Quick Answer

Freelancers outgrow spreadsheets when weekly bookkeeping is still manual and they need reliable control over residency tracking, cross-border invoicing, foreign-account reporting, and cash planning. An AI virtual CFO layer builds on automated bookkeeping by adding alerts, evidence, and forecasting. If your business is domestic-only and single-currency, standard bookkeeping may still be enough.

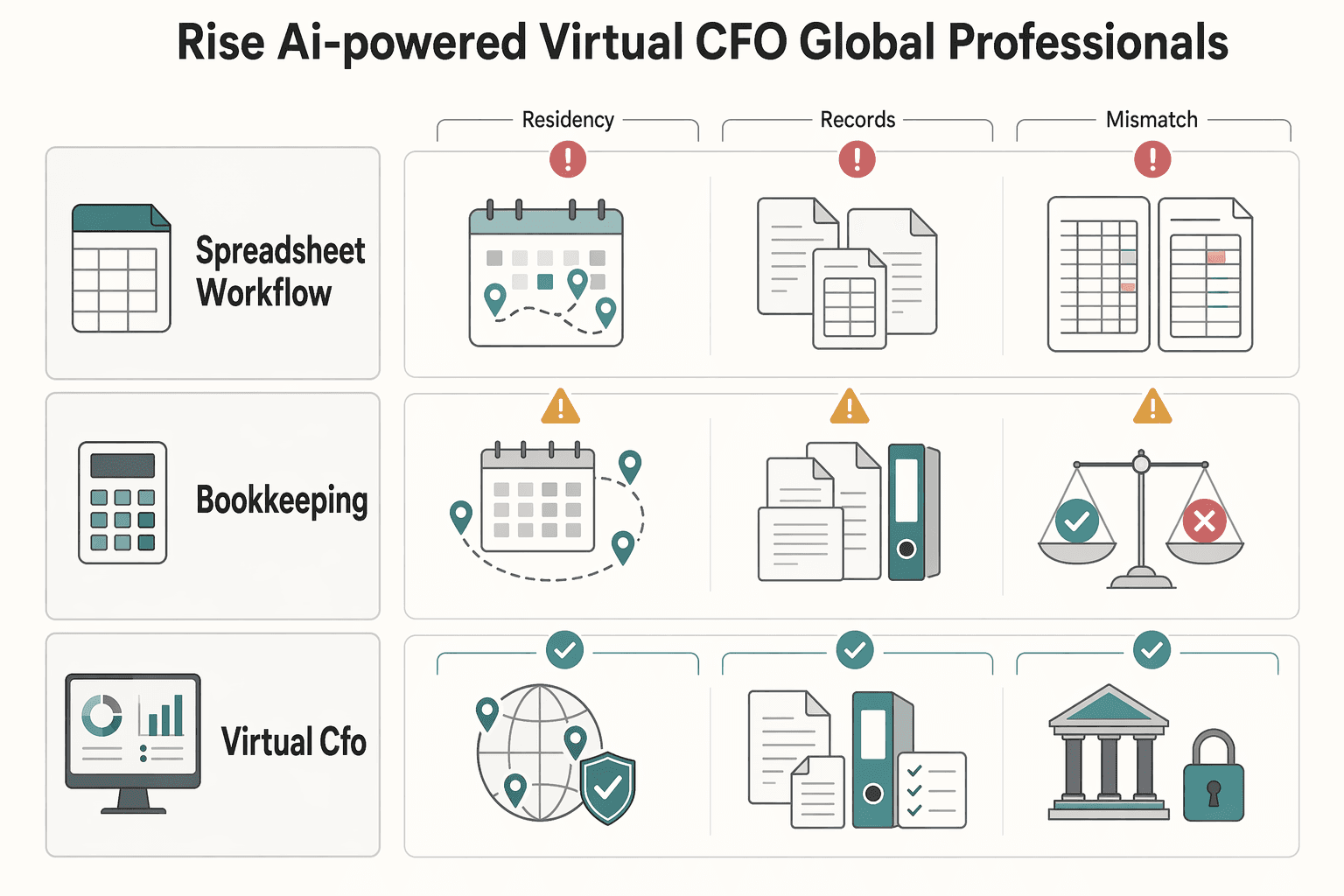

Beyond Spreadsheets: The Rise of the AI-Powered 'Virtual CFO' for Global Professionals#

If you get paid across borders, your core problem is often not basic bookkeeping. It is keeping admin from draining your focus while you stay on top of three risks that spreadsheets often handle poorly: residency tracking, cross-border invoicing compliance, and account-reporting obligations.

