator material, adviser note, or blog.

- Build a short evidence pack with rule text, your interpretation, open questions, and owners.

- Send the pack to your counsel and relevant professional advisers for written confirmation before submission.

- If any critical point is unclear or unsupported, pause and escalate.

Then lock in cadence. Run your checklist now, and repeat this verification routine before each business change so records, adviser instructions, and planned filings stay aligned. Consistency over time is what turns this from a one-off project into dependable compliance practice.

Frequently Asked Questions

What is the main law governing companies in the British Virgin Islands?

The Financial Services Commission Act, 2001 established the BVI Financial Services Commission as an autonomous regulator. For the current primary companies legislation, amendments, and regulations, verify with local counsel.

What changed in BVI company filing expectations?

Current practitioner guidance describes a core filing set with the Registrar of Corporate Affairs: register of directors, register of members, and register of beneficial owners. That means legacy checklists can miss active filing expectations. Refresh older templates before reuse.

Is the register of members public in BVI?

Do not treat this as a simple yes or no based on short summaries. A 2021 fact sheet says director and shareholder details are not publicly available, but that older statement does not settle current register access after later changes. Confirm current position with your registered agent and local counsel before making disclosure commitments.

What new filings involve nominee shareholders and professional directors?

Exact filing triggers tied to nominee shareholders or professional directors should be confirmed with local counsel. Director, member, and beneficial owner registers are core filings. Treat any change in those roles as a legal review checkpoint before instructions are submitted.

How does the beneficial ownership regime affect a small professional business?

Small size does not remove the need for a clear ownership and control record. Internal records, beneficial ownership data, and registered agent records should align. If they do not align, resolve that before filing.

What is still unclear unless you read the full Act and regulations?

Short briefings still leave open points such as current register access rules, exact role-based filing triggers, and current strike-off timelines. Older guidance notes that strike-off can stop a company from carrying on business, so timeline accuracy matters. Verify these points in current legal text and adviser guidance.

How can I verify obligations safely when summaries conflict?

Use a three-step check: validate the claim against current legal text, reconcile it with your registered agent's filing view, and get written legal confirmation where ownership or control is disputed. Store that confirmation with core records. This keeps future reviews evidence based rather than memory based.

What should I do if my team disagrees on interpretation before a filing deadline?

Treat disagreement as a legal risk signal, not a drafting detail. Pause submission, document both interpretations, and request one written position from counsel and your registered agent that states the basis for action. File only after that position aligns with your internal records and filing instructions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- federalregister.gov/documents/2020/02/28/2020-02707/prohibitions...trusted

- sec.gov/files/rules/proposed/2020/bhca-8.pdftrusted

- sec.gov/Archives/edgar/data/2039384/0001493152240412...trusted

- bvifars.vgexternal

- bvifsc.vgexternal

- gov.uk/government/publications/money-laundering-und...external

- onealwebster.com/wp-content/uploads/2022/02/An-Overview-of-Tr...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

What Is FinCEN for Freelancers and FinTech Users

If you are asking **what is fincen**, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.

Italy Regime Forfettario for Freelancers: Eligibility, Red Flags, and Monthly Checks

Start with a simple go-or-no-go call. If your facts fit the eligibility rules, `Regime Forfettario` can be a simpler way to manage freelance compliance in Italy. Then protect that decision with regular checks so your setup stays aligned as your facts change.