Those risks are concrete. U.S. residency tests can hinge on day counts. The Substantial Presence Test includes 31 days in the current year and 183 days across a 3-year period. For EU B2B services, place of taxation is tied to where the customer is established, and invoices are generally required for most B2B supplies. For U.S. persons, FBAR can be triggered when aggregate foreign-account value exceeds $10,000 at any point in the year. The due date is April 15, with an automatic extension to October 15.

This guide is for freelancers, solo operators, and small teams with international clients, cross-border movement, or foreign accounts. It is probably not for you if your setup is domestic-only, single-currency, and already covered well by standard bookkeeping plus periodic accountant review.

| Approach | Scope | Risk coverage | Decision support |

|---|---|---|---|

| Spreadsheet workflow | Manual tracking, custom tabs, ad hoc reminders | Low, depends on what you remember to check | Low, mostly historical and fragmented |

| AI bookkeeping | Bank-feed imports, transaction categorization, reconciliation support | Medium for record hygiene, limited for cross-border rule monitoring | Limited, helps explain what happened |

| AI virtual CFO for freelancers | Adds higher-level guidance, with some tools adding monitoring and alerts | Higher when it tracks the obligations that actually apply to you | Higher, helps decide what to do next |

Use one quick test when comparing tools: do they go beyond auto-import and categorization? Those features are common, and reconciliation still needs manual review for unmatched items. The stronger option connects your financial data to the obligations you actually manage, such as residency day logs, invoicing context, and foreign-account balance tracking over time.

From there, the sequence is straightforward. Automate the foundation, tighten compliance coverage, and then use cleaner data for better growth decisions. The decision lens stays the same throughout: control, compliance reliability, and growth insight.

Related: The 'AI Co-Pilot' for Global Compliance: A Product Vision.

Step 1: Automate the Foundation to Reclaim Your Strategic Mind#

If you want less admin and better decisions, start by automating the bookkeeping work that should stay current every week. The point is not prettier reports. It is spending less time reconstructing the past and more time deciding what to do next.

Bookkeeping includes recording income and expenses, tracking invoices and payments, reconciling bank accounts, preparing reports, and organizing receipts. One 2025 source reports that 72% of U.S. small businesses spend over 10 hours a month on bookkeeping. Use that as a pressure test. If you still need a heavy catch-up session before you trust your numbers, your setup is not automated enough yet.

Use a weekly finance workflow you can verify#

Use a repeatable weekly sequence with visible checks, not full hands-off autonomy.

- Data capture: connect every business cash source, including bank accounts, cards, and payment processors, route invoices through one system, and store receipts with transaction records.

- Classification: let the tool suggest categories, then review exceptions such as new vendors, transfers, refunds, and large or uncategorized items before close.

- Reconciliation: confirm bank activity matches your books and clear duplicates, missing entries, and unmatched items.

- Dashboard visibility: review cash in and out, open invoices, and category spend only after the first three checks are clean.

If you cannot explain this week's cash position quickly, treat the dashboard as incomplete and fix the inputs first.

Make cross-border invoicing consistent and reviewable#

For international clients, keep invoicing consistent and reviewable. Use approved templates instead of drafting each invoice from scratch.

Because rules vary, verify tax and legal wording for each invoice type before sending. If a required field or legal phrase still needs confirmation, mark it as pending official verification until details are validated. If you invoice different buyer types or regions, maintain separate approved templates instead of editing tax wording ad hoc.

Focus on consistency and verification before sending. If key details are uncertain, confirm them before issuing or reissuing an invoice.

Know where AI bookkeeping ends#

Clean books are the base layer. Virtual CFO support starts where recordkeeping stops and judgment begins. AI bookkeeping helps keep records current, while virtual CFO support adds outsourced, remote financial leadership and strategic guidance, including part-time support where needed.

| Decision area | AI bookkeeping | Virtual CFO support |

|---|---|---|

| Automation depth | Strong for routine bookkeeping tasks done frequently in real time | Includes bookkeeping support plus strategic financial guidance |

| Compliance readiness | Useful for cleaner records, but not a replacement for human guidance | Adds human interpretation when finances get more complex |

| Forecasting capability | Focused on keeping records current and reporting-ready | More likely to support cash-flow optimization, financial reporting, and financial modeling |

| Scope limits | May not provide personalized tax-deduction advice unless built for that | Provides strategic guidance, often on an ongoing part-time basis |

| Human review path | Needed as complexity rises | Built for ongoing or part-time strategic review |

If a tool markets automation but gives you no reliable review-and-correction path, treat that as a risk. AI can speed up bookkeeping, but it does not automatically replace human guidance or guarantee personalized tax advice.

Before you move to compliance, make sure the basics are in place. If any of these still break each week, fix them before you add more layers:

- Connect all business cash accounts and payment rails in one bookkeeping workflow.

- Use consistent invoice templates, with any unverified legal or tax wording clearly marked as pending official verification.

- Configure category rules, then review exceptions weekly.

- Run a weekly cycle for capture, classification, reconciliation, and dashboard checks, with human accountant review when complexity increases.

You might also find this useful: The Best Virtual Phone Number Services for Freelancers.

Step 2: Build Your Compliance Fortress - The Non-Negotiable Shield Against Catastrophic Risk#

Once your books are current, the next priority is controlling avoidable compliance mistakes before they turn into payment delays, filing issues, or audit friction. The compliance layer should do three things well: track what is knowable, flag what is uncertain, and hand off cleanly when advisor judgment is required.

Turn residency into tracked inputs, rule logic, alerts, and evidence#

Residency risk is manageable when you treat it as a tracked process, not something you reconstruct from memory. Use one operating record with four parts: input capture, rule logic, alerting, and audit-trail output.

| Control part | Article details |

|---|---|

| Input capture | Record arrival and departure dates, jurisdiction, trip purpose, relevant client or entity tie, and supporting records such as tickets, passport stamps, accommodation invoices, and calendar entries. |

| Provisional counts | If a day count cannot be traced to source records, treat it as provisional. |

| Rule logic | Apply verified jurisdiction rules to those inputs. Where a rule is not confirmed by a current primary source or advisor, mark it as current rule pending official verification. One sourced anchor is the U.S. substantial presence test: 31 days in the current year and an 183-day test across the weighted 3-year period, with some days excluded by rule. |

| Alerts and output | Set alerts before review points, not after a threshold is crossed. Output should show the rule version used, excluded days, and attached trip evidence so advisor review is fast and defensible. |

Capture the same inputs every time. Record arrival and departure dates, jurisdiction, trip purpose, relevant client or entity tie, and supporting records such as tickets, passport stamps, accommodation invoices, and calendar entries. If a day count cannot be traced to source records, treat it as provisional.

Apply verified jurisdiction rules to those inputs only after confirming them against a current primary source or advisor. Until then, mark the rule as pending official verification. One sourced anchor is the U.S. substantial presence test. It uses day-count logic across a 3-year window. That includes 31 days in the current year and an 183-day test across the weighted 3-year period, with some days excluded by rule.

Set alerts before review points, not after a threshold is crossed. Your output should show the rule version used, excluded days, and attached trip evidence so advisor review is fast and defensible.

Put every cross-border invoice through one control flow#

Cross-border invoice errors are usually control failures. A fixed workflow is safer than ad hoc edits.

| Step | What to do | If there is an issue |

|---|---|---|

| Validate buyer tax status | Confirm buyer type, collect registration details, and where relevant check VAT registration in VIES before issuing the invoice. | Treat failed validation as an exception for review, not an automatic tax conclusion. |

| Check required fields | Include seller entity details, buyer billing details, invoice date, invoice number, service description, currency, payment terms, and stated tax treatment. | Under EU rules, an invoice is required for most B2B supplies. |

| Apply reverse-charge handling only when verified | For many EU cross-border B2B service cases, sellers usually do not charge VAT and the customer accounts for VAT under reverse charge. | In covered cases where the customer is liable for VAT, include the words "Reverse charge." |

| Escalate exceptions | If buyer status is unclear, VAT validation fails, or the transaction type is unusual, hold issuance. | Route it to manual review with the evidence attached. |

Keep separate approved templates by transaction pattern and jurisdiction logic. Do not treat one global template as universally valid.

Monitor thresholds continuously and predefine escalation#

Compliance monitoring is strongest when aggregation, normalization, threshold watch, and handoff are defined before deadlines hit. FBAR, FinCEN Form 114, is a concrete example.

| FBAR item | Article detail |

|---|---|

| Trigger | U.S. persons report qualifying foreign financial accounts when aggregate value exceeds $10,000 at any time during the calendar year. |

| Due date | April 15, with an automatic extension to October 15. |

| Record retention | Records are generally kept for 5 years from the FBAR due date. |

| Filing method | Filing is e-file because obsolete or printed paper forms are not accepted. |

| Monitoring design | Design monitoring so all relevant accounts are aggregated, balances are normalized consistently, and threshold alerts are watched. |

| Handoff pack | Include an account list, highest known balances, conversion method used, statement files, ownership notes, and a filing calendar draft. |

U.S. persons report qualifying foreign financial accounts when aggregate value exceeds $10,000 at any time during the calendar year. The due date is April 15, with an automatic extension to October 15. Records are generally kept for 5 years from the FBAR due date, and filing is e-file because obsolete or printed paper forms are not accepted.

Design your monitoring so all relevant accounts are aggregated, balances are normalized consistently, and threshold alerts are watched. For jurisdiction-specific logic, keep threshold values and escalation language marked as pending official verification until confirmed by current official guidance or advisor review.

When an alert fires, the handoff pack should include an account list, highest known balances, conversion method used, statement files, ownership notes, and a filing calendar draft. If detection exists but exportable evidence does not, the control is incomplete.

| Approach | Detection speed | False-negative risk | Evidence readiness for audits |

|---|---|---|---|

| Manual process | Variable; depends on reminders and manual checks | Can be high if logs, account coverage, and invoice review are inconsistent | Depends on deliberate recordkeeping |

| Basic bookkeeping tool | Variable; depends on configured rules and exception workflows | Can remain material if jurisdiction logic and escalation routing are incomplete | Can be partial if support files and rule history are kept outside the tool |

| AI virtual CFO compliance layer | Variable; depends on validated rules, review gates, and document capture | Can remain material without jurisdiction verification and advisor-review handoffs | Can be audit-ready when alerts, rule versions, validation outcomes, and handoff files are stored together |

In practical terms, if you are deciding where to invest first, fund monitoring and evidence controls before advanced forecasting.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

Before you commit to any platform, run a quick compliance baseline for your travel pattern and filing exposure with the Tax Residency Tracker.

Step 3: Activate Your Growth Engine with a True AI Co-Pilot#

If your operating data is clean and reviewable, the next move is to turn that data into decisions you can act on now. The practical test of an AI co-pilot is simple: does it help you decide what to prioritize, what to keep, what to cut, and what you can fund with confidence?

Turn forecasts into a planning loop#

A practical forecasting loop starts with traceable inputs, tests assumptions, and runs scenarios on a repeatable cadence. Pull from committed revenue, likely pipeline, known obligations, and planned costs, and label each input by confidence. If an input is uncertain, mark it as provisional and keep it out of your committed-cash view.

Before you trust the output, pressure-test these assumptions:

- Are payment dates based on contract terms or actual client behavior?

- Did you include irregular and annual costs, not just monthly averages?

- Are you counting pipeline revenue before approvals or signed scope?

Run two views each cycle:

- Near-term cash outlook for obligations already forming

- Medium-term cash outlook for choices you can still shape

Use scenario toggles for expected, slower, and faster payment timing, plus cost changes you are considering. Keep an assumption log with date, source, and owner so you can tell whether performance changed or your estimate did.

AI should support this loop, not replace your judgment. GrowthPad describes growth work as moving toward "AI-augmented systems" focused on "Sustainable, measurable growth" across acquisition, retention, and monetization. In practice, use the tool to improve decisions in those three areas, not just summarize past activity.

Judge clients by profit, not revenue#

Client decisions should come from total economics, not top-line billing alone. Break each client or project into four parts:

- Revenue: contracted value, add-ons, discounting, and payment reliability

- Delivery effort: production time, revisions, rework, and subcontracting

- Support burden: meetings, updates, admin follow-up, and exception handling

- Operational overhead: invoicing complexity, approvals, and recurring admin effort

Then tie that profile to an action:

- Strong revenue with manageable effort and support: retain

- Strong revenue with heavy support or rework: reprice or reset scope

- Weak revenue with recurring friction or slow collections: exit candidate

- Marginal outcome that depends on best-case execution: high risk, redesign or decline

Close each cycle by comparing estimated effort with actual effort, including non-billable time. If that gap keeps showing up, pricing or scope control may be off.

Choose the right level of finance tooling#

Pick the operating approach before you pick a product. A risk is selecting tooling that does not match your actual workflow.

| Option | Best fit | Capability focus | Implementation effort | Cost framing |

|---|---|---|---|---|

| Lightweight finance stack | You mainly need clear records and visibility | Core bookkeeping and reporting | Varies | Include subscription and manual analysis time |

| Broader finance platform | You need cross-functional planning and reporting | Expanded planning and operations | Varies | Include onboarding and ongoing operating effort |

| AI-assisted advisory workflow | You need faster planning and decision support with human review | Scenario support and synthesis | Varies | Include tool spend, advisor time, and decision-risk tradeoffs |

Model decisions before you commit cash#

Run scenarios before decisions that add fixed cost, shift capacity, or change pricing power. Typical cases include hiring support, adding tooling, or changing your client mix.

Before you act, validate a few basics:

- Which single assumption drives the outcome most?

- Which costs stay fixed if revenue slips?

- What evidence supports the revenue side today?

- What happens if payments land later than planned?

- Does this improve acquisition, retention, or monetization, or just add activity?

Keep the objective measurable and grounded in margin and cash resilience. AI can increase output, but outcomes can still be uneven if pricing discipline and client selection stay weak.

For related context, see A Guide to Foreign Exchange (Forex) Risk for Freelancers.

Conclusion: You Are the CEO. It's Time You Had the Co-Pilot.#

Choose tool depth based on your bottleneck: automate the foundation first, secure compliance risk second, then add forecasting and planning.

Start by fixing the foundation. Connect your bank accounts and confirm you get a live view of cash, income, and expenses. You should not spend the first week of each month looking backward and recategorizing. If the trial still feels like manual reconciliation in a cleaner UI, you may be getting bookkeeping, not a real decision system.

Then test the risk layer. For global operators, common pressure points include the unknowns around tax residency, invoice defects that delay payment, and filing mistakes that can carry real downside. A single missing VAT detail can stall payment. Ask the platform to show what triggered each warning, what data it used, and what record you can retain. If AI is moving data between systems, confirm there are guardrails on what it can change automatically.

Use this decision lens: AI bookkeeping may be enough when you mainly need accurate records, reconciliations, and historical reporting. You may need a virtual CFO workflow when you also need cross-border risk visibility and forward-looking planning support. Before you choose, verify these in a live trial:

- Direct bank connections that create live visibility, not just month-end cleanup

- Clear warning trails for your highest cross-border risks, with records you can keep

- At least one forward-looking output built from your own data, such as a cash forecast or scenario view

- Guardrails for any automated data movement between tools

- A clear correction path when an invoice, residency count, or filing flag is wrong

For a step-by-step walkthrough, see The FIRE Movement for Freelancers Who Need Reliable Cashflow.

If you want a practical shortlist before making a switch, use Gruv's freelancer tools hub to compare workflows and pressure-test your setup.

Frequently Asked Questions

Do you need residency tracking, or is a travel spreadsheet enough?

If your tax position can change based on day counts, use more than a raw travel spreadsheet. Your method should apply the substantial-presence thresholds of 31 days in the current year and 183 days across the 3-year test, account for excluded days where the rules permit, and keep a usable day-count record with your travel documents. Before you buy, confirm you can review date entries and retain the record.

Should you rely on alerts for FBAR reporting?

Use alerts for monitoring, not as a substitute for review. They should track aggregate foreign-account balances against the FBAR trigger and not rely on month-end snapshots alone. You still need to file FinCEN Form 114 when required, follow the April 15 timeline with automatic extension to October 15, and retain records for generally five years from the due date. Missing required filings can carry civil and criminal penalties.

Do you need AI bookkeeping or an AI virtual CFO for freelancers?

It depends on whether your bottleneck is recordkeeping or decision-making. If you mainly need accurate transaction records, reconciliations, and historical reporting, AI bookkeeping may be enough. If you need cash forecasting, scenario changes, client-level profitability, and forward decisions, you need CFO-like capability. Before you buy, ask for a live demo built from real data.

How should you judge a startup-focused platform if you work alone?

Judge it by workflow fit, not startup branding. Verify whether the tool assumes payroll, department reporting, or multi-user approvals you do not need, and confirm current plan pricing directly. The right choice should match your headcount, entity setup, jurisdictions, and reporting obligations.

What should an EU VAT invoicing tool actually do?

Judge an EU VAT invoicing tool transaction by transaction, not by one global template. For B2B supplies, invoicing is generally required, and where the customer is VAT-liable the invoice should include a reverse-charge mention. Where invoicing is required, the supplier VAT ID should appear, and the tool should let you validate the counterparty VAT number in VIES and record the check result and date.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bls.gov/ooh/Office-and-Administrative-Support/Bookke...trusted

- bls.gov/ooh/management/financial-managers.htmtrusted

- elon.edu/u/imagining/surveys/vi-2014/2025-internet-ai...trusted

- eur-lex.europa.eu/EN/legal-content/summary/micro-small-and-med...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- hbs.edu/coursecatalog/print.htmltrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

How Solo Professionals Can Use an AI Compliance Co-Pilot

If you run a cross-border business on your own, you are managing growth and compliance at the same time. In practice, that means keeping four risk areas aligned with your actual records:

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.